|

市场调查报告书

商品编码

1833436

女性健康治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Womens Health Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

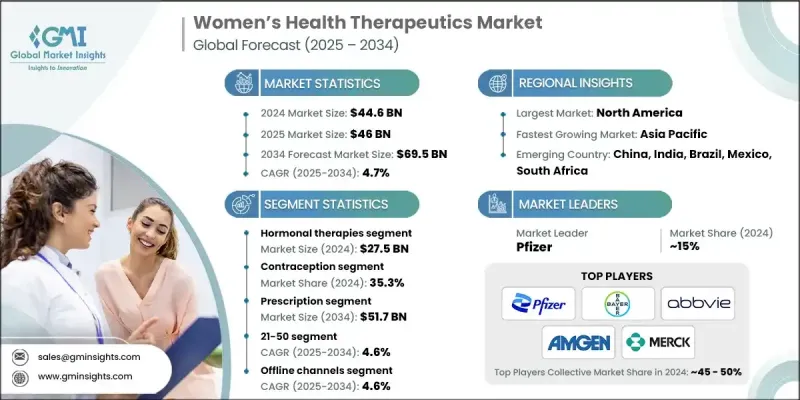

2024 年全球女性健康治疗市场价值为 446 亿美元,预计到 2034 年将以 4.7% 的复合年增长率增长至 695 亿美元。

子宫内膜异位症、更年期相关问题、多囊性卵巢症候群 (PCOS) 和骨质疏鬆症等疾病日益常见。日益加重的疾病负担推动了对更有效、更有针对性的治疗方法的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 446亿美元 |

| 预测值 | 695亿美元 |

| 复合年增长率 | 4.7% |

荷尔蒙疗法的采用率不断提高

2024年,荷尔蒙疗法领域占据了相当大的份额,这得益于针对更年期症状、子宫内膜异位症和荷尔蒙失衡等疾病的治疗需求不断增长。随着人们对荷尔蒙替代疗法 (HRT) 以及未经治疗的荷尔蒙问题的长期健康影响的认识不断提高,越来越多的女性正在寻求医疗干预。市场在给药机制方面不断创新,包括贴片、凝胶和缓释植入物,从而提高了患者的依从性。

避孕普及率不断上升

2024年,避孕市场占据了相当大的份额,这得益于对长效可逆避孕药 (LARC) 和非荷尔蒙避孕药需求的不断增长。现代生活方式、推迟计划生育以及公共卫生部门对生殖自主权日益增长的支持,推动了广泛人群对避孕药的采用。随着阴道环、子宫内避孕器 (IUD) 和注射剂型的创新,避孕市场正在超越传统的口服避孕药。

获得牵引力的处方

处方药市场在2024年占据了相当大的份额,这得益于骨质疏鬆症、生育问题和妇科癌症等疾病的大多数治疗都具有临床性质。医生仍然是关键的决策者,患者对处方药的信任度继续推动品牌忠诚度。监管审批途径、处方集定位和保险覆盖范围对此领域的销售业绩有显着影响。

北美将成为推动力地区

2025-2034年期间,北美女性健康治疗市场可望实现可观的复合年增长率。该地区受益于先进的医疗基础设施、强有力的监管以及患者和医疗机构的高度认知。市场参与者正在利用优惠的报销政策以及对女性生命週期各个阶段(从青春期到更年期后)的针对性治疗日益增长的需求。

女性健康治疗市场的主要参与者有 Theramex、Cipla、Kissei Pharmaceutical、Evofem、辉瑞、Shionogi、Ferring、Organon、安进、Besins、Allergan (AbbVie)、赛诺菲、Gedeon Richter、Lupin、Atossa Therapeutics、诺华、强生和拜耳。

为了巩固在女性健康治疗领域的市场地位,各公司正采取多管齐下的策略。关键策略包括透过内部研发和许可交易来扩大产品线,尤其针对子宫肌瘤和女性性功能障碍等医疗资源匮乏的疾病。此外,各公司也利用併购来巩固市场地位并获得创新技术。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 慢性病和生活方式疾病盛行率上升

