|

市场调查报告书

商品编码

1871280

汽车资讯通信技术服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive TIC Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

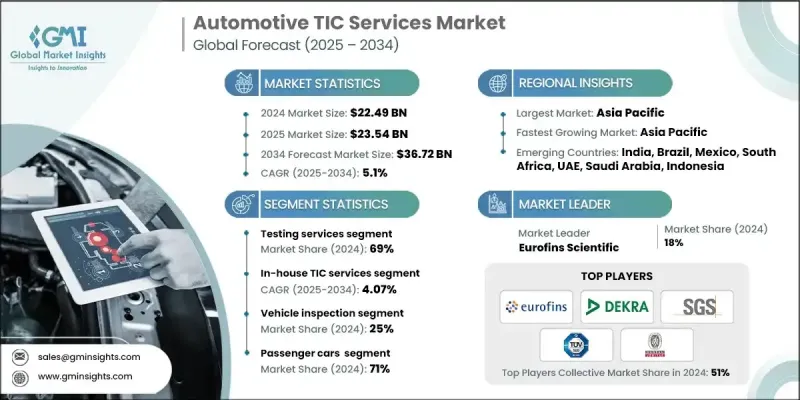

2024 年全球汽车 TIC 服务市值为 224.9 亿美元,预计到 2034 年将以 5.1% 的复合年增长率增长至 367.2 亿美元。

汽车技术资讯认证 (TIC) 产业已成为不断发展的出行格局中不可或缺的一部分,确保配备电动动力系统、数位系统和连网技术的现代车辆符合严格的安全、性能和环保标准。这些服务验证每个组件和流程是否符合国际和地区法规,从而支援汽车产业转型为永续和智慧。随着电动和混合动力车在全球的普及,对 TIC 服务的需求持续增长,这需要对电池系统、零排放推进系统和连网软体平台进行更复杂的验证。此外,主要经济体各国政府实施的严格法规也推动了对独立验证和认证的需求,以确保符合碳中和目标和安全要求。针对电动车和自动驾驶汽车的新全球标准的推出也提高了测试要求,从而推动了全球 TIC 服务供应商的稳定成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 224.9亿美元 |

| 预测值 | 367.2亿美元 |

| 复合年增长率 | 5.1% |

2024年,测试服务业务占据了69%的市场份额,预计到2034年将以4.53%的复合年增长率成长。该业务的领先地位归功于不断发展的监管标准和技术复杂性,这些因素要求对车辆性能和安全性进行持续验证。测试仍然是汽车合规性的基石,因为它在车辆交付给消费者之前评估其耐久性、排放、安全机制和整体功能。不同区域市场对精度和可靠性的日益增长的需求,并持续推动测试服务业务的发展。

2024年,企业内部测试业务占59%的市场份额,预计2025年至2034年将以4.07%的复合年增长率成长。企业倾向于采用内部测试与认证(TIC)营运模式,以全面控製品质保证、资料安全以及与内部生产系统的整合。拥有专用测试基础设施的大型汽车原始设备製造商(OEM)依靠内部验证来满足严格的监管要求并确保製造标准的一致性。这种方法能够加快认证速度并实现更深入的流程优化,从而巩固了该领域在全球市场的主导地位。

亚太地区汽车检测、测试和认证服务市场占38%的市场份额,预计2024年市场规模将达到85.3亿美元。该地区的领先地位得益于其庞大的汽车生产能力、不断完善的监管体係以及先进的技术。亚太各国正在扩展车辆测试框架,以满足更高的安全和排放标准。此外,该地区持续的工业化进程以及对电动车和智慧网联汽车测试设施的投资也推动了市场成长。

汽车检测与认证服务市场的主要参与者包括TUV莱茵、Eurofins Scientific、DEKRA、BSI、必维国际检验集团、Intertek、SGS、TUV SUD和DNV GL。这些领先企业正致力于策略扩张、数位转型和合作伙伴关係,以巩固其市场地位。许多公司正在投资自动化和人工智慧驱动的测试解决方案,以提高效率、缩短测试时间并提升准确性。与汽车原始设备製造商 (OEM) 和政府机构的合作有助于服务提供者适应新兴的监管框架,并为电动车和自动驾驶汽车开发先进的测试能力。此外,各公司也透过併购和合资等方式拓展地域范围,以进入新市场并实现服务组合多元化。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预报

