|

市场调查报告书

商品编码

1811755

全球内视镜再处理市场(至 2030 年)按产品类型(AER、HLD 和试纸、清洁剂和擦拭巾、内视镜干燥/储存/运输系统、追踪解决方案)、内视镜类型(柔性/刚性)和最终用户(医院/ASC/专科诊所)划分Endoscope Reprocessing Market by Product (AER, HLD & Test Strip, Detergent & Wipe, Endoscope Drying, Storage, & Transport System, Tracking Solution), Endoscope Type (Flexible, Rigid), End User (Hospital, ASC, Specialty Clinic) - Global Forecast to 2030 |

||||||

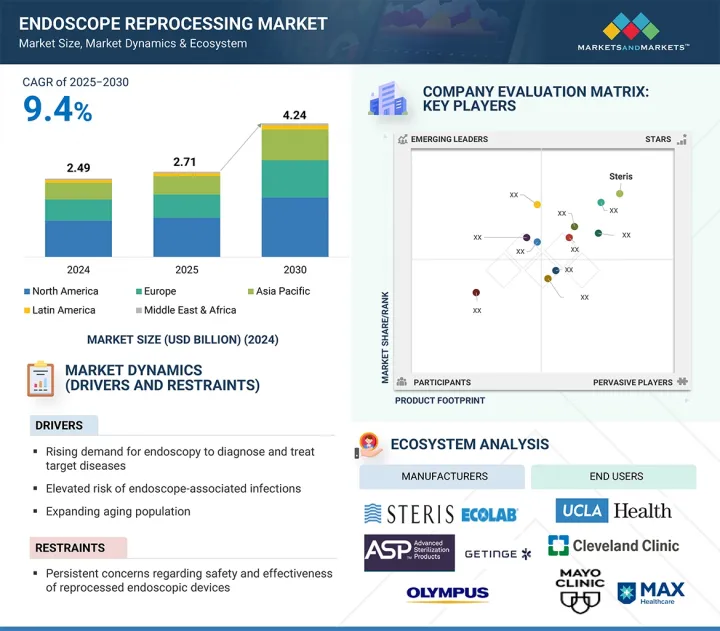

全球内视镜再处理市场预计将从 2025 年的 27.1 亿美元成长到 2030 年的 42.4 亿美元,预测期内的复合年增长率为 9.4%。

| 调查范围 | |

|---|---|

| 调查年份 | 2024-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 单元 | 金额(美元) |

| 部分 | 产品类型、内视镜类型、最终用户 |

| 目标区域 | 北美、欧洲、亚太地区、拉丁美洲、中东和非洲 |

全球内视镜再处理市场的成长主要源自于消化器官系统、呼吸系统和泌尿器官系统疾病的发生率不断上升,以及全球老龄化人口的不断增长,导致内视镜检查数量不断增加。此外,随着人们越来越意识到受污染或消毒不当的内视镜可能带来的感染风险,医疗机构开始实施更严格的再处理通讯协定,这进一步增加了对先进再处理解决方案的需求。

此外,美国食品药物管理局 (FDA)、美国疾病管制与预防中心 (CDC) 和新加坡药品管理局 (SGNA) 等全球卫生机构日益严格的监管规定和更新的指南,正在推动更安全、更标准化的再处理实践。自动化再处理系统的日益普及、医疗基础设施投资的不断增加以及全球为改善患者安全所做的努力,也推动了市场的成长。然而,高额资本投入和复杂的再处理工作流程等挑战可能会限制市场扩张,尤其是在资源有限的地区。

“按内视镜类型划分,软式内视镜将在 2024 年占据最大的市场份额。”

软式内视镜细分市场在2024年占据市场主导地位,该细分市场广泛应用于胃肠病学、呼吸内科和泌尿系统。软式内视镜因其能够到达解剖学上难以触及的部位并提高患者舒适度而受到青睐。大肠镜检查和支气管镜检查等常规和高级检查的兴起,也推动了对有效再处理解决方案的需求,以防止交叉感染并确保安全。此外,越来越多的法规要求对十二指肠镜等复杂器械实施更严格的清洗标准,这也推动了与软式内视镜相容的再处理系统的采用。

“基于最终用户,医院和门诊手术中心部门预计将在 2024 年占据最大份额,并在预测期内实现最高的复合年增长率。”

这一成长的驱动因素包括先进的基础设施建设、对感染预防的投资以及为满足监管和认证标准而采用的自动化再处理设备。此外,医院专注于减少院内感染 (HAI) 并遵守最新的再处理通讯协定,这迅速增加了对灵活高效系统的需求。由于节省成本和提高患者周转率等优势,门诊手术中心也正在进行越来越多的内视镜手术,从而推动了对高通量再处理解决方案的需求。

本报告调查了全球内视镜再处理市场,并提供了市场概况、影响市场成长的各种因素分析、技术和专利趋势、法律制度、案例研究、市场规模趋势和预测、各个细分市场、地区/主要国家的详细分析、竞争格局和主要企业的概况。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章重要考察

第五章 市场概况

- 市场动态

- 驱动程式

- 抑制因素

- 机会

- 任务

- 影响客户业务的趋势/中断

- 定价分析

- 价值链分析

- 供应链分析

- 生态系分析

- 投资金筹措场景

- 技术分析

- 专利分析

- 贸易分析

- 2025-2026年重要会议和活动

- 监管分析

- 波特五力分析

- 主要相关人员和采购标准

- 人工智慧/生成式人工智慧对内视镜再处理市场的影响

- 2025年美国关税对内视镜再处理市场的影响

第六章内视镜再处理市场(依产品)

- 内视镜再处理装置

- 内视镜自动再处理装置

- 内视镜干燥、储存及运送系统

- 内视镜再处理耗材

- 清洁剂和湿纸巾

- 高效消毒剂和试纸

- 其他的

- 内视镜追踪解决方案

第七章内视镜再处理市场(以内视镜类型)

- 软式内视镜

- 硬式内视镜

第八章内视镜再处理市场(依最终用户)

- 医院和 ASC

- 专科诊所

- 其他的

第九章内视镜再处理市场(按地区)

- 北美洲

- 宏观经济展望

- 美国

- 加拿大

- 欧洲

- 宏观经济展望

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他的

- 亚太地区

- 宏观经济展望

- 日本

- 中国

- 印度

- 澳洲

- 其他的

- 拉丁美洲

- 宏观经济展望

- 巴西

- 墨西哥

- 其他的

- 中东和非洲

第十章 竞争格局

- 主要参与企业的策略/优势

- 收益分析

- 市占率分析

- 估值和财务指标

- 品牌/产品比较

- 公司评估矩阵:主要企业

- 公司估值矩阵:Start-Ups/中小型企业

- 竞争场景

第十一章:公司简介

- 主要企业

- STERIS

- ASP

- OLYMPUS CORPORATION

- GETINGE AB

- ECOLAB INC.

