|

市场调查报告书

商品编码

1859020

太阳能光电模组市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Solar PV Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

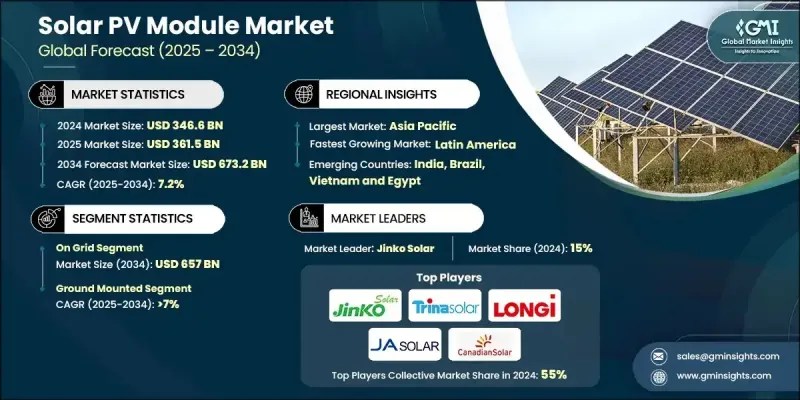

2024年全球太阳能光电模组市场价值为3,466亿美元,预计到2034年将以7.2%的复合年增长率成长至6,732亿美元。

这些系统利用硅等半导体材料製成的光伏电池,将太阳光转化为电能。太阳能组件旨在产生直流电,并可互连成阵列以满足不同的能源需求。技术进步,加上大规模生产效率的提高和安装技术的简化,正在降低成本,使太阳能光电发电更容易普及且更具竞争力。同时,包括激励计画和财政支持政策在内的有利监管环境,正在推动商业、住宅和公用事业用户采用太阳能。日益增强的环保意识和减少碳排放的需求,持续提升人们对太阳能的兴趣。随着企业、政府和个人用户将永续发展努力与清洁能源的使用相结合,全球市场对光伏组件的需求持续增长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3466亿美元 |

| 预测值 | 6732亿美元 |

| 复合年增长率 | 7.2% |

到2034年,併网太阳能市场规模将达到6,570亿美元,这主要得益于组件效率的突破以及单晶硅和双面等先进面板设计技术的进步。这些发展显着提高了能源输出,使併网系统更有效率。不同地区提供的税收优惠和补贴等扶持性财政政策也进一步促进了太阳能的普及应用。

至2034年,地面光伏装置市场将以7%的复合年增长率成长,这主要得益于其适合大规模部署的特性。技术创新,特别是高效能太阳能板和柔性薄膜组件的进步,使得这些装置的成本效益越来越高,对公用事业专案也更具吸引力。此外,它们每平方公尺能提供更多能量的能力也增强了其商业吸引力。

欧洲太阳能光电模组市场预计到2034年将以5%的复合年增长率成长。区域成长得益于不断提高的品质标准、永续发展需求以及旨在实现供应链多元化的各项措施。德国、荷兰和西班牙等国在净计量和企业电力采购策略等政策工具的推动下,正引领太阳能光电模组的普及应用。儘管欧洲的製造能力落后于亚洲市场,但其优势在于先进的应用和整合能力,确保了其竞争优势。

全球太阳能光电模组市场的主要参与者包括隆基、维克拉姆太阳能、天合光能、中新光能科技、晶澳太阳能、REC Solar Holdings、晶科能源、Indosolar、First Solar、Solaria Corporation、RENESOLA、Su-vastika Systems Private Limited、协鑫科技、深圳新光能股份有限公司、SEM PEM IT 有限公司ENERGY、英利太阳能和韩华集团。为了巩固市场地位,太阳能光电模组企业正积极扩大生产规模、投资先进电池技术并建立策略合作伙伴关係。许多企业致力于开发超高效率组件并整合智慧功能,以满足不断变化的消费者需求。此外,各企业也进行地域多元化布局,在需求强劲且政策支持完善的地区建立生产基地。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系统

