|

市场调查报告书

商品编码

1797851

煞车卡钳市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Brake Caliper Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

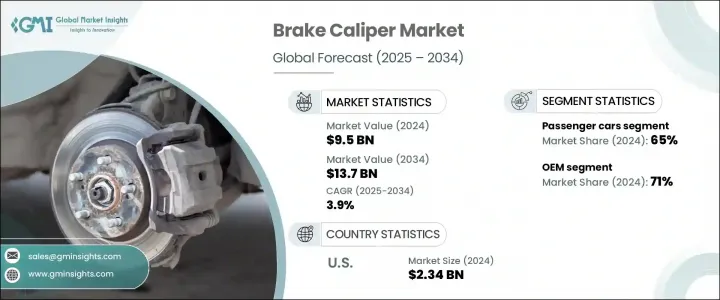

2024 年全球煞车卡钳市场价值为 95 亿美元,预计到 2034 年将以 3.9% 的复合年增长率成长至 137 亿美元。受电气化等汽车技术发展、高级驾驶辅助系统 (ADAS) 的成长以及对轻量化零件的需求推动,该市场正在经历快速转型。随着行动解决方案向电动车和智慧汽车架构转变,煞车卡钳已发展成为复杂、精密的零件,远远超出了其传统的液压作用。机电煞车系统和铝製煞车卡钳等技术创新,加上内建感测器,在重塑乘用车和电动两轮车的煞车应用方面发挥重要作用。汽车产量的反弹,尤其是在亚太地区,进一步增强了OEM和售后市场管道的需求。

随着汽车电气化进程的加速,汽车製造商优先考虑使用阻力较小的卡钳,以便与电子煞车系统配合使用。製造商正透过设计适用于各种车辆架构的模组化标准化卡钳平台来顺应这一转变。爱信、博世、万都株式会社和布雷博等一级供应商正在与全球汽车製造商建立长期联盟,共同设计符合区域市场需求、经济高效且安全合规的卡钳。从传统铸铁零件到轻量化铝製卡钳的过渡,在高性能和大众市场车型中持续受到关注。随着原始设备製造商专注于车辆减重策略以满足更严格的碳排放和燃油效率目标,这项转型在2020年开始加速。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 95亿美元 |

| 预测值 | 137亿美元 |

| 复合年增长率 | 3.9% |

乘用车领域占了65%的市场份额,预计到2034年将以4%的复合年增长率成长。随着汽车製造商寻求兼顾性能、效率和先进的煞车能力,中型和豪华乘用车正在引领铝製和电子卡钳的采用。在整个乘用车领域,汽车製造商越来越多地将多活塞铝製卡钳和电子驻车煞车集成为轿车和跨界车型的标准配备。该领域持续向智慧轻量化零件转型,正在推动全球市场的需求成长。

原始设备製造商 (OEM) 在煞车卡钳市场保持强势地位,2024 年市占率达 71%,预计到 2034 年将以 3% 的复合年增长率成长。 OEM 凭藉其高度整合的方案以及与煞车系统领导者(包括采埃孚 (ZF)、曙光煞车株式会社 (Akebono Brake Corporation)、大陆集团 (Continental) 和爱信精机 (Aisin))的策略合作,继续主导价值链。电气化趋势正推动 OEM 与这些一级供应商紧密合作,开发兼容再生煞车的卡钳、轻量化合金变体以及先进的整合式电子驻车煞车 (EPB)。随着 OEM 越来越多地转向可扩展的、以电动为中心的车辆平台,预计到 2030 年,对精密设计且符合法规要求的卡钳的需求将大幅增长。

2024年,美国煞车卡钳市场占87%的市场份额,产值达23.4亿美元。美国各生产中心汽车製造业的强劲成长推动了煞车卡钳市场的需求,这些中心主要生产大量的SUV、跨界车和皮卡。这些车型对煞车系统的结构性要求很高,因此需要更多整合耐用的铝製前后煞车卡钳组件,以满足联邦燃油经济性和车辆动力学标准。在福特和通用等主要厂商的支持下,美国本土汽车生态系统正在加速优化煞车解决方案的需求。

万都株式会社、爱信精机、大陆集团、布雷博、博世、曙光煞车株式会社和采埃孚等领先製造商持续塑造着全球煞车卡钳产业的格局。煞车卡钳领域的顶尖企业正透过与汽车原始设备製造商建立策略合作伙伴关係,共同开发符合不断发展的平台需求的尖端煞车技术,从而提升其市场占有率。製造商正大力投资研发更轻、更耐用的铝製煞车卡钳以及相容电动传动系统的系统。区域生产扩张、经济高效的平臺本地化以及将智慧感测器整合到煞车卡钳设计中,正在帮助供应商满足全球监管标准,同时满足当地市场的特定需求。各公司也专注于模组化产品平台,以简化跨多种车型的生产流程,降低复杂性并提高可扩展性。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 对车辆安全合规性的需求不断增长

