|

市场调查报告书

商品编码

1683100

风力发电机维护、维修和大修 (MRO) 市场 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Wind Turbine Maintenance, Repair and Overhaul (MRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

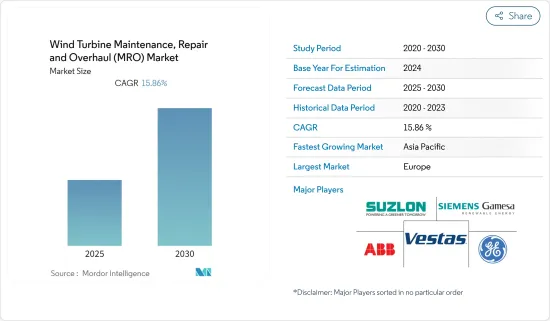

风力发电机维护、维修和大修 (MRO) 市场预计在预测期内的复合年增长率为 15.86%

关键亮点

- 离岸风力发电机的不断增加将推动全球风力发电机维护、维修和大修(MRO)市场的发展,这很可能成为预测期内成长最快的领域。

- 此外,利用风力发电的现像也显着增加。随着各国对风电市场的投资,维护需求可能增加。中东和非洲的风力发电厂正在显着成长,预计将为全球风力发电机维护、维修和大修(MRO)市场的成长提供机会。

- 预计2020年亚太地区将成为全球风电装置规模最大、成长最快的地区。

风力发电机MRO 市场趋势

离岸风力发电设备可望大幅成长

- 随着能源需求的增加,各大国家和企业纷纷转向引进可以提供清洁能源的可再生能源。利用先进技术的离岸风力发电的引入,正吸引各国和企业的大量投资。

- 根据安装位置,由于成本下降和技术进步,预计预测期内海上产业将继续推动全球风力发电机产业的投资。

- 2020年全球海上市场维持稳定,新增装置容量达606千万瓦,与2019年大致持平。海上累积设置容量达3,530万千瓦,与前一年同期比较成长21.7%。

- 2020年,离岸风电产业迎来大规模装机,如中国一年内新增离岸风电3GW,其次是荷兰(150万千瓦)、比利时(706千万瓦)、英国(483万千瓦)、德国(237千万瓦)。然而,英国新安装速度的放缓主要是由于付款合约 (CfD) 第 1 轮和 CfD2 轮之间的计划交付滞后。此外,在德国,新装置容量放缓主要是由于不利条件和近期离岸风力发电计划储备水准较低。

- 预计风力发电机将越来越多地部署在更复杂、更具攻击性的环境中,例如更远的海上,再加上风力发电机容量的增加,这将对风力发电机的运行组件带来额外的压力。这可能会导致变速箱等零件过早失效,从而造成风电场的发电量大幅下降。此外,提供 MRO 服务的成本比在陆上站点提供 MRO 服务的成本高得多。与陆上设施相比,材料和服务增加以及地形不易到达等因素限制了成长。

- 因此,鑑于上述情况,预计在预测期内,离岸风力发电的采用将在风力发电机维护、维修和大修市场中呈现显着成长。

亚太地区可望成为成长最快的市场

- 亚太地区是全球成长最快的风力发电市场,这主要得益于中国的贡献。该地区累积设备容量346.70GW,其中陆上风电装置容量336.29GW,离岸风力发电装置容量10.41GW。

- 截至2020年,中国是亚太地区风电装置容量最大的国家,约278.32吉瓦。它也是全球陆上风电市场的领导者。 2020年,全国新增风电装置5893万千瓦,其中,陆域风电4894万千瓦,离岸风电999万千瓦。这显示中国有望成为亚太地区最大的维护、修理和大修(MRO)服务市场。

- 同时,亚太地区风电装置容量第二大的印度,截至2020年也仅3,862.5万千瓦。然而,在印度这个拥有13.5亿人口的国家,未来10年的电力需求预计将会翻倍。印度政府因此设定了目标,到2022年将可再生能源发电至175GW,其中风电为60GW;到2030年将提升至450GW,其中风电为140GW。韩国拥有庞大的技术潜力,轮毂高度为120米,发电容量可达695GW。

- 韩国也计画在2030年实现可再生能源装置容量达到6,380万千瓦,其中约1,800万千瓦来自风能。 Orsted 等跨国公司表示,韩国有潜力在风力发电领域取得成功,尤其是考虑到其地理位置,在离岸风力发电领域。

- 预计这表明,在预测期内,亚太地区将成为全球风力发电机维护、维修和大修业务参与企业的主要业务目的地。

风力发电机MRO 产业概况

全球风力发电机维护、维修和大修(MRO)市场适度细分。该市场的主要企业包括西门子歌美飒可再生能源公司、通用电气公司、苏司兰能源有限公司、ABB 有限公司和维斯塔斯风力系统公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概况

