|

市场调查报告书

商品编码

1851469

相变材料:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Phase Change Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

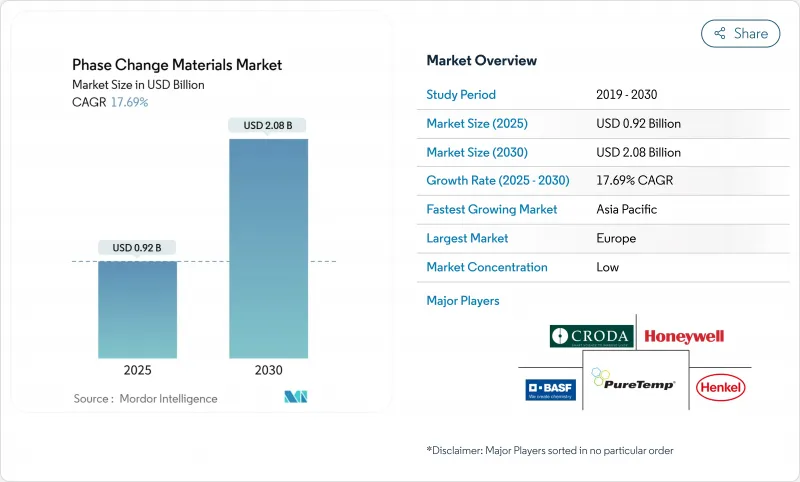

相变材料市场规模预计到 2025 年将达到 9.2 亿美元,预计到 2030 年将达到 20.8 亿美元,在预测期(2025-2030 年)内复合年增长率为 17.69%。

持续高温、净零排放建筑目标以及交通运输的快速电气化,使得潜热储存成为商业能源策略的核心。低温运输物流和电动车电池组也正在拓展这项技术的应用范围,涵盖交通运输、製药和资料中心冷却等领域。盐水合物长期以来受限于相分离和过冷问题,但随着近期导电性能的突破,其应用前景日益广阔。同时,源自农业废弃物的生物基相变材料在不牺牲热容量的前提下,解决了防火安全和永续性问题,正从实验室研究走向可规模化商业化产品。在亚太地区,高纯度盐水合物正成为产能扩张的关键,製造商纷纷增设本地生产线以规避相关的供应链风险。

全球相变材料市场趋势与洞察

强制性建筑节能规范加速了相变材料(PCM)的集成

基于性能的合规标准允许建筑师以潜热储存层替代刚性隔热材料,从而将轻质墙体的峰值冷却负荷降低35%至45%。明尼苏达州的测量结果显示,室内高峰温度降低了摄氏5.49度,并且77.8%的负荷转移到了非尖峰时段,这为监管机构提供了暖通空调系统节能的实际证据。预计为实现欧盟2027年维修目标,更高的合规基准值将更加重视相变材料填充的石膏板和混凝土块,从而增加整个相变材料市场的采购量。

低温运输物流基础设施快速发展

疫苗、先进生技药品和精准肉类通常需要温度范围在三天内仅能承受±0.5°C偏差的温度区域。相变材料(PCM)无需外部电源即可将这种耐受性延长至72小时,从而减少机场和海关延误期间对柴油发电机的依赖。与主动冷却相比,甘油-水-氯化钠混合物可减少30-40%的碳排放,并将药品保质期延长15-25%,推动相变材料市场出现两位数成长。

相变材料的危险特性

石蜡的燃点约为170 ℃,需要使用溴化阻燃剂,这会增加成本,并可能引发健康标籤法规的限制。无机阻燃剂,例如硝酸锂(LiNO3),则有毒性风险。近年来,原位聚合的固体-固体材料(PCM)无需卤素即可消除洩漏并达到UL94 V-0阻燃标准。其更广泛的应用取决于封装技术的进步以及全球化学品安全标准的统一。

细分市场分析

有机石蜡仍将是相变材料市场的主要收入来源,预计2024年将占全球收入的44.19%。其市场主导地位源自于其成熟的供应链、宽广的温度范围以及与建筑板材中使用的大分子胶囊化板材的兼容性。然而,随着相关人员寻求减少生命週期排放,相变材料市场正迅速转向生物基油、牛油和脂肪酸混合物。在LEED认证积分和政府绿色采购政策的推动下,这个新兴细分市场预计将以19.21%的复合年增长率成长,到2030年将超越竞争对手,这些政策明确支持生物来源材料。

