|

市场调查报告书

商品编码

1797779

发酵槽和陈化设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Fermenters and Aging Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

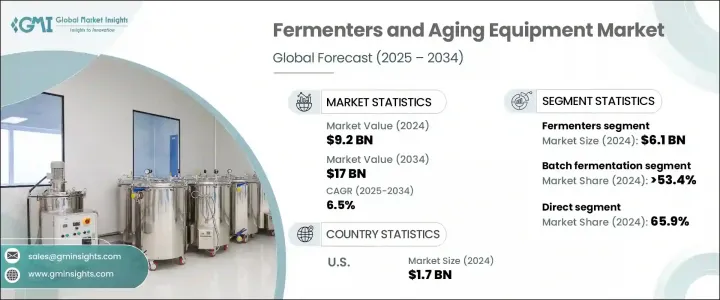

2024年,全球发酵槽和陈化设备市场规模达92亿美元,预计2034年将以6.5%的复合年增长率成长,达到170亿美元。这一市场成长主要得益于依赖发酵和陈化製程的多个行业日益增长的需求。对尖端发酵系统的需求正在不断增长,这主要得益于生物製药领域的进步,该领域对生物製剂、单株抗体和疫苗的需求日益增长。全球医疗保健投资的不断增长以及慢性病盛行率的激增,促使人们进一步关注高效、无污染的发酵过程。

自动化系统和一次性发酵槽等技术的采用简化了操作流程,并提高了生产效率。此外,由于高品质天然加工产品的普及,食品饮料产业持续推动发酵设备的成长。对永续性和天然食品加工的兴趣是另一个重要的催化剂,它推动着发酵和发酵技术在各种生产设施中的整合。亚太地区等新兴经济体也发挥关键作用,这得益于其工业化程度的提高和基础设施的改善,这些因素支持了现代发酵技术的部署。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 92亿美元 |

| 预测值 | 170亿美元 |

| 复合年增长率 | 6.5% |

发酵槽因其在多个垂直行业的广泛应用,继续占据整个市场的主导地位。这些系统在培养微生物和细胞培养物方面发挥着至关重要的作用,而这些微生物和细胞培养物对于生产生物製剂、酵素、治疗化合物和发酵食品至关重要。与通常应用范围较为有限的老化设备相比,它们的应用范围要广泛得多。随着对精准驱动和可扩展生产的需求日益增长,製造商正在积极投资开发下一代发酵槽。这些系统融合了增强监控、自动化和抗污染等特性。透过提高效率和适应性,这些创新使生产商能够更轻鬆地快速回应市场需求,尤其是在产品一致性和纯度至关重要的行业。

2024年,批量发酵领域占据53.4%的市场份额,预计到2034年将以7.3%的复合年增长率成长。由于操作简便、适应性广,这种发酵方法在生物製药和食品行业中仍然是最受欢迎的。批量处理允许在受控环境中添加、加工和移除原料,为各种产品类别提供了简单易行的理想设定。该技术尤其适用于中小规模生产,因为这些生产对精度、灵活性和清洁度至关重要。它支援需要精细监控的高价值产品的生产,而无需像连续或大规模操作那样复杂。

美国发酵槽和陈年设备市场占67.7%的市场份额,2024年产值达17亿美元。美国市场主导地位源自于其先进的製药生产格局、先进的研发设施和强大的供应商网路。快速发展的生物製剂和个人化疗法市场,正激发大型製造商和合约开发机构对更先进发酵解决方案的兴趣。美国持续受益于公共和私营部门旨在提高製药产量和创新的持续投资。

包括赛默飞世尔科技、阿法拉伐、赛多利斯、默克(MilliporeSigma)和基伊埃集团在内的主要市场参与者正积极透过策略性措施塑造竞争格局。这些公司优先考虑研发,以推出更智慧、模组化和可扩展的系统,以满足生物加工和食品产业不断变化的需求。他们也透过区域製造中心、在地化服务中心和策略性收购扩大全球影响力。与学术机构和生物製药公司的合作有助于这些参与者在市场变化中保持领先地位,并快速测试和部署新技术。透过提升产品性能、提高自动化程度并提供整合的数位解决方案,这些公司正在巩固其市场地位,并满足市场对灵活高效加工技术的需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 生物製药需求不断成长

