|

市场调查报告书

商品编码

1871279

测试、检验及认证 (TIC) 服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034 年)Testing, Inspection and Certification (TIC) Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

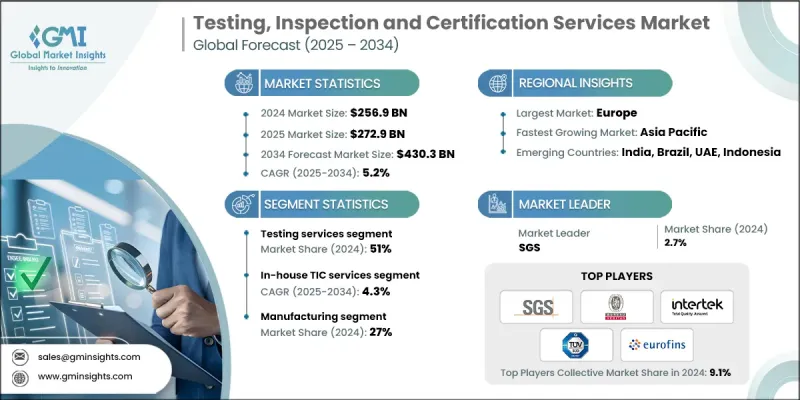

2024 年全球测试、检验和认证 (TIC) 服务市值为 2569 亿美元,预计到 2034 年将以 5.2% 的复合年增长率增长至 4303 亿美元。

检验、认证和合规 (TIC) 服务市场在确保产品品质、安全性和合规性方面发挥着至关重要的作用,涵盖製造业、能源、建筑业和消费品等众多行业。这些服务可协助製造商验证其产品是否符合国内和国际标准,从而在产品进入全球市场前确保其一致性、安全性和可靠性。随着全球贸易的扩张,TIC 服务在降低风险、维护消费者信任和提高营运效率方面变得至关重要。监管合规的重要性日益凸显,尤其是在汽车、医疗保健、食品和电子等行业,这持续推动对 TIC 服务的稳定需求。世界各国政府和私人企业都依赖这些服务来确保产品符合严格的品质、性能和环境法规。国际贸易的日益复杂化和不断提高的安全期望促使企业更加依赖独立的 TIC 服务供应商,这进一步推动了全球市场的成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2569亿美元 |

| 预测值 | 4303亿美元 |

| 复合年增长率 | 5.2% |

北美、欧洲和亚太等地区的政府强制规定正在加速推动对第三方技术资讯认证(TIC)服务的需求。国家和地区主管机关要求对产品进行统一的测试和认证,以保护消费者健康和确保环境安全,无论是在国内还是出口市场。製造商越来越多地与获得认证的TIC服务提供者合作,由其负责合规性评估,从而有效率地满足国际贸易标准。独立的测试和认证能够验证产品是否符合进口法规和地区技术要求,帮助企业更快进入市场,并降低因召回或出口被拒而造成的高成本风险。

到2024年,测试服务板块占据51%的市场。这些服务广泛应用于医疗保健、製造业、电子产品和消费品等行业,以确保产品性能的准确性和安全性。测试仍然是确认产品符合本地和国际标准的重要步骤。另一方面,检验服务则广泛应用于建筑和农业等行业,用于在产品上市前验证其安全性、品质一致性以及是否符合监管规范。

预计2025年至2034年间,企业内部检测、认证和合规(TIC)服务市场将以4.3%的复合年增长率成长。许多公司倾向于内部开展TIC业务,以保持直接监督并保护专有资讯。内部服务还能提供更快的周转时间、更强的品质保证控制以及与内部合规框架的一致性。采用这种方式的企业通常会投入资金建立检测实验室、购买专用设备并聘请技术人员,确保有效率、保密地提供服务,同时遵守全球标准。

2024年,美国测试、检验和认证(TIC)服务市场规模达637亿美元。该国市场成长的主要驱动力来自製造业,製造业高度依赖TIC服务来维持生产标准、符合法规要求并确保产品可靠性。该产业在支持汽车、电子和机械等关键产业方面发挥着重要作用,凸显了其在维护产品完整性和维持国际市场竞争力方面的重要性。

