|

市场调查报告书

商品编码

1801802

生活用纸市场机会、成长动力、产业趋势分析及2025-2034年预测Household Paper Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

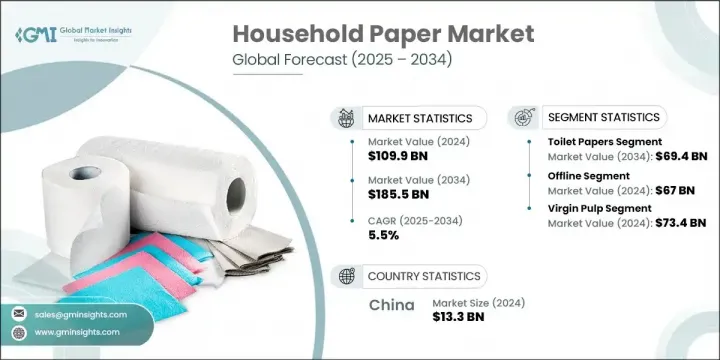

2024年,全球生活用纸市场规模达1,099亿美元,预计到2034年将以5.5%的复合年增长率成长,达到1,855亿美元。随着生活方式的转变、城市人口的扩张以及可支配收入的提高,消费者习惯正在改变,这一上升趋势仍在持续。随着越来越多的人迁入城市,对便利和卫生相关纸製品的需求也日益增长。城市生活不仅带来了更繁忙的日常生活,还带来了诸如用水短缺等挑战,从而增加了对一次性卫生用品的需求。相较之下,低收入家庭取得此类产品的机会有限,由此产生的差距至今仍在影响着全球市场的发展轨迹。

可支配收入较高的消费者往往更青睐柔软度、耐用性和品牌品质更高的高端纸製品。这些消费者更有可能在纸巾、厨房纸巾和卫生纸等必需品中寻求附加价值。此外,全球卫生标准意识的不断提高也推动了对一次性纸製品的需求不断扩大。由于创新,市场也正在发生动态变化——环保材料、超柔软质地和多层结构等新功能正在帮助品牌迎合现代消费者不断变化的偏好,他们注重舒适性和可持续性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1099亿美元 |

| 预测值 | 1855亿美元 |

| 复合年增长率 | 5.5% |

2024年,卫生纸市场规模达396亿美元,预计2034年将增加至694亿美元。卫生纸一直是最主要的家用纸类别。其实用性、广泛的接受度以及人们对柔软、芳香和高品质卫生纸日益增长的偏好,推动了其在已开发经济体和新兴经济体的强劲表现。随着收入水准的提高和都市化进程的扩大,卫生纸作为全球家庭日常用品的地位持续巩固。

2024年,线下零售通路市场规模达670亿美元,预计2025-2034年复合年增长率将达5.3%。由于便利的取得、即时的商品供应以及消费者对实体零售环境的信任等因素,离线销售仍占据全球最大份额。该领域包括超市、便利商店和大卖场等零售连锁店,它们让顾客能够亲自评估产品,这通常比线上通路更有效地影响购买行为。

2024年,中国生活用纸市场规模达133亿美元,预计2025年至2034年期间将以6.2%的复合年增长率强劲成长。由于卫生意识的增强、中产阶级的壮大以及消费者支出能力的提升,中国的生活用纸市场正在快速扩张。现代零售体系和数位平台正在提升产品的覆盖范围和可及性,公众对健康的日益关注——尤其是在全球卫生事件之后——将继续推动人们转向日常使用生活纸。

影响全球生活用纸市场的知名公司包括金佰利、爱生雅、恆安国际集团、乔治亚太平洋、索菲德尔集团、亚洲浆纸、WEPA 集团、爱生雅集团/瑞典纤维素股份公司、日本製纸、王子控股、宝洁、克鲁格产品、美莎纸业集团、维达国际控股和 Cascades。为了在不断发展变化的生活用纸市场中保持竞争力,领导企业已专注于几项关键策略。一个主要领域是投资于产品创新,例如环保材料和多功能设计,以吸引註重健康和环保的消费者。各公司也透过扩大零售业务和利用全通路策略来加强其分销网络,尤其是在新兴经济体。策略合作伙伴关係和合併正在帮助公司扩大其地域足迹。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 监理框架

