|

市场调查报告书

商品编码

1876651

舷外船用引擎市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Outboard Boats Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

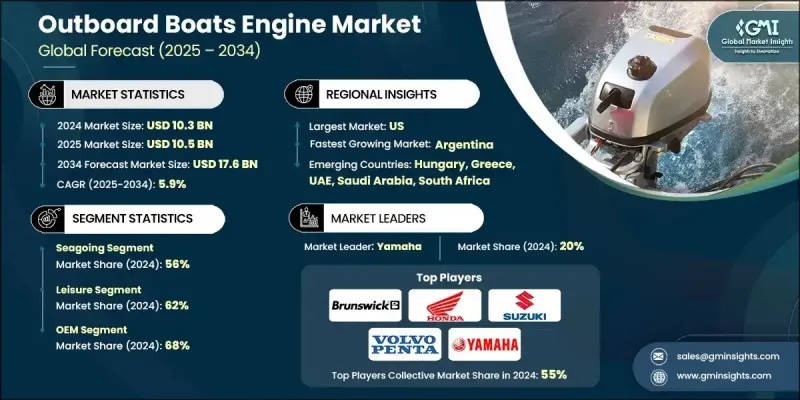

2024 年全球舷外船用引擎市场价值为 103 亿美元,预计到 2034 年将以 5.9% 的复合年增长率增长至 176 亿美元。

随着休閒划船和水上活动在沿海和内陆地区日益普及,对舷外机的需求持续增长。消费者在休閒设备上的支出增加,以及码头基础设施的扩建和旅游业的发展,正在加速预测期内舷外机的普及。製造商推出更轻、更节能、排放更低的先进技术,适用于商业营运和休閒划船,也推动了市场的发展。向四衝程系统和燃油直喷设计的过渡正在增强长期成长,尤其是在排放标准日益严格的背景下。商业捕鱼、小型海上运输和沿海物流对可靠舷外机的依赖性日益增强,也强化了对先进高性能舷外机的需求。沿海开发投资的增加,以及手工和水产养殖活动的扩展,也为引擎供应商创造了更多机会,并支撑着稳定的市场前景。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 103亿美元 |

| 预测值 | 176亿美元 |

| 复合年增长率 | 5.9% |

2024年,远洋航行领域市占率达到56%,预计到2034年将以超过5.9%的复合年增长率成长。人们对沿海旅行、近海探险和水上运动的兴趣日益浓厚,推动了专为高耐久性、远距离航行和更强近海性能而设计的远洋舷外机的应用。此外,由于其反应迅速、性能可靠,远洋航行领域和商业运输中日益广泛的应用也进一步促进了其普及。

2024年,休閒娱乐领域占了62%的市场份额,预计2025年至2034年将以5%的复合年增长率成长。人们对休閒划船、家庭出游和週末水上活动的日益热情,持续推高了中小型船隻舷外发动机的需求。可支配收入的增加、都市生活方式的趋势以及水上休閒活动参与度的提高,都在推动湖泊、海岸和河流沿岸地区的销售成长。

2024年,美国舷外机市场占86%的市场份额,市场规模达35.7亿美元。由于消费者购买力强劲以及码头网路快速发展,休閒船艇市场依然活跃。无论是在咸水或淡水环境中,对渔船、水上摩托车和休閒船艇的需求都在持续增长。美国製造商正致力于研发技术先进的四行程和数位化控制舷外机,以提高燃油经济性、降低排放并提升操控性能。

全球舷外机市场的主要公司包括 Brunswick、Oxe Marine、Yamaha、Honda、Suzuki Motor、Cox Powertrain、Parsun Power Machine、Hidea Power、Volvo Penta 和 Tohatsu。为了满足不断变化的消费者和监管需求,舷外机市场的企业正透过开发燃油效率更高、排放更低、结构更轻的引擎来巩固其市场地位。许多公司正在投资数位控制系统和先进的诊断技术,以提升效能并简化终端用户的维护工作。与船舶製造商的策略合作有助于拓展分销网络并确保长期的OEM合作伙伴关係。此外,各公司也正在提升产能,以满足日益增长的四衝程和高功率引擎的需求。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 休閒钓鱼和水上运动的需求不断增长

- 小型充气便携式船隻越来越受欢迎

- 为了提高多功能性,可以从舷内机切换到舷外机。

- 沿海旅游与海洋休閒产业的扩张

- 对轻量化、节能型推进系统的需求

- 产业陷阱与挑战

- 严格的海洋排放法规

- 噪音和振动问题

- 电动舷外机的续航里程有限

- 大马力车型的前期投入成本较高

- 市场机会

- 电气化与混合动力一体化

- 新兴市场对便携式舷外机的需求

- 生态旅游与永续划船的发展

- 老旧车队的更新换代需求

- 成长驱动因素

- 成长潜力分析

- 主要市场趋势和颠覆性因素

- 未来市场趋势

- 监管环境

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 目前技术

- 先进燃油喷射系统

- 用于海水环境的耐腐蚀材料

- 数位引擎监控与智慧控制

- 新兴技术

- 电动和混合动力舷外推进系统

- 轻质复合材料

- 模组化手提式电源装置

- 联网舷外机(物联网整合)