- HOYA CORPORATION

- CONMED CORPORATION

- THE MIELE GROUP

- ARC HEALTHCARE SOLUTIONS

- METREX RESEARCH, LLC

- 其他公司

- MEDALKAN

- MICRO-SCIENTIFIC, LLC

- ENDO-TECHNIK W. GRIESAT GMBH

- BES HEALTHCARE LTD

- FUJIFILM HOLDINGS CORPORATION

- BORER CHEMIE AG

- MEDONICA CO. LTD

- TUTTNAUER

- SHINVA MEDICAL INSTRUMENT CO., LTD.

- SBSYSTEM

- OLIVE HEALTH CARE

- MMM GROUP

- AMITY INTERNATIONAL

- MIXTA MEDIKAL

- MEDICAL DEVICES GROUP SRL

第十二章 附录

The global endoscope reprocessing market is projected to reach USD 4.24 billion by 2030 from USD 2.71 billion in 2025, at a CAGR of 9.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, type of endoscope, end user |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

The global endoscope reprocessing market growth is mainly driven by the increasing number of endoscopic procedures, supported by the rising prevalence of gastrointestinal, respiratory, and urological conditions, as well as the growing geriatric population worldwide. Additionally, increased awareness of infection risks linked to contaminated or improperly disinfected endoscopes has led healthcare facilities to implement stricter reprocessing protocols, further increasing the demand for advanced reprocessing solutions.

Furthermore, regulatory pressures and updated guidelines from global health authorities such as the FDA, CDC, and SGNA are encouraging safer and more standardized reprocessing practices. The rising adoption of automated reprocessing systems, higher investments in healthcare infrastructure, and the worldwide effort to improve patient safety are also fueling market growth. However, challenges like high capital costs and the complexity of reprocessing workflows may limit market expansion, especially in resource-limited regions.

The flexible endoscopes segment accounted for the largest market share in the endoscope reprocessing market in 2024.

The endoscope reprocessing market, by type of endoscope, is divided into flexible endoscopes and rigid endoscopes. In 2024, the flexible endoscopes segment led the market due to their widespread use in diagnostic and therapeutic procedures across gastroenterology, pulmonology, and urology. These scopes are favored because of their ability to access difficult-to-reach anatomical areas and provide greater patient comfort. The rising number of routine and advanced procedures, such as colonoscopies and bronchoscopies, which mainly use flexible scopes, has further increased the demand for effective reprocessing solutions to ensure safety and prevent cross-contamination. Additionally, regulatory focus on strict cleaning standards for complex devices like duodenoscopes is strengthening the adoption of reprocessing systems designed for flexible endoscopes.

The hospitals & ambulatory surgery centers segment commanded the largest market share in 2024 and is expected to witness the highest CAGR from 2025 to 2030.

By end user, the endoscope reprocessing market is segmented into hospitals & ambulatory surgery centers, specialty clinics, and other end users. The hospitals and ambulatory surgery centers segment holds the largest share of the endoscope reprocessing market in 2024 and is expected to grow faster during the forecast period, driven by the high volume of endoscopy procedures in these settings. Its growth is supported by factors such as the availability of advanced infrastructure, increased funding for infection prevention, and the adoption of automated reprocessing equipment to meet regulatory and accreditation standards. Furthermore, as hospitals seek to reduce healthcare-associated infections (HAIs) and comply with updated reprocessing protocols, the need for compliant and efficient systems is rapidly increasing. ASCs, offering cost savings and shorter patient turnaround times, are also experiencing a rise in endoscopic procedures, boosting the demand for high-throughput reprocessing solutions.

Europe accounted for the second-largest share of the endoscope reprocessing market by region in 2024.

The global endoscope reprocessing market is divided into five main regions: North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2024, Europe's endoscope reprocessing market is the second-largest regional market. This strong position is supported by robust healthcare infrastructure, regulatory enforcement on infection control, and the increasing burden of chronic diseases that require frequent endoscopic procedures and examinations. Among the European countries, Germany has the largest share, driven by its growing elderly population and increasing surgical procedures. According to the United Nations Population Division, Germany's population aged 65 and older is expected to increase by 41%, reaching roughly 24 million by 2050, which will be about 30% of the total population. Additionally, the Financial Times reports that by 2050, more than half of Germany's population will be aged 48 and older, with nearly a third exceeding 60 years. This demographic change is leading to a rise in age-related gastrointestinal, orthopedic, and cardiovascular conditions, resulting in greater demand for endoscopic procedures and boosting the need for advanced and reliable endoscope reprocessing systems to ensure infection control and safety standards.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1- 40%, Tier 2- 30%, and Tier 3- 30%

- By Designation: C Level- 27%, Director Level- 18% and Others- 55%

- By Region: North America- 35%, Europe- 30%, Asia Pacific- 22%, Latin America- 10%, and Middle East & Africa- 3%

Note 1: Companies are classified into tiers based on their total revenue. As of 2024, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = <USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the endoscope reprocessing market are STERIS (Ireland), ASP (US), Olympus Corporation (Japan), Ecolab (US), Getinge AB (Sweden), HOYA Corporation (Japan), Conmed Corporation (US), Miele (Germany), Endo-Technik W. Griesat GmbH (UK), Fujifilm Holdings Corporation (Japan), BES Healthcare Ltd (UK), ARC Healthcare Solutions (Canada), and Metrex Research, LLC. (Canada), Borer Chemie AG (Switzerland), Tuttnauer (Netherlands), Medonica Co., Ltd. (South Korea), Shinva Medical Instrument Co., Ltd. (China), Micro-Scientific, LLC (US), Medalkan (Greece), Medical Devices Group Srl (Italy), SBSystem (Italy), Olive Health Care (India), MMM Group (Germany), Amity International (UK), and MIXTA MEDIKAL (Turkey), among others.

