|

市场调查报告书

商品编码

1871320

工业风机及鼓风机市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Industrial Fans and Blowers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

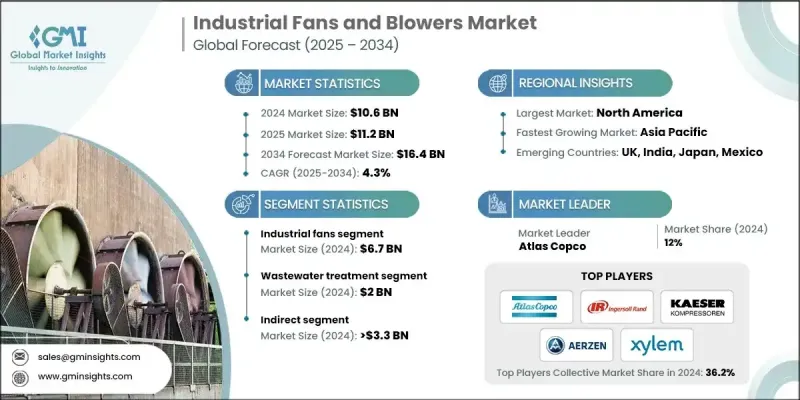

2024 年全球工业风扇和鼓风机市场价值为 106 亿美元,预计到 2034 年将以 4.3% 的复合年增长率增长至 164 亿美元。

工业风机和鼓风机是众多行业不可或缺的组件,它们确保良好的通风,提升工作场所安全,并维持最佳的空气品质。随着各行业日益认识到健康工作环境的重要性,他们正投资于能够降低营运成本、同时提升效率和生产力的技术。製造商也积极响应,不断创新,研发节能高效的系统。豪顿(Howden)和阿特拉斯·科普柯(Atlas Copco)等领先企业致力于提供满足关键行业不断变化的需求的解决方案,涵盖从重型製造业到废水处理等各个领域,并着重强调可持续性、安全性和运行可靠性。日益增强的环保意识和更严格的监管标准进一步加速了风机和鼓风机的应用,使其成为现代工业运作中不可或缺的一部分。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 106亿美元 |

| 预测值 | 164亿美元 |

| 复合年增长率 | 4.3% |

2024年,工业风扇市场规模预计将达67亿美元。由于其在空气循环、排气系统、冷却和除尘等方面的多功能应用,市场需求不断增长。风扇能够更好地调节温度和湿度,改善空气质量,从而显着提高製造工厂、化工厂和资料中心等环境的安全性和生产效率。

预计到2024年,废水处理产业将创造20亿美元的产值。世界各国政府都在加大对废水处理设施的投资,以应对城市人口成长和日益严格的环境法规。风扇和鼓风机在提供曝气、通风和除臭方面至关重要,有助于实现高效合规的废水管理。

预计到2024年,美国工业风机和鼓风机市占率将达到78.7%。该国的工业基础设施推动了包括製造业、化学、能源和暖通空调在内的关键产业的需求。风机和鼓风机对于空气循环、冷却和污染控制至关重要。监管框架和环境政策促进了节能创新解决方案的发展,而持续的城市化和基础设施建设也为市场的持续扩张提供了支持。

全球工业风机和鼓风机市场的主要参与者包括英格索兰 (Ingersoll Rand)、索法科 (Sofaco)、凯撒 (Kaeser)、凯国际 (Kay International)、皮勒 (Piller)、艾尔岑 (Aerzen)、布施 (Busch)、纽约鼓风机 (New York Blower)、赛莱默 (Xyda)、欧莱默 (Dicheng). (Savio)、珠峰 (Everest)、阿特拉斯·科普柯 (Atlas Copco) 和大西洋鼓风机 (Atlantic Blower)。这些公司致力于创新、提高效率和拓展市场,以巩固其市场地位。对研发的投入使其能够开发出节能、高性能且维护成本低的产品。与工业製造商、建筑公司和废水处理设施建立策略合作伙伴关係,有助于拓展分销管道并扩大专案覆盖范围。各公司强调永续性和合规性,并将产品定位为对环境负责的解决方案。产品组合的多元化,以满足多个产业和应用的需求,有助于巩固市场地位。行销活动着重宣传营运效率、成本节约和效能可靠性,以建立客户信任。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 工业通风需求不断成长

