|

市场调查报告书

商品编码

1801892

内视镜再处理市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Endoscope Reprocessing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

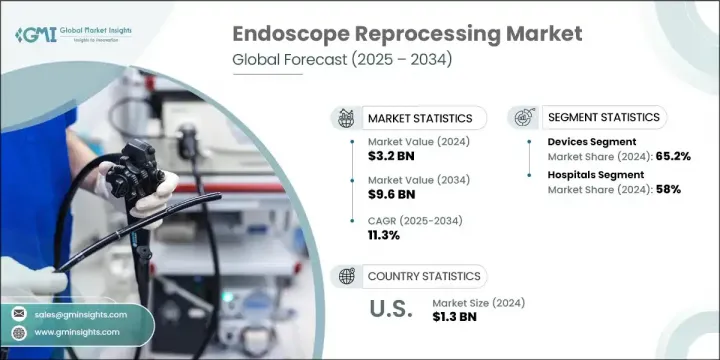

2024年,全球内视镜再处理市场规模达32亿美元,预计到2034年将以11.3%的复合年增长率成长,达到96亿美元。这一市场的快速扩张得益于微创手术技术的日益普及,以及胃肠道疾病和癌症等需要频繁进行内视镜诊断和治疗的疾病的盛行率不断上升。随着越来越多的手术转移到门诊和流动手术中心,对可靠高效的再处理系统的需求,以确保使用者之间内视镜的安全,变得愈发重要。

确保可重复使用内视镜的消毒和安全是临床环境中感染控制的核心。监管机构持续执行严格的内视镜设备清洁和消毒规程。随着医疗保健提供者面临日益增长的减少院内感染的压力,制定全面、经过验证的再处理规程的重要性也日益凸显。此外,对抗菌素抗药性的日益担忧以及对更严格感染预防的需求,也不断加剧了对高效能、高品质内视镜再处理系统的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 32亿美元 |

| 预测值 | 96亿美元 |

| 复合年增长率 | 11.3% |

预计到2034年,配件市场的复合年增长率将达到10.9%,这得益于设备组件的创新,这些创新旨在提升性能并简化工作流程。持续的研发投入使企业能够引入自动化技术,这不仅可以提高再处理的一致性,还可以减少对人工的依赖,而人工往往会导致生产不稳定和潜在的错误。自动化内视镜再处理机的稳定成长,在提高效率的同时,也确保了合规性,并最大限度地降低了不当灭菌的风险。

2024年,医院细分市场占据了58%的市场。此细分市场的主导地位主要归功于其庞大的患者数量,以及日益重视透过严格遵守消毒规程来减少感染传播。医疗机构高度重视技术人员培训、合规性追踪以及清洁週期记录,以确保始终如一地进行正确的消毒。因此,医院正在整合先进的追踪系统,以监控每个内视镜的再处理历史,并优化工作流程的安全性。

2024年,美国内视镜再处理市场规模达13亿美元。美国占据主导地位,得益于其与慢性病相关的高手术量,以及联邦政府对改善医疗机构感染控制的重视。医疗基础设施的升级以及对病人安全计画的财政投入不断增加,正在推动北美地区更广泛地采用自动化和数位化再处理解决方案。

推动全球内视镜再处理市场创新和竞争的主要参与者包括 Olympus、Wassenburg Medical、Steelco、Getinge、Metrex、Ecolab、Belimed、ASP、Shinva Medical Instrument、Creo Medical、CONMED Corporation、Karl Storz、ARC Group of Companies 和 STERIS。为了巩固其在内视镜再处理市场中的地位,领先的公司正在大力投资研发先进的系统,以提供一致的清洁性能并减少人为错误。许多公司专注于自动化和数位集成,以增强可追溯性、提高工作流程效率并确保法规遵循。与医院和外科中心的策略合作有助于扩大客户群并根据实际需求量身定制解决方案。一些参与者提供增值服务,如员工培训、维护和合规性追踪。透过区域製造工厂和本地化服务支援进行全球扩张正在帮助製造商提高市场渗透率。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 内视镜检查的需求不断增加

- 内视镜再处理的技术进步

- 微创手术的偏好日益增加

- 胃肠道疾病、癌症和其他慢性疾病的盛行率不断上升

- 产业陷阱与挑战

- 化学消毒剂的不良反应

- 内视镜再处理设备成本高

- 市场机会

- 感染控制意识不断提高

- 医疗基础设施的成长

- 成长动力

- 成长潜力

- 成长潜力分析

- 报销场景

- 监管格局

- 北美洲

- 欧洲

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 未来市场趋势

- 新产品开发格局

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 装置

- 自动内视镜再处理器(AER)

