|

市场调查报告书

商品编码

1858799

热管理领域相变材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Phase Change Materials in Thermal Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

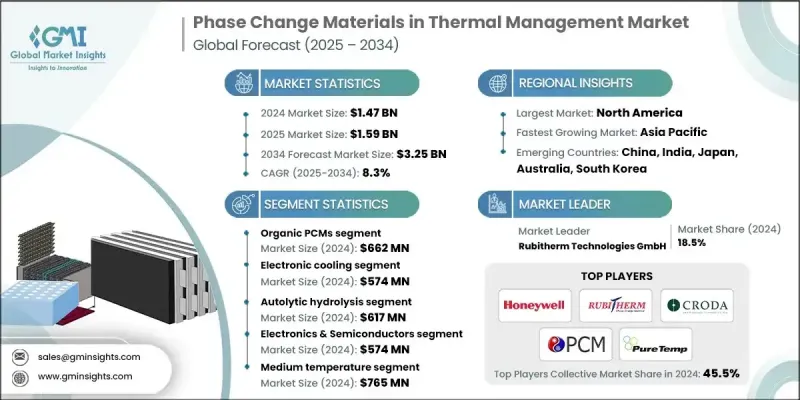

2024 年全球热管理相变材料市场价值为 14.7 亿美元,预计到 2034 年将以 8.3% 的复合年增长率增长至 32.5 亿美元。

市场专注于开发和应用能够在熔化或凝固等状态变化过程中储存、吸收和释放热能的材料。这些材料广泛应用于电子、汽车和建筑等领域,有助于调节温度并提高能源效率。各行业对高效热控制日益增长的需求是相变材料(PCM)技术的主要成长动力。全球对高性能热调节系统的需求不断增长,这些系统能够支援更小巧、更强大的电子设备、永续建筑和先进的汽车系统。奈米增强型PCM和微胶囊化等创新技术显着提高了材料的耐久性、导热性和整合潜力,从而改善了传热性能和生命週期性能。这些改进使PCM更具吸引力,可用于印刷电路板、电池、散热器等设备的集成,从而在对热要求极高的应用领域得到更广泛的应用。市场成长反映了人们向更智慧的能源利用和更优化的热管理迈进的趋势。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 14.7亿美元 |

| 预测值 | 32.5亿美元 |

| 复合年增长率 | 8.3% |

2024年,有机相变材料(PCM)市场规模预计将达到6.62亿美元。其强劲的市场地位源自于其可靠的热性能、优异的潜热储存能力和长期的化学稳定性,这些特性对于电子元件冷却和建筑热调节等领域至关重要。石蜡基相变材料因其熔点范围宽广而被广泛应用,而脂肪酸和醇基相变材料则因其在汽车和电子应用中的循环稳定性而备受关注,这些应用需要反覆进行相变而不发生材料分解。

2024年,电子冷却领域市场规模预计将达到5.74亿美元,反映出控制紧凑型高密度设备产生的热量的压力日益增大。随着设备尺寸缩小和功耗增加,控制热峰值和维持安全的工作温度变得至关重要。微封装相变材料(PCM)专为电子组件应用而设计,可无缝整合到对热敏感的系统中,而不会影响结构完整性或电气性能。

2024年,美国相变材料(PCM)在热管理领域的市场规模达到3.78亿美元。这一领先地位归功于美国强大的工业实力以及政府支持的旨在提高建筑和製造业效率的能源计划。鼓励永续建筑实践和采用先进节能技术的政策,为PCM的市场发展奠定了坚实的基础。此外,美国先进的汽车和电子产业也不断寻求新的热调节解决方案,进一步推动了PCM的应用。

全球相变材料热管理市场主要的活跃企业包括:Cryopak Industries Inc.、Sonoco ThermoSafe、Climate Change Materials、AeroSafe Global、Pelican BioThermal、Rubitherm Technologies GmbH、Pluss Advanced Technologies Pvt. Ltd.、Cold Chain Technologies、Entropy Solutions Inc./PureTemp LLC、Cowabt. Ltd.、Cold Chain Technologies. Inc.、va-Q-tec、Salca BV、Outlast Technologies LLC、Datum Phase Change、PCM Energy Pvt. Ltd./Teappcm、Nanolope、Phase Change Material Products Limited (PlusICE)、Advanced Cooling Technologies Inc.、Mesa Laboratories Inc。 Plc。这些企业正采取一系列策略来扩大市场份额并保持竞争力。许多企业正投资研发奈米增强型或生物基相变材料等先进配方,以提高导热性、减少环境影响并增强循环耐久性。与电子和汽车原始设备製造商 (OEM) 的策略合作,使得相变材料解决方案更容易整合到高性能係统中。此外,领先的製造商正在扩大产能并实现生产自动化,以满足日益增长的全球需求。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 电子产品小型化所带来的需求不断成长

