|

市场调查报告书

商品编码

1876821

动物饲料蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Animal Feed Protein Hydrolysate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

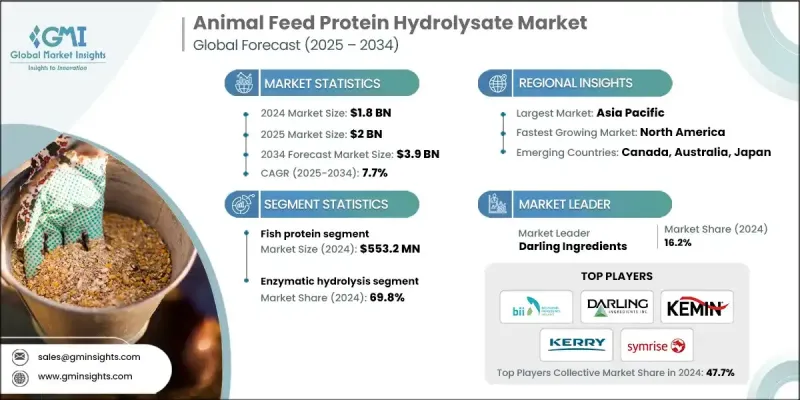

2024 年全球动物饲料蛋白水解物市场价值为 18 亿美元,预计到 2034 年将以 7.7% 的复合年增长率增长至 39 亿美元。

畜牧、水产养殖和家禽饲料中对高品质蛋白质补充剂的需求日益增长,以提升生长性能、免疫力和整体健康水平,这推动了市场扩张。动物饲料蛋白水解物源自动物性蛋白质的酵素解或化学分解,以其优异的消化率和生物活性而闻名。随着畜牧和水产养殖业不断关注提高生产性能和增强抗病能力,饲料生产商越来越多地将这些水解物用作功能性添加剂。这种朝向营养更丰富、更注重健康的动物营养模式的转变,正在塑造饲料配方的未来。先进酶水解技术的应用进一步巩固了市场,提高了生产效率,确保了胜肽结构的稳定性,并降低了生产成本。这些创新使得生产具有特定功能优势的水解物成为可能,从而促进动物健康和生长。对可持续、营养丰富且能提升生产性能的饲料原料的持续追求,将持续推动全球对动物饲料蛋白水解物的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 18亿美元 |

| 预测值 | 39亿美元 |

| 复合年增长率 | 7.7% |

2024年,鱼蛋白创造了5.532亿美元的产值。其高营养价值、丰富的氨基酸组成和大量的生物活性化合物使其成为促进动物最佳生长和健康的理想原料。海产产业丰富的鱼类副产品为生产商提供了可持续且经济高效的原料来源。此外,鱼源营养物质具有极佳的消化率和适口性,使其成为寻求高效环保解决方案的饲料生产商的首选。

2024年,酵素水解过程占据了69.8%的市场份额,并继续保持其作为最高效、最环保的生产方法的地位。此製程能够精确控制水解过程,从而开发出具有特定生物活性的胜肽,同时保持其营养价值。酶水解製程温和的操作条件确保了产品的稳定性和均匀性。此外,与化学製程相比,酵素水解是更环保的选择,符合业界对永续和高性能动物营养成分日益增长的需求。

预计2025年至2034年间,北美动物饲料蛋白水解物市场将以7.8%的复合年增长率成长。该地区市场成长的主要驱动力是人们日益关注动物健康、肠道健康和免疫力。随着动物饲料中对永续和天然成分的需求不断增长,美国饲料生产商正积极采用水解物配方。酵素法製程的进步提高了水解物的消化率和稳定性,使生产商能够生产出高品质、环保的产品。这与北美地区有机和环保饲料生产的持续趋势相契合。

全球动物饲料蛋白水解物市场的主要参与者包括 Symrise AG、Kerry Group、BioMarine Ingredients Ireland、Kemin Industries、SAMPI、Darling Ingredients、Titan Biotech、Copalis、Janatha Fish Meal、Empro Europe 和 Proliver。这些关键企业正致力于透过多种策略来巩固其全球市场地位。许多企业正在投资先进的水解技术,以提高产量、胜肽功能和营养功效。它们积极寻求策略合作和併购,以拓展产品组合和区域影响力。此外,各公司也强调永续采购和循环经济实践,以有效利用鱼类和肉类副产品。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 对优质动物性蛋白质的需求不断增长

- 人们越来越关注动物健康和营养

- 功能性饲料添加剂的采用率不断提高

- 产业陷阱与挑战

- 高昂的生产成本

- 来自合成替代品的竞争

- 市场机会

- 新兴蛋白质来源开发

- 生物活性胜肽的应用

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 来源

- 未来市场趋势

- 专利格局

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国(註:仅提供重点国家的贸易统计)