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 严格的监理合规

- 汽车产业的全球化

- 车辆性能测试的需求日益增长

- 消费者对品质保证的需求

- 汽车系统的技术进步

- 产业陷阱与挑战

- 先进TIC设备成本高昂

- 复杂的监管环境

- 市场机会

- 新兴市场的成长机会

- 电动和自动驾驶汽车的研发

- 扩充商用车TIC服务

- OEM厂商将TIC服务外包

- 成长驱动因素

- 成长潜力分析

- 专利分析

- 波特的分析

- PESTEL 分析

- 成本細項分析

- 技术格局

- 当前技术趋势

- 新兴技术

- 监管环境

- 价格趋势

- 按地区

- 透过服务

- 永续性和环境合规性

- 碳足迹和排放测试

- 生命週期评估 (LCA) 服务

- 循环经济和可回收性测试

- 环境永续性认证

- 绿色车辆合规标准

- 成本优化与投资报酬率分析

- TIC服务投资报酬分析

- 成本效益评估框架

- 总拥有成本模型

- 产能利用率和资源优化

- 实验室能力分析

- 设备利用率

- 劳动生产力指标

- 外包与内部决策分析

- 自製与外购决策框架

- 核心能力评估

- 风险收益分析

- 服务水平协议基准测试

- 服务等级协定 (SLA) 效能标准

- 品质指标和关键绩效指标

- 惩罚与激励机制

- 汽车测试中的网路安全

- 软体安全测试与验证

- 漏洞评估和渗透测试

- ISO/SAE 21434 合规性与标准

- 互联自动驾驶汽车网路安全

- 快速上市和敏捷测试

- 加速测试方案

- 并行测试方法

- 快速认证途径

- 压缩开发週期策略

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新采购计划

- 扩张计划和资金

第五章:市场估算与预测:依服务类型划分,2021-2034年

- 主要趋势

- 测试服务

- 检查服务

- 认证服务

- 其他的

第六章:市场估算与预测:依采购方式划分,2021-2034年

- 主要趋势

- 内部

- 外包

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 车辆检查

- 排放测试

- 组件测试

- 车载资讯系统

- 高级驾驶辅助系统

- 认证测试

- 燃料、液体和润滑油

- 电气系统和组件

- 其他的

第八章:市场估算与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 印尼

- 菲律宾

- 泰国

- 韩国

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- 全球参与者

- BSI

- Bureau Veritas

- DEKRA

- DNV GL

- Eurofins Scientific

- Intertek

- Kiwa

- RINA

- SGS

- TUV Rheinland

- TUV SUD

- UL Solutions

- 区域玩家

- ALS

- Applus+ Services

- MISTRAS

- NSF International

- SOCOTEC

- The Smithers

- TUV NORD

- UTAC CERAM

- 新兴参与者/颠覆者

- AVL

- Element Materials Technology

- ESCRYPT

- ETAS

- Keysight Technologies

The Global Automotive TIC Services Market was valued at USD 22.49 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 36.72 billion by 2034.

The automotive TIC sector has become a fundamental part of the evolving mobility landscape, ensuring that modern vehicles equipped with electric powertrains, digital systems, and connected technologies meet rigorous safety, performance, and environmental standards. These services validate that every component and process complies with international and regional regulations, supporting the automotive industry's transition toward sustainable and intelligent mobility. The demand for TIC services continues to rise as electric and hybrid vehicles expand globally, requiring more sophisticated validation for battery systems, emissions-free propulsion, and connected software platforms. In addition, the implementation of stringent regulations by governments across major economies is driving the need for independent verification and certification to ensure compliance with carbon neutrality goals and safety mandates. The introduction of new global standards for electric and autonomous vehicles has also intensified testing requirements, fueling steady growth for TIC providers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.49 Billion |

| Forecast Value | $36.72 Billion |

| CAGR | 5.1% |

The testing services segment held a 69% share in 2024 and is projected to grow at a 4.53% CAGR through 2034. The segment's dominance is attributed to evolving regulatory standards and technological complexity that demand continuous validation of vehicle performance and safety. Testing remains the cornerstone of automotive compliance as it assesses durability, emissions, safety mechanisms, and overall functionality before vehicles reach consumers. The rising need for precision and reliability across diverse regional markets continues to propel the testing services segment forward.