- 电动汽车热管理领域的成长

- 技术进步提升了相变材料(PCM)的性能

- 专注于建筑物的能源效率

- 产业陷阱与挑战

- 高昂的生产和整合成本

- 材料稳定性与生命週期问题

- 市场机会

- 电动汽车应用领域的扩展

- 融入再生能源系统

- 智慧建筑材料的进步

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依材料类型

- 未来市场趋势

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依材料类型划分,2021-2034年

- 主要趋势

- 有机相变材料

- 石蜡

- 脂肪酸

- 非石蜡有机物

- 无机相变材料

- 盐水合物

- 金属合金

- 共晶盐

- 生物基相变材料

- 植物性化合物

- 天然脂肪酸

- 复合型和增强型相变材料

- 奈米增强型

- 石墨增强型

- 金属泡沫复合材料

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 建筑施工

- 暖通空调系统

- 墙板和石膏

- 混凝土及结构

- 隔热与建筑

- 电子冷却

- 半导体热学

- 资料中心冷却

- 消费性电子产品

- 电力电子冷却

- 电池热

- 电动汽车电池

- 电网储能

- 便携式设备电池

- 汽车

- 引擎热

- 客舱舒适度

- 电动汽车热管理

- 纺织品和穿戴式设备

- 冷链与物流

第七章:市场估计与预测:依外型尺寸划分,2021-2034年

- 主要趋势

- 散装及原料相变材料

- 微胶囊化

- 聚合物壳封装

- 无机壳封装

- 宏观封装

- 基于容器的

- 面板和管

- 形状稳定

- 多孔支撑体

- 复合基体

第八章:市场估算与预测:依最终用途产业划分,2021-2034年

- 主要趋势

- 建筑材料

- 电子与半导体

- 汽车与运输

- 能源与公用事业

- 航太与国防

- 医疗保健与製药

第九章:市场估计与预测:依温度范围划分,2021-2034年

- 主要趋势

- 低温相变材料(-50°C 至 15°C)

- 舒适范围相变材料(15°C 至 32°C)

- 中温相变材料(32°C 至 100°C)

- 高温相变材料(100°C 至 800°C)

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十一章:公司简介

- AeroSafe Global

- Advanced Cooling Technologies Inc.

- Axiotherm GmbH

- Climator Sweden AB

- Climate Change Materials

- Cold Chain Technologies

- Croda International Plc

- Cowa Thermal Solutions

- Datum Phase Change

- Entropy Solutions Inc./PureTemp LLC

- Honeywell International Inc.

- i-TES

- Microtek Laboratories Inc.

- Mesa Laboratories Inc.

- Nanolope

- Outlast Technologies LLC

- Pelican BioThermal

- Phase Change Energy Solutions

- Phase Change Material Products Limited (PlusICE)

- Pluss Advanced Technologies Pvt. Ltd.

- PCM Energy Pvt. Ltd./Teappcm

- Rubitherm Technologies GmbH

- Salca BV

- Sonoco ThermoSafe

- Sunamp

- Tetramer Technologies

- va-Q-tec

- Cryopak Industries Inc.

The Global Phase Change Materials in Thermal Management Market was valued at USD 1.47 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 3.25 billion by 2034.

The market focuses on the development and deployment of materials capable of storing, absorbing, and releasing thermal energy during state changes such as melting or solidifying. These materials are widely applied in sectors like electronics, automotive, and buildings, helping regulate temperature while improving energy efficiency. The increasing need for efficient thermal control across industries is a major growth driver for PCM technologies. Global demand is rising for high-performance thermal regulation systems that support smaller, more powerful electronic devices, sustainable buildings, and advanced automotive systems. Innovations like nano-enhanced PCMs and microencapsulation have significantly boosted durability, thermal conductivity, and integration potential, improving heat transfer and lifecycle performance. These improvements have made PCMs more attractive for integration in printed circuit boards, batteries, heat sinks, and more, enabling wider adoption across thermal-critical applications. The market's growth reflects the broader push toward smarter energy use and optimized heat management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.47 Billion |

| Forecast Value | $3.25 Billion |

| CAGR | 8.3% |

The organic PCMs segment generated USD 662 million in 2024. Their strong position comes from their reliable thermal characteristics, excellent latent heat storage capacity, and long-term chemical stability, all of which are essential in areas like electronic component cooling and thermal regulation in buildings. Paraffin-based PCMs are widely used due to their broad melting point range, while fatty acids and alcohol-based PCMs are gaining recognition for their cycling stability in automotive and electronics applications that demand repetitive phase transitions without material breakdown.

