|

市场调查报告书

商品编码

1858804

政府及公共服务领域人工智慧市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)AI in Government and Public Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

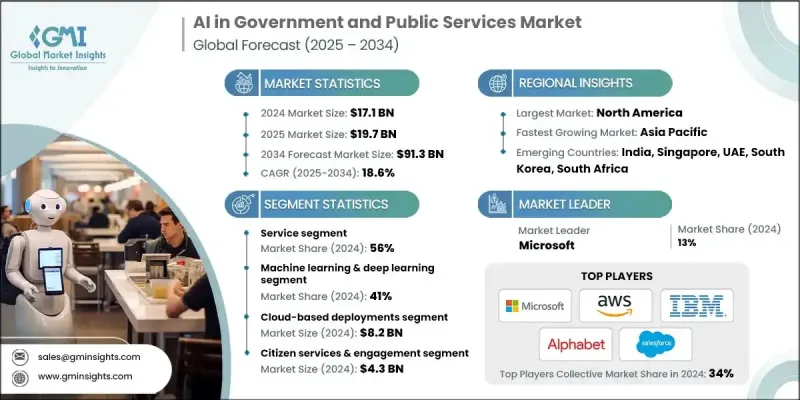

2024 年全球政府和公共服务领域人工智慧市场价值为 171 亿美元,预计到 2034 年将以 18.6% 的复合年增长率增长至 913 亿美元。

人工智慧的快速发展,以及数位化治理的日益普及,正在推动这一成长。世界各国政府都在利用人工智慧来提高营运效率、实现公共服务现代化,并更有效地与公民互动。人工智慧技术透过自动化资料输入、文件处理和公众咨询等重复性行政工作,正在改变传统的官僚体系。这使得政府机构能够加快工作流程、减少错误,并将人力资源重新分配到更具战略意义的任务上。利用人工智慧来增强即时决策、预测分析和服务自动化,正成为数位转型议程的核心要素。此外,对更敏捷、反应迅速和数据驱动的治理模式的重视,也促使公共部门机构加快采用人工智慧的步伐。各国政府意识到人工智慧在提高透明度、优化资源配置以及为公民提供更个人化服务方面的益处,同时还能在公共管理中维护严格的隐私和道德标准。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 171亿美元 |

| 预测值 | 913亿美元 |

| 复合年增长率 | 18.6% |

2024年,服务板块占据56%的市场份额,预计2025年至2034年将以16%的复合年增长率成长。该板块涵盖系统整合、实施咨询、员工培训和技术支持,每一项都在政府生态系统中顺利部署人工智慧解决方案方面发挥着至关重要的作用。公共部门机构通常依赖专家咨询来确定可行的人工智慧应用案例、设计可扩展的实施计划并确保符合监管要求。由于前期投资需求高,且传统系统整合面临许多挑战,对专业服务的需求持续成长,凸显了其在人工智慧长期成功中的关键作用。

机器学习和深度学习领域在2024年占据了41%的市场份额,预计到2034年将以17%的复合年增长率成长。这些核心人工智慧技术透过实现模式识别、预测分析和智慧自动化,为政府的众多应用提供了支撑。政府机构正在部署机器学习模型,以支援诈欺侦测、绩效分析、风险评估和资源规划。这些工具能够处理大量结构化和非结构化资料,使其成为现代公共部门运作的关键。

2024年,亚太地区政府和公共服务领域的人工智慧市场占有率达到24%,预计2025年至2034年间将以21%的复合年增长率成长。该地区以人口众多、都市化快速进程的国家为主导,正大力投资人工智慧以满足现代治理的需求。在亚太地区最具发展潜力的市场中,有一个国家因其大规模人工智慧计画而脱颖而出,这些计画旨在实现智慧城市管理、以公民为中心的服务和数位化行政。强而有力的政府支持和战略规划正在推动人工智慧在政府各个职能部门的广泛应用。