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依来源划分,2021-2034年

- 主要趋势

- 鱼类蛋白

- 鲑鱼

- 鲔鱼

- 沙丁鱼和凤尾鱼

- 动物性蛋白质

- 家禽副产品

- 猪肉副产品

- 牛肉副产品

- 血液和血浆

- 植物蛋白

- 大豆

- 米

- 豌豆

- 其他的

- 牛奶

- 乳清

- 酪蛋白

- 牛奶加工副产品

- 其他的

第六章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 酵素水解

- 基于Alcalase的加工

- 基于Protamex的加工

- 其他的

- 酸水解

- 盐酸处理

- 硫酸加工

- 其他的

- 先进处理技术

- 其他的

第七章:市场估计与预测:依畜牧业划分,2021-2034年

- 主要趋势

- 家禽

- 肉鸡

- 层

- 土耳其

- 其他的

- 猪

- 小猪

- 种植者

- 终结者

- 反刍动物

- 牛

- 乳製品

- 小型反刍动物

- 水产养殖

- 鳍鱼

- 甲壳类动物

- 软体动物

- 伴侣动物

- 狗粮

- 猫粮

- 宠物特殊食品

- 其他牲畜

- 马科动物

- 珍稀动物和猎物

- 其他的

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- BioMarine Ingredients Ireland

- Copalis

- Darling Ingredients

- 欧洲安普罗

- Janatha Fish Meal

- Kemin Industries

- Kerry Group

- Proliver

- SAMPI

- Symrise AG

- Titan Biotech

The Global Animal Feed Protein Hydrolysate Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 3.9 billion by 2034.

The market expansion is influenced by the increasing need for high-quality protein supplements in livestock, aquaculture, and poultry feed to boost growth performance, immunity, and overall health. Animal feed protein hydrolysates are derived from the enzymatic or chemical breakdown of animal proteins and are known for their superior digestibility and bioactivity. As the livestock and aquaculture industries continue to focus on performance enhancement and disease resistance, feed manufacturers are increasingly turning to these hydrolysates as functional additives. This transition toward more nutrient-dense and health-focused animal nutrition is shaping the future of feed formulation. The adoption of advanced enzymatic hydrolysis technologies has further strengthened the market by improving production efficiency, ensuring consistency in peptide structure, and reducing manufacturing costs. These innovations have made it possible to produce hydrolysates with specific functional benefits, promoting better animal health and growth. The continuous drive toward sustainable, nutrient-rich, and performance-boosting feed ingredients will keep fueling demand for animal feed protein hydrolysates globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.9 Billion |

| CAGR | 7.7% |

Fish protein generated USD 553.2 million in 2024. Its strong nutritional value, high amino acid profile, and abundance of bioactive compounds make it an ideal ingredient for supporting optimal growth and health in animals. The seafood industry's extensive supply of fish by-products offers a sustainable and cost-effective raw material source for manufacturers. In addition, fish-derived nutrients exhibit excellent digestibility and palatability, making them a preferred choice among feed producers seeking efficient and eco-friendly solutions.

The enzymatic hydrolysis segment accounted for a 69.8% share in 2024, maintaining its position as the most efficient and environmentally sustainable production method. This process allows for precise control of hydrolysis, enabling the development of peptides with specific bioactive properties while preserving nutritional quality. The mild operational conditions of enzymatic hydrolysis ensure high product stability and uniformity. Moreover, it is a greener alternative compared to chemical processes, aligning with the industry's growing focus on sustainable and high-performance animal nutrition ingredients.

North America Animal Feed Protein Hydrolysate Market is projected to grow at a CAGR of 7.8% between 2025 and 2034. The region's market growth is driven by the increasing focus on animal wellness, gut health, and immunity. With a rising preference for sustainable and natural ingredients in animal feed, U.S. feed producers are actively adopting hydrolysate-based formulations. Advancements in enzymatic processes have enhanced digestibility and stability, allowing manufacturers to create high-quality, environmentally friendly products. This aligns with North America's ongoing trend toward organic and eco-conscious feed production.