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 波特五力分析

- PESTEL分析

- 消费者行为分析

- 购买模式

- 偏好分析

- 消费者行为的区域差异

- 电子商务对购买决策的影响

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- MEA

- 拉丁美洲

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依类型,2021-2034

- 主要趋势

- 卫生纸

- 卫生纸

- 厨房用纸

- 面纸

- 其他的

第六章:市场估计与预测:依材料,2021-2034

- 主要趋势

- 原生纸浆

- 再生纸浆

第七章:市场估计与预测:依定价,2021-2034 年

- 主要趋势

- 低的

- 中等的

- 高的

第八章:市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 在线的

- 电子商务网站

- 公司拥有的网站

- 离线

- 大卖场/超市

- 百货公司

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 沙乌地阿拉伯

- 阿联酋

- 南非

第十章:公司简介

- Asia Pulp & Paper

- Cascades

- Essity

- Georgia-Pacific

- Hengan International Group

- Kimberly-Clark

- Kruger Products

- Metsa Tissue - Metsa Group

- Nippon Paper Industries

- Oji Holdings

- Procter & Gamble

- SCA Group / Svenska Cellulosa Aktiebolaget

- Sofidel Group

- Vinda International Holdings

- WEPA Group

The Global Household Paper Market was valued at USD 109.9 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 185.5 billion by 2034. This upward trend continues as shifting lifestyles, expanding urban populations, and rising disposable incomes reshape consumer habits. As more people move into cities, the demand for convenience and hygiene-related paper products has intensified. Urban living not only leads to busier routines but also brings challenges like limited access to water, increasing the need for disposable hygiene products. In contrast, households in lower-income brackets face restricted access to such products, creating disparities that still influence the global market's trajectory.

Consumers with higher disposable incomes tend to gravitate toward premium paper products that offer better softness, durability, and branded quality. These consumers are more likely to seek added value in essentials such as tissues, paper towels, and toilet paper. Furthermore, growing awareness around hygiene standards worldwide is driving broader demand for disposable paper items. The market is also witnessing dynamic shifts thanks to innovation-new features such as eco-friendly materials, ultra-soft textures, and multi-ply construction are helping brands cater to the evolving preferences of modern buyers focused on comfort and sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $109.9 Billion |

| Forecast Value | $185.5 Billion |

| CAGR | 5.5% |

The toilet paper segment generated USD 39.6 billion in 2024 and is forecast to rise to USD 69.4 billion by 2034. It has maintained its lead as the most dominant household paper category. Its practical nature, widespread acceptance, and growing preference for soft, fragranced, and high-quality variants have driven strong performance across both developed and emerging economies. As income levels rise and urbanization expands, toilet paper continues to solidify its role as a daily-use product within homes worldwide.

In 2024, the offline retail channels segment generated USD 67 billion and is expected to grow at a CAGR of 5.3% during 2025-2034. Offline sales still hold the largest share globally due to factors like easy accessibility, immediate product availability, and consumer trust in physical retail environments. This segment includes retail chains such as supermarkets, convenience stores, and hypermarkets, which offer customers the ability to assess products in person-often influencing purchasing behavior more effectively than online channels.

China Household Paper Market generated USD 13.3 billion in 2024 and is poised for strong growth at a CAGR of 6.2% between 2025 and 2034. China is seeing rapid expansion in this sector due to increasing hygiene consciousness, a swelling middle class, and higher consumer spending power. Modern retail systems and digital platforms are improving product reach and availability, and growing public concern about health-particularly after global health events-continues to reinforce the shift toward regular use of household paper goods.