- 食品饮料业的成长

- 技术进步

- 产业陷阱与挑战

- 高资本投入

- 操作和维护的复杂性

- 机会

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依设备类型

- 监管格局

- 标准和合规要求

- 区域监理框架

- 认证标准

- 贸易统计(HS 编码 - 84199090)

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依设备类型,2021 - 2034 年

- 主要趋势

- 发酵槽

- 潜水发酵槽(例如搅拌槽)

- 固态发酵罐

- 厌氧发酵罐

- 有氧发酵罐

- 老化设备

- 陈年罐(例如不锈钢、橡木、塑胶)

- 酒桶(例如橡木桶、混合桶)

- 装瓶与二次陈酿系统

- 酒窖陈酿单元

第六章:市场估计与预测:按运营,2021 - 2034 年

- 主要趋势

- 大量发酵

- 补料分批发酵

- 连续发酵

第七章:市场估计与预测:依建筑材料,2021 - 2034 年

- 主要趋势

- 不銹钢

- 玻璃

- 塑胶/聚合物

- 混凝土(用于葡萄酒/苹果酒陈酿)

- 木材(主要用于陈年)

第八章:市场估计与预测:依自动化水平,2021 - 2034 年

- 主要趋势

- 手动的

- 半自动

- 全自动

第九章:市场估计与预测:按应用 2021 - 2034

- 主要趋势

- 食品和饮料

- 製药

- 生物技术

- 营养保健品

- 化妆品和个人护理

第十章:市场估计与预测:按配销通路2021 - 2034

- 主要趋势

- 直接的

- 间接

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十二章:公司简介

- Alfa Laval

- Applikon Biotechnology

- Bioengineering

- Bucher Vaslin

- Danaher Corporation

- Eppendorf

- GEA Group

- Merck

- Paul Mueller Company

- Sartorius

- STS Canada

- Tetra Pak

- Thermo Fisher Scientific

- Ziemann Holvrieka

- JVNW

The Global Fermenters and Aging Equipment Market was valued at USD 9.2 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 17 billion by 2034. This market growth is fueled by the increasing demand across multiple industries that rely on fermentation and aging processes. The need for cutting-edge fermentation systems is rising, driven largely by advancements in the biopharmaceutical sector, where biologics, monoclonal antibodies, and vaccines are seeing heightened demand. Growing investments in healthcare globally and a surge in chronic disease prevalence are prompting further focus on efficient and contamination-free fermentation processes.

The adoption of technologies such as automated systems and single-use fermenters has streamlined operations and improved production outcomes. Alongside, the food and beverage industry continue to push growth in aging equipment, thanks to the popularity of high-quality, naturally processed products. Interest in sustainability and natural food processing is another major catalyst, encouraging the integration of both fermentation and aging technologies across various manufacturing setups. Emerging economies in regions such as APAC are also playing a key role due to increased industrialization and infrastructure improvements that support the deployment of modern fermentation technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.2 Billion |

| Forecast Value | $17 Billion |

| CAGR | 6.5% |

Fermenters continue to dominate the overall market, owing to their wide-ranging usage across several industrial verticals. These systems play a crucial role in cultivating microorganisms and cell cultures essential for producing biologics, enzymes, therapeutic compounds, and fermented food items. Their applications are far more extensive when compared to aging equipment, which is generally more limited in scope. As demand for precision-driven and scalable production intensifies, manufacturers are actively investing in the development of next-generation fermenters. These systems incorporate features such as enhanced monitoring, automation, and contamination resistance. By enabling higher efficiency and adaptability, these innovations are making it easier for producers to respond quickly to market needs, especially in sectors where product consistency and purity are critical.

