|

市场调查报告书

商品编码

1822632

软体定义资料中心市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Software-Defined Data Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

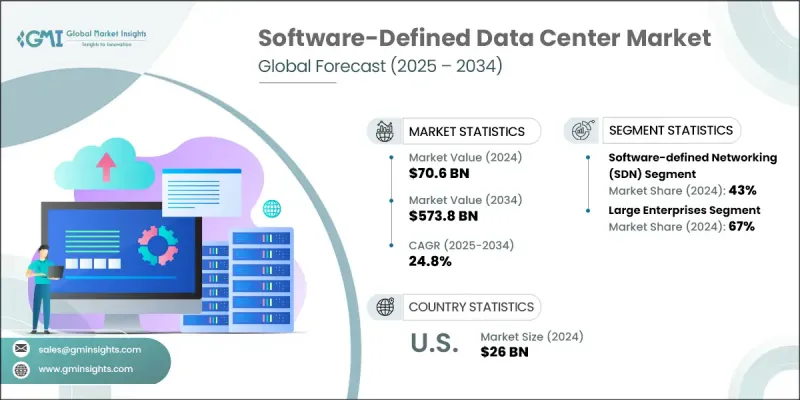

2024 年全球软体定义资料中心市场价值为 706 亿美元,预计到 2034 年将以 24.8% 的复合年增长率成长,达到 5,738 亿美元。

资料中心架构的这种转变正在推动企业设计和管理基础架构方式的重大变革。企业不再只依赖僵化的硬体驱动模式,而是转向软体驱动、敏捷且可扩展的框架。人工智慧、机器学习和基于意图的网路与 SDDC 解决方案的整合正在迅速改变人们的期望。因此,对了解跨领域技术(例如编排、虚拟化和云端原生基础架构)的专业人员的需求日益增长。高级认证和持续培训对于确保最佳性能和营运敏捷性至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 706亿美元 |

| 预测值 | 5738亿美元 |

| 复合年增长率 | 24.8% |

企业数位转型的演变,尤其是在以技术为中心的公私合作领域,正在为软体定义资料中心 (SDDC) 的采用提供更强劲的动力。早在疫情爆发之前,企业就已开始从传统的硬体模式转型为虚拟化、软体定义的环境,以降低成本并提升灵活性。这种转变在电信、金融服务、保险和保险业 (BFSI) 以及超大规模云端服务供应商等产业最为明显。虽然私有云和混合云端模式先前已获得广泛应用,但大规模部署的步伐此前一直受到高昂的前期投资需求和熟练专家短缺的阻碍。然而,自动化和统一基础设施管理的快速发展正在帮助消除这些障碍。

2024年,软体定义网路 (SDN) 占据了43%的市场份额,预计到2034年将以23%的复合年增长率成长。基于人工智慧的自动化技术正在彻底改变SDN,它能够实现即时流量控制、预测性问题检测以及基于即时工作负载的动态网路配置。随着网路变得更加智慧和自主配置,企业正在减少停机时间,同时提升边缘和多云环境下的服务效能。这些进步也有助于减少人工干预,同时增强整个生态系统的可扩展性和网路安全。

大型企业在2024年占了67%的份额,预计在2025年至2034年期间将以20%的复合年增长率成长。这些企业正引领向人工智慧整合分析的转变,这些分析有助于优化工作负载、预测硬体问题并实现自主基础设施管理。随着即时智慧嵌入运算、储存和网路元件,企业正在获得敏捷性和更快的投资回报。这种层级的智慧资源分配支援满足不断变化的业务需求和扩展所需的灵活性,而不受传统系统的限制。

美国软体定义资料中心市场占了90%的市场份额,2024年市场规模达到260亿美元。美国的主导地位得益于其广泛采用的混合云和多云模式、积极的数位基础设施建设以及深厚的供应商生态系统。企业级自动化投资的强劲成长(尤其是在财富500强企业中)也推动了这一成长。此外,科技公司、教育机构和公共部门之间的策略合作正专注于劳动力发展和数位化现代化,从而加快了整体应用步伐。