- 目前技术

- 专利分析

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 价格趋势

- 按地区

- 透过推进

- 定价分析与价值链经济学

- 按马力分類的舷外机价格趋势

- 高马力车型的溢价策略

- 成本结构细分

- 区域价格敏感性

- 成本細項分析

- 组件级成本结构分析

- 製造成本驱动因素和最佳化

- 区域成本差异及其对竞争的影响

- 成本管理策略与竞争定位

- 用例

- 政府和公共安全应用

- 商业港口和码头运营

- 休閒和旅游应用

- 电气化和混合动力整合应用

- 替代燃料与永续推进应用

- 最佳情况

- 加速电气化进程,并提供基础设施支持

- 永续燃料整合与循环经济

- 卓越性能和技术领先地位

- 全球市场扩张与新兴市场发展

- 综合永续性和卓越绩效

- 全球贸易与进出口分析

- 按地区导入相依性

- 贸易法规和关税影响

- 永续性和环境方面

- 减少实体原型製作和测试

- 提高能源效率

- 支援电气化和减排技术

- 电子垃圾生命週期及管理

- 遵守环境法规

- 产品路线图框架

- 创新需求分析

- 受监管驱动的产品开发

- 绩效提升机会

- 永续性和生物基解决方案

- 高阶产品线扩展

- 永续性和生物基解决方案路线图

- 近期永续发展实施方案(2025-2027 年)

- 中期转型策略(2027-2035)

- 长期愿景与碳中和(2035-2050 年)

- 高性能船用引擎应用

- 生物基永续船用润滑油

- 战略意义

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

- 高端定位策略

- 策略性OEM合作伙伴机会

- 技术标准和认证要求

- 策略市场机会

第五章:机油分配概况

- 主要分销管道

- 通道结构

- 分销领域的关键参与者

- 通路经济学

- 分布趋势

- 分销方面的挑战

- 机会

第六章:市场估算与预测:依水路划分,2021-2034年

- 主要趋势

- 远洋

- 閒暇

- 货物运输

- 人员运输

- 钓鱼

- 政府用途

- 内陆

- 閒暇

- 货物运输

- 人员运输

- 钓鱼

- 政府用途

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 閒暇

- 货物运输

- 人员运输

- 钓鱼

- 政府用途

第八章:市场估算与预测:以推进方式划分,2021-2034年

- 主要趋势

- 汽油

- 柴油引擎

- 电的

第九章:市场估算与预测:依销售管道划分,2021-2034年

- 主要趋势

- 原始设备製造商

- 售后市场

第十章:市场估价与预测:依引擎类型划分,2021-2034年

- 主要趋势

- 二衝程

- 四衝程

- 电的

第十一章:市场估计与预测:依电力产业划分,2021-2034年

- 主要趋势

- 低的

- 中

- 高的

第十二章:市场估算与预测:以点火方式划分,2021-2034年

- 主要趋势

- 电的

- 手动的

第十三章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 匈牙利

- 希腊

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十四章:公司简介

- 全球参与者

- Mercury Marine

- Yamaha Motor Company

- Honda Marine

- Suzuki Marine

- Tohatsu

- Regional Champions

- Aquamot

- BRP/Evinrude

- ePropulsion

- Hidea

- Lehr Propane Engines

- Mariner

- OXE Marine

- Parsun

- Powertec Outboards

- Rad Propulsion

- Ray Electric Outboards

- Selva Marine

- Torqeedo

- Volvo Penta

- 新兴参与者和颠覆者

- Aquawatt

- Bixpy

- Candela

- Cox Marine

- Elco Motor Yachts

- Evoy

- Flux Marine

- FPT Neander Motors

- Remigo

- Temo

- Vision Marine Technologies

- Zerojet

The Global Outboard Boats Engine Market was valued at USD 10.3 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 17.6 billion by 2034.

