|

市场调查报告书

商品编码

1876806

再生热塑性塑胶市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Recycled Thermoplastic Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

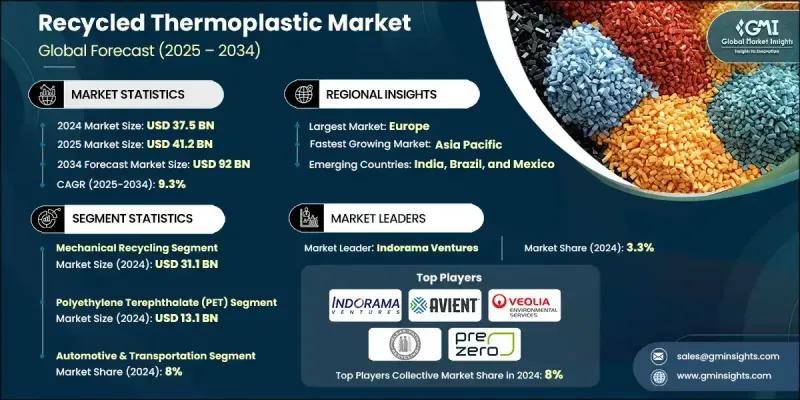

2024 年全球再生热塑性塑胶市场价值为 375 亿美元,预计到 2034 年将以 9.3% 的复合年增长率成长至 920 亿美元。

市场正迅速采用先进的回收技术,例如化学解聚、酵素法回收、等离子体处理和微波辅助法。这些技术能够将混合、受污染和多层塑胶转化为符合原生材料标准的高品质再生聚合物。循环经济原则的日益普及、消费者意识的增强以及政府强制规定最低再生材料含量和限制一次性塑胶使用的强有力政策,都在推动市场需求。闭环系统和回收基础设施投资的增加,进一步提高了再生热塑性塑胶的供应量。汽车、包装和电子产业是主要的终端用户,他们利用这些材料进行永续製造。预计未来十年,对生态高效生产和高价值应用的日益重视将使市场保持持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 375亿美元 |

| 预测值 | 920亿美元 |

| 复合年增长率 | 9.3% |

先进和混合回收技术领域预计将以复合年增长率成长。 2024 年全球再生热塑性塑胶市场价值为 375 亿美元,预计到 2034 年将以 9.3% 的复合年增长率成长至 920 亿美元。

市场正迅速采用先进的回收技术,例如化学解聚、酵素法回收、等离子体处理和微波辅助法。这些技术能够将混合、受污染和多层塑胶转化为符合原生材料标准的高品质再生聚合物。循环经济原则的日益普及、消费者意识的增强以及政府强制规定最低再生材料含量和限制一次性塑胶使用的强有力政策,都在推动市场需求。闭环系统和回收基础设施投资的增加,进一步提高了再生热塑性塑胶的供应量。汽车、包装和电子产业是主要的终端用户,他们利用这些材料进行永续製造。预计未来十年,对生态高效生产和高价值应用的日益重视将使市场保持持续成长。

预计到 2034 年,先进和混合回收技术领域的复合年增长率将达到 9.8%。这些方法可以回收复杂且难以处理的塑胶废料,同时最大限度地减少碳足迹,生产适用于高端应用的高性能聚合物。

2024年,聚对苯二甲酸乙二醇酯(PET)市场规模达131亿美元,主要得益于其在饮料瓶、包装和再生PET(rPET)纤维领域的广泛应用。由于PET具有高可回收性和多功能性,其回收利用持续成长,尤其是在食品级和纺织品应用领域。

2024年,美国再生热塑性塑胶市场规模预计将达到94亿美元,这得益于先进的回收基础设施以及分类和收集流程的改进。美国和加拿大都在大力投资机械和化学回收,以提高原料回收率和材料品质。包装、汽车和电子产业的需求尤其显着,同时,闭环系统和循环经济措施也日益受到重视。

