|

市场调查报告书

商品编码

1858885

风力涡轮机运转及维护市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Wind Turbine Operation and Maintenance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

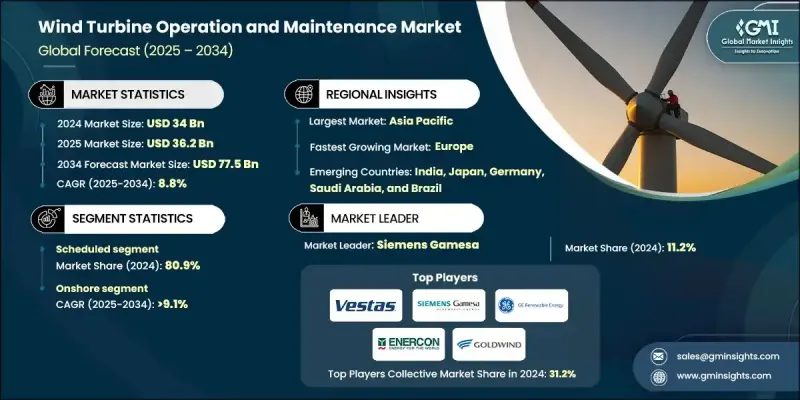

2024 年全球风力涡轮机运转和维护市场价值为 340 亿美元,预计到 2034 年将以 8.8% 的复合年增长率增长至 775 亿美元。

全球风能基础设施的日益成熟持续推动着可扩展且经济高效的运维服务的需求。随着风电在全球能源结构中占据越来越大的份额,高效能、技术整合的维护变得愈发重要。自动化诊断、机器学习和数据驱动系统的创新正在显着提高风扇效率并减少运行停机时间。这些智慧工具透过提供预测性洞察和即时监控,正在重塑运维格局。此外,随着能源生产商转向永续性和全生命週期效率,主动维护策略的角色正在迅速增长。预测分析和远端存取工具正在取代传统的维护模式,以确保最大限度地减少中断并优化资产效能。无人机技术和机器人自动化正在进一步改变风扇的维护方式,尤其是在难以到达的地区。这些进步正在促进一个更精简和永续的维运生态系统的发展,巩固了陆上和海上资产市场的稳定扩张。数位化以及对清洁能源的政策支持,将持续加速全球风力发电机组维护服务的演进。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 340亿美元 |

| 预测值 | 775亿美元 |

| 复合年增长率 | 8.8% |

2024年,计画性维护服务市占率达到80.9%,预计到2034年将以9.3%的复合年增长率成长。这一主导地位反映了由数位化平台支援的主动式服务模式的广泛应用。营运商越来越多地利用先进的诊断技术和性能资料来优化风扇的生命週期,避免代价高昂的故障。随着风能资产老化以及偏远或海上地区新装置的出现,对智慧调度、资产追踪和预测性洞察的需求不断增长,以支援复杂的维护营运。

2024年,陆域风电市占率达到88.5%,预计2025年至2034年将以9.1%的复合年增长率成长。陆域风电场正致力于数位转型,以降低维护成本并提高可靠性。由于老旧风电场需要更专业的维护,营运商正在部署人工智慧驱动的分析、物联网感测器和先进的监控工具,以预测零件故障并延长风扇寿命。这种向互联、主动维护解决方案的转变,使营运商能够简化工作流程、提高正常运作时间,并从其资产中获得长期价值。

2034年,欧洲风力涡轮机运维市场规模将达190亿美元。这一增长主要得益于离岸风电项目投资的增加以及人工智慧诊断、机器人技术和远端控制系统等智慧技术的日益普及。该地区许多陆上风电场正在进行改造升级,从而催生了对客製化运维服务的新需求。政府政策、环境目标以及对低排放能源的监管支持,都鼓励营运商投资于智慧且永续的维护解决方案,进而推动了整体市场成长。

全球风力涡轮机运作和维护市场的主要参与者包括维斯塔斯风力系统公司 (Vestas Wind Systems A/S)、Enercon GmbH、苏司兰能源有限公司 (Suzlon Energy Ltd)、弗雷德·奥尔森风力运输公司 (Fred. Olsen Windcarrier)、RTS Wind AG、B9 Energy Group、Moventas Windtechnik)、ABB有限公司、比尔芬格公司 (Bilfinger Inc.)、Dana SAC UK Ltd、Global Wind Service company、采埃孚股份公司 (ZF Friedrichshafen AG)、Mistras Group、Mitarsh Energy、NORDEX SE、REETEC、西门子歌美飒 (Siemens Gamesa) 和蓝水航运航运。为了巩固其在全球风力涡轮机运行和维护市场的地位,主要参与者正在积极推动数位转型并投资先进技术。各公司越来越多地采用预测性维护平台,利用人工智慧、巨量资料和基于感测器的诊断技术来即时监测涡轮机的健康状况。与软体供应商和技术创新者的策略合作有助于将自动化、无人机和机器人技术整合到其服务产品中,从而降低成本并提高工人安全。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系统