- 两轮车从鼓式煞车改为碟式煞车

- SUV 和高性能汽车销售成长

- 轻量化车辆要求

- 车辆电气化

- 产业陷阱与挑战

- 原料成本上涨

- 售后市场分散,仿冒品成本低廉

- 市场机会

- 基于整合感测器的卡尺

- 电动车专用煞车系统

- 拓展东协和非洲市场

- 售后客製化和性能调整

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 生产统计

- 生产中心

- 消费中心

- 汇出和汇入

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:Caliper,2021 - 2034 年

- 主要趋势

- 固定的

- 漂浮的

第六章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商用车

- 轻型

- 中型

- 重负

- 两轮车

- 摩托车

- 踏板车

第七章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第八章:市场估计与预测:按燃料,2021 - 2034 年

- 主要趋势

- 汽油

- 柴油引擎

- 全电动

- 杂交种

- 燃料电池汽车

第九章:市场估计与预测:依资料,2021 - 2034 年

- 主要趋势

- 铝

- 钢

- 钛

- 酚类物质

第 10 章:市场估计与预测:按製造工艺,2021 年至 2034 年

- 主要趋势

- 高压压铸

- 重力压铸

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- Global companies

- Technology and innovation companies

- Racing and performing specialist companies

- Two-wheeler companies

- Technology-focused companies

The Global Brake Caliper Market was valued at USD 9.5 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 13.7 billion by 2034. The market is undergoing rapid transformation, driven by evolving automotive technologies such as electrification, the growth of advanced driver-assistance systems (ADAS), and demand for lightweight components. As mobility solutions shift toward electric vehicles and smart vehicle architectures, brake calipers have evolved into intricate, precision-engineered components far beyond their traditional hydraulic role. Technological innovations like electromechanical braking systems and calipers made from aluminum, combined with built-in sensors, play a major role in reshaping braking applications across passenger cars and electric two-wheelers. The rebound of vehicle production, particularly in Asia-Pacific region, has further strengthened demand across both OEM and aftermarket channels.

As vehicle electrification accelerates, automakers are prioritizing calipers with lower drag for use with electronic braking systems. Manufacturers are aligning with this shift by designing modular, standardized caliper platforms suitable for various vehicle architectures. Tier-1 suppliers such as Aisin, Bosch, Mando Corporation, and Brembo are forming long-term alliances with global carmakers to co-engineer cost-efficient, safety-compliant calipers tailored to regional market needs. The transition from traditional cast iron components to lightweight aluminum calipers continues gaining traction across both performance and mass-market vehicle lines. The movement began gaining pace in 2020 as OEMs focused on vehicle weight reduction strategies to meet stricter carbon emission and fuel efficiency targets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.5 Billion |

| Forecast Value | $13.7 Billion |

| CAGR | 3.9% |

The Passenger vehicles segment held a 65% share and is forecast to grow at a CAGR of 4% through 2034. Mid-size and luxury passenger vehicles are spearheading the adoption of aluminum and electronic calipers as OEMs seek to combine performance, efficiency, and advanced braking capabilities. Across the passenger vehicle landscape, automakers are increasingly integrating multi-piston aluminum calipers and electric parking brakes as standard features across sedans and crossover models. This segment's continuous shift toward smart, lightweight components is driving demand growth across global markets.

The Original equipment manufacturers maintained their stronghold in the brake caliper market with a 71% share in 2024 and are projected to grow at 3% CAGR through 2034. OEMs continue to dominate the value chain with their integration-heavy approach and strategic collaborations with brake system leaders, including ZF, Akebono Brake Corporation, Continental, and Aisin. Electrification trends are pushing OEMs to work closely with these Tier-1 suppliers to develop regenerative braking-compatible calipers, lightweight alloy variants, and advanced integrated EPBs. As OEMs increasingly transition to scalable, electric-centric vehicle platforms, the need for precision-engineered and regulatory-compliant calipers is expected to rise significantly toward 2030.

United States Brake Caliper Market held 87% share in 2024, generating USD 2.34 billion. The country's demand is propelled by strong automotive manufacturing activity across production hubs, where high volumes of SUVs, crossovers, and pickups are built. These vehicle segments place high structural demands on braking systems, which is leading to increased integration of durable front and rear caliper units made from aluminum to meet federal fuel economy and vehicle dynamics standards. The local automotive ecosystem, supported by key players such as Ford and GM, is accelerating demand for optimized braking solutions.

