|

市场调查报告书

商品编码

1797857

资料中心浸入式冷却市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Data Center Immersion Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

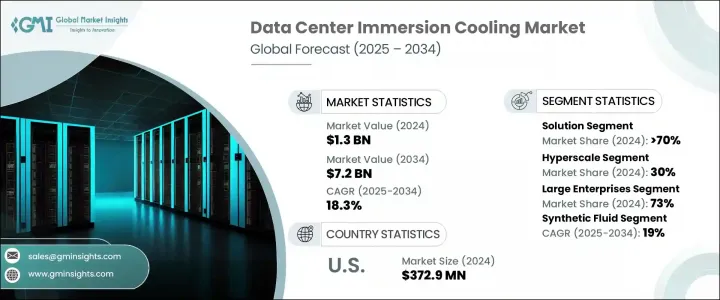

2024 年全球资料中心浸入式冷却市场规模达 13 亿美元,预计到 2034 年将以 18.3% 的复合年增长率成长,达到 72 亿美元。这一快速成长主要得益于人工智慧、机器学习和高效能运算的日益普及——这些应用都会产生大量热负荷,需要先进的冷却解决方案。浸入式冷却已成为支援这些高要求应用的关键技术,尤其是在传统空气冷却系统已无法满足需求的设施中。伺服器基础设施的复杂性和密度日益增长,尤其是在超大规模环境和加密货币挖矿环境中,进一步凸显了对更有效的热管理系统的需求。随着数位工作负载对功率和效能的要求越来越高,营运商越来越多地转向浸入式系统,以降低能耗、提高效率并保持最佳设备效能。

北美凭藉其强大的超大规模资料中心生态系统和对下一代冷却方法的早期采用,继续占据市场主导地位,从而能够在不影响热可靠性的情况下无缝过渡到高密度运算。该地区受益于高度发达的数位基础设施以及主要云端服务提供商的大量投资,这些服务提供商正在快速扩展业务。这为实施浸入式冷却系统创造了理想的环境,该系统不仅可以提高能源效率,还可以降低营运成本。政府的激励措施和对永续IT实践的监管重点进一步加速了其应用。此外,北美成熟的技术人才库和以研究为导向的资料中心优化方法,使该地区在热管理解决方案创新方面处于领先地位,巩固了其在全球市场的领导地位。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 13亿美元 |

| 预测值 | 72亿美元 |

| 复合年增长率 | 18.3% |

2024年,解决方案细分市场占据70%的份额,创造9亿美元的市场价值。此细分市场涵盖所有核心硬件,例如泵浦、热交换器、浸没式水箱、过滤器和流体分配单元。这些组件共同构成了有效实施浸没式冷却所需的结构基础。这些系统不仅支援高热负荷,而且在散热方面也优于传统冷却方法,使资料中心能够在相同的占地面积内容纳更多伺服器。此外,浸没式冷却还能提高空间利用率,并降低维持硬体处于最佳温度所需的运作能耗,从而支持大型设施的长期永续发展目标和成本节约。

超大规模资料中心市场在2024年创造了4亿美元的收入。这些大型基础设施枢纽旨在处理大量资料,并要求最高的营运效率。浸入式冷却因其能够支援高密度配置并最大限度地降低能耗,在这些环境中变得越来越重要。随着运算密集型工作负载的广泛部署,超大规模资料中心营运商寻求减少碳足迹并优化热性能。随着对可扩展和高效系统的需求不断增长,浸入式冷却正持续被整合到新的设施设计中,并被改造到现有结构中,以提高性能指标并减少停机时间。

美国资料中心浸入式冷却市场占72%的市场份额,2024年市场规模达3.729亿美元。由于科技公司的高度集中以及创新基础设施的早期采用者,美国在浸入式冷却部署方面仍处于领先地位。随着云端服务供应商和科技公司营运的资料中心的扩张,对高效可扩展冷却方法的需求也显着增长。由于美国拥有大量超大规模资料中心营运商,并拥有许多全球最大的资料处理设施,对浸入式冷却系统的投资持续激增。

全球资料中心浸入式冷却市场的领导者包括 Vertiv、Green Revolution Cooling、Bitfury Group、Asperitas、LiquidCool Solutions、Submer 和富士通 (Fujitsu)。为了巩固市场地位,资料中心浸入式冷却行业的公司正专注于有针对性的策略,例如扩展产品组合,纳入适用于不同规模和密度资料中心的模组化和可扩展浸入式系统。许多公司正在加强研发力度,以优化流体类型、提高导热性并延长组件使用寿命。与云端服务供应商、主机託管中心和企业客户的合作是一项重要策略,旨在根据特定的工作负载需求提供客製化解决方案。一些製造商也优先考虑国际扩张,尤其是在高效能运算需求日益增长的地区。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 地区