推动政府和公共服务市场人工智慧创新和部署的关键企业包括Alphabet、IBM、Salesforce、NVIDIA、微软、亚马逊网路服务(AWS)、Oracle、Cognizant、OpenAI和埃森哲。为了巩固自身地位,这些主要企业正致力于与政府机构进行策略合作,共同开发满足公共服务需求的AI驱动平台。各公司正大力投资研发,以创造符合政府合规标准的、可扩展、安全且符合伦理规范的AI解决方案。许多公司正在加强其专业服务部门,以支援系统整合、监管咨询和AI培训。与地方政府的合作使得企业能够根据区域需求进行客製化,同时,基于云端的AI产品也在不断扩展,以支援远端和可扩展的部署。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 云端服务供应商

- 人工智慧平台提供商

- 系统整合商

- 硬体和基础设施供应商

- 安全与治理解决方案提供商

- 成本结构

- 利润率

- 每个阶段的价值增加

- 影响供应链的因素

- 颠覆者

- 供应商格局

- 对力的影响

- 成长驱动因素

- 对营运效率和成本降低的需求

- 公民对数位服务的期望日益提高

- 需要数据驱动的政策和决策

- 加强公共安全保障

- 产业陷阱与挑战

- 资料隐私、安全和伦理问题

- 高额初始投资和遗留系统集成

- 市场机会

- 主动和预测性的公共服务

- 改善城市规划和智慧城市发展

- 成长驱动因素

- 技术趋势与创新生态系统

- 目前技术

- 大型语言模型演化

- 多模态人工智慧集成

- 强化学习进展

- 神经架构搜寻

- 新兴技术

- 面向智能体的联邦学习

- 边缘人工智慧与分散式运算

- 量子计算集成

- 脑机介面开发

- 目前技术

- 成长潜力分析

- 监管环境

- 监理合规与治理框架

- 联邦人工智慧行政命令实施

- OMB人工智慧治理准则合规性

- NIST人工智慧风险管理框架的采用

- 国际人工智慧治理标准一致性

- 安全与隐私管理

- FedRAMP授权要求

- 网路安全框架集成

- 资料隐私和保护协议

- 跨境资料传输合规性

- 监理合规与治理框架

- 波特的分析

- PESTEL 分析

- 专利分析

- 成本細項分析

- 价格趋势

- 按地区

- 副产品

- 永续性和环境方面

- 环境影响评估与生命週期分析

- 社会影响力与社区关係

- 公司治理与企业责任

- 永续技术发展

- 用例

- 遗留系统整合与现代化

- 传统基础设施相容性挑战

- 系统整合架构策略

- 资料迁移和互通性解决方案

- 分阶段现代化方法

- 劳动力转型与技能发展

- 人工智慧技能差距评估和培训需求

- 变革管理与使用者采纳策略

- 公共部门人才招募挑战

- 跨机构知识共享计划

- 采购与供应商选择框架

- 政府采购流程的复杂性

- 供应商资格和安全许可要求

- 合约管理及绩效指标

- 多供应商整合策略

- 伦理人工智慧与偏见缓解

- 演算法公平性和透明度要求

- 偏见检测与缓解框架

- 可解释人工智慧实施标准

- 公共问责与审计机制

- 互通性和标准化

- 跨机构资料共享协议

- API标准化与集成

- 通用平台开发计划

- 联邦企业架构调整

- 预算优化和投资报酬率演示

- 政府预算策略

- 成本效益分析框架

- 绩效衡量与关键绩效指标制定

- 价值实现与影响评估

- 公众信任与透明度

- 公民参与和沟通策略

- 透明度和可解释性要求

- 公众回馈与问责机制

- 媒体与利害关係人关係管理

- 跨机构协作与协调

- 机构间伙伴关係模式

- 共享服务和平台策略

- 联邦-州-地方协调框架

- 公私合作发展

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依产品类型划分,2021-2034年

- 主要趋势

- 解决方案/软体

- 服务

- 咨询顾问

- 系统整合与部署

- 培训与教育

- 支援与维护

第六章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 机器学习与深度学习

- 自然语言处理(NLP)

- 图片和影片

- 机器人流程自动化 (RPA)