- 介绍

- 全球可再生能源结构(2020 年)

- 风电装置容量(GW)及 2027 年预测

- 市场规模与需求预测(2027 年,单位:十亿美元)

- 2018-2027 年全球平均风力发电机尺寸(MW)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 限制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场区隔

- 部署位置

- 陆上

- 海上

- 服务类型

- 维护

- 维修

- 大修

- 成分

- 变速箱

- 发电机

- 叶轮

- 其他的

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 南美洲

- 中东和非洲

第六章 竞争格局

- 併购、合资、合作、协议

- 主要企业策略

- 公司简介

- Siemens Gamesa Renewable Energy SA

- General Electric Company

- Stork(a Fluor Company)

- Moventas Gears Oy

- ZF Friedrichshafen AG

- Vestas Wind Systems A/S

- Suzlon Energy Ltd

- ABB Ltd

- Dana SAC UK Ltd

- Nordex SE

- Mistras Group

- Integrated Power Services LLC

第七章 市场机会与未来趋势

简介目录

Product Code: 48701

The Wind Turbine Maintenance, Repair and Overhaul Market is expected to register a CAGR of 15.86% during the forecast period.

Key Highlights

- Increasing, offshore deployment of wind turbine is likely to drive the global wind turbine maintenance, repair, and overhaul (MRO) market, thus making it fastest growing segment during the forecast period.

- Moreover, the adoption of wind power for power generation is increasing significantly. Various countries are investing in the wind energy market which likely to increase the requirement for maintenance. Middle-East and Africa region witnessing significant growth in wind power plant which is likely to provide the opportunity to the growth of global wind turbine maintenance, repair & overhaul market.

- Asia-Pacific is expected to be the fastest growing region, owing to the largest and fastest increase in wind power installed capacity in 2020.

Wind Turbine MRO Market Trends

Offshore Wind Installations Expected to Witness Signifcant Growth

- As demand for energy is rising, major countries and companies are turning towards the adoption of renewable energy as it has the ability to provide clean energy. The adoption of offshore wind energy with advance technology attracted the countries and companies for high investment.

- By location of deployment, the offshore industry is expected to remain the driver of the global wind turbine industry investments during the forecast period, owing to declining costs and improved technology.

- The global offshore market remained stable in 2020, with 6.06 GW of new additions, almost the same as in 2019. The total cumulative offshore installations have reached 35.3 GW, representing a 21.7% increase in cumulative offshore wind installed capacity over the previous year.

- The offshore wind industry witnessed major installations in 2020. For instance, China installed a 3 GW offshore wind in a single year, followed by the Netherlands (installed 1.5 GW), Belgium (installed 706 MW), the United Kingdom (installed 483 MW), and Germany (237 MW). However, the slowdown of growth in terms of new installation in the United Kingdom was mainly due to the gap between the execution of projects in the Contracts for Difference (CfD) 1 and CfD 2 rounds. Furthermore, in Germany, the slowdown in new installations was primarily caused by unfavorable conditions and a lower level of the short-term offshore wind project pipeline.

- The expected increase in the deployment of wind turbines in more complex and challenging environments, such as farther offshore, coupled with the growing capacity of the wind turbine capacity, has put additional pressure on the operating components of the wind turbine. This results in premature failure of the components, such as gearbox and other components, and is likely to cause a significant downturn in wind farms. Additionally, the costs involved in providing MRO services are much higher than onshore sites. Factors, such as increased material, service, and hard-to-access terrains, are restraining growth compared to onshore facilities.

- Therefore, owing to the above points, offshore wind deployments are expected to witness significant growth in wind turbine maintenance, repair & overhaul market during the forecast period.

Asia-Pacific Expected to be the Fastest Growing Market

- Asia-Pacific is the fastest growing wind energy market in the world, owing to the contribution of China. The region has a cumulative installed capacity of 346.70 GW, of which onshore wind power installed capacity is 336.29 GW and offshore wind power installed capacity is 10.41 GW.

- As of 2020, China had the largest wind power installed capacity in Asia-Pacific, around 278.32 GW. The country is also considered among the top markets in the onshore wind power industry globally. In 2020, China added up to 58.93 GW of new wind power, with 48.94 GW onshore installations and 9.99 GW offshore installations. All of this indicates that China is expected to be the largest market for maintenance, repair, and overhaul services in the Asia-Pacific region.

- On the other hand, India, the second-largest country in the Asia-Pacific region in terms of wind energy installed capacity, sat only with a capacity of 38.625 GW as of 2020. However, over the next ten years, the electricity demand is expected to double in the country of 1.35 billion people. Accordingly, the Indian government has set a target of 175 GW of renewable energy capacity by 2022, of which 60 GW is expected to come from wind energy, and a target of 450 GW by 2030, of which 140 GW is expected to be wind-based generation. The country boasts a technical potential at a 120-meter hub height of a vast 695 GW.