Research Coverage

This report examines the endoscope reprocessing market by products, type of endoscope, end user, and region. The report also explores factors such as drivers, restraints, opportunities, and challenges that influence market growth and provides details of the competitive landscape for market leaders. Additionally, it analyzes micro markets based on their individual growth trends. The report forecasts the revenue of market segments across five major regions and the respective countries within those regions.

Reasons to Buy the Report

The report will help both established and smaller firms to understand the market trends, which can then assist them in increasing their market share. Companies purchasing the report may use one or a combination of the strategies listed below to strengthen their market position presence.

This report provides insights on the following points: analysis of key drivers (rising demand for endoscopy to diagnose and treat target diseases, elevated risk of endoscope-associated infections, expanding aging population, increasing emphasis on improving reprocessing guidelines by healthcare authorities, and rising adoption of minimally invasive surgeries), restraints (persistent concerns regarding safety and effectiveness of reprocessed endoscopic devices, potential health hazards associated with exposure to high-level chemical disinfectants, and high operational costs of endoscopic procedures coupled with limited reimbursement frameworks in emerging economies), opportunities (expanding medical devices industry in emerging economies and increased funding and investments for better healthcare infrastructure and endoscopy-related research), and challenges (rising demand for single-use endoscopes, increasing product failures and recalls, lack of adequately trained personnel, limited awareness among healthcare workers regarding standardized and effective reprocessing practices, and increasing FDA recommended measures to reduce infection transmission)

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the endoscope reprocessing market

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the endoscope reprocessing market

- Market Development: Comprehensive information on lucrative emerging regions

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the endoscope reprocessing market

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary sources

- 2.1.2.2 Key objectives of primary research

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.2.5 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Company revenue estimation approach

- 2.2.1.1.1 Presentations of companies and primary interviews

- 2.2.1.1.2 Primary interviews

- 2.2.1.2 Growth forecast

- 2.2.1.3 Market segment assessment

- 2.2.1.1 Company revenue estimation approach

- 2.2.2 TOP-DOWN APPROACH

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 MARKET SHARE ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.5.1 PARAMETRIC ASSUMPTIONS

- 2.5.2 GROWTH RATE ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.6.1 METHODOLOGY-RELATED LIMITATIONS

- 2.6.2 SCOPE-RELATED LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ENDOSCOPE REPROCESSING MARKET OVERVIEW

- 4.2 ASIA PACIFIC ENDOSCOPE REPROCESSING MARKET, BY PRODUCT AND COUNTRY

- 4.3 ENDOSCOPE REPROCESSING MARKET, BY COUNTRY

- 4.4 ENDOSCOPE REPROCESSING MARKET, REGIONAL MIX, 2025 VS. 2030

- 4.5 ENDOSCOPE REPROCESSING MARKET: EMERGING ECONOMIES VS. DEVELOPED MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising demand for endoscopy to diagnose and treat target diseases

- 5.2.1.2 Elevated risk of endoscope-associated infections

- 5.2.1.3 Booming geriatric population

- 5.2.1.4 Increasing emphasis on improving reprocessing guidelines

- 5.2.1.5 Growing adoption of minimally invasive surgeries

- 5.2.2 RESTRAINTS

- 5.2.2.1 Persistent concerns about safety and effectiveness of reprocessed endoscopic devices

- 5.2.2.2 Potential health hazards associated with exposure to high-level chemical disinfectants

- 5.2.2.3 High operational costs and limited reimbursement in developing economies

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expanding medical devices industry

- 5.2.3.2 Increased funding and investments for healthcare infrastructure

- 5.2.4 CHALLENGES

- 5.2.4.1 Preference for single-use endoscopes

- 5.2.4.2 Increasing number of product failures and recalls

- 5.2.4.3 Lack of adequately trained personnel

- 5.2.4.4 Limited awareness about standardized and effective reprocessing practices

- 5.2.4.5 Increasing FDA-recommended measures to reduce infection transmission

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY KEY PLAYER

- 5.4.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Automated mechanical cleaning and disinfection

- 5.9.1.2 High-level chemical disinfection

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Low-temperature sterilization

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT DATA FOR HS CODE 841920

- 5.11.2 EXPORT DATA FOR HS CODE 841920

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 REGULATORY ANALYSIS

- 5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.2 REGULATORY FRAMEWORK

- 5.13.2.1 North America

- 5.13.2.1.1 US

- 5.13.2.1.2 Canada

- 5.13.2.2 Europe

- 5.13.2.2.1 Germany

- 5.13.2.2.2 Rest of Europe

- 5.13.2.3 Asia Pacific

- 5.13.2.3.1 Japan

- 5.13.2.3.2 Australia

- 5.13.2.3.3 Rest of Asia Pacific

- 5.13.2.4 Latin America

- 5.13.2.5 Middle East & Africa

- 5.13.2.1 North America

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF BUYERS

- 5.14.4 BARGAINING POWER OF SUPPLIERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 KEY BUYING CRITERIA

- 5.16 IMPACT OF AI/GEN AI ON ENDOSCOPE REPROCESSING MARKET

- 5.16.1 INTRODUCTION

- 5.16.2 MARKET POTENTIAL OF AI/GEN AI IN ENDOSCOPE REPROCESSING MARKET

- 5.16.3 AI USE CASES

- 5.16.4 FUTURE OF AI/GEN AI IN ENDOSCOPE REPROCESSING ECOSYSTEM

- 5.17 IMPACT OF 2025 US TARIFF REGULATION ON ENDOSCOPE REPROCESSING MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 KEY IMPACT ON COUNTRY/REGION

- 5.17.4.1 North America

- 5.17.4.1.1 US

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.4.1 North America

- 5.17.5 IMPACT ON END-USE INDUSTRIES

- 5.17.5.1 Hospitals

- 5.17.5.2 Ambulatory care centers

6 ENDOSCOPE REPROCESSING MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 ENDOSCOPE REPROCESSING EQUIPMENT

- 6.2.1 AUTOMATED ENDOSCOPE REPROCESSORS

- 6.2.1.1 Automated endoscope reprocessors, by portability

- 6.2.1.1.1 Standalone automated endoscope reprocessors

- 6.2.1.1.2 Portable automated endoscope reprocessors

- 6.2.1.2 Automated endoscope reprocessors, by type

- 6.2.1.2.1 Single-basin automated endoscope reprocessors

- 6.2.1.2.2 Double-basin automated endoscope reprocessors

- 6.2.1.1 Automated endoscope reprocessors, by portability

- 6.2.2 ENDOSCOPE DRYING, STORAGE, AND TRANSPORT SYSTEMS

- 6.2.2.1 Need for patient safety and efficient reprocessing workflow to accelerate growth