Demand continues to rise as recreational boating and water-based activities gain popularity across coastal and inland regions. Higher consumer spending on leisure equipment, along with expanding marina infrastructure and tourism development, is accelerating the adoption of outboard engines throughout the forecast timeline. The market is also advancing as manufacturers introduce lighter, more fuel-efficient, and lower-emission technologies suitable for both commercial operations and recreational boating. Transitioning toward four-stroke systems and direct fuel-injection designs is strengthening long-term growth, particularly as emission standards continue to tighten. Growing dependence on reliable outboard engines for commercial fishing, small-scale marine transport, and coastal logistics is reinforcing demand for advanced, high-performance models. Rising investments in coastal development, along with expanding artisanal and aquaculture activities, are also enhancing opportunities for engine suppliers and supporting a steady market outlook.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.3 Billion |

| Forecast Value | $17.6 Billion |

| CAGR | 5.9% |

The seagoing segment held a 56% share in 2024 and is expected to grow at a CAGR above 5.9% through 2034. Interest in coastal travel, offshore excursions, and water-sport activities is boosting the utilization of seagoing outboard engines designed for high durability, long-distance travel, and stronger offshore capabilities. Their growing use in marine security operations and commercial transport is further driving adoption due to their fast response and dependable performance.

The leisure segment held a 62% share in 2024 and is projected to grow at a CAGR of 5% from 2025 to 2034. Rising enthusiasm for recreational boating, family outings, and weekend water activities continues to elevate demand for outboard engines across small and mid-sized boats. Higher disposable income, urban lifestyle trends, and expanding participation in marine recreation are fueling sales across lakes, coasts, and river systems.

US Outboard Boats Engine Market held an 86% share and generated USD 3.57 billion in 2024. Recreational boating remains highly active due to strong consumer purchasing power and a rapidly growing marina network. Demand for fishing boats, personal watercraft, and leisure vessels continues to rise across saltwater and freshwater environments. Manufacturers in the US are focusing on technologically enhanced four-stroke and digitally controlled outboard engines that deliver improved fuel economy, lower emissions, and smoother handling.

Major companies in the Global Outboard Boats Engine Market include Brunswick, Oxe Marine, Yamaha, Honda, Suzuki Motor, Cox Powertrain, Parsun Power Machine, Hidea Power, Volvo Penta, and Tohatsu. Companies in the Outboard Boats Engine Market are reinforcing their market position by developing engines with higher fuel efficiency, reduced emissions, and lightweight construction to meet shifting consumer and regulatory expectations. Many firms are investing in digital control systems and advanced diagnostics to elevate performance and simplify maintenance for end users. Strategic collaborations with boat manufacturers help expand distribution networks and secure long-term OEM partnerships. Firms are also enhancing their production capabilities to meet growing demand for four-stroke and high-horsepower engines.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Waterways

- 2.2.3 Application

- 2.2.4 Propulsion

- 2.2.5 Engine

- 2.2.6 Power

- 2.2.7 Ignition

- 2.2.8 Sales channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for recreational fishing & water sports

- 3.2.1.2 Growing popularity of small inflatable & portable boats

- 3.2.1.3 Shift from inboard to outboard engines for versatility

- 3.2.1.4 Expansion of coastal tourism & marine leisure industry

- 3.2.1.5 Demand for lightweight, fuel-efficient propulsion systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent marine emission regulations

- 3.2.2.2 Noise & vibration concerns

- 3.2.2.3 Limited range for electric outboards

- 3.2.2.4 High upfront cost of high-horsepower models

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification & hybrid integration

- 3.2.3.2 Demand for portable outboards in emerging markets

- 3.2.3.3 Growth in eco-tourism & sustainable boating

- 3.2.3.4 Replacement demand from aging fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and disruptions

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current Technologies

- 3.9.1.1 Advanced Fuel Injection Systems

- 3.9.1.2 Corrosion-Resistant Materials for Saltwater Use

- 3.9.1.3 Digital Engine Monitoring & Smart Controls

- 3.9.2 Emerging Technologies

- 3.9.2.1 Electric & Hybrid Outboard Propulsion

- 3.9.2.2 Lightweight Composite Materials

- 3.9.2.3 Modular & Portable Power Units

- 3.9.2.4 Connected Outboards (IoT Integration)

- 3.9.1 Current Technologies

- 3.10 Patent analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Price trends