全球再生热塑性塑胶市场的主要参与者包括PreZero Polymers AG、威立雅环境服务公司(Veolia Environmental Services)、伊士曼化学公司(Eastman Chemical Company)、KW Plastics Manufacturing、Loop Industries Inc.、Republic Services Inc.、Carubios SA、利安德巴塞尔德公司(Lyon Basul Holdings. Inc.、苏伊士集团(SUEZ Recycling & Recovery)、Avient Corporation、Clear Path Recycling和Indorama Ventures Public Company Limited。这些企业正采取多种策略来提升市场地位并扩大业务范围。这些策略包括投资先进的化学和机械回收技术以提高聚合物品质、扩大加工能力以及与原料供应商建立合作关係以确保稳定的原料供应。许多企业正致力于开发闭环系统和高性能再生聚合物,以满足高阶终端应用的需求。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲 (MEA)

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 透过加工方法

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依加工方式划分,2021-2034年

- 主要趋势

- 机械回收

- 收集和分类系统

- 洗涤和清洁过程

- 粉碎和尺寸缩减

- 熔化和造粒

- 化学回收

- 热解技术

- 解聚过程

- 气化方法

- 溶剂分解技术

- 催化裂解

- 酵素解聚

- 先进技术

- 生物基回收方法

- 基于等离子体的技术

- 微波增强处理

- 其他新兴技术

第六章:市场估算与预测:依产品类型划分,2021-2034年

- 主要趋势

- 宠物

- 高密度聚乙烯

- 低密度聚乙烯

- PP

- PS

- 其他的

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 包装

- 食品和饮料容器

- 非食品包装

- 柔性包装和薄膜

- 瓶盖和封口

- 汽车与运输

- 内部组件

- 引擎盖下应用

- 外板和装饰条

- 电池外壳和电动车组件

- 建筑施工

- 管道及配件

- 绝缘材料

- 屋顶和露台

- 视窗轮廓

- 电学

- 设备外壳

- 连接器和组件

- 电缆绝缘

- 消费品和家具

- 家居用品

- 户外家具

- 玩具和体育用品

- 农业与园艺

- 温室电影

- 灌溉系统

- 花盆和容器

- 纺织品和服装

- 合成纤维

- 地毯和地板

- 非织物

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Avient Corporation

- Biffa plc

- Carbios SA

- Clear Path Recycling

- Eastman Chemical Company

- Indorama Ventures Public Company Limited

- KW Plastics Manufacturing

- Loop Industries Inc.

- Lyondell Basell

- Plastipak Holdings Inc.

- PreZero Polymers AG

- Remondis Recycling GmbH

- Republic Services Inc.

- SUEZ Recycling & Recovery

- Veolia Environmental Services

The Global Recycled Thermoplastic Market was valued at USD 37.5 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 92 billion by 2034.

The market is witnessing rapid adoption of advanced recycling technologies such as chemical depolymerization, enzymatic recycling, plasma processing, and microwave-assisted methods. These techniques enable the transformation of mixed, contaminated, and multilayer plastics into high-quality recycled polymers that meet the standards of virgin materials. Rising adoption of circular economy principles, growing consumer awareness, and strong government policies mandating minimum recycled content and restricting single-use plastics are fueling demand. Closed-loop systems and increased investments in recycling infrastructure are further enhancing the availability of recycled thermoplastics. The automotive, packaging, and electronics industries are among the primary end-users, leveraging these materials for sustainable manufacturing. Rising emphasis on eco-efficient production and high-value applications is expected to sustain consistent growth in the market over the coming decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.5 Billion |

| Forecast Value | $92 Billion |

| CAGR | 9.3% |

The advanced and hybrid recycling technologies segment is projected to grow at a CAGR The Global Recycled Thermoplastic Market was valued at USD 37.5 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 92 billion by 2034.