- 监管环境

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 成长潜力分析

- 价格趋势分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 战略仪錶板

- 策略倡议

- 公司标竿分析

- 创新与技术格局

第五章:市场规模及预测:依类型划分,2021-2034年

- 主要趋势

- 已安排

- 非计划性

第六章:市场规模及预测:依地区划分,2021-2034年

- 主要趋势

- 陆上

- 离岸

第七章:市场规模及预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 瑞典

- 英国

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 中东和非洲

- 埃及

- 南非

- 摩洛哥

- 沙乌地阿拉伯

- 拉丁美洲

- 巴西

- 墨西哥

- 智利

第八章:公司简介

- ABB

- B9 Energy Group

- Bilfinger Inc.

- Dana SAC UK Ltd

- Deutsche Windtechnik

- Enercon GmbH

- Fred. Olsen Windcarrier

- Global Wind Service company

- GoldWind

- Mistras Group,

- Mitarsh Energy

- Moventas Gears Oy

- NORDEX SE

- REETEC

- RTS Wind AG

- Siemens Gamesa

- Suzlon Energy Limited

- Suzlon Energy Ltd

- Vestas Wind Systems A/S

- ZF Friedrichshafen AG

The Global Wind Turbine Operation and Maintenance Market was valued at USD 34 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 77.5 billion by 2034.

The increasing maturity of global wind energy infrastructure continues to drive demand for scalable and cost-effective O&M services. As wind power claims a larger share of the global energy portfolio, the need for efficient, technology-integrated maintenance becomes more critical. Innovations in automated diagnostics, machine learning, and data-driven systems are significantly enhancing turbine efficiency and reducing operational downtime. These smart tools are reshaping the O&M landscape by offering predictive insights and real-time monitoring. Additionally, with energy producers shifting toward sustainability and lifecycle efficiency, the role of proactive maintenance strategies is growing rapidly. Predictive analytics and remote access tools are replacing traditional maintenance models to ensure minimal disruptions and optimized asset performance. Drone technology and robotic automation are further transforming the way turbines are serviced, especially in hard-to-reach locations. These advancements are fostering a more streamlined and sustainable O&M ecosystem, reinforcing the market's steady expansion across both onshore and offshore assets. Digitalization, combined with policy support for clean energy, continues to accelerate the evolution of wind turbine servicing across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34 Billion |

| Forecast Value | $77.5 Billion |

| CAGR | 8.8% |

In 2024, the scheduled maintenance services segment held an 80.9% share and is forecasted to grow at a CAGR of 9.3% through 2034. This dominance reflects the widespread adoption of proactive service models supported by digital platforms. Operators are increasingly using advanced diagnostics and performance data to optimize turbine life cycles and avoid costly breakdowns. As wind energy assets age and new installations emerge in remote or offshore areas, demand is rising for smart scheduling, asset tracking, and predictive insights to support complex maintenance operations.

The onshore segment held an 88.5% share in 2024 and is expected to grow at a CAGR of 9.1% from 2025 to 2034. Onshore wind farms are focusing on digital transformation to reduce maintenance costs and improve reliability. With older wind farms requiring more specialized care, operators are deploying AI-driven analytics, IoT-enabled sensors, and advanced monitoring tools to anticipate component failures and extend turbine life. This shift toward connected, proactive maintenance solutions allows operators to streamline workflows, improve uptime, and drive long-term value from their assets.

Europe Wind Turbine Operation and Maintenance Market will reach USD 19 billion by 2034. This growth is propelled by rising investments in offshore wind projects and increasing integration of intelligent technologies like AI-based diagnostics, robotics, and remote control systems. Many onshore fleets across the region are undergoing repowering, which is creating fresh demand for tailored O&M services. Government policy, environmental targets, and regulatory backing for low-emission energy sources are encouraging operators to invest in smart and sustainable maintenance solutions, which in turn boosts overall market growth.