The electronics cooling segment generated USD 574 million in 2024, reflecting the increasing pressure to manage heat generated by compact, high-density devices. As devices shrink and power demands rise, managing heat spikes and maintaining safe operational temperatures becomes essential. Microencapsulated PCMs are tailored for use within electronic assemblies, offering seamless integration into heat-sensitive systems without compromising structural integrity or electrical performance.

US Phase Change Materials in Thermal Management Market generated USD 378 million in 2024. This leadership is attributed to strong industrial capabilities and government-backed energy initiatives aimed at improving efficiency in construction and manufacturing. Policies encouraging sustainable building practices and the adoption of advanced energy-saving technologies have given PCMs a significant foothold. Additionally, the country's advanced automotive and electronics sectors consistently seek out new solutions for thermal regulation, further driving PCM adoption.

Top companies active in the Global Phase Change Materials in Thermal Management Market are Cryopak Industries Inc., Sonoco ThermoSafe, Climate Change Materials, AeroSafe Global, Pelican BioThermal, Rubitherm Technologies GmbH, Pluss Advanced Technologies Pvt. Ltd., Cold Chain Technologies, Entropy Solutions Inc./PureTemp LLC, Cowa Thermal Solutions, Tetramer Technologies, Microtek Laboratories Inc., va-Q-tec, Salca BV, Outlast Technologies LLC, Datum Phase Change, PCM Energy Pvt. Ltd./Teappcm, Nanolope, Phase Change Material Products Limited (PlusICE), Advanced Cooling Technologies Inc., Mesa Laboratories Inc., Phase Change Energy Solutions, i-TES, Honeywell International Inc., Climator Sweden AB, Axiotherm GmbH, and Croda International Plc. Companies in the Phase Change Materials in Thermal Management Market are adopting a range of strategies to expand their market reach and stay competitive. Many are investing in advanced formulations such as nano-enhanced or bio-based PCMs to improve thermal conductivity, reduce environmental impact, and enhance cycling durability. Strategic collaborations with electronics and automotive OEMs are enabling easier integration of PCM solutions into high-performance systems. Additionally, leading manufacturers are expanding production capabilities and automating fabrication to meet growing global demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Material type

- 2.2.2 Application

- 2.2.3 Form factor

- 2.2.4 End Use Industry

- 2.2.5 Temperature Range

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Rising demand from electronics miniaturization

- 3.2.3 Growth in electric vehicle thermal management

- 3.2.4 Technological advancements boosting PCM performance

- 3.2.5 Focus on energy efficiency in buildings

- 3.3 Industry pitfalls and challenges

- 3.3.1 High production and integration costs

- 3.3.2 Material stability and lifecycle concerns

- 3.4 Market opportunities

- 3.4.1 Expansion in electric vehicle applications

- 3.4.2 Integration in renewable energy systems

- 3.4.3 Advancements in smart building materials

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By material type

- 3.11 Future market trends

- 3.12 Patent landscape

- 3.13 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.13.1 Major importing countries

- 3.13.2 Major exporting countries

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.15 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Organic PCMs

- 5.2.1 Paraffin waxes

- 5.2.2 Fatty acids

- 5.2.3 Non-paraffin organics

- 5.3 Inorganic PCMs

- 5.3.1 Salt hydrates

- 5.3.2 Metallic alloys

- 5.3.3 Eutectic salts

- 5.4 Bio-based PCMs

- 5.4.1 Vegetable-based compounds

- 5.4.2 Natural fatty acids

- 5.5 Composite & Enhanced PCMs

- 5.5.1 Nano-enhanced

- 5.5.2 Graphite-enhanced

- 5.5.3 Metal foam composites

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Building & construction

- 6.2.1 HVAC systems

- 6.2.2 Wallboard & gypsum

- 6.2.3 Concrete & structural

- 6.2.4 Insulation & building

- 6.3 Electronics cooling

- 6.3.1 Semiconductor thermal

- 6.3.2 Data center cooling

- 6.3.3 Consumer electronics

- 6.3.4 Power electronics cooling

- 6.4 Battery thermal

- 6.4.1 Electric vehicle battery

- 6.4.2 Grid energy storage

- 6.4.3 Portable device batteries

- 6.5 Automotive

- 6.5.1 Engine thermal

- 6.5.2 Cabin comfort

- 6.5.3 EV thermal

- 6.6 Textiles & wearables

- 6.7 Cold chain & logistics

Chapter 7 Market Estimates and Forecast, By Form Factor, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bulk & raw PCMs