- 加强教育和公共卫生活动

- 个人化医疗日益进步

- 对月经健康和卫生疗法的需求不断增加

- 产业陷阱与挑战

- 月经、不孕和更年期的社会耻辱

- 治疗费用高

- 监管挑战

- 市场机会

- 新兴市场的扩张

- 预防性女性保健日益受到关注

- 成长动力

- 成长潜力分析

- 监管格局

- 管道分析

- 女性健康领域的投资与融资格局

- 技术格局

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按药物类型,2021 - 2034 年

- 主要趋势

- 荷尔蒙疗法

- 疼痛和症状管理药物

- GnRH调节剂

- 骨骼健康剂

- 代谢药物

- 生育药物

- 其他药物类型

第六章:市场估计与预测:按应用,2021 - 2034

- 主要趋势

- 避孕

- 更年期和停经后管理

- 荷尔蒙失调

- 子宫内膜异位症和子宫肌瘤

- 生殖健康及生育保健

- 骨骼健康与骨质疏鬆症

- 其他应用

第七章:市场估计与预测:按药物类型,2021 - 2034

- 主要趋势

- 场外交易(OTC)

- 处方

第八章:市场估计与预测:按年龄组,2021 - 2034 年

- 主要趋势

- 20岁以下

- 21-50

- 51岁以上

第九章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 线下通路

- 医院药房

- 零售药局

- 其他线下门市

- 线上通路

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Allergan (AbbVie)

- Amgen

- Atossa Therapeutics

- Bayer

- Besins

- Cipla

- Evofem

- Ferring

- Gedeon Richter

- Johnson & Johnson

- Kissei Pharmaceutical

- Lupin

- Novartis

- Organon

- Pfizer

- Sanofi

- Shionogi

- Theramex

The Global Womens Health Therapeutics Market was valued at USD 44.6 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 69.5 billion by 2034.

Conditions like endometriosis, menopause-related issues, polycystic ovary syndrome (PCOS), and osteoporosis is increasingly common. This growing disease burden is pushing demand for more effective and targeted therapeutics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $44.6 Billion |

| Forecast Value | $69.5 Billion |

| CAGR | 4.7% |

Increasing Adoption of Hormonal Therapies

The hormonal therapies segment held a significant share in 2024, driven by the rising demand for treatments that address conditions such as menopause symptoms, endometriosis, and hormonal imbalances. As awareness grows around hormone replacement therapy (HRT) and the long-term health impacts of untreated hormonal issues, more women are seeking medical intervention. The market has seen continuous innovation in delivery mechanisms, including patches, gels, and sustained-release implants, which enhance patient compliance.

Rising Prevalence of Contraception

The contraception segment generated a sizeable share in 2024, driven by rising demand for both long-acting reversible contraceptives (LARCs) and non-hormonal options. Modern lifestyles, delayed family planning, and growing public health support for reproductive autonomy have fueled adoption across a broad demographic. The market is evolving beyond traditional oral contraceptives, with innovations in vaginal rings, intrauterine devices (IUDs), and injectable formats.

Prescription to Gain Traction

The prescription segment held a substantial share in 2024, owing to the clinical nature of most treatments for conditions like osteoporosis, fertility issues, and gynecological cancers. Physicians remain key decision-makers, and patient trust in prescribed medications continues to drive brand loyalty. Regulatory approval pathways, formulary positioning, and insurance coverage significantly impact sales performance in this segment.

North America to Emerge as a Propelling Region

North America womens health therapeutics market is poised to grow at a decent CAGR during 2025-2034. The region benefits from advanced healthcare infrastructure, strong regulatory oversight, and high awareness levels among both patients and providers. Market players are capitalizing on favorable reimbursement policies and rising demand for targeted treatments across various stages of a woman's life cycle, from adolescence to post-menopause.

Major players in the women's health therapeutics market are Theramex, Cipla, Kissei Pharmaceutical, Evofem, Pfizer, Shionogi, Ferring, Organon, Amgen, Besins, Allergan (AbbVie), Sanofi, Gedeon Richter, Lupin, Atossa Therapeutics, Novartis, Johnson & Johnson, and Bayer.

