|

市场调查报告书

商品编码

1822636

动物饲料蛋白市场机会、成长动力、产业趋势分析及2025-2034年预测Animal Feed Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

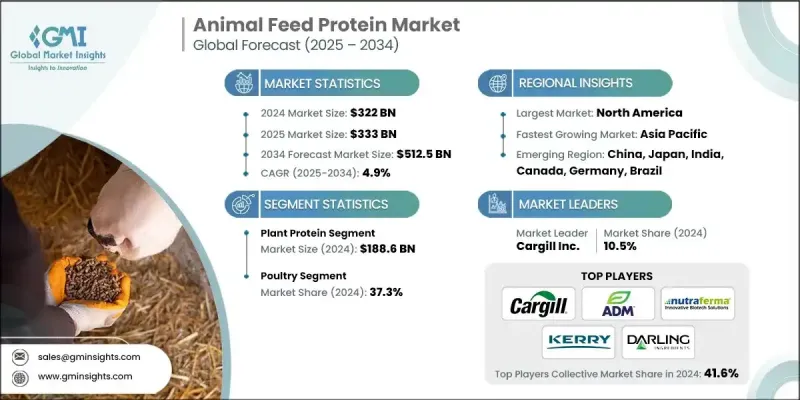

根据 Global Market Insights Inc. 发布的最新报告,2024 年全球动物饲料蛋白市场规模估计为 3,220 亿美元,预计将从 2025 年的 3,330 亿美元增长到 2034 年的 5,125 亿美元,复合年增长率为 4.9%。

随着全球人口成长和收入提高,尤其是在发展中国家,肉类和乳製品的需求不断增长。这推动了对高品质动物饲料蛋白的需求,以支持牲畜的健康生长和生产力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3220亿美元 |

| 预测值 | 5125亿美元 |

| 复合年增长率 | 4.9% |

植物性蛋白质的采用率不断上升

植物蛋白领域在2024年占据了显着的份额,这得益于其成本效益高、供应充足和可持续的采购。豆粕、菜籽油和豌豆蛋白等原料因其高营养价值和易于消化的特点,被广泛应用于多种牲畜。各公司正在投资非基因改造和有机植物蛋白的开发,以及旨在改善胺基酸组成和提高生物利用度的加工创新,以实现有针对性的动物健康效益。

家禽业将获得发展

2024年,家禽市场占据了可持续的份额,这得益于全球对鸡肉和鸡蛋的高需求,因为鸡肉和鸡蛋价格实惠且富含瘦肉蛋白。大规模商业化养殖和人均家禽消费量的增加推动了市场的成长。主要行业参与者正专注于客製化饲料配方,以提高饲料转换率并降低疾病风险。策略包括结合酶强化蛋白混合物和针对特定地区的营养计划,以满足肉鸡、蛋鸡和种鸡的独特需求。

区域洞察

北美将成为利润丰厚的地区

2024年,北美动物饲料蛋白市场收入可观,这得益于其成熟的畜牧业、高涨的肉类和乳製品消费需求以及先进的农业实践。在北美营运的公司正在采取前瞻性策略,包括与饲料厂合併、扩大生产设施以及对永续蛋白质替代品的研发投资。此外,精准营养和数位化饲料管理系统也受到重视,旨在提高动物生产性能并减少投入浪费。

动物饲料蛋白市场的主要参与者包括 Angel Yeast、Deep Branch Biotechnology、Archer Daniels Midland Company (ADM)、Ynsect、Nutraferma LLC、CHS Inc.、Unibio Group、Innovafeed、杜邦 (EI DuPont De Nemours and Company)、Darling Ingredients、Kerry Group、Carpill Inc.、La Nemours and Company)、Darling Ingredients、Kerry Group、Carpill Inc.、Lakmands, Biopat。

为了巩固市场地位,动物饲料蛋白产业的公司正在追求创新、合作和永续发展的结合。许多公司正在拓展替代蛋白来源,例如藻类和昆虫蛋白,以丰富产品组合併减少对传统原料的依赖。与畜牧农场和营养研究中心建立策略联盟,有助于根据实际需求客製化产品开发。此外,企业正在利用数位工具提供数据驱动的饲养解决方案,以最大限度地提高效率。如今,品牌推广工作也强调可追溯性和生态认证,以符合不断变化的消费者和监管期望。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)

(註:仅提供重点国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 多边环境协定

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品,2021-2034

- 主要趋势

- 植物蛋白

- 动物性蛋白质

- 替代蛋白质

第六章:市场估计与预测:依牲畜,2021-2034

- 主要趋势

- 家禽

- 猪

- 牛

- 水产养殖

- 宠物食品

- 马

第七章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第八章:公司简介

- Cargill Inc.

- Archer Daniels Midland Company (ADM)

- DuPont (EI DuPont De Nemours and Company)

- Kerry Group

- Nutraferma LLC

- Darling Ingredient

- Lallemand Inc.

- Angel Yeast

- Imcopa Food Ingredients BV

- CHS Inc.

- Crescent Biotech

- Deep Branch Biotechnology

- Unibio Group

- Innovafeed

- Ynsect

The global animal feed protein market was estimated at USD 322 billion in 2024 and is expected to grow from USD 333 billion in 2025 to USD 512.5 billion by 2034, at a CAGR of 4.9%, according to the latest report published by Global Market Insights Inc.