The in-house segment held a 59% share in 2024 and is estimated to register a 4.07% CAGR from 2025 to 2034. Companies favor in-house TIC operations to maintain full control over quality assurance, data security, and integration with internal production systems. Large automotive OEMs with dedicated testing infrastructure rely on in-house validation to meet strict regulatory requirements and ensure consistent manufacturing standards. This approach enables faster certification timelines and deeper process optimization, which has strengthened the dominance of this segment in the global market.

Asia Pacific Automotive TIC Services Market held a 38% share and generated USD 8.53 billion in 2024. The region's leadership is due to its vast automotive production capacity, regulatory evolution, and technological progress. Countries across APAC are expanding their vehicle testing frameworks to meet higher safety and emissions standards. The region's continuous industrialization and investment in electric and connected vehicle testing facilities are also propelling market growth.

Prominent players in the Automotive TIC Services Market include TUV Rheinland, Eurofins Scientific, DEKRA, BSI, Bureau Veritas, Intertek, SGS, TUV SUD, and DNV GL. Leading companies in the Automotive TIC Services Market are focusing on strategic expansion, digital transformation, and partnerships to strengthen their market position. Many firms are investing in automated and AI-driven testing solutions to improve efficiency, reduce testing times, and enhance accuracy. Collaborations with automotive OEMs and government bodies help providers align with emerging regulatory frameworks and develop advanced testing capabilities for electric and autonomous vehicles. Companies are also expanding geographically through mergers, acquisitions, and joint ventures to access new markets and diversify service portfolios.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Sourcing

- 2.2.4 Application

- 2.2.5 Vehicle

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent regulatory compliance

- 3.2.1.2 Globalization of the automotive industry

- 3.2.1.3 Rising demand for vehicle performance testing

- 3.2.1.4 Consumer demand for quality assurance

- 3.2.1.5 Technological advancements in automotive systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced TIC equipment

- 3.2.2.2 Complex regulatory environment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth opportunities in emerging markets

- 3.2.3.2 Development of electric and autonomous vehicles

- 3.2.3.3 Expansion of commercial vehicle TIC services

- 3.2.3.4 Outsourcing of TIC services by OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Cost breakdown analysis

- 3.8 Technology landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia Pacific

- 3.9.4 Latin America

- 3.9.5 Middle East and Africa

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By service

- 3.11 Sustainability & environmental compliance

- 3.11.1 Carbon footprint and emissions testing

- 3.11.2 Lifecycle assessment (LCA) services

- 3.11.3 Circular economy and recyclability testing

- 3.11.4 Environmental sustainability certifications

- 3.11.5 Green vehicle compliance standards

- 3.12 Cost optimization & ROI analysis

- 3.12.1 TIC service investment return analysis

- 3.12.2 Cost-benefit assessment framework

- 3.12.3 Total cost of ownership models

- 3.13 Capacity utilization & resource optimization

- 3.13.1 Laboratory capacity analysis

- 3.13.2 Equipment utilization rates

- 3.13.3 Workforce productivity metrics

- 3.14 Outsourcing vs in-house decision analysis

- 3.14.1 Make vs buy decision framework

- 3.14.2 Core competency assessment

- 3.14.3 Risk-benefit analysis

- 3.15 Service level agreement benchmarking

- 3.15.1 SLA performance standards

- 3.15.2 Quality metrics & KPIs

- 3.15.3 Penalty & incentive structures

- 3.16 Cybersecurity in automotive testing

- 3.16.1 Software security testing and validation

- 3.16.2 Vulnerability assessment and penetration testing

- 3.16.3 ISO/SAE 21434 compliance and standards

- 3.16.4 Connected and autonomous vehicle cybersecurity

- 3.17 Speed to market & agile testing

- 3.17.1 Accelerated testing protocols

- 3.17.2 Parallel testing methodologies

- 3.17.3 Rapid certification pathways

- 3.17.4 Compressed development cycle strategies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New sourcing launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 (USD Bn)