- 国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 机架功率密度和散热挑战的增加

- 可持续性和降低 PUE

- 在超大规模和高效能运算环境中部署

- 主机代管和企业资料中心的兴趣日益浓厚

- 产业陷阱与挑战

- 初始成本高且设计复杂

- 材料相容性和维护问题

- 市场机会

- 人工智慧/机器学习工作负载和超级运算领域的扩展

- 恶劣环境中边缘资料中心部署不断成长

- 流体创新和双相繫统采用

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 消费者行为分析

- 偏好OEM还是第三方浸入式冷却系统

- 偏好 CAPEX 与 OPEX 模型(全系统购买与沉浸式即服务模型)

- 售后市场和服务趋势分析

- 浸入式冷却系统的维护合约和性能 SLA

- 冷却剂更换週期、流体降解监测和硬体升级

- 评估浸泡槽和组件的OEM与第三方服务和支援供应商

- 数位化和自动化趋势分析

- 基于物联网的热能和效能监控的智慧浸入式系统的兴起

- AI/ML 在预测流体管理、系统最佳化和故障检测中的作用

- 浸入式冷却系统部署、启动和热平衡的自动化

- 与 DCIM(资料中心基础设施管理)和遥测平台集成

- 用于模拟浸入式冷却性能和规划改造的数位孪生应用程式

- 跨超大规模、主机託管、HPC 和边缘环境的案例研究和实际部署

- 再生能源整合对资料中心浸没式冷却设计的影响分析

- 混合能源设定(电网+太阳能+电池)中的浸入式系统效率

- 直流供电与交流供电沉浸式基础设施的系统级影响

- 浸入式冷却与备用储存系统(例如锂离子、液流电池)的相容性

- 智慧逆变器和动态能源路由在冷却负载管理中的作用

- 浸入式冷却、净零或低 PUE资料中心案例

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

- 品牌比较分析

- 品牌认知度

- 合作伙伴生态系统

- 客户服务

- 分销网络实力

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 解决方案

- 冷却液

- 冷却架/模组

- 过滤器

- 泵浦

- 热交换器

- 其他的

- 服务

- 安装与维护

- 培训与咨询

第六章:市场估计与预测:按冷却技术,2021 - 2034 年

- 主要趋势

- 单相冷却

- 两相冷却

第七章:市场估计与预测:按冷却液,2021 - 2034 年

- 主要趋势

- 矿物油

- 合成液

- 氟碳基流体

第八章:市场估计与预测:依组织规模,2021 - 2034 年

- 主要趋势

- 中小企业

- 大型企业

第九章:市场估计与预测:按应用,2021 - 2034

- 主要趋势

- 超大规模

- 超级计算

- 企业 HPC

- 加密货币

- 边缘/5G运算

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 波兰

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 东南亚

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 哥伦比亚

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 11 章:公司简介

- Global players

- Regional players

- Emerging players

The Global Data Center Immersion Cooling Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 18.3% to reach USD 7.2 billion by 2034. This rapid growth is largely driven by the rising adoption of artificial intelligence, machine learning, and high-performance computing-all of which generate substantial heat loads and require advanced cooling solutions. Immersion cooling has emerged as a critical technology to support these demanding applications, particularly in facilities where traditional air-based systems are no longer sufficient. The growing complexity and density of server infrastructure, especially within hyperscale environments and crypto mining operations, further highlight the need for more effective heat management systems. With higher power requirements and performance expectations across digital workloads, operators are increasingly transitioning to immersion-based systems to reduce energy usage, enhance efficiency, and maintain optimal equipment performance.

North America continues to dominate the landscape due to its strong ecosystem of hyperscale data centers and early adoption of next-generation cooling methods, enabling a seamless shift to high-density computing without compromising thermal reliability. The region benefits from a highly developed digital infrastructure and substantial investments by major cloud service providers that are rapidly scaling operations. This creates an ideal environment for implementing immersion cooling systems, which not only improve energy efficiency but also reduce operational costs. Government incentives and regulatory focus on sustainable IT practices have further accelerated adoption. Additionally, North America's mature tech talent pool and research-driven approach to data center optimization position the region at the forefront of innovation in thermal management solutions, reinforcing its leadership in the global market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 18.3% |

In 2024, the solution segment accounted 70% share, generating USD 900 million. This segment includes all core hardware such as pumps, heat exchangers, immersion tanks, filters, and fluid distribution units. These elements together form the structural foundation needed to implement immersion cooling effectively. These systems not only support high thermal loads but also outperform traditional cooling methods in heat dissipation, allowing data centers to accommodate more servers within the same footprint. Additionally, immersion cooling offers better space utilization and reduces the operational energy required to keep hardware at optimal temperatures, supporting long-term sustainability goals and cost savings across large-scale facilities.