As global populations grow and incomes rise, especially in developing countries, the demand for meat and dairy products increases. This drives the need for high-quality animal feed protein to support healthy livestock growth and productivity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $322 Billion |

| Forecast Value | $512.5 Billion |

| CAGR | 4.9% |

Rising Adoption of Plant Protein

The plant protein segment held a notable share in 2024, driven by its cost-effectiveness, abundant availability, and sustainable sourcing. Ingredients like soybean meal, canola, and pea protein are widely used for their high nutritional value and ease of digestion across multiple livestock species. Companies are investing in non-GMO and organic plant-based protein development, as well as in processing innovations that improve amino acid profiles and enhance bioavailability for targeted animal health benefits.

Poultry to Gain Traction

The poultry segment held a sustainable share in 2024, supported by high global demand for chicken meat and eggs due to their affordability and lean protein content. The market growth is fueled by large-scale commercial farming operations and increasing per capita poultry consumption. Key industry players are focusing on tailored feed formulations that boost feed conversion ratios and reduce disease risks. Strategies include incorporating enzyme-enhanced protein blends and region-specific nutrition plans to meet the unique requirements of broilers, layers, and breeders.

Regional Insights

North America to Emerge as a Lucrative Region

North America animal feed protein market generated notable revenues in 2024, backed by a well-established livestock sector, high consumer demand for meat and dairy, and advanced agricultural practices. Companies operating in North America are adopting forward-looking strategies, including mergers with feed mills, expansion of production facilities, and R&D investments in sustainable protein alternatives. Emphasis is also being placed on precision nutrition and digital feed management systems to enhance animal performance and reduce input waste.

Major players in the animal feed protein market are Angel Yeast, Deep Branch Biotechnology, Archer Daniels Midland Company (ADM), Ynsect, Nutraferma LLC, CHS Inc., Unibio Group, Innovafeed, DuPont (E.I. DuPont De Nemours and Company), Darling Ingredients, Kerry Group, Cargill Inc., Lallemand Inc., Crescent Biotech, and Imcopa Food Ingredients B.V.

To strengthen their market presence, companies in the animal feed protein sector are pursuing a combination of innovation, partnerships, and sustainability. Many are expanding into alternative protein sources-like algae and insect protein-to diversify their offerings and reduce reliance on traditional raw materials. Strategic alliances with livestock farms and nutrition research centers help tailor product development to real-world needs. Additionally, players are leveraging digital tools to provide data-driven feeding solutions that maximize efficiency. Branding efforts now also emphasize traceability and eco-certifications to align with evolving consumer and regulatory expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Livestock

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trend

- 5.2 Plant protein

- 5.3 Animal protein

- 5.4 Alternative protein

Chapter 6 Market Estimates & Forecast, By Livestock, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Poultry

- 6.3 Swine

- 6.4 Cattle

- 6.5 Aquaculture

- 6.6 Petfood

- 6.7 Equine

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East & Africa

Chapter 8 Company Profiles

- 8.1 Cargill Inc.

- 8.2 Archer Daniels Midland Company (ADM)

- 8.3 DuPont (E.I. DuPont De Nemours and Company)

- 8.4 Kerry Group

- 8.5 Nutraferma LLC

- 8.6 Darling Ingredient

- 8.7 Lallemand Inc.

- 8.8 Angel Yeast

- 8.9 Imcopa Food Ingredients B.V.

- 8.10 CHS Inc.

- 8.11 Crescent Biotech

- 8.12 Deep Branch Biotechnology

- 8.13 Unibio Group

- 8.14 Innovafeed

- 8.15 Ynsect

微量元素肥料市场规模、份额和成长分析:按产品类型、应用方法、最终用户、配方类型和地区划分-2026-2033年产业预测

微量元素肥料市场规模、份额和成长分析:按产品类型、应用方法、最终用户、配方类型和地区划分-2026-2033年产业预测 动物饲料市场分析及预测(至2035年):类型、产品、形态、应用、技术、材料种类、最终使用者、功能、成分饲料市场分析及预测(至2035年):依类型、产品类型、应用、技术、成分、形态、最终用户微藻类製程划分

动物饲料市场分析及预测(至2035年):类型、产品、形态、应用、技术、材料种类、最终使用者、功能、成分饲料市场分析及预测(至2035年):依类型、产品类型、应用、技术、成分、形态、最终用户微藻类製程划分 2026-2034年全球动物饲料用蛋白质成分市场规模、份额、趋势及成长分析报告饲料蛋白市场-2026-2031年预测非基因改造饲料市场-2026-2031年预测

2026-2034年全球动物饲料用蛋白质成分市场规模、份额、趋势及成长分析报告饲料蛋白市场-2026-2031年预测非基因改造饲料市场-2026-2031年预测 动物饲料替代蛋白市场机会、成长要素、产业趋势分析及预测(2026年至2035年)动物饲料蛋白原料市场机会、成长要素、产业趋势分析及预测(2026年至2035年)动物饲料蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

动物饲料替代蛋白市场机会、成长要素、产业趋势分析及预测(2026年至2035年)动物饲料蛋白原料市场机会、成长要素、产业趋势分析及预测(2026年至2035年)动物饲料蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球动物饲料微量营养素市场规模、份额、行业分析报告(按形式、营养素类型、牲畜和地区)、展望和预测(2025-2032 年)

全球动物饲料微量营养素市场规模、份额、行业分析报告(按形式、营养素类型、牲畜和地区)、展望和预测(2025-2032 年)