- 其他的

第七章:市场估算与预测:依部署模式划分,2021-2034年

- 主要趋势

- 本地部署

- 基于云端的

- 杂交种

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 公民服务与参与

- 用于公共查询的数位助理和聊天机器人

- 公共传播多语种翻译

- 个人化政府入口网站

- 公共安全与保全

- 监视与监控

- 犯罪预测与分析

- 紧急应变系统

- 医疗保健和社会服务

- 疾病预测与疫情控制

- 智慧资源分配

- 福利和救济金分配监督

- 国防与国家安全

- 威胁侦测与分析

- 人工智慧驱动的网路安全系统

- 军事决策支援系统

- 行政效率

- 智慧城市与城市管理

- 其他的

第九章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 联邦/国家政府

- 州/省政府

- 地方/市政府

- 其他的

第十章:市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- 全球参与者

- Accenture

- Alphabet

- Amazon Web Services

- Cognizant

- IBM

- Microsoft

- NVIDIA

- Open AI

- Oracle

- Salesforce

- SAP

- 区域玩家

- Booz Allen Hamilton

- CACI International

- General Dynamics Information Technology

- Leidos

- Lockheed Martin

- Palantir Technologies

- Raytheon Technologies

- SAIC (Science Applications International)

- 新兴玩家

- Appian

- Automation Anywhere

- Blue Prism

- C3.ai

- DataRobot

- H2 O.ai

- UiPath

- Verint Systems

The Global AI in Government and Public Services Market was valued at USD 17.1 billion in 2024 and is estimated to grow at a CAGR of 18.6% to reach USD 91.3 billion by 2034.

Rapid advancements in artificial intelligence, combined with the increasing shift toward digital governance, are fueling this growth. Governments worldwide are leveraging AI to enhance operational efficiency, modernize public services, and engage citizens more effectively. AI technologies are transforming traditional bureaucratic systems by automating repetitive administrative duties such as data entry, document processing, and public inquiries. This allows government agencies to accelerate workflows, reduce errors, and redirect human resources to more strategic tasks. The use of AI to enhance real-time decision-making, predictive analytics, and service automation is becoming a core element of digital transformation agendas. Additionally, the focus on more agile, responsive, and data-driven governance models has pushed public sector organizations to adopt AI at a faster pace. Governments are recognizing the benefits of AI in enhancing transparency, optimizing resource allocation, and providing more personalized services to citizens, all while maintaining strong privacy and ethical standards in public administration.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.1 Billion |

| Forecast Value | $91.3 Billion |

| CAGR | 18.6% |

In 2024, the services segment held a 56% share and is anticipated to grow at a CAGR of 16% from 2025 to 2034. This segment includes system integration, implementation consulting, staff training, and technical support, each playing a vital role in enabling the smooth deployment of AI solutions within government ecosystems. Public sector organizations often rely on expert consulting to identify viable AI use cases, design scalable implementation plans, and ensure regulatory compliance. With high upfront investment needs and challenges around legacy system integration, the demand for specialized services continues to increase, underscoring their critical role in long-term AI success.

The machine learning and deep learning segment held a 41% share in 2024 and is projected to grow at a CAGR of 17% through 2034. These core AI technologies underpin a wide range of government applications by enabling pattern recognition, predictive analytics, and intelligent automation. Government bodies are deploying machine learning models to support fraud detection, performance analysis, risk evaluation, and resource planning. The ability of these tools to process large volumes of structured and unstructured data makes them essential for modern public sector operations.

Asia-Pacific AI in Government and Public Services Market held 24% share in 2024 and will grow at a CAGR of 21% during 2025-2034. The region, led by countries with large populations and rapid urbanization, is investing heavily in AI to meet the demands of modern governance. Among the most promising markets in the region, one country stands out due to its large-scale AI initiatives targeting smart city management, citizen-centric services, and digital administration. Strong governmental support and strategic planning are enabling widespread AI adoption across various government functions.