Prominent players in the Global Animal Feed Protein Hydrolysate Market include Symrise AG, Kerry Group, BioMarine Ingredients Ireland, Kemin Industries, SAMPI, Darling Ingredients, Titan Biotech, Copalis, Janatha Fish Meal, Empro Europe, and Proliver. Key companies in the Animal Feed Protein Hydrolysate Market are focusing on multiple strategies to reinforce their global market position. Many are investing in advanced hydrolysis technologies to improve yield, peptide functionality, and nutritional efficacy. Strategic collaborations and mergers are being pursued to expand product portfolios and regional presence. Firms are also emphasizing sustainable sourcing and circular economy practices to utilize fish and meat by-products efficiently.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source trends

- 2.2.2 Technology trends

- 2.2.3 Livestock trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-quality animal protein

- 3.2.1.2 Growing focus on animal health & nutrition

- 3.2.1.3 Increasing adoption of functional feed additives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Competition from synthetic alternatives

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging protein sources development

- 3.2.3.2 Bioactive peptide applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries( Note: the trade statistics will be provided for key countries only)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fish protein

- 5.2.1 Salmon

- 5.2.2 Tuna

- 5.2.3 Sardine & anchovy

- 5.3 Animal protein

- 5.3.1 Poultry by-product

- 5.3.2 Pork by-product

- 5.3.3 Beef by-product

- 5.3.4 Blood & plasma

- 5.4 Plant protein

- 5.4.1 Soy

- 5.4.2 Rice

- 5.4.3 Pea

- 5.4.4 Others

- 5.5 Milk

- 5.5.1 Whey

- 5.5.2 Casein

- 5.5.3 Milk processing by-products

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Enzymatic hydrolysis

- 6.2.1 Alcalase-based processing

- 6.2.2 Protamex-based processing

- 6.2.3 Others

- 6.3 Acid hydrolysis

- 6.3.1 Hydrochloric acid processing

- 6.3.2 Sulfuric acid processing

- 6.3.3 Others

- 6.4 Advanced processing technologies

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Livestock, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Poultry

- 7.2.1 Broiler

- 7.2.2 Layer

- 7.2.3 Turkey

- 7.2.4 Others

- 7.3 Swine

- 7.3.1 Piglet

- 7.3.2 Grower

- 7.3.3 Finisher

- 7.4 Ruminant

- 7.4.1 Cattle

- 7.4.2 Dairy

- 7.4.3 Small ruminants

- 7.5 Aquaculture

- 7.5.1 Finfish

- 7.5.2 Crustacean

- 7.5.3 Mollusk

- 7.6 Companion animal

- 7.6.1 Dog food

- 7.6.2 Cat food

- 7.6.3 Specialty pet foods

- 7.7 Other livestock

- 7.7.1 Equine

- 7.7.2 Exotic & game animals

- 7.7.3 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BioMarine Ingredients Ireland

- 9.2 Copalis

- 9.3 Darling Ingredients

- 9.4 Empro Europe

- 9.5 Janatha Fish Meal

- 9.6 Kemin Industries

- 9.7 Kerry Group

- 9.8 Proliver

- 9.9 SAMPI

- 9.10 Symrise AG

- 9.11 Titan Biotech

2026-2034年全球动物饲料蛋白酶市场规模、份额、趋势和成长分析报告

2026-2034年全球动物饲料蛋白酶市场规模、份额、趋势和成长分析报告 微量元素肥料市场规模、份额和成长分析:按产品类型、应用方法、最终用户、配方类型和地区划分-2026-2033年产业预测

微量元素肥料市场规模、份额和成长分析:按产品类型、应用方法、最终用户、配方类型和地区划分-2026-2033年产业预测 动物饲料市场分析及预测(至2035年):类型、产品、形态、应用、技术、材料种类、最终使用者、功能、成分饲料市场分析及预测(至2035年):依类型、产品类型、应用、技术、成分、形态、最终用户微藻类製程划分2026-2034年全球动物饲料用蛋白质成分市场规模、份额、趋势及成长分析报告饲料蛋白市场-2026-2031年预测非基因改造饲料市场-2026-2031年预测

动物饲料市场分析及预测(至2035年):类型、产品、形态、应用、技术、材料种类、最终使用者、功能、成分饲料市场分析及预测(至2035年):依类型、产品类型、应用、技术、成分、形态、最终用户微藻类製程划分2026-2034年全球动物饲料用蛋白质成分市场规模、份额、趋势及成长分析报告饲料蛋白市场-2026-2031年预测非基因改造饲料市场-2026-2031年预测 动物饲料替代蛋白市场机会、成长要素、产业趋势分析及预测(2026年至2035年)动物饲料蛋白原料市场机会、成长要素、产业趋势分析及预测(2026年至2035年)

动物饲料替代蛋白市场机会、成长要素、产业趋势分析及预测(2026年至2035年)动物饲料蛋白原料市场机会、成长要素、产业趋势分析及预测(2026年至2035年) 全球动物饲料微量营养素市场规模、份额、行业分析报告(按形式、营养素类型、牲畜和地区)、展望和预测(2025-2032 年)

全球动物饲料微量营养素市场规模、份额、行业分析报告(按形式、营养素类型、牲畜和地区)、展望和预测(2025-2032 年)