全球软体定义资料中心市场的主要参与者包括 Nutanix、思科系统、甲骨文、华为、微软、戴尔科技和Google。这些公司在云端原生基础设施、虚拟化环境和人工智慧自动化领域中引领创新。软体定义资料中心市场的顶尖公司正在积极投资人工智慧驱动的基础架构编排、混合云端支援和自动化工作负载管理工具,以使自己脱颖而出。许多公司正在增强与第三方云端平台的互通性,以提供跨公有和私有环境的无缝整合。与学术机构、政府机构和云端原生新创公司的策略合作伙伴关係有助于建立一支熟练的员工队伍并加速技术部署。产品开发现在专注于容器化支援、即时分析和基于意图的网路。此外,华为、微软、Google、甲骨文、思科系统、戴尔科技和 Nutanix 等公司正在优先考虑基于订阅的模式并扩展其 SaaS 产品组合,以提高客户保留率和长期盈利能力。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 对敏捷、可扩展的 IT 基础架构的需求

- 人工智慧与自动化的融合

- 混合云和多云采用

- 资料中心虚拟化的成长

- 产业陷阱与挑战

- 前期投资高

- 安全和合规挑战

- 市场机会

- 边缘运算集成

- 政府主导的数位基础设施计划

- 产业特定的 SDDC 解决方案

- 供应商驱动的培训和认证

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 专利分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 人工智慧与机器学习集成

- AI 驱动的 SDDC 管理与编排

- 机器学习在基础设施自动化的应用

- AIOps 和智慧营运

- 边缘运算和分散式 SDDC

- Edge SDDC 架构与设计

- 5G与物联网集成

- 边缘用例和应用

- 容器和 Kubernetes 的演变

- 容器原生 SDDC 平台

- Kubernetes 编排与管理

- 服务网格和应用程式连接

- 量子运算和下一代技术

- 量子运算与 SDDC 的集成

- 量子安全与加密

- 量子网路与通讯

- 混合经典量子计算

- 永续性和绿色计算

- 节能的 SDDC 设计与营运

- 减少并优化碳足迹

- 再生能源整合

- 循环经济与资源优化

- 人工智慧与机器学习集成

- 价格趋势

- 按地区

- 按产品

- 历史定价分析与市场演变(2019-2024)

- 软体授权成本趋势

- 虚拟机器管理程式和虚拟化许可

- SDN 控制器和网路软体定价

- 储存虚拟化软体成本

- 管理和编排平台定价

- 企业授权协议 (ELA) 趋势

- 硬体成本影响和最佳化

- 每个虚拟机器的伺服器硬体成本

- 储存硬体成本最佳化

- 网路硬体减少的好处

- 商品硬体与专有解决方案

- 硬体更新周期优化

- 服务和支持定价的演变

- 专业服务成本趋势

- 实施和迁移服务定价

- 持续的支援和维护成本

- 培训和认证定价

- 託管服务和外包成本

- 软体授权成本趋势

- 目前 SDDC 定价格局(2024-2025 年)

- 授权模式分析与比较

- 永久许可与订阅许可

- 按插槽定价模型与按核心定价模型

- 基于容量的定价(每 Tb、每 Vm)

- 基于使用情况和消费的定价

- 混合和多云定价模型

- 区域定价差异及分析

- 供应商定价策略分析

- 总拥有成本 (TCO) 和投资报酬率分析

- SDDC 与传统基础设施 TCO 对比

- ROI计算和商业价值

- 成本优化策略

- 授权模式分析与比较

- 未来价格预测与市场趋势(2025-2034)

- 短期价格预测(1-2年)

- 中期价格演变(3-5年)

- 长期价格趋势(5-10年)