- 6.2.1 AUTOMATED ENDOSCOPE REPROCESSORS

- 6.3 ENDOSCOPE REPROCESSING CONSUMABLES

- 6.3.1 DETERGENTS & WIPES

- 6.3.1.1 Rising focus on pre-cleaning protocols to aid growth

- 6.3.2 HIGH-LEVEL DISINFECTANTS & TEST STRIPS

- 6.3.2.1 Growing number of infection outbreaks to drive market

- 6.3.3 OTHER PRODUCTS

- 6.3.1 DETERGENTS & WIPES

- 6.4 ENDOSCOPE TRACKING SOLUTIONS

- 6.4.1 IMPROVED TRACEABILITY AND SUPERVISION TO FOSTER GROWTH

7 ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE

- 7.1 INTRODUCTION

- 7.2 FLEXIBLE ENDOSCOPES

- 7.2.1 REAL-TIME IMAGING CAPABILITIES TO CONTRIBUTE TO GROWTH

- 7.3 RIGID ENDOSCOPES

- 7.3.1 SUPERIOR IMAGE RESOLUTION AND ENHANCED STABILITY TO SPUR GROWTH

8 ENDOSCOPE REPROCESSING MARKET, BY END USER

- 8.1 INTRODUCTION

- 8.2 HOSPITALS & ASCS

- 8.2.1 RISE IN INFECTION CASES TO FACILITATE GROWTH

- 8.3 SPECIALTY CLINICS

- 8.3.1 NEED TO MAINTAIN HIGH STANDARDS OF SAFETY AND QUALITY TO FOSTER GROWTH

- 8.4 OTHER END USERS

9 ENDOSCOPE REPROCESSING MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 9.2.2 US

- 9.2.2.1 Rising incidence of colorectal cancer to augment growth

- 9.2.3 CANADA

- 9.2.3.1 High prevalence of hospital-acquired infections to promote growth

- 9.3 EUROPE

- 9.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 9.3.2 GERMANY

- 9.3.2.1 Aging population and increasing disease burden to support growth

- 9.3.3 UK

- 9.3.3.1 Increasing use of endoscopy procedures to foster growth

- 9.3.4 FRANCE

- 9.3.4.1 Strong public investment in healthcare infrastructure to aid growth

- 9.3.5 ITALY

- 9.3.5.1 Growing geriatric population to drive market

- 9.3.6 SPAIN

- 9.3.6.1 Demographic shift and increasing number of specialized care personnel to expedite growth

- 9.3.7 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 9.4.2 JAPAN

- 9.4.2.1 Increasing number of endoscopic surgeries to spur growth

- 9.4.3 CHINA

- 9.4.3.1 Rising elderly population to facilitate growth

- 9.4.4 INDIA

- 9.4.4.1 Improved healthcare infrastructure and booming healthcare tourism to bolster growth

- 9.4.5 AUSTRALIA

- 9.4.5.1 Growing number of age-related illnesses to boost market

- 9.4.6 REST OF ASIA PACIFIC

- 9.5 LATIN AMERICA

- 9.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 9.5.2 BRAZIL

- 9.5.2.1 Need to maintain hygiene and safety standards to boost market

- 9.5.3 MEXICO

- 9.5.3.1 Rising cancer burden to accelerate growth

- 9.5.4 REST OF LATIN AMERICA

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 EMERGING STANDARDS FOR REPROCESSING TO AUGMENT GROWTH

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 10.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN ENDOSCOPE REPROCESSING MARKET

- 10.3 REVENUE ANALYSIS, 2020-2024

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 COMPANY VALUATION AND FINANCIAL METRICS

- 10.6 BRAND/PRODUCT COMPARISON

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.7.5.1 Company footprint

- 10.7.5.2 Region footprint

- 10.7.5.3 Product footprint

- 10.7.5.4 End-user footprint

- 10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.8.5.1 Detailed list of key startups/SMEs

- 10.8.5.2 Competitive benchmarking of key startups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

- 10.9.3 EXPANSIONS

- 10.9.4 OTHER DEVELOPMENTS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 STERIS

- 11.1.1.1 Business overview

- 11.1.1.2 Products offered

- 11.1.1.3 MnM view

- 11.1.1.3.1 Key strengths

- 11.1.1.3.2 Strategic choices

- 11.1.1.3.3 Weaknesses and competitive threats

- 11.1.2 ASP

- 11.1.2.1 Business overview

- 11.1.2.2 Products offered

- 11.1.2.3 MnM view

- 11.1.2.3.1 Key strengths

- 11.1.2.3.2 Strategic choices

- 11.1.2.3.3 Weaknesses and competitive threats

- 11.1.3 OLYMPUS CORPORATION

- 11.1.3.1 Business overview

- 11.1.3.2 Products offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Product launches

- 11.1.3.3.2 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 GETINGE AB

- 11.1.4.1 Business overview

- 11.1.4.2 Products offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches

- 11.1.4.3.2 Deals

- 11.1.5 ECOLAB INC.

- 11.1.5.1 Business overview

- 11.1.5.2 Products offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Other developments

- 11.1.6 HOYA CORPORATION

- 11.1.6.1 Business overview

- 11.1.6.2 Products offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Deals

- 11.1.7 CONMED CORPORATION

- 11.1.7.1 Business overview

- 11.1.7.2 Products offered

- 11.1.8 THE MIELE GROUP

- 11.1.8.1 Business overview

- 11.1.8.2 Products offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Deals

- 11.1.9 ARC HEALTHCARE SOLUTIONS

- 11.1.9.1 Business overview

- 11.1.9.2 Products offered

- 11.1.10 METREX RESEARCH, LLC

- 11.1.10.1 Business overview

- 11.1.10.2 Products offered

- 11.1.1 STERIS

- 11.2 OTHER PLAYERS

- 11.2.1 MEDALKAN

- 11.2.2 MICRO-SCIENTIFIC, LLC

- 11.2.3 ENDO-TECHNIK W. GRIESAT GMBH

- 11.2.4 BES HEALTHCARE LTD

- 11.2.5 FUJIFILM HOLDINGS CORPORATION

- 11.2.6 BORER CHEMIE AG

- 11.2.7 MEDONICA CO. LTD

- 11.2.8 TUTTNAUER

- 11.2.9 SHINVA MEDICAL INSTRUMENT CO., LTD.

