|

市场调查报告书

商品编码

1876795

互联卡车市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Connected Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

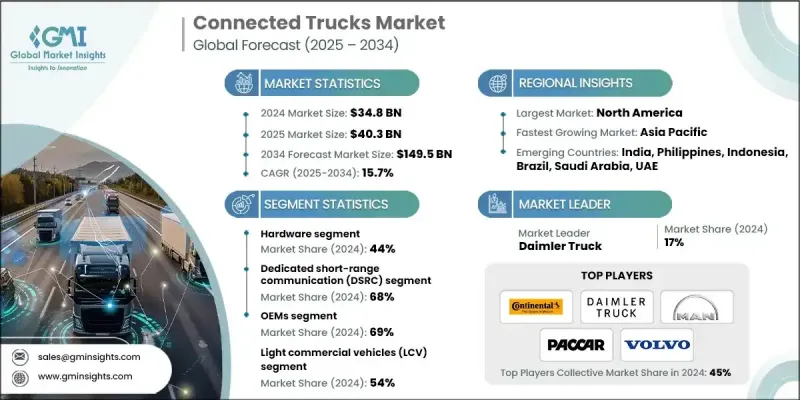

2024 年全球连网卡车市场价值为 348 亿美元,预计到 2034 年将以 15.7% 的复合年增长率成长至 1,495 亿美元。

对互联卡车技术日益增长的需求正在重塑全球物流和长途运输网络。先进的远端资讯处理、预测性车队分析和车内互联技术正在改变营运商监控路线、预测交付时间、优化装载以及最大限度减少空驶或怠速行驶的方式。数位孪生模拟技术使车队管理人员和原始设备製造商 (OEM) 能够以虚拟方式测试营运模式,从而降低成本、提高安全性并提升交付可靠性。随着产业向电动和低排放车队转型,互联卡车平台正被用于管理能源分配、安排充电和优化续航里程效率。智慧充电和车网通讯系统的整合确保了能源使用的平衡并降低了电网压力。此外,在混合车队营运中,互联繫统能够实现动态负载平衡和路线最佳化,从而延长电池寿命。诸如自动煞车、车道维持和卡车编队行驶等高级驾驶辅助技术的快速整合进一步凸显了可靠、低延迟连接的重要性。 OEM 和车队营运商正增加对感测器融合和云端分析的投资,以将即时资料转化为可操作的安全性和合规性洞察。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 348亿美元 |

| 预测值 | 1495亿美元 |

| 复合年增长率 | 15.7% |

2024年,硬体部分占据44%的市场份额,预计到2034年将以13.9%的复合年增长率成长。硬体继续引领市场,因为它构成了实现连接、通讯和远端资讯处理整合的基础框架。包括远端资讯处理控制单元(TCU)、GPS/GNSS设备、感测器和无线通讯模组在内的关键组件,是收集和传输即时运行资料的基础。这些系统支援车辆、云端平台和车队管理网路之间的无缝交互,构成了驱动数位化交通生态系统的实体层。

专用短程通讯 (DSRC) 市场在 2024 年占据了 68% 的市场份额,预计 2025 年至 2034 年将以 15.1% 的复合年增长率成长。 DSRC 技术凭藉其强大的性能和低延迟,仍然是连网卡车的首选通讯方式,这对于即时车对车 (V2V) 和车对基础设施 (V2I) 通讯至关重要。这使得碰撞侦测、车道变更警报和紧急应变系统等增强安全性的应用能够实现即时资料交换。其久经考验的可靠性和符合监管要求的特性,也持续推动 DSRC 技术在现代卡车运输营运中的应用。

美国互联卡车市场占85%的市场份额,预计2024年市场规模将达123亿美元。美国市场受益于先进互联繫统的早期应用、广泛的远端资讯处理基础设施以及全球卡车製造商的积极参与。原始设备製造商(OEM)已整合工厂预装的数位互联平台,支援即时监控、远端诊断和效能最佳化,从而推动了市场快速渗透。此外,对车队效率日益增长的需求、日益严格的安全法规以及主要远端资讯处理服务提供者的存在,都在加速区域车队的技术部署。

