|

市场调查报告书

商品编码

1876581

人工智慧编排市场机会、成长驱动因素、产业趋势分析及预测(2025-2034 年)AI Orchestration Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

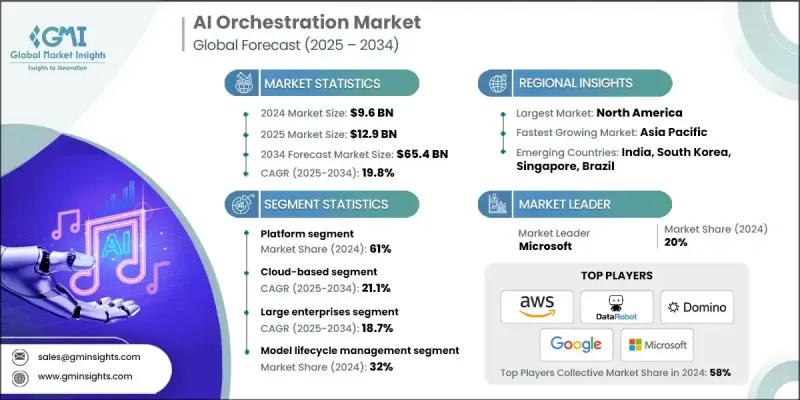

2024 年全球 AI 编排市场价值为 96 亿美元,预计到 2034 年将以 19.8% 的复合年增长率增长至 654 亿美元。

研究机构、超级计算中心和工业应用领域中日益复杂的AI工作负载正在推动对编排解决方案的需求。 AI编排能够无缝管理模型训练、模拟和预测分析,从而提高医疗保健、製造业和科学研究等行业的效率和决策水平。政府和公共部门组织正越来越多地采用AI编排来实现智慧基础设施、交通管理和能源优化。包括美国、中国、德国和巴西在内的多个国家报告称,其40%至55%的机构已部署了编排式AI系统,以实现工作流程自动化、提升营运绩效并简化行政流程。与工业AI应用的整合支援预测性维护、自适应生产和即时监控,帮助企业和政府机构维持弹性、永续和高效的营运。全球大型企业与专注于AI的新创公司之间日益密切的合作也在加速编排平台的普及应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 96亿美元 |

| 预测值 | 654亿美元 |

| 复合年增长率 | 19.8% |

到2024年,平台型解决方案的市占率将达到61%。平台型解决方案之所以备受青睐,是因为它们能够自动部署模型、智慧分配资源、整合治理功能并即时监控模型效能。调查显示,70%的大型企业优先考虑建立强大的平台基础设施,以便在多云和本地环境中有效管理人工智慧工作流程。

预计到2034年,基于云端的部署领域将以21.1%的复合年增长率成长。基于云端的编排提供可扩展性、灵活性和快速资源配置,使其成为研究机构、企业和中小型企业的理想选择。据报道,欧洲研究机构中超过60%的人工智慧专案利用云端编排来管理多云工作流程并促进高效能模型训练。

2024年,美国人工智慧编排市场规模预计将达33亿美元。联邦政府对人工智慧基础设施的大力投资以及《国家人工智慧倡议法案》等政策正在推动人工智慧的普及。多云策略日益流行,编排工具对于管理跨AWS、Azure和Google Cloud等平台的人工智慧工作负载至关重要,同时也能确保符合资料主权和网路安全标准,包括FedRAMP和NIST框架。

全球人工智慧编排市场的主要参与者包括 IBM、NVIDIA、微软、亚马逊 (AWS)、Palantir Technologies、DataRobot、Domino Data Lab、Oracle、Salesforce 和Google (Alphabet)。这些公司正透过投资具备多云和混合云功能的先进人工智慧平台来巩固其市场地位,从而实现人工智慧工作流程在不同环境中的无缝整合。与云端服务供应商、研究机构和产业垂直领域的策略合作,有助于它们拓展业务范围并提高市场接受度。许多公司正在增强自动化、即时监控和治理能力,以提升效能、合规性和可扩展性。併购和合作专案有助于它们拓展技术产品,同时提高市场渗透率。持续创新、以客户为中心的解决方案和全球扩展策略,使这些公司能够巩固其市场地位,并在快速成长的人工智慧编排领域中保持竞争优势。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预报

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 企业对生成式人工智慧和生命週期管理(LLM)的采用日益增长

- 扩展混合云和多云部署

- 日益关注人工智慧的运维化(MLOps + AIOps 融合)

- 人工智慧应用规模激增,协助即时决策

- 产业陷阱与挑战

- 跨异构环境的整合复杂性

- 对云端服务供应商的高度依赖和供应商锁定

- 市场机会

- 面向边缘和物联网生态系统的AI编排技术的发展

- 对自主编排(自优化工作流程)的需求日益增长

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 碳足迹评估

- 循环经济一体化

- 电子垃圾管理要求

- 绿色製造倡议

- 用例和应用

- 最佳情况

- 市场采纳模式

- 企业与中小企业采用趋势对比

- 垂直行业特定采用

- 本机部署、云端部署和混合式部署的采用情况

- 使用无程式码/低程式码编排工具

- 定价和授权模式

- 订阅许可与永久许可

- 基于云端的按需付费模式

- 企业谈判趋势

- 定价对采用率的影响

- 新兴商业模式

- AI 编排即服务 (AIOaaS)