The market is witnessing rapid adoption of advanced recycling technologies such as chemical depolymerization, enzymatic recycling, plasma processing, and microwave-assisted methods. These techniques enable the transformation of mixed, contaminated, and multilayer plastics into high-quality recycled polymers that meet the standards of virgin materials. Rising adoption of circular economy principles, growing consumer awareness, and strong government policies mandating minimum recycled content and restricting single-use plastics are fueling demand. Closed-loop systems and increased investments in recycling infrastructure are further enhancing the availability of recycled thermoplastics. The automotive, packaging, and electronics industries are among the primary end-users, leveraging these materials for sustainable manufacturing. Rising emphasis on eco-efficient production and high-value applications is expected to sustain consistent growth in the market over the coming decade.

The advanced and hybrid recycling technologies segment is projected to grow at a CAGR of 9.8% through 2034. These methods can recycle complex and hard-to-process plastic waste streams while minimizing carbon footprint, producing high-performance polymers suitable for premium applications.

In 2024, the polyethylene Terephthalate (PET) accounted for USD 13.1 billion, driven by its use in beverage bottles, packaging, and recycled PET (rPET) fibers. PET recycling continues to expand, particularly for food-grade and textile applications, due to its high recyclability and versatility.

U.S. Recycled Thermoplastic Market reached USD 9.4 billion in 2024, supported by advanced recycling infrastructure and improved sorting and collection processes. Both the U.S. and Canada are investing heavily in mechanical and chemical recycling to enhance feedstock recovery and material quality. Key demand stems from the packaging, automotive, and electronics sectors, with increasing focus on closed-loop systems and circular economy initiatives.

Leading players in the Global Recycled Thermoplastic Market include PreZero Polymers AG, Veolia Environmental Services, Eastman Chemical Company, KW Plastics Manufacturing, Loop Industries Inc., Republic Services Inc., Carbios SA, Lyondell Basell, Biffa plc, Remondis Recycling GmbH, Plastipak Holdings Inc., SUEZ Recycling & Recovery, Avient Corporation, Clear Path Recycling, and Indorama Ventures Public Company Limited. Companies in the Recycled Thermoplastic Market are employing multiple strategies to enhance their market position and expand their reach. These include investing in advanced chemical and mechanical recycling technologies to improve polymer quality, expanding processing capacity, and establishing partnerships with feedstock suppliers to secure consistent input. Many players are focusing on developing closed-loop systems and high-performance recycled polymers to cater to premium end-use applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Processing method

- 2.2.3 Product type

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa (MEA)

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By processing method

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Processing Method, 2021-2034 (USD Billion & Tons)

- 5.1 Key trends

- 5.2 Mechanical recycling

- 5.2.1 Collection & sorting systems

- 5.2.2 Washing & cleaning processes

- 5.2.3 Shredding & size reduction

- 5.2.4 Melting & pelletizing

- 5.3 Chemical recycling

- 5.3.1 Pyrolysis technologies

- 5.3.2 Depolymerization processes

- 5.3.3 Gasification methods

- 5.3.4 Solvolysis techniques

- 5.3.5 Catalytic cracking

- 5.3.6 Enzymatic depolymerization

- 5.4 Advanced technologies

- 5.4.1 Bio based recycling methods

- 5.4.2 Plasma based technologies

- 5.4.3 Microwave enhanced processing

- 5.4.4 Other emerging technologies

Chapter 6 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion & Tons)

- 6.1 Key trends

- 6.2 PET

- 6.3 HDPE

- 6.4 LDPE

- 6.5 PP

- 6.6 PS

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion & Tons)