- 成本效益分析与财务建模

- 财务论证框架

- 预算规划与分配模型

- 成本中心与利润中心分析

- 退款和展示退款模型

- 财务风险评估与缓解

- 历史定价分析与市场演变(2019-2024)

- 加速数位转型场景

- 市场规模和成长预测

- 科技采用加速

- 行业纵向扩展

- 地理市场开发

- 投资和併购活动

- 人工智慧和自动化革命场景

- AI驱动的SDDC管理

- 自主基础设施运营

- 智慧工作负载优化

- 预测分析和维护

- 新的服务模式和产品

- 边缘运算普及场景

- 分散式 SDDC 架构

- 5G与物联网融合

- 即时处理要求

- 边缘到云端的编排

- 新的市场机会

- 技术突破场景

- 量子计算集成

- 先进的人工智慧和机器学习

- 下一代网路技术

- 永续和绿色计算

- 沉浸式技术(AR/VR/元宇宙)

- 监管和市场演变情景

- 数据主权和本地化要求

- 网路安全法规和标准

- 环境与永续发展任务

- 产业整合与标准化

- 开源和社群驱动的开发

- 战略意义和建议

- 技术投资策略

- 市场进入与扩张规划

- 伙伴关係和生态系统发展

- 创新和研发重点

- 风险缓解和应急计划

- 案例研究

- 企业 SDDC 转型案例研究

- 全球製造业数位转型

- 医疗保健系统 SDDC 和合规性

- 成功案例

- 中小企业和中型市场成功案例

- 政府和公共部门实施

- 产业转型案例

- 能源效率及成本优化案例

- 用例

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 多边环境协定

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按解决方案,2021 - 2034 年

- 主要趋势

- 软体定义网路 (SDN)

- 硬体

- 软体

- 服务

- 託管

- 专业的

- 软体定义储存 (SDS)

- 硬体

- 软体

- 服务

- 託管

- 专业的

- 软体定义计算 (SDC)

- 硬体

- 软体

- 服务

- 託管

- 专业的

第六章:市场估计与预测:依组织规模,2021 - 2034 年

- 主要趋势

- 中小企业

- 大型企业

第七章:市场估计与预测:依最终用途,2021 - 2034

- 主要趋势

- 金融服务业协会

- 零售与电子商务

- 政府

- 卫生保健

- 製造业

- IT支援服务

- 其他的

第 8 章:市场估计与预测:按部署,2021 年至 2034 年

- 主要趋势

- 本地

- 公共云端

- 私有云端

- 混合云端

第九章:市场估计与预测:按应用,2021 - 2034

- 主要趋势

- 资源池化与虚拟化

- 灾难復原和业务连续性

- 资料中心整合

- 动态资源分配

- DevOps 和 CI/CD 自动化

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- 全球参与者

- Advanced Systems Group

- Cisco Systems

- Citrix Systems

- Dell Technologies

- Equinix

- Fujitsu

- Hewlett Packard Enterprise (HPE)

- Hitachi Data Systems

- Huawei

- IBM

- Juniper

- Microsoft

- NEC Corporation of America

- NetApp

- Nutanix

- Red Hat

- VMware

- 区域参与者

- Cloudistics

- DriveScale

- Maxta

- Nexenta Systems

- Pluribus Networks

- QTS Realty Trust

- Rahi Systems

- SUSE

- Super Micro Computer

- Emerging and specialist players

- Atlantis Computing

- Cloudistics

- Maxta

- Cloud and hyperscale players

- Alibaba Cloud

- Amazon Web Services (AWS)

- Huawei Technologies

- Oracle

The Global Software-Defined Data Center Market was valued at USD 70.6 billion in 2024 and is estimated to grow at a CAGR of 24.8% to reach USD 573.8 billion by 2034.