The hyperscale data centers segment generated USD 400 million in 2024. These large-scale infrastructure hubs are designed to handle massive volumes of data processing and require maximum operational efficiency. Immersion cooling has become increasingly vital in these environments due to its ability to support dense configurations while minimizing energy consumption. With extensive deployments of compute-intensive workloads, hyperscale operators seek to reduce their carbon footprint and optimize thermal performance. As the demand for scalable and high-efficiency systems grows, immersion cooling continues to be integrated into new facility designs and retrofitted into existing structures to improve performance metrics and reduce downtime.

United States Data Center Immersion Cooling Market held 72% share and generated USD 372.9 million in 2024. The country remains at the forefront of immersion cooling deployment, driven by a high concentration of technology firms and early adopters of innovative infrastructure. The demand for efficient and scalable cooling methods has grown significantly alongside the expansion of data centers run by cloud providers and tech companies. With the country hosting a substantial number of hyperscale operators and being home to many of the world's largest data processing facilities, investment in immersion systems continues to surge.

Leading players in the Global Data Center Immersion Cooling Market include Vertiv, Green Revolution Cooling, Bitfury Group, Asperitas, LiquidCool Solutions, Submer, and Fujitsu. To strengthen their market position, companies in the data center immersion cooling industry are focusing on targeted strategies such as expanding product portfolios to include modular and scalable immersion systems suited for different data center sizes and densities. Many firms are enhancing R&D efforts to optimize fluid types, improve thermal conductivity, and extend component lifespan. Collaboration with cloud providers, colocation centers, and enterprise clients is a major tactic, enabling customized solutions tailored to specific workload needs. Several manufacturers are also prioritizing international expansion, especially in regions with emerging high-performance computing demand.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Region

- 1.3.2 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Cooling technique

- 2.2.4 Cooling fluid

- 2.2.5 Organization size

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in rack power density and thermal challenges

- 3.2.1.2 Sustainability and reduction in PUE

- 3.2.1.3 Deployment in hyperscale and high-performance computing environments

- 3.2.1.4 Increasing interest from colocation and enterprise data centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs and design complexity

- 3.2.2.2 Material compatibility and maintenance issues

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in AI/ML workloads and supercomputing sectors

- 3.2.3.2 Growing edge data center deployments in harsh environments

- 3.2.3.3 Fluid innovation and two-phase systems adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Consumer behavior analysis

- 3.11.1 Preference for OEM vs third-party immersion cooling systems

- 3.11.2 Preference for CAPEX vs OPEX models (full system purchase vs immersion-as-a-service models)

- 3.12 Analysis of aftermarket and service trends

- 3.12.1 Maintenance contracts and performance SLAs for immersion cooling systems

- 3.12.2 Coolant replacement cycles, fluid degradation monitoring, and hardware upgrades

- 3.12.3 Evaluation of OEM vs third-party service and support providers for immersion tanks and components

- 3.13 Analysis of digitalization and automation trends

- 3.13.1 Rise of smart immersion systems with IoT-based thermal and performance monitoring

- 3.13.2 Role of AI/ML in predictive fluid management, system optimization, and fault detection

- 3.13.3 Automation in immersion cooling system deployment, startup, and thermal balancing

- 3.13.4 Integration with DCIM (Data Center Infrastructure Management) and telemetry platforms

- 3.13.5 Digital twin applications for simulating immersion cooling performance and planning retrofits

- 3.14 Case studies and real-world deployments across hyperscale, colocation, HPC, and edge environments

- 3.15 Analysis of impact of renewable integration on data center immersion cooling design

- 3.15.1 Immersion system efficiency in hybrid energy setups (grid + solar + battery)

- 3.15.2 System-level implications of DC-powered vs AC-powered immersion infrastructure

- 3.15.3 Compatibility of immersion cooling with backup storage systems (e.g., lithium-ion, flow batteries)

- 3.15.4 Role of smart inverters and dynamic energy routing in cooling load management

- 3.15.5 Case examples of immersion-cooled, net-zero or low-PUE data centers

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Analysis of brand comparison