- 11.2.10 SBSYSTEM

- 11.2.11 OLIVE HEALTH CARE

- 11.2.12 MMM GROUP

- 11.2.13 AMITY INTERNATIONAL

- 11.2.14 MIXTA MEDIKAL

- 11.2.15 MEDICAL DEVICES GROUP SRL

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS

List of Tables

- TABLE 1 ENDOSCOPE REPROCESSING MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 EXCHANGE RATES USED FOR CONVERSION OF YEN TO USD, 2023-2025

- TABLE 3 EXCHANGE RATES USED FOR CONVERSION OF SEK TO USD, 2022-2024

- TABLE 4 ENDOSCOPE REPROCESSING MARKET: KEY DATA FROM PRIMARY SOURCES

- TABLE 5 ENDOSCOPE REPROCESSING MARKET: PARAMETRIC ASSUMPTIONS

- TABLE 6 ENDOSCOPE REPROCESSING MARKET: RISK ANALYSIS

- TABLE 7 AVERAGE SELLING PRICE TREND OF ENDOSCOPE REPROCESSING DEVICES, BY KEY PLAYER, 2022-2024 (USD)

- TABLE 8 AVERAGE SELLING PRICE TREND OF ENDOSCOPE REPROCESSING DEVICES, BY REGION, 2022-2024 (USD)

- TABLE 9 ENDOSCOPE REPROCESSING MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 10 ENDOSCOPE REPROCESSING MARKET: LIST OF PATENTS/PATENT REGISTRATIONS, 2023-2024

- TABLE 11 IMPORT DATA FOR HS CODE 841920, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 12 EXPORT DATA FOR HS CODE 841920, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 13 ENDOSCOPE REPROCESSING MARKET: KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 14 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 ENDOSCOPE REPROCESSING MARKET: PORTER'S FIVE FORCES

- TABLE 20 INFLUENCE OF KEY STAKEHOLDERS ON BUYING PROCESS, BY END USER (%)

- TABLE 21 KEY BUYING CRITERIA, BY END USER

- TABLE 22 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 23 ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 24 ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 25 ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 26 NORTH AMERICA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 27 EUROPE: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 28 ASIA PACIFIC: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 29 LATIN AMERICA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 30 MANUFACTURERS AND RESPECTIVE AUTOMATED ENDOSCOPE REPROCESSOR MODELS

- TABLE 31 AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 32 NORTH AMERICA: AUTOMATED ENDOSCOPE RREPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 33 EUROPE: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 34 ASIA PACIFIC: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 35 LATIN AMERICA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 36 AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 37 STANDALONE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 38 NORTH AMERICA: STANDALONE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 39 EUROPE: STANDALONE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 40 ASIA PACIFIC: STANDALONE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 41 LATIN AMERICA: STANDALONE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 42 PORTABLE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 43 NORTH AMERICA: PORTABLE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 44 EUROPE: PORTABLE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 45 ASIA PACIFIC: PORTABLE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 46 LATIN AMERICA: PORTABLE AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 47 AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 48 MANUFACTURERS AND RESPECTIVE SINGLE-BASIN AUTOMATED ENDOSCOPE REPROCESSOR MODELS

- TABLE 49 SINGLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 50 NORTH AMERICA: SINGLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 51 EUROPE: SINGLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 52 ASIA PACIFIC: SINGLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 53 LATIN AMERICA: SINGLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 54 MANUFACTURERS AND RESPECTIVE DUAL-BASIN AUTOMATED ENDOSCOPE REPROCESSOR MODELS

- TABLE 55 DOUBLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 56 NORTH AMERICA: DOUBLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 57 EUROPE: DOUBLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 58 ASIA PACIFIC: DOUBLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 59 LATIN AMERICA: DOUBLE-BASIN AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 60 ENDOSCOPE DRYING, STORAGE, AND TRANSPORT SYSTEMS OFFERED BY KEY PLAYERS

- TABLE 61 ENDOSCOPE DRYING, STORAGE, AND TRANSPORT SYSTEMS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 62 NORTH AMERICA: ENDOSCOPE DRYING, STORAGE, AND TRANSPORT SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 63 EUROPE: ENDOSCOPE DRYING, STORAGE, AND TRANSPORT SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 64 ASIA PACIFIC: ENDOSCOPE DRYING, STORAGE, AND TRANSPORT SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 65 LATIN AMERICA: ENDOSCOPE DRYING, STORAGE, AND TRANSPORT SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 66 ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 67 ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 68 NORTH AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 69 EUROPE: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 70 ASIA PACIFIC: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 71 LATIN AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 72 ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR DETERGENTS & WIPES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 73 NORTH AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR DETERGENTS & WIPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 74 EUROPE: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR DETERGENTS & WIPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 75 ASIA PACIFIC: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR DETERGENTS & WIPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 76 LATIN AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR DETERGENTS & WIPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 77 ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR HIGH-LEVEL DISINFECTANTS & TEST STRIPS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 78 NORTH AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR HIGH-LEVEL DISINFECTANTS & TEST STRIPS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 79 EUROPE: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR HIGH-LEVEL DISINFECTANTS & TEST STRIPS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 80 ASIA PACIFIC: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR HIGH-LEVEL DISINFECTANTS & TEST STRIPS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 81 LATIN AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR HIGH-LEVEL DISINFECTANTS & TEST STRIPS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 82 OTHER REPROCESSING CONSUMABLE PRODUCTS OFFERED BY MANUFACTURERS