This shift in data center architecture is driving a major transformation in how organizations design and manage infrastructure. Instead of relying solely on rigid, hardware-driven models, businesses are now leaning into software-powered, agile, and scalable frameworks. The integration of AI, machine learning, and intent-based networking into SDDC solutions is rapidly evolving expectations. As a result, there is a growing demand for professionals who understand cross-domain technologies such as orchestration, virtualization, and cloud-native infrastructure. Advanced certifications and ongoing training are becoming essential for ensuring optimal performance and operational agility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $70.6 Billion |

| Forecast Value | $573.8 Billion |

| CAGR | 24.8% |

The evolution of enterprise digital transformation, especially in tech-centric public-private collaborations, is fueling stronger momentum for SDDC adoption. Even before the pandemic, companies began transitioning from traditional hardware-bound models to virtualized, software-defined environments to reduce costs and boost flexibility. This shift has been most evident across sectors such as telecom, BFSI, and hyperscale cloud providers. While private and hybrid cloud models saw earlier traction, the pace of widespread deployment was previously held back by large upfront investment needs and a shortage of skilled experts. However, rapid advancements in automation and unified infrastructure management are helping eliminate these roadblocks.

In 2024, the software-defined networking (SDN) held a 43% share and is anticipated to grow at a CAGR of 23% through 2034. AI-based automation is radically transforming SDN by enabling real-time traffic control, predictive issue detection, and dynamic network configurations based on live workloads. As networks become more intelligent and self-configuring, enterprises are reducing downtime while increasing service performance across edge and multi-cloud setups. These advances are also helping reduce manual intervention while enhancing scalability and cybersecurity throughout the ecosystem.

The large enterprises segment held a 67% share in 2024 and is projected to grow at a 20% CAGR between 2025 and 2034. These businesses are leading the shift toward AI-integrated analytics that help optimize workloads, predict hardware issues, and enable autonomous infrastructure management. With real-time intelligence embedded across compute, storage, and networking components, enterprises are gaining agility and faster ROI. This level of smart resource allocation supports the flexibility needed to meet shifting business demands and scale without the limitations of legacy systems.

United States Software-Defined Data Center Market held a 90% share and generated USD 26 billion in 2024. The US dominance is driven by its widespread adoption of hybrid and multi-cloud models, active digital infrastructure development, and deep vendor ecosystems. The strong presence of enterprise-grade automation investments-especially among Fortune 500 firms-is also pushing this growth. Moreover, strategic collaborations between technology companies, educational institutions, and public sector initiatives are focusing on workforce development and digital modernization, enhancing the overall pace of adoption.

Major players in the Global Software-Defined Data Center Market include Nutanix, Cisco Systems, Oracle, Huawei, Microsoft, Dell Technologies, and Google. These companies are leading innovation across cloud-native infrastructure, virtualized environments, and AI-powered automation. Top companies in the Software-Defined Data Center Market are aggressively investing in AI-driven infrastructure orchestration, hybrid cloud enablement, and automated workload management tools to differentiate themselves. Many are enhancing interoperability with third-party cloud platforms to provide seamless integration across public and private environments. Strategic partnerships with academic institutions, government bodies, and cloud-native startups are helping to build a skilled workforce and accelerate technology deployment. Product development now focuses on containerization support, real-time analytics, and intent-based networking. In addition, players like Huawei, Microsoft, Google, Oracle, Cisco Systems, Dell Technologies, and Nutanix are prioritizing subscription-based models and expanding their SaaS portfolios to improve customer retention and long-term profitability.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Organization size

- 2.2.4 End use

- 2.2.5 Deployment

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Demand for agile, scalable IT infrastructure

- 3.2.1.2 Integration of AI and automation

- 3.2.1.3 Hybrid and multi-cloud adoption

- 3.2.1.4 Data center virtualization growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront investment

- 3.2.2.2 Security and compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Edge computing integration

- 3.2.3.2 Government-led digital infrastructure initiatives

- 3.2.3.3 Industry-specific SDDC solutions

- 3.2.3.4 Vendor-driven training and certification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Patent analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.8.2.1 Artificial intelligence and machine learning integration