- 7.3 Microencapsulated

- 7.3.1 Polymer-shell encapsulation

- 7.3.2 Inorganic shell encapsulation

- 7.4 Macroencapsulated

- 7.4.1 Container-based

- 7.4.2 Panel & tube

- 7.5 Shape-stabilized

- 7.5.1 Porous support

- 7.5.2 Composite matrix

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Construction & building materials

- 8.3 Electronics & semiconductors

- 8.4 Automotive & transportation

- 8.5 Energy & utilities

- 8.6 Aerospace & defense

- 8.7 Healthcare & pharmaceuticals

Chapter 9 Market Estimates and Forecast, By Temperature range, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Low Temperature PCMs (-50°C to 15°C)

- 9.3 Comfort Range PCMs (15°C to 32°C)

- 9.4 Medium Temperature PCMs (32°C to 100°C)

- 9.5 High Temperature PCMs (100°C to 800°C)

Chapter 10 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 AeroSafe Global

- 11.2 Advanced Cooling Technologies Inc.

- 11.3 Axiotherm GmbH

- 11.4 Climator Sweden AB

- 11.5 Climate Change Materials

- 11.6 Cold Chain Technologies

- 11.7 Croda International Plc

- 11.8 Cowa Thermal Solutions

- 11.9 Datum Phase Change

- 11.10 Entropy Solutions Inc./PureTemp LLC

- 11.11 Honeywell International Inc.

- 11.12 i-TES

- 11.13 Microtek Laboratories Inc.

- 11.14 Mesa Laboratories Inc.

- 11.15 Nanolope

- 11.16 Outlast Technologies LLC

- 11.17 Pelican BioThermal

- 11.18 Phase Change Energy Solutions

- 11.19 Phase Change Material Products Limited (PlusICE)

- 11.20 Pluss Advanced Technologies Pvt. Ltd.

- 11.21 PCM Energy Pvt. Ltd./Teappcm

- 11.22 Rubitherm Technologies GmbH

- 11.23 Salca BV

- 11.24 Sonoco ThermoSafe

- 11.25 Sunamp

- 11.26 Tetramer Technologies

- 11.27 va-Q-tec

- 11.28 Cryopak Industries Inc.

生物基相变材料市场规模、份额和成长分析:按产品类型、应用、最终用户和地区划分-2026-2033年产业预测

生物基相变材料市场规模、份额和成长分析:按产品类型、应用、最终用户和地区划分-2026-2033年产业预测 2026年全球相变材料市场报告

2026年全球相变材料市场报告 相变材料市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年

相变材料市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年 家用电器相变材料市场(按产品类型、技术、电源、分销管道和最终用户划分)—2026-2032年全球预测相变润滑脂市场依产品类型、应用、终端用户产业及通路划分-2026年至2032年全球预测

家用电器相变材料市场(按产品类型、技术、电源、分销管道和最终用户划分)—2026-2032年全球预测相变润滑脂市场依产品类型、应用、终端用户产业及通路划分-2026年至2032年全球预测 相变材料(PCM)市场规模、份额和成长分析(按类型、应用、终端用户产业、类型和地区划分)-2026-2033年产业预测

相变材料(PCM)市场规模、份额和成长分析(按类型、应用、终端用户产业、类型和地区划分)-2026-2033年产业预测 相变材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

相变材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球相变材料市场按类型、应用和地区划分-预测至2030年

全球相变材料市场按类型、应用和地区划分-预测至2030年 相变材料市场:依产品类型、化学成分、封装技术、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测相变材料(PCM)市场按应用、类型、最终用途和形态划分-全球预测,2025-2032年

相变材料市场:依产品类型、化学成分、封装技术、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测相变材料(PCM)市场按应用、类型、最终用途和形态划分-全球预测,2025-2032年