- 不断扩展的工业应用

- 都市化和基础设施发展

- 安全问题

- 产业陷阱与挑战

- 维护和营运成本

- 竞争性定价压力

- 机会

- 节能智慧通风系统

- 暖通空调和污染控制应用领域的成长

- 成长驱动因素

- 成长潜力分析

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监管环境

- 标准和合规要求

- 区域监理框架

- 认证标准

- 贸易统计(HS编码-8414.59.30)

- 主要进口国

- 主要出口国

- 差距分析

- 风险评估与缓解

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2021-2034年

- 主要趋势

- 工业风扇

- 离心风扇

- 前弯

- 向后弯曲

- 轴流风扇

- 混流风扇

- 横流风扇

- 其他(通风风扇等)

- 离心风扇

- 工业鼓风机

- 容积式鼓风机

- 离心式鼓风机

- 高速涡轮鼓风机

- 多段式离心式鼓风机

- 其他(再生式鼓风机等)

第六章:市场估算与预测:依电源类型划分,2021-2034年

- 主要趋势

- 绳索

- 无线

第七章:市场估计与预测:依产能划分,2021-2034年

- 主要趋势

- 高的

- 中等的

- 低的

第八章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 餐饮

- 废水处理

- 水泥厂

- 钢铁厂

- 矿业

- 发电厂

- 化学

- 石油和天然气

- 航太与国防

- 食品加工

- 纸浆和造纸

- 水处理厂

- 其他的

第九章:市场估算与预测:依配销通路划分,2021-2034年

- 主要趋势

- 直接的

- 间接

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- Aerzen

- Atlantic Blower

- Atlas Copco

- Busch

- Dicheng

- Everest

- Howden

- Ingersoll Rand

- Kaeser

- Kay International

- New York Blower

- Piller

- Savio

- Sofaco

- Xylem

The Global Industrial Fans and Blowers Market was valued at USD 10.6 billion in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 16.4 billion by 2034.

Industrial fans and blowers are essential components across numerous sectors, ensuring proper ventilation, enhancing workplace safety, and maintaining optimal air quality. As industries increasingly recognize the importance of healthier work environments, they are investing in technologies that reduce operational costs while boosting efficiency and productivity. Manufacturers are responding with innovations in energy-efficient and high-performance systems. Leading companies such as Howden and Atlas Copco focus on delivering solutions that meet the evolving needs of critical industries, ranging from heavy manufacturing to wastewater treatment, emphasizing sustainability, safety, and operational reliability. Rising environmental awareness and stricter regulatory standards have further accelerated adoption, making fans and blowers a vital part of modern industrial operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.6 Billion |

| Forecast Value | $16.4 Billion |

| CAGR | 4.3% |

The industrial fans category generated USD 6.7 billion in 2024. Demand is rising due to their multifunctional use in air circulation, exhaust systems, cooling, and dust control. Fans enable better temperature and humidity regulation while improving air quality, which significantly enhances safety and productivity in environments such as manufacturing facilities, chemical plants, and data centers.

The wastewater treatment segment generated USD 2 billion in 2024. Governments worldwide are increasing investments in treatment facilities to address urban population growth and stricter environmental regulations. Fans and blowers are critical in providing aeration, ventilation, and odor control, supporting efficient and compliant wastewater management.

U.S. Industrial Fans and Blowers Market held 78.7% share in 2024. The country's industrial infrastructure drives demand across key sectors, including manufacturing, chemicals, energy, and HVAC. Fans and blowers are critical for air circulation, cooling, and pollution control. Regulatory frameworks and environmental policies promote energy-efficient and innovative solutions, while ongoing urbanization and infrastructure development support continued market expansion.

Major players in the Global Industrial Fans and Blowers Market include Ingersoll Rand, Sofaco, Kaeser, Kay International, Piller, Aerzen, Busch, New York Blower, Xylem, Dicheng, Howden, Savio, Everest, Atlas Copco, and Atlantic Blower. Companies in the Industrial Fans and Blowers Market focus on innovation, efficiency, and market expansion to strengthen their presence. Investment in research and development enables the creation of energy-efficient, high-performance, and low-maintenance products. Strategic partnerships with industrial manufacturers, construction companies, and wastewater management facilities enhance distribution channels and project reach. Companies emphasize sustainability and regulatory compliance, positioning products as environmentally responsible solutions. Diversification of product portfolios to cater to multiple industries and applications strengthens market foothold. Marketing campaigns highlight operational efficiency, cost savings, and performance reliability to build customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Power source