- 3.8.2.1.1 AI-powered SDDC management and orchestration

- 3.8.2.1.2 Machine learning for infrastructure automation

- 3.8.2.1.3 AIOps and intelligent operations

- 3.8.2.2 Edge computing and distributed SDDC

- 3.8.2.2.1 Edge SDDC architecture and design

- 3.8.2.2.2 5G and IoT integration

- 3.8.2.2.3 Edge use cases and applications

- 3.8.2.3 Container and Kubernetes evolution

- 3.8.2.3.1 Container-native SDDC platforms

- 3.8.2.3.2 Kubernetes orchestration and management

- 3.8.2.3.3 Service mesh and application connectivity

- 3.8.2.4 Quantum computing and next-generation technologies

- 3.8.2.4.1 Quantum computing integration with SDDC

- 3.8.2.4.2 Quantum-safe security and encryption

- 3.8.2.4.3 Quantum networking and communication

- 3.8.2.4.4 Hybrid classical-quantum computing

- 3.8.2.5 Sustainability and green computing

- 3.8.2.5.1 Energy-efficient SDDC design and operations

- 3.8.2.5.2 Carbon footprint reduction and optimization

- 3.8.2.5.3 Renewable energy integration

- 3.8.2.5.4 Circular economy and resource optimization

- 3.8.2.1 Artificial intelligence and machine learning integration

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.9.2.1 Historical pricing analysis and market evolution (2019-2024)

- 3.9.2.1.1 Software licensing cost trends

- 3.9.2.1.1.1 Hypervisor and virtualization licensing

- 3.9.2.1.1.2 SDN controller and network software pricing

- 3.9.2.1.1.3 Storage virtualization software costs

- 3.9.2.1.1.4 Management and orchestration platform pricing

- 3.9.2.1.1.5 Enterprise license agreement (ELA) trends

- 3.9.2.1.2 Hardware cost impact and optimization

- 3.9.2.1.2.1 Server hardware cost per virtual machine

- 3.9.2.1.2.2 Storage hardware cost optimization

- 3.9.2.1.2.3 Network hardware reduction benefits

- 3.9.2.1.2.4 Commodity hardware vs proprietary solutions

- 3.9.2.1.2.5 Hardware refresh cycle optimization

- 3.9.2.1.3 Service and support pricing evolution

- 3.9.2.1.3.1 Professional services cost trends

- 3.9.2.1.3.2 Implementation and migration service pricing

- 3.9.2.1.3.3 Ongoing support and maintenance costs

- 3.9.2.1.3.4 Training and certification pricing

- 3.9.2.1.3.5 Managed services and outsourcing costs

- 3.9.2.1.1 Software licensing cost trends

- 3.9.2.2 Current SDDC pricing landscape (2024-2025)

- 3.9.2.2.1 Licensing model analysis and comparison

- 3.9.2.2.1.1 Perpetual vs subscription licensing

- 3.9.2.2.1.2 Per-socket vs per-core pricing models

- 3.9.2.2.1.3 Capacity-based pricing (per Tb, per Vm)

- 3.9.2.2.1.4 Usage-based and consumption pricing

- 3.9.2.2.1.5 Hybrid and multi-cloud pricing models

- 3.9.2.2.2 Regional pricing variations and analysis

- 3.9.2.2.3 Vendor pricing strategy analysis

- 3.9.2.2.4 Total cost of ownership (TCO) and ROI analysis

- 3.9.2.2.4.1 SDDC vs traditional infrastructure TCO

- 3.9.2.2.4.2 ROI calculation and business value

- 3.9.2.2.4.3 Cost optimization strategies

- 3.9.2.2.1 Licensing model analysis and comparison

- 3.9.2.3 Future pricing projections and market trends (2025-2034)

- 3.9.2.3.1 Short-term pricing forecast (1-2 years)