- 按类型

- 单门自动排气扇

- 双门自动排气扇

- 按可移植性

- 独立 AER

- 手提式空气脱气机

- 按类型

- 内视镜干燥、储存及运送系统

- 其他设备

- 自动内视镜再处理器(AER)

- 耗材

- 阀门和适配器

- 高水准消毒剂

- 床头套件

- 其他耗材

- 配件

第六章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 其他最终用途

第七章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 奥地利

- 瑞士

- 中东欧

- 波兰

- 匈牙利

- 罗马尼亚

- 捷克共和国

- 保加利亚

- 中东欧其他地区

- 北欧国家

- 丹麦

- 瑞典

- 挪威

- 其他北欧国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲和纽西兰

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第八章:公司简介

- ARC Group of Companies

- ASP

- Belimed

- CONMED Corporation

- Creo Medical

- Ecolab

- Getinge

- Metrex

- Olympus

- Shinva Medical Instrument

- Steelco

- STERIS

- Karl Storz

- Wassenburg Medical

The Global Endoscope Reprocessing Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 9.6 billion by 2034. This rapid market expansion is being fueled by the increasing shift toward minimally invasive surgical techniques, coupled with the rising prevalence of conditions such as gastrointestinal diseases and cancers that require frequent diagnostic and therapeutic endoscopic procedures. As more procedures shift to outpatient and ambulatory surgical centers, the need for reliable and efficient reprocessing systems that ensure endoscope safety between users becomes more critical.

Ensuring the disinfection and safety of reusable endoscopes is central to infection control in clinical environments. Regulatory bodies continue to enforce strict protocols for cleaning and disinfecting endoscopic devices. As healthcare providers face heightened pressure to mitigate healthcare-associated infections, the importance of thorough, validated reprocessing protocols has grown considerably. Additionally, increasing concerns surrounding antimicrobial resistance and the demand for greater infection prevention continue to intensify the need for effective, high-quality endoscope reprocessing systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 11.3% |

The accessories segment is expected to grow at a CAGR of 10.9% through 2034, driven by innovation in device components that enhance performance and simplify workflows. Continued investments in R&D are allowing companies to introduce automated technologies that not only improve reprocessing consistency but also reduce reliance on manual labor, which often leads to variability and potential error. The steady rise of automated endoscope reprocessors is enhancing efficiency while ensuring regulatory compliance and minimizing the risk of improper sterilization.

In 2024, the hospitals segment held 58% share. The dominance of this segment is primarily attributed to the high volume of patients and the increasing focus on reducing infection transmission through strict adherence to sterilization protocols. Facilities are placing strong emphasis on technician training, compliance tracking, and documentation of cleaning cycles to ensure that proper disinfection is achieved consistently. As a result, hospitals are integrating advanced tracking systems to monitor the reprocessing history of every scope and optimize workflow safety.

U.S. Endoscope Reprocessing Market was valued at USD 1.3 billion in 2024. The country's dominance stems from high procedural volumes tied to chronic diseases, as well as federal focus on improving infection control across healthcare facilities. Upgrades to healthcare infrastructure and growing financial investment in patient safety initiatives are supporting stronger adoption of automated and digitalized reprocessing solutions across North America.

Key players driving innovation and competition in the Global Endoscope Reprocessing Market include Olympus, Wassenburg Medical, Steelco, Getinge, Metrex, Ecolab, Belimed, ASP, Shinva Medical Instrument, Creo Medical, CONMED Corporation, Karl Storz, ARC Group of Companies, and STERIS. To strengthen their position in the endoscope reprocessing market, leading companies are investing heavily in R&D to develop advanced systems that deliver consistent cleaning performance and reduce human error. Many are focusing on automation and digital integration to enhance traceability, improve workflow efficiency, and ensure regulatory compliance. Strategic collaborations with hospitals and surgical centers are helping expand their client base and tailor solutions to real-world needs. Some players are offering value-added services such as staff training, maintenance, and compliance tracking. Global expansion through regional manufacturing facilities and localized service support is helping manufacturers increase market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for endoscopy procedures

- 3.2.1.2 Technological advancements in endoscope reprocessing

- 3.2.1.3 Rising preferences for minimally invasive procedures

- 3.2.1.4 Increasing prevalence of GI disorders, cancer, and other chronic ailments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects of chemical disinfectants