全球测试、检验和认证 (TIC) 服务市场的主要企业包括 TÜV SÜD、SGS、DEKRA、Eurofins、Bureau Veritas、BSI、DNV、TUV Rheinland、Intertek 和 UL Solutions。这些企业正透过併购和策略联盟来加强其全球影响力,以拓展服务组合和地理覆盖范围。领先企业正大力投资自动化、数位化平台和基于人工智慧的检测工具,以提高测试精度、缩短週转时间并提升效率。为应对日益严格的环境法规,许多企业正在采用以永续发展为导向的测试和合规解决方案。此外,拓展在再生能源、自动驾驶汽车和智慧製造等新兴领域的业务能力也成为企业关注的重点。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预报

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 日益严格的产品安全和品质法规正在更强的执行。

- 新兴经济体的工业化和製造业产出不断提高

- 消费者对经过认证的永续产品的意识和需求不断提高

- 采用数位化和远端检测技术(人工智慧、物联网、区块链)

- 产业陷阱与挑战

- 复杂测试环境的高昂营运和服务成本

- 各地区认证标准存在差异

- 市场机会

- TIC服务在再生能源、电动车和绿色科技领域的拓展

- 网路安全和数位系统认证的需求日益增长

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利分析

- 永续性和环境方面

- 碳足迹评估

- 循环经济一体化

- 电子垃圾管理要求

- 绿色製造倡议

- 用例和应用

- 最佳情况

- 成本效益分析框架

- 内部TIC服务与外包TIC服务成本比较

- 总拥有成本 (TCO) 分析

- 上市时间影响评估

- 合规风险缓解价值分析

- 数位服务交付成本模型与传统服务交付成本模型对比

- 市场成熟度及技术采纳分析

- 按地区分類的TIC市场成熟度评估

- 技术采纳曲线和实施时间表

- 数位转型准备度指数

- 监理协调进展分析

- 产业基准研究

- 客户需求与采购分析

- 供应商选择标准和基准框架

- 合规成本优化策略

- 投资报酬率分析与绩效指标

- 风险管理和业务连续性要求

- 数位能力评估框架

- 品质保证与认证要求

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依服务类型划分,2021-2034年

- 主要趋势

- 测试服务

- 电磁相容性测试

- 电气安全和性能测试

- 机械和材料测试

- 其他的

- 检查服务

- 装运前及货物检验

- 工业场地和设备检查

- 建筑和基础设施检查

- 其他的

- 认证服务

- 产品认证

- 管理系统认证

- 人员认证

- 其他的

- 校准服务

- 仪器校准

- 计量和测量标准

- 其他的

- 其他的

第六章:市场估算与预测:依采购方式划分,2021-2034年

- 主要趋势

- 内部TIC服务

- 内部测试和品质控制实验室

- 专属检验和认证部门

- 企业研发和合规性测试中心

- 其他的

- 外包TIC服务

- 独立的第三方TIC提供者

- 合约检测实验室

- 外部检验和认证机构

- 其他的

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 製造业

- 工业机械设备测试

- 品质控制和工厂审核

- 供应炼和零件验证

- 能源与公用事业

- 再生能源系统测试

- 智慧电网和电池认证

- 核电厂安全检查

- 油气资产完整性评估

- 食品和饮料

- 食品安全和卫生检测

- 包装和标籤合规性

- 供应链可追溯性和原产地验证

- 有机认证和永续发展认证

- 汽车

- 电动汽车测试和认证

- 自动驾驶车辆验证

- 连网汽车网路安全测试

- 车辆检验和认证

- 化学品

- 化学成分和纯度测试

- 危险物质认证

- 环境和监管合规性审计

- 建筑和基础设施

- 建筑材料测试

- 结构完整性检查

- 绿建筑与永续发展认证

- 医疗保健和生命科学

- 生物相容性和灭菌测试

- 药物和临床试验验证

- 医疗器材和软体验证

- 航太与国防

- 航空零件认证

- 国防系统和军事标准测试

- 空间系统资格

- 消费品

- 电器安全测试

- 玩具、纺织品和化妆品认证

- 消费者保护和品质保证

- 其他的

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- 全球顶尖玩家

- Bureau Veritas

- DEKRA

- DNV

- Eurofins Scientific

- Intertek

- SGS

- TUV Rheinland

- TUV SUD

- Regional Champions

- APAVE

- BSI

- Centre Testing International

- CCIC

- CSA

- Lloyd's Register

- SOCOTEC

- UL Solutions

- 新兴参与者和专家

- ALS

- Applus+ Services

- Element Materials Technology

- Kiwa

- NSF International

- QIMA

- RINA

The Global Testing, Inspection, and Certification (TIC) Services Market was valued at USD 256.9 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 430.3 billion by 2034.

The TIC services market plays a vital role in ensuring product quality, safety, and compliance across diverse industries, including manufacturing, energy, construction, and consumer goods. These services help manufacturers verify that their products meet both domestic and international standards, guaranteeing consistency, safety, and reliability before entering global markets. As global trade expands, TIC services are becoming essential in minimizing risk, maintaining consumer trust, and enhancing operational efficiency. The increasing importance of regulatory compliance, particularly in sectors such as automotive, healthcare, food, and electronics, continues to drive steady demand for TIC services. Governments and private entities worldwide depend on these services to ensure that products meet stringent quality, performance, and environmental regulations. The rising complexity of international trade and heightened safety expectations are pushing companies to rely more on independent TIC providers, further strengthening market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $256.9 Billion |