Leading companies active in the Global Wind Turbine Operation and Maintenance Market include Vestas Wind Systems A/S, Enercon GmbH, Suzlon Energy Ltd, Fred. Olsen Windcarrier, RTS Wind AG, B9 Energy Group, Moventas Gears Oy, GoldWind, Deutsche Windtechnik, ABB Ltd., Bilfinger Inc., Dana SAC UK Ltd, Global Wind Service company, ZF Friedrichshafen AG, Mistras Group, Mitarsh Energy, NORDEX SE, REETEC, Siemens Gamesa, and Blue Water Shipping. To strengthen their foothold in the Global Wind Turbine Operation and Maintenance Market, major players are embracing digital transformation and investing in advanced technologies. Companies are increasingly adopting predictive maintenance platforms that utilize AI, big data, and sensor-based diagnostics to monitor turbine health in real time. Strategic collaborations with software providers and tech innovators help integrate automation, drones, and robotics into their service offerings, reducing costs and improving worker safety.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research & validation

- 1.3.1 Primary sources

- 1.4 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Type trends

- 2.4 Location trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Price trend analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Scheduled

- 5.3 Unscheduled

Chapter 6 Market Size and Forecast, By Location, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Onshore

- 6.3 Offshore

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Sweden

- 7.3.4 UK

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Egypt

- 7.5.2 South Africa

- 7.5.3 Morocco

- 7.5.4 Saudi Arabia

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 B9 Energy Group

- 8.3 Bilfinger Inc.

- 8.4 Dana SAC UK Ltd

- 8.5 Deutsche Windtechnik

- 8.6 Enercon GmbH

- 8.7 Fred. Olsen Windcarrier

- 8.8 Global Wind Service company

- 8.9 GoldWind

- 8.10 Mistras Group,

- 8.11 Mitarsh Energy

- 8.12 Moventas Gears Oy

- 8.13 NORDEX SE

- 8.14 REETEC

- 8.15 RTS Wind AG

- 8.16 Siemens Gamesa

- 8.17 Suzlon Energy Limited

- 8.18 Suzlon Energy Ltd

- 8.19 Vestas Wind Systems A/S

- 8.20 ZF Friedrichshafen AG

全球风力发电机运转和维护市场规模、份额、趋势和成长分析报告(2026-2034年)

全球风力发电机运转和维护市场规模、份额、趋势和成长分析报告(2026-2034年) 风力发电机维护服务市场按服务类型、合约类型、零件类型、供应商类型和涡轮机尺寸划分 - 全球预测 2026-2032 年

风力发电机维护服务市场按服务类型、合约类型、零件类型、供应商类型和涡轮机尺寸划分 - 全球预测 2026-2032 年 风力发电机运转和维护市场规模、份额和成长分析(按类型、地点、组件和地区划分)-2026-2033年产业预测风力发电机运转和维护市场按合约类型、涡轮机类型、所有权模式、维护模式、服务供应商类型、服务类型、零件类型和检验方法划分-全球预测,2025-2032年

风力发电机运转和维护市场规模、份额和成长分析(按类型、地点、组件和地区划分)-2026-2033年产业预测风力发电机运转和维护市场按合约类型、涡轮机类型、所有权模式、维护模式、服务供应商类型、服务类型、零件类型和检验方法划分-全球预测,2025-2032年 全球风力发电机营运和维护市场:预测至 2032 年 - 按服务类型、组件、部署、维护类型、服务供应商、应用程式和地区进行分析

全球风力发电机营运和维护市场:预测至 2032 年 - 按服务类型、组件、部署、维护类型、服务供应商、应用程式和地区进行分析 全球风力发电机营运与维护市场(按位置、类型、涡轮机拓扑结构和地区划分)- 预测至 2030 年

全球风力发电机营运与维护市场(按位置、类型、涡轮机拓扑结构和地区划分)- 预测至 2030 年 风力发电机维护、维修和大修 (MRO) 市场 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

风力发电机维护、维修和大修 (MRO) 市场 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 风力发电机运作和维护市场(按应用、服务类型和地区)

风力发电机运作和维护市场(按应用、服务类型和地区) 风力发电机营运与维护 (O&M) 市场 - 成长、未来展望、竞争分析,2025-2033 年全球风力涡轮机营运市场规模(按服务类型、涡轮机容量、组件类型、地区、范围和预测)

风力发电机营运与维护 (O&M) 市场 - 成长、未来展望、竞争分析,2025-2033 年全球风力涡轮机营运市场规模(按服务类型、涡轮机容量、组件类型、地区、范围和预测)