- South Korea also aims to have a total renewable energy capacity of 63.8 GW by 2030, with approximately 18 GW coming from wind power. The international players, such as Orsted, have stated that South Korea may thrive from wind power generation, particularly in offshore areas considering its geographical characteristics.

- This, in turn, is expected to present Asia-Pacific as an excellent business destination for players involved in the global wind turbine maintenance, repair & overhaul business during the forecast period.

Wind Turbine MRO Industry Overview

The global wind turbine maintenance, repair, and overhaul market is moderately fragmented. Some of the key players in this market include Siemens Gamesa Renewable Energy SA, General Electric Company, Suzlon Energy Ltd, ABB Ltd, and Vestas Wind Systems A/S among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Global Renewable Energy Mix, 2020

- 4.3 Wind Power Installed Capacity and Forecast in GW, till 2027

- 4.4 Market Size and Demand Forecast in USD billion, till 2027

- 4.5 Global Average Size of Wind Turbine in MW, 2018-2027

- 4.6 Recent Trends and Developments

- 4.7 Government Policies and Regulations

- 4.8 Market Dynamics

- 4.8.1 Drivers

- 4.8.2 Restraints

- 4.9 Supply Chain Analysis

- 4.10 Porter's Five Forces Analysis

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Consumers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes Products and Services

- 4.10.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Service Type

- 5.2.1 Maintenance

- 5.2.2 Repair

- 5.2.3 Overhaul

- 5.3 Component

- 5.3.1 Gearbox

- 5.3.2 Generators

- 5.3.3 Rotor Blades

- 5.3.4 Other Components

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Siemens Gamesa Renewable Energy SA

- 6.3.2 General Electric Company

- 6.3.3 Stork (a Fluor Company)

- 6.3.4 Moventas Gears Oy

- 6.3.5 ZF Friedrichshafen AG

- 6.3.6 Vestas Wind Systems A/S

- 6.3.7 Suzlon Energy Ltd

- 6.3.8 ABB Ltd

- 6.3.9 Dana SAC UK Ltd

- 6.3.10 Nordex SE

- 6.3.11 Mistras Group

- 6.3.12 Integrated Power Services LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

全球风力发电机运转和维护市场规模、份额、趋势和成长分析报告(2026-2034年)

全球风力发电机运转和维护市场规模、份额、趋势和成长分析报告(2026-2034年) 风力发电机维护服务市场按服务类型、合约类型、零件类型、供应商类型和涡轮机尺寸划分 - 全球预测 2026-2032 年

风力发电机维护服务市场按服务类型、合约类型、零件类型、供应商类型和涡轮机尺寸划分 - 全球预测 2026-2032 年 风力发电机运转和维护市场规模、份额和成长分析(按类型、地点、组件和地区划分)-2026-2033年产业预测

风力发电机运转和维护市场规模、份额和成长分析(按类型、地点、组件和地区划分)-2026-2033年产业预测 风力涡轮机运转及维护市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)风力发电机运转和维护市场按合约类型、涡轮机类型、所有权模式、维护模式、服务供应商类型、服务类型、零件类型和检验方法划分-全球预测,2025-2032年

风力涡轮机运转及维护市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)风力发电机运转和维护市场按合约类型、涡轮机类型、所有权模式、维护模式、服务供应商类型、服务类型、零件类型和检验方法划分-全球预测,2025-2032年 全球风力发电机营运和维护市场:预测至 2032 年 - 按服务类型、组件、部署、维护类型、服务供应商、应用程式和地区进行分析

全球风力发电机营运和维护市场:预测至 2032 年 - 按服务类型、组件、部署、维护类型、服务供应商、应用程式和地区进行分析 全球风力发电机营运与维护市场(按位置、类型、涡轮机拓扑结构和地区划分)- 预测至 2030 年

全球风力发电机营运与维护市场(按位置、类型、涡轮机拓扑结构和地区划分)- 预测至 2030 年 风力发电机运作和维护市场(按应用、服务类型和地区)

风力发电机运作和维护市场(按应用、服务类型和地区) 风力发电机营运与维护 (O&M) 市场 - 成长、未来展望、竞争分析,2025-2033 年全球风力涡轮机营运市场规模(按服务类型、涡轮机容量、组件类型、地区、范围和预测)

风力发电机营运与维护 (O&M) 市场 - 成长、未来展望、竞争分析,2025-2033 年全球风力涡轮机营运市场规模(按服务类型、涡轮机容量、组件类型、地区、范围和预测)

▼