全球互联卡车市场的主要参与者包括Trimble、Continental、戴姆勒卡车、比亚迪、塔塔汽车、PACCAR、MAN商用车、斯堪尼亚、Geotab和沃尔沃。这些领导企业正在实施多项策略以巩固其市场地位。许多企业致力于开发先进的互联生态系统,将硬体、软体和远端资讯处理技术结合,以提供整合的车队智慧。他们正积极寻求与物流供应商和原始设备製造商(OEM)进行策略合作,以拓展产品组合併确保大规模部署。此外,各企业在人工智慧和数据驱动分析领域投入巨资,以提升预测性维护、驾驶员安全和能源优化水准。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 车队管理效率的需求日益增长

- 5G与物联网技术的融合

- 政府关于安全和排放的法规

- 基于云端的远端资讯处理平台日益普及

- 对预测性维护的需求日益增长

- 产业陷阱与挑战

- 较高的初始实施和维护成本

- 对资料安全和隐私的担忧

- 市场机会

- 自动驾驶和半自动驾驶卡车的扩张

- 边缘运算在即时分析中的兴起

- 提高商用车的电气化程度

- 新兴市场采用率不断上升

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利分析

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 成本細項分析

- 永续性和环境影响分析

- 生命週期评估与环境建模

- 永续设计与最佳化

- 环境合规与报告

- 绿色科技与创新

- 商业案例及投资报酬率分析

- 总拥有成本框架

- 投资报酬率计算方法

- 实施时间表和里程碑

- 风险评估与缓解策略

- 绩效基准化分析与关键绩效指标

- 营运效率指标

- 安全与合规指标

- 财务绩效基准

- 驾驶员绩效评分系统

- 业界标准与协议

- SAE J1939 通讯标准

- TMC推荐做法

- 互通性和资料交换协议

- 网路安全和功能安全标准

- 实施最佳实践

- 部署策略与方法

- 变革管理与驾驶员培训

- 数据整合和分析设置

- 维护与支援优化

- 供应商选择与评估框架

- 技术评价标准

- 整合能力评估

- 可扩展性和麵向未来的考量

- 支援和服务等级要求

- 未来展望与技术路线图

- 技术演进时间轴

- 自动驾驶卡车集成

- 电动卡车互联

- 数据货币化策略

- 监理演变的影响

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 硬体

- 车载资讯控制单元(TCUS)

- 车载诊断(OBD)设备

- 通讯模组(蜂窝网路、Wi-Fi、蓝牙)

- 感测器和资料采集设备

- GPS/GNSS定位系统

- 其他的

- 软体

- 车队管理软体平台

- 行动应用程式和驱动程式接口

- 分析与商业智慧工具

- 整合和 API 管理软体

- 网路安全与资料保护软体

- 其他的

- 服务

- 安装与整合服务

- 数据分析与咨询服务

- 维护和技术支援

- 培训与变革管理服务

- 託管服务和外包

- 其他的

第六章:市场估算与预测:以连结方式划分,2021-2034年

- 主要趋势

- 车路通讯(V2I)

- 交通号誌一体化

- 智慧公路系统

- 收费和支付系统

- 称重站通信

- 停车及装卸区管理

- 车联网(V2C)通信

- 车队管理平台

- 远端诊断与监控

- 无线更新和配置

- 数据分析与商业智能

- 监理合规报告

- 车对车(V2V)通信

- 排队和车队行动

- 防碰撞系统

- 交通流量优化

- 紧急车辆通讯

- 协同自适应巡航控制

- 其他的

第七章:市场估算与预测:依区间划分,2021-2034年

- 主要趋势

- 专用短程通讯(DSRC)

- 远端

第八章:市场估算与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 轻型商用车(LCV)

- 1-2类车辆

- 皮卡车和货车

- 小型送货车辆

- 服务和多用途车辆

- 城市最后一公里应用

- 中型商用车(MCV)