| Forecast Value | $430.3 Billion |

| CAGR | 5.2% |

Government mandates across regions like North America, Europe, and Asia-Pacific are accelerating demand for third-party TIC services. National and regional authorities require consistent product testing and certification to protect consumer health and ensure environmental safety, both domestically and for exports. Manufacturers increasingly partner with accredited TIC service providers to handle compliance assessments, enabling them to meet international trade standards efficiently. Independent testing and certification validate that products adhere to import regulations and regional technical requirements, helping companies gain faster market access and reduce the risk of costly recalls or export rejections.

The testing services segment held a 51% share in 2024. These services are widely applied across healthcare, manufacturing, electronics, and consumer goods sectors to ensure performance accuracy and safety. Testing remains an essential step in confirming compliance with both local and international standards. Inspection services, on the other hand, are widely adopted in industries such as construction and agriculture to verify product safety, quality consistency, and compliance with regulatory norms before market release.

The in-house TIC services segment is projected to grow at a CAGR of 4.3% from 2025 to 2034. Many companies prefer to perform TIC operations internally to maintain direct oversight and safeguard proprietary information. In-house services also provide faster turnaround times, greater control over quality assurance, and alignment with internal compliance frameworks. Organizations investing in this approach often allocate capital to establish testing laboratories, specialized equipment, and technical expertise, ensuring efficient and confidential service delivery while maintaining adherence to global standards.

U.S. Testing, Inspection, and Certification (TIC) Services Market generated USD 63.7 billion in 2024. The country's market growth is primarily driven by the manufacturing sector, which depends heavily on TIC services for maintaining production standards, regulatory compliance, and product reliability. The industry's role in supporting critical sectors such as automotive, electronics, and machinery underscores its importance in maintaining product integrity and sustaining competitiveness in international markets.

Key companies operating in the Global Testing, Inspection and Certification (TIC) Services Market include TUV SUD, SGS, DEKRA, Eurofins, Bureau Veritas, BSI, DNV, TUV Rheinland, Intertek, and UL Solutions. Companies operating in the Testing, Inspection, and Certification (TIC) Services Market are strengthening their global presence through mergers, acquisitions, and strategic alliances to expand their service portfolios and geographical reach. Leading firms are heavily investing in automation, digital platforms, and AI-based inspection tools to improve testing accuracy, reduce turnaround time, and enhance efficiency. Many are adopting sustainability-driven testing and compliance solutions in response to growing environmental regulations. Expanding capabilities in emerging sectors such as renewable energy, autonomous vehicles, and smart manufacturing has also become a key focus.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Sourcing