- 监管环境

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 成长潜力分析

- 价格趋势分析,2021-2034年

- 透过安装

- 按地区

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东

- 非洲

- 拉丁美洲

- 战略仪錶板

- 策略倡议

- 公司标竿分析

- 创新与技术格局

第五章:市场规模及预测:依技术划分,2021-2034年

- 主要趋势

- 薄膜

- 晶体硅

第六章:市场规模及预测:依产品划分,2021-2034年

- 主要趋势

- 单晶

- 多晶

- 碲化镉

- 非晶硅

- 铜铟镓二硒化物

第七章:市场规模及预测:以连结方式划分,2021-2034年

- 主要趋势

- 并网

- 离网

第八章:市场规模及预测:以安装量计算,2021-2034年

- 主要趋势

- 地面安装

- 屋顶

第九章:市场规模及预测:依最终用途划分,2021-2034年

- 主要趋势

- 住宅

- 商业及工业

- 公用事业

第十章:市场规模及预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 奥地利

- 挪威

- 丹麦

- 芬兰

- 法国

- 德国

- 义大利

- 瑞士

- 西班牙

- 瑞典

- 英国

- 荷兰

- 波兰

- 比利时

- 爱尔兰

- 波罗的海

- 葡萄牙

- 亚太地区

- 中国

- 澳洲

- 印度

- 日本

- 韩国

- 泰国

- 菲律宾

- 越南

- 马来西亚

- 新加坡

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿联酋

- 约旦

- 阿曼

- 科威特

- 土耳其

- 非洲

- 南非

- 埃及

- 阿尔及利亚

- 奈及利亚

- 摩洛哥

- 拉丁美洲

- 巴西

- 智利

- 阿根廷

- 秘鲁

第十一章:公司简介

- CsunSolarTech

- Canadian Solar

- EMMVEE SOLAR

- First Solar

- GCL-SI

- Hanwha Group

- Indosolar

- Jinko Solar

- JA SOLAR Technology Co.Ltd.

- LONGi

- RENESOLA

- RISEN ENERGY Co. LTD

- REC Solar Holdings AS

- Shenzhen Shine Solar Co.Ltd

- SOLAR FRONTIER KK

- SunPower Corporation

- Su-vastika Systems Private Limited

- The Solaria Corporation

- Trina Solar

- VIKRAM SOLAR LTD

- Yingli Solar

The Global Solar PV Module Market was valued at USD 346.6 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 673.2 billion by 2034.

These systems harness sunlight and transform it into electricity using photovoltaic cells made of semiconducting materials like silicon. Solar modules are designed to generate direct current (DC) electricity and can be interconnected in arrays to meet diverse energy requirements. Technological improvements, coupled with mass manufacturing efficiencies and simplified installation techniques, are driving down costs, making solar PV more accessible and competitive. Simultaneously, favorable regulatory environments, including incentive programs and financial support policies, are pushing solar adoption among commercial, residential, and utility-scale users. Growing environmental consciousness and the need to cut down carbon emissions continue to strengthen interest in solar energy. With corporations, governments, and individual users aligning their sustainability efforts with clean energy usage, the demand for PV modules continues to rise across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $346.6 Billion |

| Forecast Value | $673.2 Billion |

| CAGR | 7.2% |

The on-grid segment will reach USD 657 billion by 2034, owing to breakthroughs in module efficiency and advanced panel designs such as monocrystalline and bifacial technologies. These developments significantly boost energy output, making grid-connected systems more efficient. Supportive financial policies such as tax incentives and rebate schemes offered across different regions further encourage solar energy adoption.

The ground-mounted solar installations segment will grow at a CAGR of 7% through 2034, driven by its suitability for large-scale deployments. Technological innovation, particularly in high-efficiency panels and flexible thin-film modules, is making these installations increasingly cost-effective and attractive for utility projects. Their ability to deliver more energy per square meter enhances their commercial appeal.

Europe Solar PV Module Market is projected to grow at 5% CAGR through 2034. Regional growth is supported by rising quality standards, sustainability demands, and initiatives aimed at diversifying supply chains. Countries like Germany, the Netherlands, and Spain are spearheading adoption, aided by policy instruments such as net metering and corporate power procurement strategies. Though manufacturing in Europe lags Asian markets, its strength lies in advanced applications and integration capabilities that ensure a competitive edge.

Key players in the Global Solar PV Module Market include LONGi, VIKRAM SOLAR, Trina Solar, CSUN SolarTech, JA SOLAR Technology, REC Solar Holdings, Jinko Solar, Indosolar, First Solar, The Solaria Corporation, RENESOLA, Su-vastika Systems Private Limited, GCL-SI, Shenzhen Shine Solar Co.Ltd, SOLAR FRONTIER, SunPower Corporation, Canadian Solar, EMMVEE SOLAR, RISEN ENERGY, Yingli Solar, and Hanwha Group. To strengthen their presence, solar PV module companies are actively expanding manufacturing facilities, investing in advanced cell technologies, and forming strategic partnerships. Many are focusing on developing ultra-high-efficiency modules and integrating smart features to cater to evolving consumer preferences. Companies are also diversifying geographically, establishing production units in regions with strong demand and supportive policy frameworks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research & validation

- 1.3.1 Primary sources

- 1.4 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Product trends

- 2.5 Mounting trends

- 2.6 Connectivity trends

- 2.7 End Use trends

- 2.8 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Price trend analysis, 2021-2034

- 3.5.1 By mounting

- 3.5.2 By region

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Thin Film

- 5.3 Crystalline Silicon

Chapter 6 Market Size and Forecast, By Product, 2021 - 2034 (USD Billion & MW)