- 3-5级车辆

- 厢型车和小型货车

- 餐饮服务车、饮料车

- 公用事业和市政车辆

- 区域分销应用

- 冷藏运送(冷藏)单元

- 重型商用车辆(HCV)

- 6-8级车辆

- 长途牵引车与拖车

- 重型卡车和拖车

- 工程和专用车辆

- 专用重型设备

第九章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 车队管理

- 安全与合规

- 远端诊断和维护

- 资讯娱乐与互联

- 其他的

第十章:市场估价与预测:依销售管道划分,2021-2034年

- 主要趋势

- 原始设备製造商

- 售后市场

第十一章:市场估计与预测:按地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- 全球参与者

- BYD Company

- Daimler Truck

- Iveco

- MAN Truck & Bus

- Navistar International

- PACCAR

- Scania

- Tata Motors

- Tesla

- Volvo

- Telematics Providers

- Fleet Complete

- Geotab

- MiX Telematics

- Omnitracs

- Platform Science

- Samsara Networks

- Teletrac Navman

- Trimble

- Verizon Connect

- Zonar Systems

- ADAS & Component Suppliers

- Aptiv

- Autoliv

- Continental

- DENSO

- Knorr-Bremse

- Magna International

- Mobileye

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- Connectivity & Hardware

- HARMAN International

- Murata Manufacturing

- NXP Semiconductors

- Qualcomm Technologies

- Sierra Wireless

- TE Connectivity

The Global Connected Trucks Market was valued at USD 34.8 billion in 2024 and is estimated to grow at a CAGR of 15.7% to reach USD 149.5 billion by 2034.

The growing demand for connected truck technologies is reshaping logistics and long-haul transportation networks worldwide. Advanced telematics, predictive fleet analytics, and in-cabin connectivity are transforming the way operators monitor routes, forecast delivery times, optimize loads, and minimize idle or empty trips. The use of digital-twin simulations enables fleet managers and OEMs to test operational models virtually, leading to cost reduction, enhanced safety, and improved delivery reliability. As the industry transitions toward electric and low-emission fleets, connected truck platforms are being utilized to manage energy distribution, schedule charging, and optimize range efficiency. Integration of smart charging and vehicle-to-grid communication systems ensures balanced energy usage and reduced grid strain. Furthermore, in mixed fleet operations, connected systems enable dynamic load balancing and route optimization to preserve battery life. The rapid integration of advanced driver assistance technologies such as automated braking, lane keeping, and truck platooning further underscores the importance of reliable, low-latency connectivity. OEMs and fleet operators are increasingly investing in sensor fusion and cloud analytics to turn real-time data into actionable safety and compliance insights.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.8 Billion |

| Forecast Value | $149.5 Billion |

| CAGR | 15.7% |

The hardware segment held a 44% share in 2024 and is projected to grow at a CAGR of 13.9% through 2034. Hardware continues to lead the market as it forms the essential framework that enables connectivity, communication, and telematics integration. Key components, including telematics control units (TCUs), GPS/GNSS devices, sensors, and wireless communication modules, serve as the backbone for collecting and transmitting real-time operational data. These systems support seamless interaction between vehicles, cloud platforms, and fleet management networks, forming the physical layer that powers digital transport ecosystems.

The dedicated short-range communication (DSRC) segment accounted for a 68% share in 2024 and is projected to grow at a CAGR of 15.1% from 2025 to 2034. DSRC technology remains the preferred communication method for connected trucks due to its robust performance and low latency, which are crucial for real-time vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication. This enables instantaneous data exchange for applications that enhance safety, such as collision detection, lane-changing alerts, and emergency response systems. Its proven reliability and regulatory alignment continue to strengthen its adoption in modern trucking operations.

United States Connected Trucks Market held an 85% share, generating USD 12.3 billion in 2024. The U.S. market benefits from early adoption of advanced connectivity systems, extensive telematics infrastructure, and strong participation from global truck manufacturers. OEMs have integrated factory-installed digital connectivity platforms that support real-time monitoring, remote diagnostics, and performance optimization, driving rapid market penetration. Additionally, growing demand for fleet efficiency, stringent safety regulations, and the presence of major telematics providers are accelerating technology deployment across regional fleets.

