|

市场调查报告书

商品编码

1876824

云端微服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Cloud Microservices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

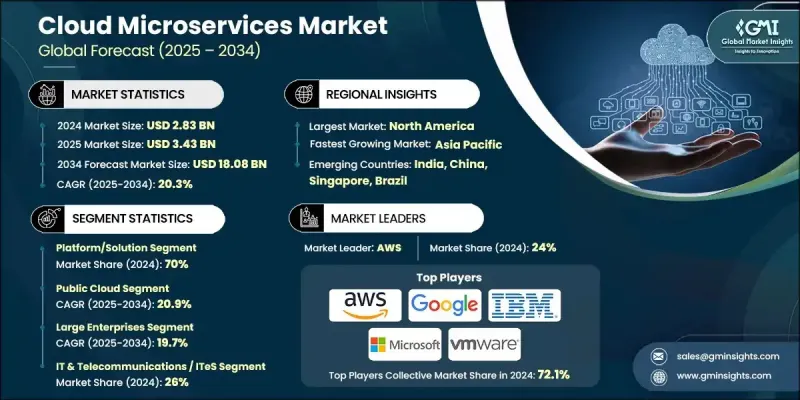

2024 年全球云端微服务市场价值为 28.3 亿美元,预计到 2034 年将以 20.3% 的复合年增长率成长至 180.8 亿美元。

企业应用程式从传统单体系统到现代云端原生架构的迁移日益增多,推动了微服务的快速发展。约 62.3% 的企业已采用微服务和容器化技术,以增强灵活性、简化应用程式开发并加速跨分散式环境的软体部署。微服务的模组化设计使开发团队能够更有效率地扩展服务和部署更新。然而,维运挑战依然存在;36% 的企业表示有整合难题,35% 的企业则指出在不同的服务环境中应用一致的安全策略十分复杂。人工智慧维运 (AIOps) 的出现可望重塑市场格局,基于人工智慧的自动化将提升预测性扩展、异常检测和系统效能。透过将机器学习与 IT 维运结合,企业能够更聪明、更可靠、更经济高效地管理微服务环境。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 28.3亿美元 |

| 预测值 | 180.8亿美元 |

| 复合年增长率 | 20.3% |

到了2024年,平台和解决方案细分市场占据70%的市场份额,成为市场成长的主要驱动力。对安全、可互通且高度可扩展的开发框架日益增长的依赖,推动了这一领域的领先地位。企业正在采用容器编排技术来管理分散式应用程序,而整合自动化、可观测性和API管理功能的平台也越来越受欢迎。这些进步使企业能够提高效率、保持可扩展性并简化复杂的基于微服务的工作流程,从而巩固了该细分市场在全球市场中的显着份额。

预计到2034年,公有云市场将以20.9%的复合年增长率成长。这一市场的成长主要得益于公有云环境提供的弹性託管基础设施服务的广泛应用。约76%的企业选择透过公有云框架部署微服务应用,因为公有云框架具有成本效益高、可扩展性强和运行速度快等优势。随着公有云生态系统的日趋成熟,该市场持续成长。公有云生态系统提供增强的DevOps整合、自动化编排和原生容器支援等功能,简化了全球企业的部署和效能管理。

2024年,美国云端微服务市场规模预计将达到11.1亿美元。美国商业领域,尤其是资讯科技和製造业,对云端技术的广泛采用是其市场领先地位的关键因素。超过60%的资讯产业企业表示正在积极使用云端应用,而製造业的中小型企业与往年相比,在云端应用方面遇到的障碍也越来越少。各行业云端应用的持续成长,使美国成为微服务部署和创新的重要中心。

全球云端微服务市场的主要企业包括微软、甲骨文、VMware、Salesforce、戴尔科技、Google、阿里巴巴、亚马逊AWS、SAP和IBM。为了巩固在全球云端微服务市场的地位,各大公司正实施以创新、合作和服务拓展为核心的策略。它们正大力投资开发整合平台,将自动化、分析和人工智慧驱动的编排相结合,以优化云端原生营运。与软体开发商、企业和云端服务供应商的策略合作,正在增强互通性并加快产品部署速度。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预报

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 云端原生应用程式越来越多地采用微服务。

- 容器化和 Kubernetes 编排的兴起

- 持续整合和持续交付(CI/CD)的需求

- 需要具有弹性和容错能力的架构

- 产业陷阱与挑战

- 管理分散式服务的复杂性

- 微服务架构中的安全漏洞

- 市场机会

- 边缘运算中微服务的扩展

- 与人工智慧/机器学习整合以实现智慧服务编排

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 碳足迹评估

- 循环经济一体化

- 电子垃圾管理要求

- 绿色製造倡议

- 用例和应用

- 最佳情况

- 产业特定成长机会

- 自动驾驶车辆和运输系统

- 智慧製造与工业物联网

- 再生能源与电网管理

- 供应链与物流优化

- 零售与电子商务平台演变

- 数位健康与个人化医疗

- 科技融合与整合趋势

- 多云和混合架构标准化

- 零信任安全模型实施

- 可观测性和 AIOps 平台集成

- GitOps 和基础架构即程式码的采用

- 永续计算与绿色技术

- 量子安全密码学与安全准备

- 开源解决方案与专有解决方案分析

- 资料管理与分析平台演进

- 投资与融资环境分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 平台/解决方案

- 容器编排平台

- API管理平台

- DevOps 和 CI/CD 整合工具

- 其他的

- 服务

- 部署与整合服务

- 咨询与顾问服务

- 维护与支援服务

- 培训与认证服务

第六章:市场估算与预测:依部署模式划分,2021-2034年

- 主要趋势

- 公共云端

- 私有云端

- 混合云端

第七章:市场估算与预测:依组织规模划分,2021-2034年

- 主要趋势

- 大型企业

- 中小企业

第八章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 资讯科技与电信/ITeS

- 零售与电子商务

- 卫生保健

- 银行、金融服务和保险业 (BFSI)