In 2024, the batch fermentation segment held a 53.4% share and is projected to grow at a CAGR of 7.3% through 2034. This fermentation method remains the most preferred across both biopharma and food industries because of its operational simplicity and broad adaptability. Batch processing allows ingredients to be added, processed, and removed in a controlled environment, offering a straightforward setup ideal for a variety of product categories. This technique is particularly well-suited to small- to medium-scale production runs, where precision, flexibility, and clean processing are paramount. It supports the manufacturing of high-value products that require detailed oversight without the complications of continuous or large-scale operations.

United States Fermenters and Aging Equipment Market held a 67.7% share and generated USD 1.7 billion in 2024. The country's dominance stems from its advanced pharmaceutical manufacturing landscape, sophisticated research facilities, and strong supplier networks. A rapidly evolving market for biologics and personalized therapies is fueling interest in more advanced fermentation solutions across both large-scale manufacturers and contract development organizations. The US continues to benefit from sustained public and private sector investments aimed at improving pharmaceutical output and innovation.

Key market players, including Thermo Fisher Scientific, Alfa Laval AB, Sartorius AG, Merck KGaA (MilliporeSigma), and GEA Group AG, are actively shaping the competitive landscape through strategic efforts. These firms are prioritizing research and development to introduce smarter, modular, and scalable systems that meet the evolving needs of bioprocessing and food industries. They are also expanding their global footprint through regional manufacturing hubs, localized service centers, and strategic acquisitions. Partnerships with academic institutions and biopharma companies help these players stay ahead of market shifts and rapidly test and deploy new technologies. By enhancing product performance, increasing automation, and offering integrated digital solutions, these companies are solidifying their market positions and responding to the demand for flexible and efficient processing technologies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.3 Data collection methods

- 1.4 Data mining sources

- 1.4.1 Global

- 1.4.2 Regional/Country

- 1.5 Base estimates and calculations

- 1.5.1 Base year calculation

- 1.5.2 Key trends for market estimation

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment Type

- 2.2.3 Operation

- 2.2.4 Automation Level

- 2.2.5 Material for construction

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.4 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for biopharmaceuticals

- 3.2.1.2 Growth of food & beverage industry

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital investment

- 3.2.2.2 Complexity of operation and maintenance

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code - 84199090)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Fermenters

- 5.2.1 Submerged fermenters (e.g., stirred tank)

- 5.2.2 Solid-state fermenters

- 5.2.3 Anaerobic fermenters

- 5.2.4 Aerobic fermenters

- 5.3 Aging Equipment

- 5.3.1 Aging tanks (e.g., stainless steel, oak, plastic)

- 5.3.2 Barrels (e.g., oak barrels, hybrid barrels)

- 5.3.3 Bottling and secondary aging systems

- 5.3.4 Cellar aging units

Chapter 6 Market Estimates & Forecast, By Operation, 2021 - 2034 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Batch fermentation

- 6.3 Fed-batch fermentation

- 6.4 Continuous fermentation

Chapter 7 Market Estimates & Forecast, By Material of Construction, 2021 - 2034 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Stainless steel

- 7.3 Glass

- 7.4 Plastic/polymer

- 7.5 Concrete (for wine/cider aging)

- 7.6 Wood (primarily for aging)

Chapter 8 Market Estimates & Forecast, By Automation Level, 2021 - 2034 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Manual

- 8.3 Semi-automatic

- 8.4 Fully automatic

Chapter 9 Market Estimates & Forecast, By Application 2021 - 2034 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Food & beverage

- 9.3 Pharmaceuticals

- 9.4 Biotechnology

- 9.5 Nutraceuticals

- 9.6 Cosmetics & personal care

Chapter 10 Market Estimates & Forecast, By Distribution Channel 2021 - 2034 ($ Bn, Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Alfa Laval

- 12.2 Applikon Biotechnology

- 12.3 Bioengineering

- 12.4 Bucher Vaslin

- 12.5 Danaher Corporation

- 12.6 Eppendorf

- 12.7 GEA Group

- 12.8 Merck

- 12.9 Paul Mueller Company

- 12.10 Sartorius

- 12.11 STS Canada

- 12.12 Tetra Pak

- 12.13 Thermo Fisher Scientific

- 12.14 Ziemann Holvrieka

- 12.15 JVNW