由于石蜡基配方具有稳定的结晶性和易于调节的0-90°C熔点范围,预计到2024年将占据相变材料市场收入的41.49%。然而,盐水合物有望崩坏这一格局,预计到2030年将以18.04%的复合年增长率成长。盐水合物具有高体积比热容(高达350 kJ/L)以及碳添加剂带来的导热性提升,因此能够减少组件的尺寸和重量。由此带来的密度优势对于电动车电池套管和空间有限的紧凑型资料中心机架尤为重要。

区域分析

2024年,欧洲将占全球销售额的32.86%,这主要得益于欧盟《建筑能源性能指令》(EPBD),该指令强制要求新建建筑和大型维修均达到接近净零能耗的目标。德国和斯堪的纳维亚半岛的先驱已证明,将相变材料(PCM)应用于外墙隔热系统后,暖通空调(HVAC)的能耗可降低20%至35%。碳排放交易和绿色债券合格的监管政策日益明朗,持续吸引资金流入富含相变材料的建筑材料领域,巩固了欧洲在相变材料市场的主导地位。

亚太地区是成长最快的地区,预计到 2030 年将以每年 18.98% 的速度成长。中国积极部署热泵,透过节约用电高峰期的电力需求,与 PCM 储热技术相辅相成,并在「热泵的未来」蓝图的指导下,鼓励协同效应。

在北美,严格的能源监管更新和电动汽车行业的蓬勃发展,促使美国数据中心运营商试行基于 PCM 的热感缓衝器,以吸收伺服器中的热峰值并推迟冷却器启动,从而利用现场储能的税额扣抵抵免。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧洲和美国强制性的建筑节能标准将加速相变材料(PCM)的整合。

- 低温运输物流基础设施快速发展

- 车辆电气化需要采用盐水合物相变材料的先进热电池组。

- 政府对净零排放建筑的奖励措施,以鼓励采用生物基相变材料

- 全球日益增长的节能和永续发展趋势

- 市场限制

- 相变材料的危险性

- 高纯度水合盐供应链的变异性

- 认知和理解有限

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 原料分析

- 专利分析

第五章 市场规模与成长预测

- 依产品类型

- 有机的

- 无机物

- 生物基

- 按化学成分

- 石蜡

- 非烷烃

- 盐水合物

- 共晶体

- 透过封装技术

- 大分子胶囊化

- 微胶囊化

- 分子封装

- 按最终用户行业划分

- 建筑/施工

- 包裹

- 纺织品

- 电子学

- 运输

- 其他产业(医疗保健、国防)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、合资、联盟、资金筹措)

- 市占率(%)/排名分析

- 公司简介

- BASF

- Appvion, LLC.

- Climator

- Croda International Plc

- Cryopak

- DuPont

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Laird Technologies, Inc.

- Microtek

- National Gypsum Services Company

- Outlast Technologies GmbH

- Parker Hannifin Corp

- Phase Change Solutions

- Pluss Advanced Technologies

- PureTemp LLC

- Rubitherm Technologies GmbH

- Shenzhen Aochuan Technology Co.,Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Sonoco Products Company

第七章 市场机会与未来展望

The Phase Change Materials Market size is estimated at USD 0.92 billion in 2025, and is expected to reach USD 2.08 billion by 2030, at a CAGR of 17.69% during the forecast period (2025-2030).

Lengthening heat waves, net-zero construction goals, and rapid electrification in transport now place latent-heat storage at the center of commercial energy strategies. Mandatory building-energy codes in Europe and North America are accelerating integration, while cold-chain logistics and electric-vehicle battery packs expand the technology's reach into transportation, pharmaceuticals, and data-center cooling. Longly constrained by phase-separation and supercooling issues, salt hydrates are gaining traction after recent conductivity breakthroughs. At the same time, bio-based PCMs derived from agricultural residues have moved from laboratory curiosity to scalable commercial products, addressing fire safety and sustainability concerns without sacrificing thermal capacity. Regionally, Asia-Pacific is evolving into the fulcrum for capacity additions as manufacturers add local production lines to hedge supply-chain risk linked to high-purity salt hydrates.