Prominent companies shaping the Global Household Paper Market include Kimberly-Clark, Essity, Hengan International Group, Georgia-Pacific, Sofidel Group, Asia Pulp & Paper, WEPA Group, SCA Group / Svenska Cellulosa Aktiebolaget, Nippon Paper Industries, Oji Holdings, Procter & Gamble, Kruger Products, Metsa Tissue - Metsa Group, Vinda International Holdings, and Cascades. To remain competitive in the evolving household paper market, leading players have focused on several key strategies. One major area has been investment in product innovation, such as eco-conscious materials and multi-functional designs that appeal to health- and environment-conscious consumers. Companies are also strengthening their distribution networks-particularly in emerging economies-by expanding retail presence and leveraging omnichannel strategies. Strategic partnerships and mergers are helping firms broaden their geographic footprint.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Pricing

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

- 3.10 Consumer behavior analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behavior

- 3.10.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 ($Bn, Tons)

- 5.1 Key trends

- 5.2 Toilet papers

- 5.3 Bathroom tissues

- 5.4 Kitchen papers

- 5.5 Facial tissues

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Material, 2021-2034 ($Bn, Tons)

- 6.1 Key trends

- 6.2 Virgin pulp

- 6.3 Recycled pulp

Chapter 7 Market Estimates & Forecast, By Pricing, 2021-2034 ($Bn, Tons)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 ($Bn, Tons)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce website

- 8.2.2 Company owned website

- 8.3 Offline

- 8.3.1 Hypermarket/Supermarket

- 8.3.2 Departmental stores

- 8.3.3 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034, ($Bn, Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Asia Pulp & Paper

- 10.2 Cascades

- 10.3 Essity

- 10.4 Georgia-Pacific

- 10.5 Hengan International Group

- 10.6 Kimberly-Clark

- 10.7 Kruger Products

- 10.8 Metsa Tissue - Metsa Group

- 10.9 Nippon Paper Industries

- 10.10 Oji Holdings

- 10.11 Procter & Gamble

- 10.12 SCA Group / Svenska Cellulosa Aktiebolaget

- 10.13 Sofidel Group

- 10.14 Vinda International Holdings

- 10.15 WEPA Group

空气除尘器市场:按产品类型、分销管道和最终用户划分 - 2026-2032 年全球预测吊挂支架市场:按产品类型、材料、应用和最终用户划分,全球预测(2026-2032年)全球衣架带市场按材料、类型、最终用途和分销管道划分,2026-2032年预测

空气除尘器市场:按产品类型、分销管道和最终用户划分 - 2026-2032 年全球预测吊挂支架市场:按产品类型、材料、应用和最终用户划分,全球预测(2026-2032年)全球衣架带市场按材料、类型、最终用途和分销管道划分,2026-2032年预测 全球节能家用电器市场预测(至2032年):依产品、能源效率等级、价格范围、通路、技术、最终用户及地区划分

全球节能家用电器市场预测(至2032年):依产品、能源效率等级、价格范围、通路、技术、最终用户及地区划分 家庭护理市场规模、份额和成长分析(按产品类型、成分类型、应用、分销管道和地区划分)-2026-2033年产业预测

家庭护理市场规模、份额和成长分析(按产品类型、成分类型、应用、分销管道和地区划分)-2026-2033年产业预测 家庭用纸市场规模、份额及成长分析(依产品类型、材料类型、最终用户、通路、价格分布及地区划分)-2026-2033年产业预测全球感官健康产品市场:预测至2032年-依感官需求、产品类型、通路、价格分布、最终用户和地区进行分析全球家用纸市场按产品类型、分销管道和最终用途划分-2025-2032年预测2032 年健康主导家居用品市场预测:按产品、材料、应用、最终用户和地区进行的全球分析全球节能家电市场:预测(至 2032 年)-依产品类型、能源效率等级、分销管道、最终用户和地区进行分析

家庭用纸市场规模、份额及成长分析(依产品类型、材料类型、最终用户、通路、价格分布及地区划分)-2026-2033年产业预测全球感官健康产品市场:预测至2032年-依感官需求、产品类型、通路、价格分布、最终用户和地区进行分析全球家用纸市场按产品类型、分销管道和最终用途划分-2025-2032年预测2032 年健康主导家居用品市场预测:按产品、材料、应用、最终用户和地区进行的全球分析全球节能家电市场:预测(至 2032 年)-依产品类型、能源效率等级、分销管道、最终用户和地区进行分析