Key companies operating in the Global Connected Trucks Market include Trimble, Continental, Daimler Truck, BYD Company, Tata Motors, PACCAR, MAN Truck & Bus, Scania, Geotab, and Volvo. Leading players in the Connected Trucks Market are implementing multiple strategies to strengthen their market presence. Many are focusing on developing advanced connectivity ecosystems combining hardware, software, and telematics to deliver integrated fleet intelligence. Strategic collaborations with logistics providers and OEMs are being pursued to expand product portfolios and ensure large-scale deployment. Companies are also investing heavily in AI and data-driven analytics to enhance predictive maintenance, driver safety, and energy optimization.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technology

- 2.2.4 Range

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.2.7 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for fleet management efficiency

- 3.2.1.2 Integration of 5G and IoT technologies

- 3.2.1.3 Government regulations on safety and emissions

- 3.2.1.4 Increasing adoption of cloud-based telematics platforms

- 3.2.1.5 Growing demand for predictive maintenance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation and maintenance costs

- 3.2.2.2 Concerns over data security and privacy

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of autonomous and semi-autonomous trucks

- 3.2.3.2 Emergence of edge computing for real-time analytics

- 3.2.3.3 Increasing electrification of commercial vehicles

- 3.2.3.4 Rising adoption in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Lifecycle assessment and environmental modeling

- 3.12.2 Sustainable design and optimization

- 3.12.3 Environmental compliance and reporting

- 3.12.4 Green technology and innovation

- 3.13 Business Case & ROI Analysis

- 3.13.1 Total cost of ownership framework

- 3.13.2 ROI calculation methodologies

- 3.13.3 Implementation timeline & milestones

- 3.13.4 Risk assessment & mitigation strategies

- 3.14 Performance Benchmarking & KPIs

- 3.14.1 Operational efficiency metrics

- 3.14.2 Safety & compliance indicators

- 3.14.3 Financial performance benchmarks

- 3.14.4 Driver performance scoring systems

- 3.15 Industry Standards & Protocols

- 3.15.1 SAE J1939 communication standards

- 3.15.2 TMC recommended practices

- 3.15.3 Interoperability & data exchange protocols

- 3.15.4 Cybersecurity & functional safety standards

- 3.16 Implementation Best Practices

- 3.16.1 Deployment strategies & methodologies

- 3.16.2 Change management & driver training

- 3.16.3 Data integration & analytics setup

- 3.16.4 Maintenance & support optimization

- 3.17 Vendor Selection & Evaluation Framework

- 3.17.1 Technology evaluation criteria

- 3.17.2 Integration capability assessment

- 3.17.3 Scalability & future-proofing considerations

- 3.17.4 Support & service level requirement

- 3.18 Future outlook & technology roadmap

- 3.18.1 Technology evolution timeline

- 3.18.2 Autonomous trucking integration

- 3.18.3 Electric truck connectivity

- 3.18.4 Data monetization strategies

- 3.18.5 Regulatory evolution impact

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Telematics control units (TCUS)

- 5.2.2 On-board diagnostics (OBD) devices

- 5.2.3 Communication modules (cellular, wi-fi, Bluetooth)

- 5.2.4 Sensors & data collection devices

- 5.2.5 GPS/GNSS positioning systems

- 5.2.6 Others

- 5.3 Software

- 5.3.1 Fleet management software platforms

- 5.3.2 Mobile applications & driver interfaces

- 5.3.3 Analytics & business intelligence tools

- 5.3.4 Integration & API management software

- 5.3.5 Cybersecurity & data protection software

- 5.3.6 Others

- 5.4 Services

- 5.4.1 Installation & integration services

- 5.4.2 Data analytics & consulting services

- 5.4.3 Maintenance & technical support

- 5.4.4 Training & change management services

- 5.4.5 Managed services & outsourcing

- 5.4.6 Others

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Vehicle-to-Infrastructure (V2I) Communication