Key companies driving innovation and deployment of AI in the Government and Public Services Market include Alphabet, IBM, Salesforce, NVIDIA, Microsoft, Amazon Web Services, Oracle, Cognizant, OpenAI, and Accenture. To strengthen their presence, key players are focusing on strategic collaborations with government agencies to co-develop AI-driven platforms tailored for public service needs. Companies are investing heavily in R&D to create scalable, secure, and ethical AI solutions aligned with government compliance standards. Many firms are enhancing their professional services divisions to support system integration, regulatory consulting, and AI training. Partnerships with local governments are enabling customization for regional needs, while cloud-based AI offerings are being expanded to support remote and scalable deployments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast

- 1.4 Primary research and validation

- 1.5 Some of the primary sources

- 1.6 Data mining sources

- 1.6.1 Secondary

- 1.6.1.1 Paid Sources

- 1.6.1.2 Public Sources

- 1.6.1.3 Sources, by region

- 1.6.1 Secondary

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Technology

- 2.2.4 Deployment mode

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Cloud service providers

- 3.1.1.2 AI platform providers

- 3.1.1.3 System integrators

- 3.1.1.4 Hardware & infrastructure providers

- 3.1.1.5 Security & governance solution providers

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Demand for operational efficiency & cost reduction

- 3.2.1.2 Rising citizen expectations for digital services

- 3.2.1.3 Need for data-driven policy and decision-making

- 3.2.1.4 Enhanced public safety and security

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Data privacy, security, and ethical concerns

- 3.2.2.2 High initial investment and legacy system integration

- 3.2.3 Market opportunities

- 3.2.3.1 Proactive and predictive public services

- 3.2.3.2 Improved urban planning and smart city development

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Large language model evolution

- 3.3.1.2 Multi-modal AI integration

- 3.3.1.3 Reinforcement learning advances

- 3.3.1.4 Neural architecture search

- 3.3.2 Emerging technologies

- 3.3.2.1 Federated learning for agents

- 3.3.2.2 Edge AI & distributed computing

- 3.3.2.3 Quantum computing integration

- 3.3.2.4 Brain-computer interface development

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 Regulatory compliance & governance framework

- 3.5.1.1 Federal AI executive order implementation

- 3.5.1.2 OMB AI governance guidelines compliance

- 3.5.1.3 NIST AI risk management framework adoption

- 3.5.1.4 International AI governance standards alignment

- 3.5.2 Security & privacy management

- 3.5.2.1 FedRAMP authorization requirements

- 3.5.2.2 Cybersecurity framework integration

- 3.5.2.3 Data privacy & protection protocols

- 3.5.2.4 Cross-border data transfer compliance

- 3.5.1 Regulatory compliance & governance framework

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Sustainability and environmental aspects

- 3.11.1 Environmental impact assessment & lifecycle analysis

- 3.11.2 Social impact & community relations

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable technological development

- 3.12 Use cases

- 3.13 Legacy system integration & modernization

- 3.13.1 Legacy infrastructure compatibility challenges

- 3.13.2 System integration architecture strategies

- 3.13.3 Data migration & interoperability solutions

- 3.13.4 Phased modernization approaches

- 3.14 Workforce transformation & skills development

- 3.14.1 AI skills gap assessment & training needs

- 3.14.2 Change management & user adoption strategies

- 3.14.3 Public sector talent acquisition challenges

- 3.14.4 Cross-agency knowledge sharing programs

- 3.15 Procurement & vendor selection framework

- 3.15.1 Government procurement process complexity

- 3.15.2 Vendor qualification & security clearance requirements

- 3.15.3 Contract management & performance metrics

- 3.15.4 Multi-vendor integration strategies

- 3.16 Ethical AI & bias mitigation

- 3.16.1 Algorithmic fairness & transparency requirements

- 3.16.2 Bias detection & mitigation frameworks

- 3.16.3 Explainable AI implementation standards

- 3.16.4 Public accountability & audit mechanisms

- 3.17 Interoperability & standardization

- 3.17.1 Cross-agency data sharing protocols

- 3.17.2 API standardization & integration

- 3.17.3 Common platform development initiatives

- 3.17.4 Federal enterprise architecture alignment

- 3.18 Budget optimization & ROI demonstration

- 3.18.1 Government budget allocation strategies

- 3.18.2 Cost-benefit analysis frameworks

- 3.18.3 Performance measurement & KPI development

- 3.18.4 Value realization & impact assessment

- 3.19 Public trust & transparency

- 3.19.1 Citizen engagement & communication strategies

- 3.19.2 Transparency & explainability requirements

- 3.19.3 Public feedback & accountability mechanisms

- 3.19.4 Media & stakeholder relations management

- 3.20 Cross-agency collaboration & coordination

- 3.20.1 Inter-agency partnership models

- 3.20.2 Shared services & platform strategies

- 3.20.3 Federal-state-local coordination frameworks

- 3.20.4 Public-private partnership development

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solutions/software

- 5.3 Services

- 5.3.1 Consulting & advisory

- 5.3.2 System integration & deployment

- 5.3.3 Training & education

- 5.3.4 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Machine learning & deep learning