- 3.9.2.3.2 Medium-term pricing evolution (3-5 years)

- 3.9.2.3.3 Long-term price trends (5-10 years)

- 3.9.2.4 Cost-benefit analysis and financial modeling

- 3.9.2.4.1 Financial justification frameworks

- 3.9.2.4.2 Budget planning and allocation models

- 3.9.2.4.3 Cost center vs profit center analysis

- 3.9.2.4.4 Chargeback and show back models

- 3.9.2.4.5 Financial risk assessment and mitigation

- 3.9.2.1 Historical pricing analysis and market evolution (2019-2024)

- 3.10 Accelerated digital transformation scenario

- 3.10.1 Market size and growth projections

- 3.10.2 Technology adoption acceleration

- 3.10.3 Industry vertical expansion

- 3.10.4 Geographic market development

- 3.10.5 Investment and M&A activity

- 3.11 AI and automation revolution scenario

- 3.11.1 AI-driven SDDC management

- 3.11.2 Autonomous infrastructure operations

- 3.11.3 Intelligent workload optimization

- 3.11.4 Predictive analytics and maintenance

- 3.11.5 New service models and offerings

- 3.12 Edge computing proliferation scenario

- 3.12.1 Distributed SDDC architecture

- 3.12.2. 5 g and IoT integration

- 3.12.3 Real-time processing requirements

- 3.12.4 Edge-to-cloud orchestration

- 3.12.5 New market opportunities

- 3.13 Technology breakthrough scenarios

- 3.13.1 Quantum computing integration

- 3.13.2 Advanced AI and machine learning

- 3.13.3 Next-generation networking technologies

- 3.13.4 Sustainable and green computing

- 3.13.5 Immersive technologies (AR/VR/metaverse)

- 3.14 Regulatory and market evolution scenarios

- 3.14.1 Data sovereignty and localization requirements

- 3.14.2 Cybersecurity regulations and standards

- 3.14.3 Environmental and sustainability mandates

- 3.14.4 Industry consolidation and standardization

- 3.14.5 Open source and community-driven development

- 3.15 Strategic implications and recommendations

- 3.15.1 Technology investment strategies

- 3.15.2 Market entry and expansion planning

- 3.15.3 Partnership and ecosystem development

- 3.15.4 Innovation and R&D priorities

- 3.15.5 Risk mitigation and contingency planning

- 3.16 Case studies

- 3.16.1 Enterprise SDDC transformation case studies

- 3.16.2 Global manufacturing company digital transformation

- 3.16.3 Healthcare system SDDC and compliance

- 3.17 Success stories

- 3.17.1 SME and mid-market success stories

- 3.17.2 Government and public sector implementations

- 3.17.3 Industry-specific transformation cases

- 3.17.4 Energy efficiency and cost optimization cases

- 3.18 Use cases

- 3.19 Sustainability and environmental aspects

- 3.19.1 Sustainable practices

- 3.19.2 Waste reduction strategies

- 3.19.3 Energy efficiency in production

- 3.19.4 Eco-friendly Initiatives

- 3.19.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Software-defined networking (SDN)

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.2.3.1 Managed

- 5.2.3.2 Professional

- 5.3 Software-defined storage (SDS)

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.3.3.1 Managed

- 5.3.3.2 Professional

- 5.4 Software-defined compute (SDC)

- 5.4.1 Hardware

- 5.4.2 Software

- 5.4.3 Services

- 5.4.3.1 Managed

- 5.4.3.2 Professional

Chapter 6 Market Estimates & Forecast, By Organization size, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 SME

- 6.3 Large enterprises

Chapter 7 Market Estimates & Forecast, By End use, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Retail and e-commerce

- 7.4 Government

- 7.5 Healthcare

- 7.6 Manufacturing

- 7.7 IT-enabled services

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 On-premises

- 8.3 Public cloud

- 8.4 Private cloud

- 8.5 Hybrid cloud

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Resource pooling & virtualization