Global Phase Change Materials Market Trends and Insights

Mandatory Building-Energy Codes Accelerating PCM Integration

Performance-based compliance criteria now allow architects to substitute rigid insulation with latent-heat storage layers, unlocking a 35-45% reduction in peak cooling loads within lightweight walls. Measured field results in Minnesota reported a 5.49 °C drop in peak indoor temperature plus a 77.8% load shift toward off-peak hours, providing regulators with real-world evidence of HVAC savings. Rising compliance thresholds for 2027 EU renovation targets are expected to place additional emphasis on PCM-infused gypsum boards and concrete blocks, thereby lifting procurement volumes across the Phase Change Material market.

Rapid Deployment of Cold-Chain Logistics Infrastructure

Vaccines, advanced biologics, and precision meats require temperature bands that often tolerate a +-0.5 °C deviation for less than three days. PCMs extend that holdover to 72 hours without external power, cutting diesel-generator reliance during airport or customs delays. Glycerol-water-NaCl blends slash carbon footprints 30-40% versus active cooling and lift pharmaceutical shelf life by 15-25%, feeding double-digit demand across the Phase Change Material market.

Hazardous Nature of Phase Change Materials

Paraffin waxes ignite at roughly 170 °C and require brominated flame retardants that add cost and can trigger health-labeling restrictions. Inorganic candidates such as LiNO3 present toxicity risks. Recent in-situ polymerized solid-solid PCMs eliminate leakage, passing UL94 V-0 flammability without halogens. Broader adoption hinges on scaling these encapsulation advances and harmonizing global chemical safety standards.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of Vehicles Necessitating Advanced Thermal Battery Packs

- Government Incentives for Net-Zero Buildings Propelling Bio-Based PCM Adoption

- Supply-Chain Volatility of High-Purity Salt Hydrates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Organic paraffin waxes remain the revenue anchor for the Phase Change Material market, accounting for 44.19% of global sales in 2024. Their dominance reflects mature supply chains, broad temperature coverage, and compatibility with macro-encapsulation slabs used in building panels. Yet the Phase Change Material market is witnessing a sharp pivot toward bio-derived oils, tallow, and fatty-acid blends as stakeholders chase lower life-cycle emissions. The emergent sub-segment is forecast to outpace all others at 19.21% CAGR to 2030, buoyed by LEED credits and municipal green-procurement mandates that explicitly endorse biogenic materials.

Paraffin-based formulations captured 41.49% of the Phase Change Material market revenue in 2024 due to their stable crystallization and ease of tailoring melting points across the 0-90 °C spectrum. Even so, salt hydrates are on course to disrupt that hierarchy, expanding at an 18.04% CAGR through 2030. High volumetric heat capacity (up to 350 kJ/L) and thermal conductivity improvements via carbon additives are allowing salt hydrates to shrink component size and weight. The resulting density advantage is especially attractive for electric-vehicle battery sleeves and compact data-center racks, where available footprint is constrained.

The Phase Change Material Market Report Segments the Industry by Product Type (Organic, Inorganic, and Bio-Based), Chemical Composition (Paraffin, Non-Paraffin Hydrocarbons, and More), Encapsulation Technology (Macro-Encapsulation, and More), End-User Industry (Building and Construction, Packaging, Textiles, Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Europe held 32.86% of global sales in 2024, underpinned by the EU's Energy Performance of Buildings Directive, which compels both new construction and deep-renovation projects to hit quasi-net-zero targets. Early adopters in Germany and the Nordics have shown 20-35% HVAC energy savings after embedding PCMs into external wall insulation systems. Regulatory clarity around carbon trading and green-bond eligibility continues to draw capital toward PCM-rich building materials, consolidating Europe's leadership position in the Phase Change Material market.

Asia-Pacific is the fastest-growing region, anticipated to expand 18.98% annually through 2030. China's aggressive heat-pump rollout complements PCM thermal storage by shaving peak electricity demand, a synergy encouraged under the "Future of Heat Pumps" roadmap.

North America combines stringent energy-code updates with an exploding electric-vehicle sector. Data-center operators in the United States, drawn by tax credits for on-site energy storage, pilot PCM-based thermal buffers to absorb server heat spikes and postpone chiller start-up.

- BASF

- Appvion, LLC.

- Climator

- Croda International Plc

- Cryopak

- DuPont

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Laird Technologies, Inc.