- TABLE 83 ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR OTHER PRODUCTS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 84 NORTH AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR OTHER PRODUCTS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 85 EUROPE: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR OTHER PRODUCTS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 86 ASIA PACIFIC: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR OTHER PRODUCTS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 87 LATIN AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET FOR OTHER PRODUCTS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 88 ENDOSCOPE TRACKING SOLUTIONS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 89 NORTH AMERICA: ENDOSCOPE TRACKING SOLUTIONS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 90 EUROPE: ENDOSCOPE TRACKING SOLUTIONS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 91 ASIA PACIFIC: ENDOSCOPE TRACKING SOLUTIONS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 92 LATIN AMERICA: ENDOSCOPE TRACKING SOLUTIONS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 93 ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 94 ENDOSCOPE REPROCESSING MARKET FOR FLEXIBLE ENDOSCOPES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 95 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET FOR FLEXIBLE ENDOSCOPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 96 EUROPE: ENDOSCOPE REPROCESSING MARKET FOR FLEXIBLE ENDOSCOPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 97 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET FOR FLEXIBLE ENDOSCOPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 98 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET FOR FLEXIBLE ENDOSCOPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 99 ENDOSCOPE REPROCESSING MARKET FOR RIGID ENDOSCOPES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 100 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET FOR RIGID ENDOSCOPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 101 EUROPE: ENDOSCOPE REPROCESSING MARKET FOR RIGID ENDOSCOPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 102 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET FOR RIGID ENDOSCOPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 103 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET FOR RIGID ENDOSCOPES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 104 ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 105 HOSPITALS PER CAPITA, BY COUNTRY, 2024

- TABLE 106 ENDOSCOPE REPROCESSING MARKET FOR HOSPITALS & ASCS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 107 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET FOR HOSPITALS & ASCS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 108 EUROPE: ENDOSCOPE REPROCESSING MARKET FOR HOSPITALS & ASCS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 109 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET FOR HOSPITALS & ASCS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 110 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET FOR HOSPITALS & ASCS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 111 ENDOSCOPE REPROCESSING MARKET FOR SPECIALTY CLINICS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 112 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET FOR SPECIALTY CLINICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 113 EUROPE: ENDOSCOPE REPROCESSING MARKET FOR SPECIALTY CLINICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 114 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET FOR SPECIALTY CLINICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 115 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET FOR SPECIALTY CLINICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 116 ENDOSCOPE REPROCESSING MARKET FOR OTHER END USERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 117 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET FOR OTHER END USERS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 118 EUROPE: ENDOSCOPE REPROCESSING MARKET FOR OTHER END USERS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 119 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET FOR OTHER END USERS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 120 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET FOR OTHER END USERS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 121 ENDOSCOPE REPROCESSING MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 122 NORTH AMERICA: KEY MACROECONOMIC INDICATORS

- TABLE 123 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 124 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 125 NORTH AMERICA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 126 NORTH AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 127 NORTH AMERICA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 128 NORTH AMERICA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 129 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 130 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 131 MEDICARE NATIONAL AVERAGE COVERAGE FOR OUTPATIENT PROCEDURES, 2025

- TABLE 132 US: INSTALLATION BASE OF AUTOMATED ENDOSCOPE REPROCESSORS IN HOSPITALS, 2023-2030 (UNITS)

- TABLE 133 US: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 134 US: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 135 US: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 136 US: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 137 US: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 138 US: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 139 US: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 140 CANADA: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 141 CANADA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 142 CANADA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 143 CANADA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 144 CANADA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 145 CANADA: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 146 CANADA: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 147 EUROPE: KEY MACROECONOMIC INDICATORS

- TABLE 148 EUROPE: ENDOSCOPE REPROCESSING MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 149 EUROPE: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 150 EUROPE: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 151 EUROPE: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 152 EUROPE: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 153 EUROPE: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 154 EUROPE: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 155 EUROPE: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 156 GERMANY: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 157 GERMANY: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 158 GERMANY: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 159 GERMANY: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 160 GERMANY: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 161 GERMANY: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 162 GERMANY: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 163 UK: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 164 UK: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 165 UK: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 166 UK: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 167 UK: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 168 UK: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 169 UK: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 170 FRANCE: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 171 FRANCE: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 172 FRANCE: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 173 FRANCE: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 174 FRANCE: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 175 FRANCE: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 176 FRANCE: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 177 ITALY: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 178 ITALY: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 179 ITALY: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 180 ITALY: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 181 ITALY: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 182 ITALY: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 183 ITALY: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 184 SPAIN: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 185 SPAIN: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 186 SPAIN: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 187 SPAIN: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 188 SPAIN: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 189 SPAIN: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 190 SPAIN: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 191 REST OF EUROPE: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 192 REST OF EUROPE: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 193 REST OF EUROPE: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 194 REST OF EUROPE: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 195 REST OF EUROPE: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 196 REST OF EUROPE: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 197 REST OF EUROPE: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 198 ASIA PACIFIC: KEY MACROECONOMIC INDICATORS

- TABLE 199 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 200 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 201 ASIA PACIFIC: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 202 ASIA PACIFIC: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 203 ASIA PACIFIC: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 204 ASIA PACIFIC: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 205 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 206 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 207 JAPAN: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 208 JAPAN: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 209 JAPAN: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 210 JAPAN: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 211 JAPAN: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 212 JAPAN: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 213 JAPAN: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 214 CHINA: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 215 CHINA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 216 CHINA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 217 CHINA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 218 CHINA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 219 CHINA: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 220 CHINA: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 221 INDIA: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 222 INDIA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 223 INDIA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 224 INDIA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 225 INDIA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 226 INDIA: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 227 INDIA: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 228 AUSTRALIA: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 229 AUSTRALIA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 230 AUSTRALIA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 231 AUSTRALIA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 232 AUSTRALIA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 233 AUSTRALIA: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 234 AUSTRALIA: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 235 REST OF ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 236 REST OF ASIA PACIFIC: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 237 REST OF ASIA PACIFIC: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 238 REST OF ASIA PACIFIC: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 239 REST OF ASIA PACIFIC: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 240 REST OF ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 241 REST OF ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 242 LATIN AMERICA: KEY MACROECONOMIC INDICATORS

- TABLE 243 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 244 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 245 LATIN AMERICA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 246 LATIN AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 247 LATIN AMERICA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 248 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 249 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 250 LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 251 BRAZIL: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 252 BRAZIL: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 253 BRAZIL: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 254 BRAZIL: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 255 BRAZIL: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 256 BRAZIL: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 257 BRAZIL: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 258 MEXICO: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 259 MEXICO: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 260 MEXICO: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 261 MEXICO: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 262 MEXICO: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 263 MEXICO: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 264 MEXICO: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 265 REST OF LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 266 REST OF LATIN AMERICA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 267 REST OF LATIN AMERICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 268 REST OF LATIN AMERICA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 269 REST OF LATIN AMERICA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 270 REST OF LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 271 REST OF LATIN AMERICA: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 272 MIDDLE EAST & AFRICA: ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 273 MIDDLE EAST & AFRICA: ENDOSCOPE REPROCESSING EQUIPMENT MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 274 MIDDLE EAST & AFRICA: ENDOSCOPE REPROCESSING CONSUMABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 275 MIDDLE EAST & AFRICA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY PORTABILITY, 2023-2030 (USD MILLION)