- 3.12.1 By region

- 3.12.2 By propulsion

- 3.13 Pricing analysis and value chain economics

- 3.13.1 Outboard pricing trends by hp segment

- 3.13.2 Premium pricing strategies in high-hp models

- 3.13.3 Cost structure breakdown

- 3.13.4 Regional price sensitivity

- 3.14 Cost breakdown analysis

- 3.14.1 Component-level cost structure analysis

- 3.14.2 Manufacturing cost drivers and optimization

- 3.14.3 Regional cost variations and competitive implications

- 3.14.4 Cost management strategies and competitive positioning

- 3.15 Use cases

- 3.15.1 Government and Public Safety Applications

- 3.15.2 Commercial Harbor and Port Operations

- 3.15.3 Recreational and Tourism Applications

- 3.15.4 Electrification and Hybrid Integration Applications

- 3.15.5 Alternative Fuel and Sustainable Propulsion Applications

- 3.16 Best-case scenario

- 3.16.1 Accelerated Electrification with Infrastructure Support

- 3.16.2 Sustainable Fuel Integration and Circular Economy

- 3.16.3 Premium Performance and Technology Leadership

- 3.16.4 Global Market Expansion and Emerging Market Development

- 3.16.5 Integrated Sustainability and Performance Excellence

- 3.17 Global trade and import/export analysis

- 3.17.1 Import Dependencies by Region

- 3.17.2 Trade Regulations and Tariff Impact

- 3.18 Sustainability and environmental aspects

- 3.18.1 Reduction of Physical Prototyping and Testing

- 3.18.2 Energy Efficiency Improvements

- 3.18.3 Support for Electrification and Emission Reduction Technologies

- 3.18.4 Lifecycle and E-Waste Management

- 3.18.5 Compliance with Environmental Regulations

- 3.19 Product roadmap framework

- 3.19.1 Innovation Requirements Analysis

- 3.19.2 Regulatory-Driven Product Development

- 3.19.3 Performance Enhancement Opportunities

- 3.19.4 Sustainability and Bio-Based Solutions

- 3.19.5 Premium Product Line Extensions

- 3.20 Sustainability and bio-based solutions roadmap

- 3.20.1 Near-Term Sustainability Implementation (2025-2027)

- 3.20.2 Medium-Term Transition Strategy (2027-2035)

- 3.20.3 Long-Term Vision and Carbon Neutrality (2035-2050)

- 3.21 High-performance marine engine applications

- 3.22 Bio-based and sustainable marine lubricants

- 3.23 Strategic implications

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Premium Positioning Strategies

- 4.8 Strategic OEM Partnership Opportunities

- 4.9 Technical Standards and Certification Requirements

- 4.10 Strategic Market Opportunities

Chapter 5 Landscape of Engine Oil Distribution

- 5.1 Key distribution channels

- 5.2 Channel structure

- 5.3 Key players in distribution

- 5.4 Channel economics

- 5.5 Trends in distribution

- 5.6 Challenges in distribution

- 5.7 Opportunities

Chapter 6 Market Estimates & Forecast, By Waterways, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Seagoing

- 6.2.1 Leisure

- 6.2.2 Transport Of goods

- 6.2.3 Transport Of people

- 6.2.4 Fishing

- 6.2.5 Government use

- 6.3 Inland

- 6.3.1 Leisure

- 6.3.2 Transport Of goods

- 6.3.3 Transport Of people

- 6.3.4 Fishing

- 6.3.5 Government use

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Leisure

- 7.2 Transport Of goods

- 7.3 Transport Of people

- 7.4 Fishing

- 7.5 Government use

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Gasoline

- 8.3 Diesel

- 8.4 Electric

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 2-stroke

- 10.3 4-stroke

- 10.4 Electric

Chapter 11 Market Estimates & Forecast, By Power, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 Low

- 11.3 Mid

- 11.4 High

Chapter 12 Market Estimates & Forecast, By Ignition, 2021 - 2034 ($Bn, Units)

- 12.1 Key trends

- 12.2 Electric

- 12.3 Manual

Chapter 13 Market Estimates & Forecast, By Region, 2021-2034 ($Bn, Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 US

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 UK

- 13.3.2 Germany

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Russia

- 13.3.7 Nordics

- 13.3.8 Hungary

- 13.3.9 Greece

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 ANZ

- 13.4.6 Southeast Asia

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global Players

- 14.1.1 Mercury Marine

- 14.1.2 Yamaha Motor Company

- 14.1.3 Honda Marine

- 14.1.4 Suzuki Marine

- 14.1.5 Tohatsu

- 14.2 Regional Champions

- 14.2.1 Aquamot

- 14.2.2 BRP/Evinrude

- 14.2.3 ePropulsion

- 14.2.4 Hidea

- 14.2.5 Lehr Propane Engines

- 14.2.6 Mariner

- 14.2.7 OXE Marine

- 14.2.8 Parsun

- 14.2.9 Powertec Outboards

- 14.2.10 Rad Propulsion

- 14.2.11 Ray Electric Outboards

- 14.2.12 Selva Marine

- 14.2.13 Torqeedo

- 14.2.14 Volvo Penta

- 14.3 Emerging Players & Disruptors

- 14.3.1 Aquawatt

- 14.3.2 Bixpy

- 14.3.3 Candela

- 14.3.4 Cox Marine

- 14.3.5 Elco Motor Yachts

- 14.3.6 Evoy

- 14.3.7 Flux Marine

- 14.3.8 FPT Neander Motors

- 14.3.9 Remigo

- 14.3.10 Temo

- 14.3.11 Vision Marine Technologies

- 14.3.12 Zerojet