- 平台获利策略

- 透过服务模式实现供应商差异化

- 基于订阅的生态系统模式

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 平台

- 人工智慧编排软体

- 工作流程引擎

- MLOps 整合工具

- 服务

- 部署

- 一体化

- 维护

- 咨询

- 训练

第六章:市场估算与预测:依部署方式划分,2021-2034年

- 主要趋势

- 本地部署

- 基于云端的

- 杂交种

第七章:市场估算与预测:依组织规模划分,2021-2034年

- 主要趋势

- 大型企业

- 中小企业

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 模型生命週期管理

- 数据管道编排

- 工作流程自动化

- 资源最佳化

- 监控与治理

第九章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 金融服务业

- 卫生保健

- 汽车

- 製造业

- 零售与电子商务

- 资讯科技与电信

- 政府和公共部门

- 其他的

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- 全球参与者

- Alibaba Cloud

- Amazon (AWS)

- Google (Alphabet)

- IBM

- Intel

- Microsoft

- NVIDIA

- Oracle

- Salesforce

- SAP

- 区域玩家

- Baidu

- Capgemini

- DataRobot

- Domino Data Lab

- Fujitsu

- Hitachi Vantara

- Huawei Cloud

- Palantir Technologies

- ServiceNow

- Tencent Cloud

- 新兴参与者/颠覆者

- Algorithmia

- C3.ai

- H2O.ai

- MindsDB

- OctoML

- Pachyderm

- Paperspace

- Run:AI

- Spell

- Verta.ai

The Global AI Orchestration Market was valued at USD 9.6 billion in 2024 and is estimated to grow at a CAGR of 19.8% to reach USD 65.4 billion by 2034.

The growing complexity of AI workloads across research institutions, supercomputing centers, and industrial applications is driving the demand for orchestration solutions. AI orchestration enables seamless management of model training, simulations, and predictive analytics, improving efficiency and decision-making across sectors such as healthcare, manufacturing, and scientific research. Governments and public sector organizations are increasingly adopting AI orchestration for smart infrastructure, transportation management, and energy optimization. Countries including the US, China, Germany, and Brazil report that 40-55% of their agencies have implemented orchestrated AI systems to automate workflows, enhance operational performance, and streamline administrative processes. Integration with industrial AI applications supports predictive maintenance, adaptive production, and real-time monitoring, helping enterprises and government agencies maintain resilient, sustainable, and efficient operations. The growing collaboration between large enterprises and AI-focused start-ups worldwide is also accelerating the adoption of orchestration platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.6 Billion |

| Forecast Value | $65.4 Billion |

| CAGR | 19.8% |

The platform segment held 61% share in 2024. Platforms are preferred for their ability to automate model deployment, intelligently allocate resources, integrate governance, and monitor model performance in real time. Surveys indicate that 70% of large organizations prioritize robust platform infrastructure to manage AI workflows effectively across multi-cloud and on-premise environments.

The cloud-based deployment segment is expected to grow at a CAGR of 21.1% through 2034. Cloud-based orchestration offers scalability, flexibility, and rapid resource provisioning, making it ideal for research institutions, enterprises, and small- to medium-sized businesses. Over 60% of AI projects in European research institutions reportedly utilize cloud orchestration to manage multi-cloud workflows and facilitate high-performance model training.

US AI Orchestration Market generated USD 3.3 billion in 2024. Strong federal investments in AI infrastructure and policies like the National AI Initiative Act are driving adoption. Multi-cloud strategies are increasingly popular, and orchestration tools are critical for managing AI workloads across platforms such as AWS, Azure, and Google Cloud while ensuring compliance with data sovereignty and cybersecurity standards, including FedRAMP and NIST frameworks.

Key players in the Global AI Orchestration Market include IBM, NVIDIA, Microsoft, Amazon (AWS), Palantir Technologies, DataRobot, Domino Data Lab, Oracle, Salesforce, and Google (Alphabet). Companies in the AI orchestration market are strengthening their presence by investing in advanced AI platforms with multi-cloud and hybrid capabilities, enabling seamless integration of AI workflows across diverse environments. Strategic partnerships with cloud providers, research institutions, and industry verticals allow them to expand their reach and enhance adoption. Many are enhancing automation, real-time monitoring, and governance capabilities to improve performance, compliance, and scalability. Mergers, acquisitions, and collaborative ventures help broaden their technological offerings while improving market penetration. Continuous innovation, customer-centric solutions, and global expansion strategies enable companies to solidify their foothold and maintain a competitive edge in the rapidly growing AI orchestration landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment

- 2.2.4 Organization Size

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing enterprise adoption of generative AI & LLMs