- TABLE 276 MIDDLE EAST & AFRICA: AUTOMATED ENDOSCOPE REPROCESSORS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 277 MIDDLE EAST & AFRICA: ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2023-2030 (USD MILLION)

- TABLE 278 MIDDLE EAST & AFRICA: ENDOSCOPE REPROCESSING MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 279 MIDDLE EAST & AFRICA: KEY MACROECONOMIC INDICATORS

- TABLE 280 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN ENDOSCOPE REPROCESSING MARKET, JANUARY 2022-JULY 2025

- TABLE 281 ENDOSCOPE REPROCESSING MARKET: DEGREE OF COMPETITION

- TABLE 282 ENDOSCOPE REPROCESSING MARKET: REGION FOOTPRINT

- TABLE 283 ENDOSCOPE REPROCESSING MARKET: PRODUCT FOOTPRINT

- TABLE 284 ENDOSCOPE REPROCESSING MARKET: END-USER FOOTPRINT

- TABLE 285 ENDOSCOPE REPROCESSING MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 286 ENDOSCOPE REPROCESSING MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 287 ENDOSCOPE REPROCESSING MARKET: PRODUCT LAUNCHES, JANUARY 2022-JULY 2025

- TABLE 288 ENDOSCOPE REPROCESSING MARKET: DEALS, JANUARY 2022-JULY 2025

- TABLE 289 ENDOSCOPE REPROCESSING MARKET: EXPANSIONS, JANUARY 2022-JULY 2025

- TABLE 290 ENDOSCOPE REPROCESSING MARKET: OTHER DEVELOPMENTS, JANUARY 2022-JULY 2025

- TABLE 291 STERIS: COMPANY OVERVIEW

- TABLE 292 STERIS: PRODUCTS OFFERED

- TABLE 293 ASP: COMPANY OVERVIEW

- TABLE 294 ASP: PRODUCTS OFFERED

- TABLE 295 OLYMPUS CORPORATION: COMPANY OVERVIEW

- TABLE 296 OLYMPUS CORPORATION: PRODUCTS OFFERED

- TABLE 297 OLYMPUS CORPORATION: PRODUCT LAUNCHES, JANUARY 2022-JULY 2025

- TABLE 298 OLYMPUS CORPORATION: EXPANSIONS, JANUARY 2022-JULY 2025

- TABLE 299 GETINGE AB: COMPANY OVERVIEW

- TABLE 300 GETINGE AB: PRODUCTS OFFERED

- TABLE 301 GETINGE AB: PRODUCT LAUNCHES, JANUARY 2022-JULY 2025

- TABLE 302 GETINGE AB: DEALS, JANUARY 2022-JULY 2025

- TABLE 303 ECOLAB INC.: COMPANY OVERVIEW

- TABLE 304 ECOLAB INC.: PRODUCTS OFFERED

- TABLE 305 ECOLAB INC.: OTHER DEVELOPMENTS, JANUARY 2022-JULY 2025

- TABLE 306 HOYA CORPORATION: COMPANY OVERVIEW

- TABLE 307 HOYA CORPORATION: PRODUCTS OFFERED

- TABLE 308 HOYA CORPORATION: DEALS, JANUARY 2022-JULY 2025

- TABLE 309 CONMED CORPORATION: COMPANY OVERVIEW

- TABLE 310 CONMED CORPORATION: PRODUCTS OFFERED

- TABLE 311 THE MIELE GROUP: COMPANY OVERVIEW

- TABLE 312 THE MIELE GROUP: PRODUCTS OFFERED

- TABLE 313 THE MIELE GROUP: DEALS, JANUARY 2022-JULY 2025

- TABLE 314 ARC HEALTHCARE SOLUTIONS: COMPANY OVERVIEW

- TABLE 315 ARC HEALTHCARE SOLUTIONS: PRODUCTS OFFERED

- TABLE 316 METREX RESEARCH, LLC: COMPANY OVERVIEW

- TABLE 317 METREX RESEARCH, LLC: PRODUCTS OFFERED

- TABLE 318 MEDALKAN: COMPANY OVERVIEW

- TABLE 319 MICRO-SCIENTIFIC, LLC: COMPANY OVERVIEW

- TABLE 320 ENDO-TECHNIK W. GRIESAT GMBH: COMPANY OVERVIEW

- TABLE 321 BES HEALTHCARE LTD: COMPANY OVERVIEW

- TABLE 322 FUJIFILM HOLDINGS CORPORATION: COMPANY OVERVIEW

- TABLE 323 BORER CHEMIE AG: COMPANY OVERVIEW

- TABLE 324 MEDONICA CO. LTD: COMPANY OVERVIEW

- TABLE 325 TUTTNAUER: COMPANY OVERVIEW

- TABLE 326 SHINVA MEDICAL INSTRUMENT CO., LTD.: COMPANY OVERVIEW

- TABLE 327 SBSYSTEM: COMPANY OVERVIEW

- TABLE 328 OLIVE HEALTH CARE: COMPANY OVERVIEW

- TABLE 329 MMM GROUP: COMPANY OVERVIEW

- TABLE 330 AMITY INTERNATIONAL: COMPANY OVERVIEW

- TABLE 331 MIXTA MEDIKAL: COMPANY OVERVIEW

- TABLE 332 MEDICAL DEVICES GROUP SRL: COMPANY OVERVIEW

List of Figures

- FIGURE 1 ENDOSCOPE REPROCESSING MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 ENDOSCOPE REPROCESSING MARKET: YEARS CONSIDERED

- FIGURE 3 ENDOSCOPE REPROCESSING MARKET: RESEARCH DESIGN

- FIGURE 4 ENDOSCOPE REPROCESSING MARKET: KEY DATA FROM SECONDARY SOURCES

- FIGURE 5 ENDOSCOPE REPROCESSING MARKET: KEY PRIMARY SOURCES

- FIGURE 6 ENDOSCOPE REPROCESSING MARKET: KEY INDUSTRY INSIGHTS

- FIGURE 7 BREAKDOWN OF PRIMARY INTERVIEWS: SUPPLY- AND DEMAND-SIDE PARTICIPANTS

- FIGURE 8 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 9 ENDOSCOPE REPROCESSING MARKET: COMPANY REVENUE ESTIMATION, 2024