- 7.1 Key trends

- 7.2 Packaging

- 7.2.1 Food & beverage containers

- 7.2.2 Non-food packaging

- 7.2.3 Flexible packaging & films

- 7.2.4 Caps & closures

- 7.3 Automotive & transportation

- 7.3.1 Interior components

- 7.3.2 Under-hood applications

- 7.3.3 Exterior panels & trim

- 7.3.4 Battery housing & EV components

- 7.4 Building & construction

- 7.4.1 Pipes & fittings

- 7.4.2 Insulation materials

- 7.4.3 Roofing & decking

- 7.4.4 Window profiles

- 7.5 Electronics & electrical

- 7.5.1 Device housings

- 7.5.2 Connectors & components

- 7.5.3 Cable insulation

- 7.6 Consumer goods & furniture

- 7.6.1 Household items

- 7.6.2 Outdoor furniture

- 7.6.3 Toys & sporting goods

- 7.7 Agriculture & horticulture

- 7.7.1 Greenhouse films

- 7.7.2 Irrigation systems

- 7.7.3 Plant pots & containers

- 7.8 Textiles & apparel

- 7.8.1 Synthetic fibers

- 7.8.2 Carpeting & flooring

- 7.8.3 Non-woven fabrics

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion & Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Avient Corporation

- 9.2 Biffa plc

- 9.3 Carbios SA

- 9.4 Clear Path Recycling

- 9.5 Eastman Chemical Company

- 9.6 Indorama Ventures Public Company Limited

- 9.7 KW Plastics Manufacturing

- 9.8 Loop Industries Inc.

- 9.9 Lyondell Basell

- 9.10 Plastipak Holdings Inc.

- 9.11 PreZero Polymers AG

- 9.12 Remondis Recycling GmbH

- 9.13 Republic Services Inc.

- 9.14 SUEZ Recycling & Recovery

- 9.15 Veolia Environmental Services

2026年全球热塑性管道市场报告

2026年全球热塑性管道市场报告 热塑性塑胶管材市场-全球产业规模、份额、趋势、机会、预测:依聚合物类型、应用、最终用户、地区和竞争格局划分,2021-2031年高温热塑性树脂市场-全球产业规模、份额、趋势、机会及预测(依树脂类型、范围、终端用户产业、区域及竞争格局划分,2021-2031年)

热塑性塑胶管材市场-全球产业规模、份额、趋势、机会、预测:依聚合物类型、应用、最终用户、地区和竞争格局划分,2021-2031年高温热塑性树脂市场-全球产业规模、份额、趋势、机会及预测(依树脂类型、范围、终端用户产业、区域及竞争格局划分,2021-2031年) 热塑性层压板市场:按材料类型、工艺、厚度、应用和最终用途行业划分,全球预测(2026-2032年)热塑性淀粉合金市场按形态、製造流程、混合类型和应用划分,全球预测(2026-2032年)高性能热塑性聚氨酯弹性体市场依产品形式、原料类型、加工技术、硬度等级、终端应用产业及通路划分-2026-2032年全球预测

热塑性层压板市场:按材料类型、工艺、厚度、应用和最终用途行业划分,全球预测(2026-2032年)热塑性淀粉合金市场按形态、製造流程、混合类型和应用划分,全球预测(2026-2032年)高性能热塑性聚氨酯弹性体市场依产品形式、原料类型、加工技术、硬度等级、终端应用产业及通路划分-2026-2032年全球预测 热塑性淀粉(TPS):市占率分析、产业趋势与统计、成长预测(2026-2031)

热塑性淀粉(TPS):市占率分析、产业趋势与统计、成长预测(2026-2031) 热塑性管道市场规模、份额和成长分析(按管道类型、聚合物类型、安装位置和地区划分)-2026-2033年产业预测

热塑性管道市场规模、份额和成长分析(按管道类型、聚合物类型、安装位置和地区划分)-2026-2033年产业预测 高性能热塑性塑胶市场规模、份额及成长分析(依产品类型、应用、製造流程、最终用途及地区划分)-2026-2033年产业预测

高性能热塑性塑胶市场规模、份额及成长分析(依产品类型、应用、製造流程、最终用途及地区划分)-2026-2033年产业预测 TCP和RTP管道:全球市场份额和排名、总收入和需求预测(2025-2031年)

TCP和RTP管道:全球市场份额和排名、总收入和需求预测(2025-2031年)