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing enforcement of stringent product safety and quality regulations

- 3.2.1.2 Rising industrialization and manufacturing output in emerging economies

- 3.2.1.3 Increased consumer awareness and demand for certified, sustainable products

- 3.2.1.4 Adoption of digital and remote inspection technologies (AI, IoT, blockchain)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operational and service costs for complex testing environments

- 3.2.2.2 Variability in certification standards across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of TIC services in renewable energy, EVs, and green technologies

- 3.2.3.2 Growing demand for cybersecurity and digital system certification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability & environmental aspects

- 3.9.1 Carbon Footprint Assessment

- 3.9.2 Circular Economy Integration

- 3.9.3 E-Waste Management Requirements

- 3.9.4 Green Manufacturing Initiatives

- 3.10 Use cases and applications

- 3.11 Best-case scenario

- 3.12 Cost-Benefit Analysis Framework

- 3.12.1 In-House vs Outsourced TIC services cost comparison

- 3.12.2 Total Cost of Ownership (TCO) analysis

- 3.12.3 Time-to-market impact assessment

- 3.12.4 Compliance risk mitigation value analysis

- 3.12.5 Digital vs traditional service delivery cost models

- 3.13 Market maturity & technology adoption analysis

- 3.13.1 TIC market maturity assessment by region

- 3.13.2 technology adoption curves & implementation timelines

- 3.13.3 digital transformation readiness index

- 3.13.4 regulatory harmonization progress analysis

- 3.13.5 industry benchmarking studies

- 3.14 Client Requirements & Procurement Analysis

- 3.14.1 Vendor selection criteria & benchmarking framework

- 3.14.2 Compliance cost optimization strategies

- 3.14.3 ROI analysis & performance metrics

- 3.14.4 Risk management & business continuity requirements

- 3.14.5 Digital capability assessment framework

- 3.14.6 Quality assurance & accreditation requirement

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Testing Services

- 5.2.1 Electromagnetic compatibility testing

- 5.2.2 Electrical safety and performance testing

- 5.2.3 Mechanical and materials testing

- 5.2.4 Others

- 5.3 Inspection Services

- 5.3.1 Pre-shipment and consignment inspection

- 5.3.2 Industrial site and equipment inspection

- 5.3.3 Construction and infrastructure inspection

- 5.3.4 Others

- 5.4 Certification Services

- 5.4.1 Product certification

- 5.4.2 Management system certification

- 5.4.3 Personnel certification

- 5.4.4 Others

- 5.5 Calibration Services

- 5.5.1 Instrument calibration

- 5.5.2 Metrology and measurement standards

- 5.5.3 Others

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Sourcing, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 In-House TIC Services