- Microtek

- National Gypsum Services Company

- Outlast Technologies GmbH

- Parker Hannifin Corp

- Phase Change Solutions

- Pluss Advanced Technologies

- PureTemp LLC

- Rubitherm Technologies GmbH

- Shenzhen Aochuan Technology Co.,Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Sonoco Products Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory Building-Energy Codes in Europe and North America Accelerating PCM Integration

- 4.2.2 Rapid Deployment of Cold-Chain Logistics Infrastructure

- 4.2.3 Electrification of Vehicles Necessitating Advanced Thermal Battery Packs Using Salt-Hydrate PCMs

- 4.2.4 Government Incentives for Net-Zero Buildings Propelling Bio-based PCM Adoption

- 4.2.5 Expanding Global Trend Towards Energy Conservation and Sustainable Development

- 4.3 Market Restraints

- 4.3.1 Hazardous Nature of Phase Change Materials

- 4.3.2 Supply-Chain Volatility of High-Purity Salt Hydrates

- 4.3.3 Limited Awareness and Understanding

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Raw-Material Analysis

- 4.7 Patent Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Organic

- 5.1.2 Inorganic

- 5.1.3 Bio-based

- 5.2 By Chemical Composition

- 5.2.1 Paraffin

- 5.2.2 Non-Paraffin Hydrocarbons

- 5.2.3 Salt Hydrates

- 5.2.4 Eutectics

- 5.3 By Encapsulation Technology

- 5.3.1 Macro-encapsulation

- 5.3.2 Micro-encapsulation

- 5.3.3 Molecular Encapsulation

- 5.4 By End-user Industry

- 5.4.1 Building and Construction

- 5.4.2 Packaging

- 5.4.3 Textiles

- 5.4.4 Electronics

- 5.4.5 Transportation

- 5.4.6 Other Industries (Healthcare, Defense)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquistions, JV, Collaboration, Funding)

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)}

- 6.4.1 BASF

- 6.4.2 Appvion, LLC.

- 6.4.3 Climator

- 6.4.4 Croda International Plc

- 6.4.5 Cryopak

- 6.4.6 DuPont

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Honeywell International Inc.

- 6.4.9 Laird Technologies, Inc.

- 6.4.10 Microtek

- 6.4.11 National Gypsum Services Company

- 6.4.12 Outlast Technologies GmbH

- 6.4.13 Parker Hannifin Corp

- 6.4.14 Phase Change Solutions

- 6.4.15 Pluss Advanced Technologies

- 6.4.16 PureTemp LLC

- 6.4.17 Rubitherm Technologies GmbH

- 6.4.18 Shenzhen Aochuan Technology Co.,Ltd.

- 6.4.19 Shin-Etsu Chemical Co., Ltd.

- 6.4.20 Sonoco Products Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Development of Phase Change Thermal Interface Material

生物基相变材料市场规模、份额和成长分析:按产品类型、应用、最终用户和地区划分-2026-2033年产业预测

生物基相变材料市场规模、份额和成长分析:按产品类型、应用、最终用户和地区划分-2026-2033年产业预测 2026年全球相变材料市场报告

2026年全球相变材料市场报告 相变材料市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年

相变材料市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年 家用电器相变材料市场(按产品类型、技术、电源、分销管道和最终用户划分)—2026-2032年全球预测相变润滑脂市场依产品类型、应用、终端用户产业及通路划分-2026年至2032年全球预测

家用电器相变材料市场(按产品类型、技术、电源、分销管道和最终用户划分)—2026-2032年全球预测相变润滑脂市场依产品类型、应用、终端用户产业及通路划分-2026年至2032年全球预测 相变材料(PCM)市场规模、份额和成长分析(按类型、应用、终端用户产业、类型和地区划分)-2026-2033年产业预测

相变材料(PCM)市场规模、份额和成长分析(按类型、应用、终端用户产业、类型和地区划分)-2026-2033年产业预测 相变材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

相变材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球相变材料市场按类型、应用和地区划分-预测至2030年

全球相变材料市场按类型、应用和地区划分-预测至2030年 相变材料市场:依产品类型、化学成分、封装技术、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测热管理领域相变材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

相变材料市场:依产品类型、化学成分、封装技术、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测热管理领域相变材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)