- 6.1 Key trends

- 6.2 Monocrystalline

- 6.3 Polycrystalline

- 6.4 Cadmium Telluride

- 6.5 Amorphous Silicon

- 6.6 Copper Indium Gallium Diselenide

Chapter 7 Market Size and Forecast, By Connectivity, 2021 - 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 On Grid

- 7.3 Off Grid

Chapter 8 Market Size and Forecast, By Mounting, 2021 - 2034 (USD Billion & MW)

- 8.1 Key trends

- 8.2 Ground Mounted

- 8.3 Roof Top

Chapter 9 Market Size and Forecast, By End Use, 2021 - 2034 (USD Billion & MW)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial & Industrial

- 9.4 Utility

Chapter 10 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion & MW)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Austria

- 10.3.2 Norway

- 10.3.3 Denmark

- 10.3.4 Finland

- 10.3.5 France

- 10.3.6 Germany

- 10.3.7 Italy

- 10.3.8 Switzerland

- 10.3.9 Spain

- 10.3.10 Sweden

- 10.3.11 UK

- 10.3.12 Netherlands

- 10.3.13 Poland

- 10.3.14 Belgium

- 10.3.15 Ireland

- 10.3.16 Baltics

- 10.3.17 Portugal

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 India

- 10.4.4 Japan

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Philippines

- 10.4.8 Vietnam

- 10.4.9 Malaysia

- 10.4.10 Singapore

- 10.5 Middle East

- 10.5.1 Israel

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.5.4 Jordan

- 10.5.5 Oman

- 10.5.6 Kuwait

- 10.5.7 Turkey

- 10.6 Africa

- 10.6.1 South Africa

- 10.6.2 Egypt

- 10.6.3 Algeria

- 10.6.4 Nigeria

- 10.6.5 Morocco

- 10.7 Latin America

- 10.7.1 Brazil

- 10.7.2 Chile

- 10.7.3 Argentina

- 10.7.4 Peru

Chapter 11 Company Profiles

- 11.1 CsunSolarTech

- 11.2 Canadian Solar

- 11.3 EMMVEE SOLAR

- 11.4 First Solar

- 11.5 GCL-SI

- 11.6 Hanwha Group

- 11.7 Indosolar

- 11.8 Jinko Solar

- 11.9 JA SOLAR Technology Co.Ltd.

- 11.10 LONGi

- 11.11 RENESOLA

- 11.12 RISEN ENERGY Co. LTD

- 11.13 REC Solar Holdings AS

- 11.14 Shenzhen Shine Solar Co.Ltd

- 11.15 SOLAR FRONTIER K.K.

- 11.16 SunPower Corporation

- 11.17 Su-vastika Systems Private Limited

- 11.18 The Solaria Corporation

- 11.19 Trina Solar

- 11.20 VIKRAM SOLAR LTD

- 11.21 Yingli Solar

固定倾斜式太阳能发电市场:2026年至2032年全球预测(依结构类型、材质、容量、安装方式、电池类型、倾斜角度和最终用途划分)金属机架模组市场:材料类型、模组类型、应用、最终用户、通路划分,全球预测(2026-2032年)

固定倾斜式太阳能发电市场:2026年至2032年全球预测(依结构类型、材质、容量、安装方式、电池类型、倾斜角度和最终用途划分)金属机架模组市场:材料类型、模组类型、应用、最终用户、通路划分,全球预测(2026-2032年) 能源智慧解决方案市场分析与预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

能源智慧解决方案市场分析与预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 2026-2034年全球商用和工业光伏组件市场规模、份额、趋势和成长分析报告

2026-2034年全球商用和工业光伏组件市场规模、份额、趋势和成长分析报告 2026年全球併网光电市场报告

2026年全球併网光电市场报告 日光弹簧系统市场-全球产业规模、份额、趋势、机会和预测:按组件、水源、位置、最终用户、地区和竞争格局划分,2021-2031年MPPT光伏控制器市场按类型、输出电流、电池类型、通讯方式、应用领域和分销管道划分,全球预测(2026-2032年)太阳能保险丝市场:按产品类型、额定电压、安装方式、应用和最终用户划分 - 全球预测 2026-2032 年太阳能害虫监测灯市场,按产品类型、害虫类型、应用、最终用户、分销管道和安装类型划分,全球预测,2026-2032年

日光弹簧系统市场-全球产业规模、份额、趋势、机会和预测:按组件、水源、位置、最终用户、地区和竞争格局划分,2021-2031年MPPT光伏控制器市场按类型、输出电流、电池类型、通讯方式、应用领域和分销管道划分,全球预测(2026-2032年)太阳能保险丝市场:按产品类型、额定电压、安装方式、应用和最终用户划分 - 全球预测 2026-2032 年太阳能害虫监测灯市场,按产品类型、害虫类型、应用、最终用户、分销管道和安装类型划分,全球预测,2026-2032年 商业太阳能发电市场按系统类型、组件、技术、部署方式、应用和地区划分

商业太阳能发电市场按系统类型、组件、技术、部署方式、应用和地区划分