- 6.2.1 Internal testing and quality control laboratories

- 6.2.2 Captive inspection and certification departments

- 6.2.3 Corporate R&D and compliance testing centers

- 6.2.4 Others

- 6.3 Outsourced TIC Services

- 6.3.1 Independent third-party TIC providers

- 6.3.2 Contract-based testing laboratories

- 6.3.3 External inspection and certification bodies

- 6.3.4 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Manufacturing

- 7.2.1 Industrial machinery and equipment testing

- 7.2.2 Quality control and factory audits

- 7.2.3 Supply chain and component verification

- 7.3 Energy and Utilities

- 7.3.1 Renewable energy system testing

- 7.3.2 Smart grid and battery certification

- 7.3.3 Nuclear plant safety inspection

- 7.3.4 Oil and gas asset integrity assessments

- 7.4 Food and Beverages

- 7.4.1 Food safety and hygiene testing

- 7.4.2 Packaging and labeling compliance

- 7.4.3 Supply chain traceability and origin verification

- 7.4.4 Organic and sustainability certifications

- 7.5 Automotive

- 7.5.1 Electric vehicle testing and certification

- 7.5.2 Autonomous vehicle validation

- 7.5.3 Connected car cybersecurity testing

- 7.5.4 Vehicle inspection and homologation

- 7.6 Chemicals

- 7.6.1 Chemical composition and purity testing

- 7.6.2 Hazardous material certification

- 7.6.3 Environmental and regulatory compliance audits

- 7.7 Construction and Infrastructure

- 7.7.1 Building materials testing

- 7.7.2 Structural integrity inspections

- 7.7.3 Green building and sustainability certification

- 7.8 Healthcare and Life Sciences

- 7.8.1 Biocompatibility and sterilization testing

- 7.8.2 Pharmaceutical and clinical trial validation

- 7.8.3 Medical device and software validation

- 7.9 Aerospace and Defense

- 7.9.1 Aviation component certification

- 7.9.2 Defense system and military standards testing

- 7.9.3 Space system qualification

- 7.10 Consumer Products

- 7.10.1 Electrical appliance safety testing

- 7.10.2 Toy, textile, and cosmetic certification

- 7.10.3 Consumer protection and quality assurance

- 7.11 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Top Global Players

- 9.1.1 Bureau Veritas

- 9.1.2 DEKRA

- 9.1.3 DNV

- 9.1.4 Eurofins Scientific

- 9.1.5 Intertek

- 9.1.6 SGS

- 9.1.7 TUV Rheinland

- 9.1.8 TUV SUD

- 9.2 Regional Champions

- 9.2.1 APAVE

- 9.2.2 BSI

- 9.2.3 Centre Testing International

- 9.2.4 CCIC

- 9.2.5 CSA

- 9.2.6 Lloyd's Register

- 9.2.7 SOCOTEC

- 9.2.8 UL Solutions

- 9.3 Emerging Players & Specialists

- 9.3.1 ALS

- 9.3.2 Applus+ Services

- 9.3.3 Element Materials Technology

- 9.3.4 Kiwa

- 9.3.5 NSF International

- 9.3.6 QIMA

- 9.3.7 RINA

2026年全球医疗设备测试、检验及认证市场报告

2026年全球医疗设备测试、检验及认证市场报告 测试、检验和认证 (TIC):市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)

测试、检验和认证 (TIC):市场份额分析、行业趋势和统计数据、成长预测 (2026-2031) OFTEC 测试服务市场:按服务类型、设备类型、测试模式和最终用户划分,全球预测,2026-2032 年商业智慧测试服务市场:全球预测(2026-2032 年),按测试类型、测试等级、服务模式、部署类型、产业垂直领域和公司规模划分海事认证服务市场按服务、认证标准、公司规模、方法论、应用和最终用户产业划分,全球预测(2026-2032年)欧洲测试、检定和认证 (TIC):市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)

OFTEC 测试服务市场:按服务类型、设备类型、测试模式和最终用户划分,全球预测,2026-2032 年商业智慧测试服务市场:全球预测(2026-2032 年),按测试类型、测试等级、服务模式、部署类型、产业垂直领域和公司规模划分海事认证服务市场按服务、认证标准、公司规模、方法论、应用和最终用户产业划分,全球预测(2026-2032年)欧洲测试、检定和认证 (TIC):市场份额分析、行业趋势和统计数据、成长预测 (2026-2031) 测试、检验和认证 (TIC) 市场规模、份额和成长分析(按采购方式、服务类型、应用、最终用户和地区划分)—2026-2033 年行业预测

测试、检验和认证 (TIC) 市场规模、份额和成长分析(按采购方式、服务类型、应用、最终用户和地区划分)—2026-2033 年行业预测 航太与生命科学测试、检验和认证市场规模、份额及成长分析(按采购方式、服务、应用和地区划分)-产业预测(2026-2033 年)2025年测试、检验和认证全球市场报告

航太与生命科学测试、检验和认证市场规模、份额及成长分析(按采购方式、服务、应用和地区划分)-产业预测(2026-2033 年)2025年测试、检验和认证全球市场报告 实验·检验·认证(TIC)的全球市场(~2035年):各服务形式,采购类别,各用途类型,不同企业规模,各主要地区,产业趋势,预测

实验·检验·认证(TIC)的全球市场(~2035年):各服务形式,采购类别,各用途类型,不同企业规模,各主要地区,产业趋势,预测