Leading manufacturers, including Mando Corporation, Aisin, Continental, Brembo, Bosch, Akebono Brake Corporation, and ZF, continue to shape the global landscape of the brake caliper industry. Top players in the brake caliper space are advancing their market presence through strategic partnerships with automotive OEMs to co-develop cutting-edge braking technologies aligned with evolving platform requirements. Manufacturers are heavily investing in R&D to develop lighter, more durable aluminum calipers and systems compatible with electric drivetrains. Regional production expansion, cost-effective platform localization, and integration of smart sensors into caliper designs are helping suppliers meet global regulatory standards while catering to the specific needs of local markets. Companies are also focusing on modular product platforms to streamline production across multiple vehicle classes, reducing complexity and enhancing scalability.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Caliper

- 2.2.3 Vehicle

- 2.2.4 Sales Channel

- 2.2.5 Fuel

- 2.2.6 Material

- 2.2.7 Manufacturing Process

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for vehicle safety compliance

- 3.2.1.2 Shift from drum to disc brakes in two-wheelers

- 3.2.1.3 Increasing SUV and performance vehicle sales

- 3.2.1.4 Lightweight vehicle mandates

- 3.2.1.5 Electrification of vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising raw material costs

- 3.2.2.2 Fragmented aftermarket and low-cost counterfeits

- 3.2.3 Market opportunities

- 3.2.3.1 Integrated sensor-based calipers

- 3.2.3.2 EV-exclusive braking systems

- 3.2.3.3 Expansion in ASEAN and African markets

- 3.2.3.4 Aftermarket customization and performance tuning

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Caliper, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Fixed

- 5.3 Floating

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicle

- 6.3.1 Light-duty

- 6.3.2 Medium-duty

- 6.3.3 Heavy-duty

- 6.4 Two-wheeler

- 6.4.1 Motorcycle

- 6.4.2 Scooters

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Gasoline

- 8.3 Diesel

- 8.4 All-electric

- 8.5 Hybrid

- 8.6 FCEV

Chapter 9 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Aluminum

- 9.3 Steel

- 9.4 Titanium

- 9.5 Phenolics

Chapter 10 Market Estimates & Forecast, By Manufacturing Process, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 High Pressure Die Casting

- 10.3 Gravity Die Casting

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Brembo

- 12.1.2 Continental

- 12.1.3 Akebono Brake Industry

- 12.1.4 ZF

- 12.1.5 Aisin Seiki

- 12.2 Technology and innovation companies

- 12.2.1 Robert Bosch

- 12.2.2 Nissin Kogyo

- 12.2.3 Knorr-Bremse

- 12.3 Racing and performing specialist companies

- 12.3.1 Wilwood Engineering

- 12.3.2 AP Racing

- 12.3.3 Alcon Components

- 12.3.4 StopTech (Centric Parts)

- 12.3.5 Regional companies

- 12.3.6 Mando

- 12.3.7 Chassis Brakes International (CBI)

- 12.3.8 Wanxiang Qianchao

- 12.4 Two-wheeler companies

- 12.4.1 Tokico

- 12.4.2 Galfer

- 12.5 Technology-focused companies

- 12.5.1 BWI Group

- 12.5.2 Haldex

汽车煞车卡钳市场:按车辆类型、产品类型、材质、应用和销售管道划分-2026-2032年全球预测固定式煞车卡钳市场:按车辆类型、活塞类型、材质、驱动方式、应用和销售管道划分-2026-2032年全球预测

汽车煞车卡钳市场:按车辆类型、产品类型、材质、应用和销售管道划分-2026-2032年全球预测固定式煞车卡钳市场:按车辆类型、活塞类型、材质、驱动方式、应用和销售管道划分-2026-2032年全球预测 汽车煞车卡钳市场-全球产业规模、份额、趋势、机会和预测,按车辆类型、产品类型、销售管道、地区和竞争格局划分,2020-2030年预测

汽车煞车卡钳市场-全球产业规模、份额、趋势、机会和预测,按车辆类型、产品类型、销售管道、地区和竞争格局划分,2020-2030年预测 汽车煞车卡钳市场预测至 2032 年:按产品类型、材料、涂层、活塞数量、车辆类型、客户类型、销售管道、地区进行的全球分析

汽车煞车卡钳市场预测至 2032 年:按产品类型、材料、涂层、活塞数量、车辆类型、客户类型、销售管道、地区进行的全球分析 全球汽车煞车卡钳市场:按车辆类型、产品类型和地区分類的范围和预测

全球汽车煞车卡钳市场:按车辆类型、产品类型和地区分類的范围和预测 汽车煞车卡钳:市场占有率分析、产业趋势/统计、成长预测(2024-2029)

汽车煞车卡钳:市场占有率分析、产业趋势/统计、成长预测(2024-2029)