To strengthen their market foothold in the women's health therapeutics space, companies are focusing on a multi-pronged approach. Key strategies include expanding product pipelines through in-house R&D and licensing deals, particularly for underserved conditions such as uterine fibroids and female sexual dysfunction. Mergers and acquisitions are also being used to consolidate market presence and gain access to innovative technologies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug type

- 2.2.3 Application

- 2.2.4 Medication type

- 2.2.5 Age group

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic and lifestyle diseases

- 3.2.1.2 Enhanced education and public health campaigns

- 3.2.1.3 Growing advancement in personalized medicine

- 3.2.1.4 Increasing demand for menstrual health and hygiene therapeutics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Social stigma around menstruation, infertility, and menopause

- 3.2.2.2 High treatment cost

- 3.2.2.3 Regulatory challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Growing focus on preventive women's healthcare

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Pipeline analysis

- 3.6 Investment and funding landscape in the women's health sector

- 3.7 Technological landscape

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hormonal therapies

- 5.3 Pain and symptom management drugs

- 5.4 GnRH modulators

- 5.5 Bone health agents

- 5.6 Metabolic drugs

- 5.7 Fertility drugs

- 5.8 Other drug types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Contraception

- 6.3 Menopause and post-menopausal management

- 6.4 Hormonal disorders

- 6.5 Endometriosis and uterine fibroids

- 6.6 Reproductive health and fertility care

- 6.7 Bone health and osteoporosis

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By Medication Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Over the counter (OTC)

- 7.3 Prescription

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Below 20

- 8.3 21-50

- 8.4 51 and above

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Offline channels

- 9.2.1 Hospital pharmacies

- 9.2.2 Retail pharmacies

- 9.2.3 Other offline stores

- 9.3 Online channels

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Allergan (AbbVie)

- 11.2 Amgen

- 11.3 Atossa Therapeutics

- 11.4 Bayer

- 11.5 Besins

- 11.6 Cipla

- 11.7 Evofem

- 11.8 Ferring

- 11.9 Gedeon Richter

- 11.10 Johnson & Johnson

- 11.11 Kissei Pharmaceutical

- 11.12 Lupin

- 11.13 Novartis

- 11.14 Organon

- 11.15 Pfizer

- 11.16 Sanofi

- 11.17 Shionogi

- 11.18 Theramex

全球女性健康照护市场规模、份额、趋势和成长分析报告(2026-2034)

全球女性健康照护市场规模、份额、趋势和成长分析报告(2026-2034) 女性健康照护市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、最终使用者、设备、功能及解决方案划分全球女性健康治疗市场规模、份额、趋势和成长分析报告(2026-2034)

女性健康照护市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、最终使用者、设备、功能及解决方案划分全球女性健康治疗市场规模、份额、趋势和成长分析报告(2026-2034) 全球女性用荷尔蒙平衡和经期健康产品市场预测(至2032年):按产品、配方、成分类型、分销管道、应用、最终用户和地区划分

全球女性用荷尔蒙平衡和经期健康产品市场预测(至2032年):按产品、配方、成分类型、分销管道、应用、最终用户和地区划分 女性健康市场-全球产业规模、份额、趋势、机会及预测(按药物、应用、地区和竞争格局划分,2021-2031年)女性健康照护市场-全球产业规模、份额、趋势、机会和预测:按药物、应用、地区和竞争格局划分,2021-2031年全球孕产妇健康治疗市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考量因素以及未来预测(2026-2034)

女性健康市场-全球产业规模、份额、趋势、机会及预测(按药物、应用、地区和竞争格局划分,2021-2031年)女性健康照护市场-全球产业规模、份额、趋势、机会和预测:按药物、应用、地区和竞争格局划分,2021-2031年全球孕产妇健康治疗市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考量因素以及未来预测(2026-2034) 日本女性健康市场报告(按年龄组类型、应用、配销通路和地区划分,2026-2034 年)

日本女性健康市场报告(按年龄组类型、应用、配销通路和地区划分,2026-2034 年) 女性健康治疗市场规模、份额和成长分析(按年龄、药物、通路、应用和地区划分)-2026-2033年产业预测

女性健康治疗市场规模、份额和成长分析(按年龄、药物、通路、应用和地区划分)-2026-2033年产业预测 女性健康消费品市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

女性健康消费品市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)