- 3.2.1.2 Expansion of hybrid and multi-cloud deployments

- 3.2.1.3 Rising focus on operationalizing AI (MLOps + AIOps convergence)

- 3.2.1.4 Surge in AI application scaling for real-time decisioning

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Integration complexity across heterogeneous environments

- 3.2.2.2 High dependency on cloud providers & vendor lock-in

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of AI orchestration for edge and IoT ecosystems

- 3.2.3.2 Rising demand for autonomous orchestration (self-optimizing workflows)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability & environmental aspects

- 3.10.1 Carbon Footprint Assessment

- 3.10.2 Circular Economy Integration

- 3.10.3 E-Waste Management Requirements

- 3.10.4 Green Manufacturing Initiatives

- 3.11 Use cases and applications

- 3.12 Best-case scenario

- 3.13 Market Adoption Patterns

- 3.13.1 Enterprise vs. SME adoption trends

- 3.13.2 Vertical-specific adoption

- 3.13.3 On-premise vs. cloud vs. hybrid deployment adoption

- 3.13.4 Use of no-code/low-code orchestration tools

- 3.14 Pricing and Licensing Models

- 3.14.1 Subscription vs. perpetual licensing

- 3.14.2 Cloud-based pay-per-use models

- 3.14.3 Enterprise negotiation trends

- 3.14.4 Pricing impact on adoption

- 3.15 Emerging Business Models

- 3.15.1 AI orchestration as a service (AIOaaS)

- 3.15.2 Platform monetization strategies

- 3.15.3 Vendor differentiation via service models

- 3.15.4 Subscription-based ecosystem models

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Platform

- 5.2.1 AI orchestration software

- 5.2.2 Workflow engines

- 5.2.3 MLOps integration tools

- 5.3 Services

- 5.3.1 Deployment

- 5.3.2 Integration

- 5.3.3 Maintenance

- 5.3.4 Consulting

- 5.3.5 Training

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 On-Premise

- 6.3 Cloud-Based

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Large Enterprises

- 7.3 Small & Medium Enterprises (SMEs)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Model Lifecycle Management

- 8.3 Data Pipeline Orchestration

- 8.4 Workflow Automation

- 8.5 Resource Optimization

- 8.6 Monitoring & Governance

Chapter 9 Market Estimates & Forecast, By End use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 Healthcare

- 9.4 Automotive

- 9.5 Manufacturing

- 9.6 Retail & E-commerce

- 9.7 IT & Telecom

- 9.8 Government & Public Sector

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Alibaba Cloud

- 11.1.2 Amazon (AWS)

- 11.1.3 Google (Alphabet)

- 11.1.4 IBM

- 11.1.5 Intel

- 11.1.6 Microsoft

- 11.1.7 NVIDIA

- 11.1.8 Oracle

- 11.1.9 Salesforce

- 11.1.10 SAP

- 11.2 Regional Players

- 11.2.1 Baidu

- 11.2.2 Capgemini

- 11.2.3 DataRobot

- 11.2.4 Domino Data Lab

- 11.2.5 Fujitsu

- 11.2.6 Hitachi Vantara

- 11.2.7 Huawei Cloud

- 11.2.8 Palantir Technologies

- 11.2.9 ServiceNow

- 11.2.10 Tencent Cloud

- 11.3 Emerging Players / Disruptors

- 11.3.1 Algorithmia

- 11.3.2 C3.ai

- 11.3.3. H2O.ai

- 11.3.4 MindsDB

- 11.3.5 OctoML

- 11.3.6 Pachyderm

- 11.3.7 Paperspace

- 11.3.8 Run:AI

- 11.3.9 Spell

- 11.3.10 Verta.ai

AI编配市场:按组件、技术、部署模式、组织规模和最终用途划分-2026-2032年全球市场预测

AI编配市场:按组件、技术、部署模式、组织规模和最终用途划分-2026-2032年全球市场预测 2026年全球函数呼叫编配市场报告2026年全球基于帐户的编配平台市场报告2026年全球大规模语言模型(LLM)应用监控市场报告2026年全球大规模语言模型(LLM)网关平台市场报告2026年全球大规模语言模型(LLM)路由器市场报告2026年全球模型并行化编配市场报告2026年全球闭式任务编配市场报告

2026年全球函数呼叫编配市场报告2026年全球基于帐户的编配平台市场报告2026年全球大规模语言模型(LLM)应用监控市场报告2026年全球大规模语言模型(LLM)网关平台市场报告2026年全球大规模语言模型(LLM)路由器市场报告2026年全球模型并行化编配市场报告2026年全球闭式任务编配市场报告 2025-2029年全球人工智慧编配平台市场

2025-2029年全球人工智慧编配平台市场 AI编配市场规模、份额和成长分析(按组件、部署模式、架构类型、组织规模、应用、最终用户和地区划分)-2026-2033年产业预测

AI编配市场规模、份额和成长分析(按组件、部署模式、架构类型、组织规模、应用、最终用户和地区划分)-2026-2033年产业预测