- 2.2.4 Capacity

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for industrial ventilation

- 3.2.1.2 Expanding industrial applications

- 3.2.1.3 Urbanization and infrastructure development

- 3.2.1.4 Security and safety concerns

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Maintenance and operational costs

- 3.2.2.2 Competitive pricing pressure

- 3.2.3 Opportunities

- 3.2.3.1 Energy-efficient and smart ventilation systems

- 3.2.3.2 Growth in HVAC and pollution control applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code-8414.59.30)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Industrial fans

- 5.2.1 Centrifugal fans

- 5.2.1.1 Forward curved

- 5.2.1.2 Backward curved

- 5.2.2 Axial fans

- 5.2.3 Mixed flow fans

- 5.2.4 Cross flow fans

- 5.2.5 Others (Plenum Fans, etc.)

- 5.2.1 Centrifugal fans

- 5.3 Industrial blower

- 5.3.1 Positive displacement blowers

- 5.3.2 Centrifugal blowers

- 5.3.3 High speed turbo blowers

- 5.3.4 Multistage centrifugal blowers

- 5.3.5 Others (regenerative blowers etc.)

Chapter 6 Market Estimates & Forecast, By Power source, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Cord

- 6.3 Cordless

Chapter 7 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 High

- 7.3 Medium

- 7.4 Low

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Wastewater treatment

- 8.4 Cement plant

- 8.5 Steel plant

- 8.6 Mining

- 8.7 Power plant

- 8.8 Chemical

- 8.9 Oil and gas

- 8.10 Aerospace and defense

- 8.11 Food processing

- 8.12 Pulp and paper

- 8.13 Water treatment plant

- 8.14 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aerzen

- 11.2 Atlantic Blower

- 11.3 Atlas Copco

- 11.4 Busch

- 11.5 Dicheng

- 11.6 Everest

- 11.7 Howden

- 11.8 Ingersoll Rand

- 11.9 Kaeser

- 11.10 Kay International

- 11.11 New York Blower

- 11.12 Piller

- 11.13 Savio

- 11.14 Sofaco

- 11.15 Xylem

工业及商业风机及鼓风机市场:依风机类型、压力类型、技术、终端用户产业及通路划分-2026-2032年全球市场预测静电放电风扇市场:依产品类型、技术、电源、应用和最终用户划分,全球预测,2026-2032年工业交流风扇市场:按产品类型、风量、安装方式、马达类型、最终用途产业和应用划分-全球预测,2026-2032年静电消除风扇市场:按类型、应用、最终用户和分销管道划分,全球预测,2026-2032年

工业及商业风机及鼓风机市场:依风机类型、压力类型、技术、终端用户产业及通路划分-2026-2032年全球市场预测静电放电风扇市场:依产品类型、技术、电源、应用和最终用户划分,全球预测,2026-2032年工业交流风扇市场:按产品类型、风量、安装方式、马达类型、最终用途产业和应用划分-全球预测,2026-2032年静电消除风扇市场:按类型、应用、最终用户和分销管道划分,全球预测,2026-2032年 全球工业风扇市场规模、份额、趋势和成长分析报告(2026-2034年)

全球工业风扇市场规模、份额、趋势和成长分析报告(2026-2034年) 日本工业风机和鼓风机市场:规模、份额、趋势和预测:按类型、材质、排气量、应用和地区划分(2026-2034 年)

日本工业风机和鼓风机市场:规模、份额、趋势和预测:按类型、材质、排气量、应用和地区划分(2026-2034 年) 2026年全球风扇与鼓风机市场报告工业捲轴市场按产品类型、材料、电缆长度、应用和最终用户产业划分-2025-2030 年全球预测蒸气吹灰器市场按类型、自动化程度、安装、应用和最终用途产业划分-全球预测,2025-2030 年

2026年全球风扇与鼓风机市场报告工业捲轴市场按产品类型、材料、电缆长度、应用和最终用户产业划分-2025-2030 年全球预测蒸气吹灰器市场按类型、自动化程度、安装、应用和最终用途产业划分-全球预测,2025-2030 年 工业风扇市场规模、份额、趋势分析报告:按产品、流量、应用、最终用途、地区和细分市场预测,2025-2030 年

工业风扇市场规模、份额、趋势分析报告:按产品、流量、应用、最终用途、地区和细分市场预测,2025-2030 年