- 5.1 Key trends

- 5.2 Testing services

- 5.3 Inspection services

- 5.4 Certification services

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Sourcing, 2021 - 2034 (USD Bn)

- 6.1 Key trends

- 6.2 In-house

- 6.3 Outsourced

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Bn)

- 7.1 Key trends

- 7.2 Vehicle inspection

- 7.3 Emission testing

- 7.4 Component testing

- 7.5 Telematics

- 7.6 ADAS

- 7.7 Homologation testing

- 7.8 Fuels, fluids and lubricants

- 7.9 Electric systems and components

- 7.10 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Bn)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCV)

- 8.3.2 Medium commercial vehicles (MCV)

- 8.3.3 Heavy commercial vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Indonesia

- 9.4.6 Philippines

- 9.4.7 Thailand

- 9.4.8 South Korea

- 9.4.9 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 BSI

- 10.1.2 Bureau Veritas

- 10.1.3 DEKRA

- 10.1.4 DNV GL

- 10.1.5 Eurofins Scientific

- 10.1.6 Intertek

- 10.1.7 Kiwa

- 10.1.8 RINA

- 10.1.9 SGS

- 10.1.10 TUV Rheinland

- 10.1.11 TUV SUD

- 10.1.12 UL Solutions

- 10.2 Regional Players

- 10.2.1 ALS

- 10.2.2 Applus+ Services

- 10.2.3 MISTRAS

- 10.2.4 NSF International

- 10.2.5 SOCOTEC

- 10.2.6 The Smithers

- 10.2.7 TUV NORD

- 10.2.8 UTAC CERAM

- 10.3 Emerging Players / Disruptors

- 10.3.1 AVL

- 10.3.2 Element Materials Technology

- 10.3.3 ESCRYPT

- 10.3.4 ETAS

- 10.3.5 Keysight Technologies

2026年全球汽车测试、检验和认证市场报告

2026年全球汽车测试、检验和认证市场报告 电动车测试、检验和认证市场:按服务类型、动力部件、测试等级和车辆类别划分-2026-2032年全球市场预测

电动车测试、检验和认证市场:按服务类型、动力部件、测试等级和车辆类别划分-2026-2032年全球市场预测 汽车TIC市场:全球产业分析、市场规模、市场份额及按服务、采购方式、应用、车辆类型、国家及地区分類的预测(2026年至2033年)全球静电消除用电离棒市场:按产品类型、安装方式、材料、技术、终端用户产业和分销管道分類的预测(2026-2032年)

汽车TIC市场:全球产业分析、市场规模、市场份额及按服务、采购方式、应用、车辆类型、国家及地区分類的预测(2026年至2033年)全球静电消除用电离棒市场:按产品类型、安装方式、材料、技术、终端用户产业和分销管道分類的预测(2026-2032年) 汽车认证服务市场 - 全球产业规模、份额、趋势、机会及预测(按类型、车辆类型、应用、地区和竞争格局划分,2021-2031年)汽车电磁相容性测试和认证服务市场(按零件类型、动力传动系统、服务类型、车辆类型和最终用户划分)—2026-2032年全球预测

汽车认证服务市场 - 全球产业规模、份额、趋势、机会及预测(按类型、车辆类型、应用、地区和竞争格局划分,2021-2031年)汽车电磁相容性测试和认证服务市场(按零件类型、动力传动系统、服务类型、车辆类型和最终用户划分)—2026-2032年全球预测 汽车TIC市场规模、份额和成长分析(按车辆类型、服务类型、采购类型、供应链服务、应用和地区划分)-产业预测(2026-2033年)

汽车TIC市场规模、份额和成长分析(按车辆类型、服务类型、采购类型、供应链服务、应用和地区划分)-产业预测(2026-2033年) 汽车品质检测人工智慧系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

汽车品质检测人工智慧系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 汽车和医疗设备静电清洗设备:全球市场份额和排名、总收入和需求预测(2025-2031年)汽车测试、检验和认证 (TIC) - 全球市场份额和排名、总收入和需求预测 2025-2031 年

汽车和医疗设备静电清洗设备:全球市场份额和排名、总收入和需求预测(2025-2031年)汽车测试、检验和认证 (TIC) - 全球市场份额和排名、总收入和需求预测 2025-2031 年