- 6.2.1 Traffic signal integration

- 6.2.2 Smart highway systems

- 6.2.3 Toll collection & payment systems

- 6.2.4 Weigh station communication

- 6.2.5 Parking & loading zone management

- 6.3 Vehicle-to-Cloud (V2C) Communication

- 6.3.1 Fleet management platforms

- 6.3.2 Remote diagnostics & monitoring

- 6.3.3 Over-the-air updates & configuration

- 6.3.4 Data analytics & business intelligence

- 6.3.5 Regulatory compliance reporting

- 6.4 Vehicle-to-Vehicle (V2V) Communication

- 6.4.1 Platooning & convoy operations

- 6.4.2 Collision avoidance systems

- 6.4.3 Traffic flow optimization

- 6.4.4 Emergency vehicle communication

- 6.4.5 Cooperative adaptive cruise control

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Range, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Dedicated short range communication (DSRC)

- 7.3 Long range

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Light Commercial Vehicles (LCV)

- 8.2.1 Class 1-2 vehicles

- 8.2.2 Pickup trucks & cargo vans

- 8.2.3 Small delivery vehicles

- 8.2.4 Service & utility vehicles

- 8.2.5 Urban last-mile applications

- 8.3 Medium Commercial Vehicles (MCV)

- 8.3.1 Class 3-5 vehicles

- 8.3.2 Box trucks & step vans

- 8.3.3 Food service & beverage trucks

- 8.3.4 Utility & municipal vehicles

- 8.3.5 Regional distribution applications

- 8.3.6 Refrigerated transport (reefer) units

- 8.4 Heavy Commercial Vehicles (HCV)

- 8.4.1 Class 6-8 vehicles

- 8.4.2 Long-haul tractors & semi-trailers

- 8.4.3 Heavy duty trucks & trailers

- 8.4.4 Construction & vocational vehicles

- 8.4.5 Specialized heavy equipment

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Fleet management

- 9.3 Safety & compliance

- 9.4 Remote diagnostics & maintenance

- 9.5 Infotainment & connectivity

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEMs

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 BYD Company

- 12.1.2 Daimler Truck

- 12.1.3 Iveco

- 12.1.4 MAN Truck & Bus

- 12.1.5 Navistar International

- 12.1.6 PACCAR

- 12.1.7 Scania

- 12.1.8 Tata Motors

- 12.1.9 Tesla

- 12.1.10 Volvo

- 12.2 Telematics Providers

- 12.2.1 Fleet Complete

- 12.2.2 Geotab

- 12.2.3 MiX Telematics

- 12.2.4 Omnitracs

- 12.2.5 Platform Science

- 12.2.6 Samsara Networks

- 12.2.7 Teletrac Navman

- 12.2.8 Trimble

- 12.2.9 Verizon Connect

- 12.2.10 Zonar Systems

- 12.3 ADAS & Component Suppliers

- 12.3.1 Aptiv

- 12.3.2 Autoliv

- 12.3.3 Continental

- 12.3.4 DENSO

- 12.3.5 Knorr-Bremse

- 12.3.6 Magna International

- 12.3.7 Mobileye

- 12.3.8 Robert Bosch

- 12.3.9 Valeo

- 12.3.10 ZF Friedrichshafen

- 12.4 Connectivity & Hardware

- 12.4.1 HARMAN International

- 12.4.2 Murata Manufacturing

- 12.4.3 NXP Semiconductors

- 12.4.4 Qualcomm Technologies

- 12.4.5 Sierra Wireless

- 12.4.6 TE Connectivity

互联卡车市场规模、份额和成长分析(按通讯技术、通讯范围、车辆类型、最终用途产业和地区划分)-2026-2033年产业预测

互联卡车市场规模、份额和成长分析(按通讯技术、通讯范围、车辆类型、最终用途产业和地区划分)-2026-2033年产业预测 2024-2029 年全球连网型卡车网路安全的成长机会

2024-2029 年全球连网型卡车网路安全的成长机会 连网型卡车:市场占有率分析、行业趋势和统计、成长预测(2024-2029)

连网型卡车:市场占有率分析、行业趋势和统计、成长预测(2024-2029)