- 4.7.1 Brand recognition

- 4.7.2 Partnership ecosystem

- 4.7.3 Customer service

- 4.7.4 Distribution network strength

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Cooling fluids

- 5.2.2 Cooling racks/modules

- 5.2.3 Filters

- 5.2.4 Pumps

- 5.2.5 Heat exchangers

- 5.2.6 Others

- 5.3 Service

- 5.3.1 Installation & maintenance

- 5.3.2 Training & consulting

Chapter 6 Market Estimates & Forecast, By Cooling Technique, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Single phase cooling

- 6.3 Two-phase cooling

Chapter 7 Market Estimates & Forecast, By Cooling Fluid, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Mineral oil

- 7.3 Synthetic fluid

- 7.4 Fluorocarbons-based fluid

Chapter 8 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Hyperscale

- 9.3 Supercomputing

- 9.4 Enterprise HPC

- 9.5 Cryptocurrency

- 9.6 Edge/5G computing

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Poland

- 10.3.7 Russia

- 10.3.8 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Chile

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Asperitas

- 11.1.2 Dell Technologies

- 11.1.3 Fujitsu

- 11.1.4 Green Revolution Cooling (GRC)

- 11.1.5 Hewlett Packard Enterprise (HPE)

- 11.1.6 Intel

- 11.1.7 Lenovo

- 11.1.8 Submer

- 11.1.9 Supermicro

- 11.1.10 Vertiv

- 11.2 Regional players

- 11.2.1 AMAX

- 11.2.2 Asetek

- 11.2.3 Bitfury Group

- 11.2.4 DCX Liquid Cooling Company

- 11.2.5 Gigabyte Technology

- 11.2.6 Inspur

- 11.2.7 LiquidCool Solutions

- 11.2.8 Midas Immersion Cooling

- 11.2.9 Nautilus Data Technologies

- 11.2.10 Schneider Electric (in collaboration/PoC phase)

- 11.3 Emerging players

- 11.3.1 E3 NV

- 11.3.2 ExaScaler

- 11.3.3 Hypertec

- 11.3.4 Iceotope

- 11.3.5 JetCool

- 11.3.6 QCT (Quanta Cloud Technology)

- 11.3.7 TAICHI Immersion Cooling

- 11.3.8 Teimmers

- 11.3.9 TMGcore

- 11.3.10 Zutacore

全球资料中心浸入式冷却液市场(至 2032 年)按技术(单相 vs. 双相)、资料中心类型(超大规模、AI/ML、加密货币挖矿)、类型(矿物油、氟碳基液体、合成液体)和地区划分

全球资料中心浸入式冷却液市场(至 2032 年)按技术(单相 vs. 双相)、资料中心类型(超大规模、AI/ML、加密货币挖矿)、类型(矿物油、氟碳基液体、合成液体)和地区划分 2025年全球资料中心冷却市场报告

2025年全球资料中心冷却市场报告 全球资料中心液浸冷却市场研究报告 - 产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球资料中心液浸冷却市场研究报告 - 产业分析、规模、份额、成长、趋势及2025年至2033年预测 循环冷却市场按产品类型、冷却类型、安装类型、冷却能力和最终用户划分 - 全球预测 2025-2030资料中心浸入式冷却市场(按组件、技术类型、资料中心规模、部署类型和最终用户划分)- 全球预测,2025 年至 2030 年

循环冷却市场按产品类型、冷却类型、安装类型、冷却能力和最终用户划分 - 全球预测 2025-2030资料中心浸入式冷却市场(按组件、技术类型、资料中心规模、部署类型和最终用户划分)- 全球预测,2025 年至 2030 年 全球资料中心冷却市场(至 2032 年)按解决方案(空调、冷却装置、冷却塔、节热器係统、液体冷却系统和控制系统)、服务、冷却类型、资料中心类型、最终用户产业和地区划分

全球资料中心冷却市场(至 2032 年)按解决方案(空调、冷却装置、冷却塔、节热器係统、液体冷却系统和控制系统)、服务、冷却类型、资料中心类型、最终用户产业和地区划分 全球资料中心冷媒市场

全球资料中心冷媒市场 2025 年至 2033 年资料中心冷却市场报告(按解决方案、服务、冷却类型、冷却技术、资料中心类型、垂直产业和地区划分)

2025 年至 2033 年资料中心冷却市场报告(按解决方案、服务、冷却类型、冷却技术、资料中心类型、垂直产业和地区划分) 亚太资料中心冷却市场(按产品、应用和国家)分析与预测(2025 年至 2035 年)

亚太资料中心冷却市场(按产品、应用和国家)分析与预测(2025 年至 2035 年) 欧洲资料中心冷却市场(按产品、应用和国家划分)分析与预测(2025-2035 年)

欧洲资料中心冷却市场(按产品、应用和国家划分)分析与预测(2025-2035 年)