- 9.3 Disaster recovery & business continuity

- 9.4 Data center consolidation

- 9.5 Dynamic resource allocation

- 9.6 DevOps and CI/CD automation

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Advanced Systems Group

- 11.1.2 Cisco Systems

- 11.1.3 Citrix Systems

- 11.1.4 Dell Technologies

- 11.1.5 Equinix

- 11.1.6 Fujitsu

- 11.1.7 Hewlett Packard Enterprise (HPE)

- 11.1.8 Hitachi Data Systems

- 11.1.9 Huawei

- 11.1.10 IBM

- 11.1.11 Juniper

- 11.1.12 Microsoft

- 11.1.13 NEC Corporation of America

- 11.1.14 NetApp

- 11.1.15 Nutanix

- 11.1.16 Red Hat

- 11.1.17 VMware

- 11.2 Regional players

- 11.2.1 Cloudistics

- 11.2.2 DriveScale

- 11.2.3 Maxta

- 11.2.4 Nexenta Systems

- 11.2.5 Pluribus Networks

- 11.2.6 QTS Realty Trust

- 11.2.7 Rahi Systems

- 11.2.8 SUSE

- 11.2.9 Super Micro Computer

- 11.3 Emerging and specialist players

- 11.3.1 Atlantis Computing

- 11.3.2 Cloudistics

- 11.3.3 Maxta

- 11.4 Cloud and hyperscale players

- 11.4.1 Alibaba Cloud

- 11.4.2 Amazon Web Services (AWS)

- 11.4.3 Google

- 11.4.4 Huawei Technologies

- 11.4.5 Oracle

2026年全球软体定义资料中心市场报告

2026年全球软体定义资料中心市场报告 软体定义资料中心市场:按元件、资料中心类型、应用领域、最终使用者类型、产业和部署方式划分-全球预测,2026-2032年

软体定义资料中心市场:按元件、资料中心类型、应用领域、最终使用者类型、产业和部署方式划分-全球预测,2026-2032年 软体定义资料中心市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

软体定义资料中心市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 软体定义资料中心市场 - 全球产业规模、份额、趋势、机会及预测(按组件、类型、部署方式、垂直产业、地区和竞争格局划分),2021-2031年

软体定义资料中心市场 - 全球产业规模、份额、趋势、机会及预测(按组件、类型、部署方式、垂直产业、地区和竞争格局划分),2021-2031年 2026-2030年全球软体定义资料中心(SDDC)市场

2026-2030年全球软体定义资料中心(SDDC)市场 软体定义资料中心市场规模、份额和成长分析(按组件、部署模式、企业规模、垂直产业和地区划分)-2026年至2033年产业预测

软体定义资料中心市场规模、份额和成长分析(按组件、部署模式、企业规模、垂直产业和地区划分)-2026年至2033年产业预测 全球软体定义资料中心(SDDC)市场:依产品、组织规模、最终用户产业、地区、机会和预测,2018-2032

全球软体定义资料中心(SDDC)市场:依产品、组织规模、最终用户产业、地区、机会和预测,2018-2032 全球软体定义资料中心市场规模、份额和趋势分析:按组件、类型、部署、企业规模、最终用途、地区和细分市场,预测 2025-2033 年

全球软体定义资料中心市场规模、份额和趋势分析:按组件、类型、部署、企业规模、最终用途、地区和细分市场,预测 2025-2033 年 2032 年软体定义资料中心市场预测:按类型、组件、组织规模、部署类型、最终用户和地区进行的全球分析

2032 年软体定义资料中心市场预测:按类型、组件、组织规模、部署类型、最终用户和地区进行的全球分析 全球软体定义资料中心市场规模(按组件、服务、部署模型、区域覆盖范围和预测):

全球软体定义资料中心市场规模(按组件、服务、部署模型、区域覆盖范围和预测):