- FIGURE 10 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- FIGURE 11 ENDOSCOPE REPROCESSING MARKET: TOP-DOWN APPROACH

- FIGURE 12 ENDOSCOPE REPROCESSING MARKET: DATA TRIANGULATION

- FIGURE 13 ENDOSCOPE REPROCESSING MARKET, BY PRODUCT, 2025 VS. 2030 (USD MILLION)

- FIGURE 14 ENDOSCOPE REPROCESSING MARKET, BY TYPE OF ENDOSCOPE, 2025 VS. 2030 (USD MILLION)

- FIGURE 15 ENDOSCOPE REPROCESSING MARKET, BY END USER, 2025 VS. 2030 (USD MILLION)

- FIGURE 16 GEOGRAPHICAL SNAPSHOT OF ENDOSCOPE REPROCESSING MARKET

- FIGURE 17 INCREASING VOLUME OF ENDOSCOPIC PROCEDURES TO DRIVE MARKET

- FIGURE 18 ENDOSCOPE REPROCESSING CONSUMABLES SEGMENT AND JAPAN LED ASIA PACIFIC MARKET IN 2024

- FIGURE 19 GERMANY TO RECORD HIGHEST GROWTH RATE FROM 2025 TO 2030

- FIGURE 20 ASIA PACIFIC TO WITNESS HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 21 EMERGING ECONOMIES TO REGISTER HIGHER GROWTH DURING FORECAST PERIOD

- FIGURE 22 ENDOSCOPE REPROCESSING MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 23 NEW REVENUE POCKETS FOR PLAYERS IN ENDOSCOPE REPROCESSING MARKET

- FIGURE 24 ENDOSCOPE REPROCESSING MARKET: VALUE CHAIN ANALYSIS

- FIGURE 25 ENDOSCOPE REPROCESSING MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 26 ENDOSCOPE REPROCESSING MARKET: ECOSYSTEM ANALYSIS

- FIGURE 27 ENDOSCOPE REPROCESSING MARKET: INVESTMENT AND FUNDING SCENARIO, 2020-2025

- FIGURE 28 ENDOSCOPE REPROCESSING MARKET: PATENT ANALYSIS, JANUARY 2015-DECEMBER 2024

- FIGURE 29 ENDOSCOPE REPROCESSING MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 30 INFLUENCE OF KEY STAKEHOLDERS ON BUYING PROCESS, BY END USER

- FIGURE 31 KEY BUYING CRITERIA, BY END USER

- FIGURE 32 KEY AI USE CASES IN ENDOSCOPE REPROCESSING MARKET

- FIGURE 33 NORTH AMERICA: ENDOSCOPE REPROCESSING MARKET SNAPSHOT

- FIGURE 34 ASIA PACIFIC: ENDOSCOPE REPROCESSING MARKET SNAPSHOT

- FIGURE 35 REVENUE ANALYSIS OF KEY PLAYERS IN ENDOSCOPE REPROCESSING MARKET, 2020-2024

- FIGURE 36 MARKET SHARE ANALYSIS OF KEY PLAYERS IN ENDOSCOPE REPROCESSING MARKET, 2024

- FIGURE 37 EV/EBITDA OF KEY VENDORS, 2025

- FIGURE 38 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS, 2025

- FIGURE 39 ENDOSCOPE REPROCESSING MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 40 ENDOSCOPE REPROCESSING MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 41 ENDOSCOPE REPROCESSING MARKET: COMPANY FOOTPRINT

- FIGURE 42 ENDOSCOPE REPROCESSING MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 43 STERIS: COMPANY SNAPSHOT (2025)

- FIGURE 44 ASP: COMPANY SNAPSHOT (2024)

- FIGURE 45 OLYMPUS CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 46 GETINGE AB: COMPANY SNAPSHOT (2024)

- FIGURE 47 ECOLAB INC.: COMPANY SNAPSHOT (2024)

- FIGURE 48 HOYA CORPORATION: COMPANY SNAPSHOT (2025)

- FIGURE 49 CONMED CORPORATION: COMPANY SNAPSHOT (2024)

自动化内视镜再处理设备市场:2026-2032年全球市场预测(依产品类型、技术、内视镜类型、最终用户和通路划分)

自动化内视镜再处理设备市场:2026-2032年全球市场预测(依产品类型、技术、内视镜类型、最终用户和通路划分) 2026年全球内视镜消毒市场报告

2026年全球内视镜消毒市场报告 自动化医疗清洁消毒设备市场分析及预测(至2035年):按类型、产品、技术、应用、最终用户、流程、组件、功能和安装类型划分

自动化医疗清洁消毒设备市场分析及预测(至2035年):按类型、产品、技术、应用、最终用户、流程、组件、功能和安装类型划分 2026-2034年全球自动化内视镜清洗消毒系统市场规模、份额、趋势及成长分析报告全球自动化内视镜清洗设备(AER)市场:市场规模、占有率、成长率、行业分析、依类型、应用和地区的考察以及未来预测(2026-2034)内视镜清洁消毒设备市场:全球预测(2026-2032 年),依产品类型、技术、应用、最终用户和分销管道划分全球医用清洗消毒机市场:市场规模、市场占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

2026-2034年全球自动化内视镜清洗消毒系统市场规模、份额、趋势及成长分析报告全球自动化内视镜清洗设备(AER)市场:市场规模、占有率、成长率、行业分析、依类型、应用和地区的考察以及未来预测(2026-2034)内视镜清洁消毒设备市场:全球预测(2026-2032 年),依产品类型、技术、应用、最终用户和分销管道划分全球医用清洗消毒机市场:市场规模、市场占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 内视镜再处理市场规模、份额和趋势分析报告:按产品、最终用途、地区和细分市场预测(2026-2033 年)全球医疗器材清洗消毒市场:市场规模、份额和趋势分析(按产品、製程阶段、最终用途和地区划分),细分市场预测(2025-2033 年)2025年内视镜再处理全球市场报告

内视镜再处理市场规模、份额和趋势分析报告:按产品、最终用途、地区和细分市场预测(2026-2033 年)全球医疗器材清洗消毒市场:市场规模、份额和趋势分析(按产品、製程阶段、最终用途和地区划分),细分市场预测(2025-2033 年)2025年内视镜再处理全球市场报告