- 3.2.2.2 High cost of endoscope reprocessing devices

- 3.2.3 Market opportunities

- 3.2.3.1 Rising awareness of infection control

- 3.2.3.2 Growth in healthcare infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential

- 3.4 Growth potential analysis

- 3.5 Reimbursement scenario

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Future market trends

- 3.9 New product development landscape

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Devices

- 5.2.1 Automated endoscope reprocessors (AERs)

- 5.2.1.1 By Type

- 5.2.1.1.1 Single-door AERs

- 5.2.1.1.2 Double-door AERs

- 5.2.1.2 By Portability

- 5.2.1.2.1 Standalone AERs

- 5.2.1.2.2 Portable AERs

- 5.2.1.1 By Type

- 5.2.2 Endoscope drying, storage, and transport systems

- 5.2.3 Other devices

- 5.2.1 Automated endoscope reprocessors (AERs)

- 5.3 Consumables

- 5.3.1 Valves and adaptors

- 5.3.2 High level disinfectants

- 5.3.3 Bedside kits

- 5.3.4 Other consumables

- 5.4 Accessories

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.3.7 Austria

- 7.3.8 Switzerland

- 7.3.9 CEE

- 7.3.9.1 Poland

- 7.3.9.2 Hungary

- 7.3.9.3 Romania

- 7.3.9.4 Czech Republic

- 7.3.9.5 Bulgaria

- 7.3.9.6 Rest of CEE

- 7.3.10 Nordic countries

- 7.3.10.1 Denmark

- 7.3.10.2 Sweden

- 7.3.10.3 Norway

- 7.3.10.4 Rest of Nordic countries

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia and New Zealand

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 ARC Group of Companies

- 8.2 ASP

- 8.3 Belimed

- 8.4 CONMED Corporation

- 8.5 Creo Medical

- 8.6 Ecolab

- 8.7 Getinge

- 8.8 Metrex

- 8.9 Olympus

- 8.10 Shinva Medical Instrument

- 8.11 Steelco

- 8.12 STERIS

- 8.13 Karl Storz

- 8.14 Wassenburg Medical

2026年全球内视镜消毒市场报告

2026年全球内视镜消毒市场报告 全球自动化内视镜清洗设备(AER)市场:市场规模、占有率、成长率、行业分析、依类型、应用和地区的考察以及未来预测(2026-2034)

全球自动化内视镜清洗设备(AER)市场:市场规模、占有率、成长率、行业分析、依类型、应用和地区的考察以及未来预测(2026-2034) 内视镜清洁消毒设备市场:全球预测(2026-2032 年),依产品类型、技术、应用、最终用户和分销管道划分全球医用清洗消毒机市场:市场规模、市场占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

内视镜清洁消毒设备市场:全球预测(2026-2032 年),依产品类型、技术、应用、最终用户和分销管道划分全球医用清洗消毒机市场:市场规模、市场占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 内视镜再处理市场规模、份额和趋势分析报告:按产品、最终用途、地区和细分市场预测(2026-2033 年)

内视镜再处理市场规模、份额和趋势分析报告:按产品、最终用途、地区和细分市场预测(2026-2033 年) 2025-2033年内视镜再处理市场报告(依产品、製程、最终用户及地区)内视镜再处理市场(依服务模式、装置类型、最终用户、应用程式和产品)-2025-2032 年全球预测全球医疗器材清洗消毒市场:市场规模、份额和趋势分析(按产品、製程阶段、最终用途和地区划分),细分市场预测(2025-2033 年)2025年内视镜再处理全球市场报告

2025-2033年内视镜再处理市场报告(依产品、製程、最终用户及地区)内视镜再处理市场(依服务模式、装置类型、最终用户、应用程式和产品)-2025-2032 年全球预测全球医疗器材清洗消毒市场:市场规模、份额和趋势分析(按产品、製程阶段、最终用途和地区划分),细分市场预测(2025-2033 年)2025年内视镜再处理全球市场报告 全球内视镜再处理市场(至 2030 年)按产品类型(AER、HLD 和试纸、清洁剂和擦拭巾、内视镜干燥/储存/运输系统、追踪解决方案)、内视镜类型(柔性/刚性)和最终用户(医院/ASC/专科诊所)划分

全球内视镜再处理市场(至 2030 年)按产品类型(AER、HLD 和试纸、清洁剂和擦拭巾、内视镜干燥/储存/运输系统、追踪解决方案)、内视镜类型(柔性/刚性)和最终用户(医院/ASC/专科诊所)划分