- 6.3 Natural Language Processing (NLP)

- 6.4 Image & video

- 6.5 Robotic Process Automation (RPA)

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Deployment mode, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 On-Premises

- 7.3 Cloud-Based

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Citizen services & engagement

- 8.2.1 Digital assistants & chatbots for public queries

- 8.2.2 Multilingual Translation for Public Communication

- 8.2.3 Personalized government portals

- 8.3 Public safety & security

- 8.3.1 Surveillance & monitoring

- 8.3.2 Crime prediction & analysis

- 8.3.3 Emergency response systems

- 8.4 Healthcare & social services

- 8.4.1 Disease prediction & outbreak control

- 8.4.2 Smart resource allocation

- 8.4.3 Benefits & welfare distribution monitoring

- 8.5 Defense & national security

- 8.5.1 Threat detection & analysis

- 8.5.2 AI-driven cybersecurity systems

- 8.5.3 Military decision support systems

- 8.6 Administrative efficiency

- 8.7 Smart cities & urban management

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Federal/National government

- 9.3 State/Provincial government

- 9.4 Local/Municipal government

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Accenture

- 11.1.2 Alphabet

- 11.1.3 Amazon Web Services

- 11.1.4 Cognizant

- 11.1.5 IBM

- 11.1.6 Microsoft

- 11.1.7 NVIDIA

- 11.1.8 Open AI

- 11.1.9 Oracle

- 11.1.10 Salesforce

- 11.1.11 SAP

- 11.2 Regional players

- 11.2.1 Booz Allen Hamilton

- 11.2.2 CACI International

- 11.2.3 General Dynamics Information Technology

- 11.2.4 Leidos

- 11.2.5 Lockheed Martin

- 11.2.6 Palantir Technologies

- 11.2.7 Raytheon Technologies

- 11.2.8 SAIC (Science Applications International)

- 11.3 Emerging players

- 11.3.1 Appian

- 11.3.2 Automation Anywhere

- 11.3.3 Blue Prism

- 11.3.4 C3.ai

- 11.3.5 DataRobot

- 11.3.6. H2 O.ai

- 11.3.7 UiPath

- 11.3.8 Verint Systems

2026年全球公民服务人工智慧市场报告

2026年全球公民服务人工智慧市场报告 政府和公共部门网路安全:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

政府和公共部门网路安全:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年) 公民服务人工智慧市场(按组件、部署类型、组织规模和最终用户划分)—2025-2032 年全球预测

公民服务人工智慧市场(按组件、部署类型、组织规模和最终用户划分)—2025-2032 年全球预测 2025-2029年全球公民服务人工智慧市场

2025-2029年全球公民服务人工智慧市场 公民服务人工智慧市场-全球产业规模、份额、趋势、机会和预测(按技术、垂直产业、地区和竞争细分,2020-2030 年)

公民服务人工智慧市场-全球产业规模、份额、趋势、机会和预测(按技术、垂直产业、地区和竞争细分,2020-2030 年) 公民服务 AI 市场:全球产业分析、市场规模、占有率、成长、趋势和未来预测(2025-2032年)

公民服务 AI 市场:全球产业分析、市场规模、占有率、成长、趋势和未来预测(2025-2032年) 市民服务AI的全球市场 - 全球产业分析,规模,占有率,成长,趋势,预测(2031年)

市民服务AI的全球市场 - 全球产业分析,规模,占有率,成长,趋势,预测(2031年) 公民服务人工智慧市场规模、份额、趋势分析报告:2024-2030 年按组件、技术、部署、应用、地区和细分市场进行的预测

公民服务人工智慧市场规模、份额、趋势分析报告:2024-2030 年按组件、技术、部署、应用、地区和细分市场进行的预测 全球公民服务人工智慧市场 2024-2031

全球公民服务人工智慧市场 2024-2031