- 製造业

- 媒体与娱乐

- 政府和公共部门

- 运输与物流

- 其他的

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球参与者

- AWS (Amazon)

- Microsoft

- IBM / Red Hat

- VMware

- Oracle

- Alibaba

- SAP

- Salesforce

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Cisco Systems

- Adobe

- Intel

- Tencent Cloud

- 区域玩家

- Huawei Cloud

- Baidu Cloud

- NTT Communications

- Fujitsu

- T-Systems

- Orange Business Services

- Capgemini

- Atos

- Rackspace Technology

- DigitalOcean

- 新兴参与者/颠覆者

- Snowflake

- Databricks

- HashiCorp

- Pulumi

- Cloudify

The Global Cloud Microservices Market was valued at USD 2.83 billion in 2024 and is estimated to grow at a CAGR of 20.3% to reach USD 18.08 billion by 2034.

The rapid expansion is driven by the increasing migration of enterprise applications from traditional monolithic systems to modern, cloud-native architectures. Around 62.3% of organizations have adopted microservices and container-based technologies to enhance flexibility, streamline application development, and accelerate software deployment across distributed environments. The modular design of microservices empowers development teams to scale services and deploy updates more efficiently. However, operational challenges remain; 36% of enterprises report integration difficulties, while 35% cite the complexity of applying consistent security policies across diverse service environments. The emergence of artificial intelligence for IT operations (AIOps) is expected to reshape the market, with AI-based automation improving predictive scaling, anomaly detection, and system performance. By combining machine learning with IT operations, organizations are achieving smarter, more reliable, and cost-effective management of microservices environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.83 Billion |

| Forecast Value | $18.08 Billion |

| CAGR | 20.3% |

The platform and solution segment accounted for a 70% share in 2024, establishing itself as the leading contributor to market growth. The increasing reliance on secure, interoperable, and highly scalable development frameworks has fueled this dominance. Enterprises are embracing container orchestration technologies for managing distributed applications, while integrated platforms combining automation, observability, and API management capabilities are gaining traction. These advancements enable businesses to improve efficiency, maintain scalability, and streamline complex microservice-based workflows, reinforcing the segment's substantial share in the global market.

The public cloud segment is forecast to grow at a CAGR of 20.9% through 2034. The growth of this segment is supported by the strong adoption of elastic, managed infrastructure services offered through public cloud environments. Approximately 76% of enterprises deploy their microservice applications through public cloud frameworks due to their cost-effectiveness, scalability, and operational speed. This market segment continues to gain strength due to the maturity of public cloud ecosystems, which provide enhanced DevOps integration, automated orchestration, and native container support factors that simplify deployment and performance management for enterprises worldwide.

United States Cloud Microservices Market generated USD 1.11 billion in 2024. The high rate of cloud adoption across the U.S. business landscape, particularly within information technology and manufacturing industries, is a key contributor to this leadership. More than 60% of firms in the information sector reported active use of cloud-based applications, while small and mid-sized enterprises in manufacturing continue to show fewer adoption barriers compared to earlier years. The steady expansion of cloud usage across various industries positions the U.S. as a major hub for microservices deployment and innovation.

Leading companies in the Global Cloud Microservices Market include Microsoft, Oracle, VMware, Salesforce, Dell Technologies, Google, Alibaba, AWS (Amazon), SAP, and IBM. To strengthen their position in the Global Cloud Microservices Market, major companies are implementing strategies focused on innovation, partnerships, and service expansion. Firms are heavily investing in developing integrated platforms that combine automation, analytics, and AI-driven orchestration to optimize cloud-native operations. Strategic collaborations with software developers, enterprises, and cloud service providers are enabling enhanced interoperability and faster product deployment.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment model

- 2.2.4 Organization Size

- 2.2.5 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of microservices for cloud-native applications

- 3.2.1.2 Rise of containerization and Kubernetes orchestration

- 3.2.1.3 Demand for continuous integration and continuous delivery (CI/CD)

- 3.2.1.4 Need for resilient and fault-tolerant architectures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity in managing distributed services

- 3.2.2.2 Security vulnerabilities in microservices architectures

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of microservices in edge computing

- 3.2.3.2 Integration with AI/ML for intelligent service orchestration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability & environmental aspects

- 3.10.1 Carbon Footprint Assessment

- 3.10.2 Circular Economy Integration

- 3.10.3 E-Waste Management Requirements

- 3.10.4 Green Manufacturing Initiatives

- 3.11 Use cases and applications

- 3.12 Best-case scenario

- 3.13 Industry-specific growth opportunities

- 3.13.1 Autonomous vehicle & transportation systems

- 3.13.2 Smart manufacturing & industrial iot

- 3.13.3 Renewable energy & grid management

- 3.13.4 Supply chain & logistics optimization

- 3.13.5 Retail & e-commerce platform evolution

- 3.13.6 Digital health & personalized medicine

- 3.14 Technology convergence & integration trends

- 3.14.1 Multi-cloud & hybrid architecture standardization

- 3.14.2 Zero trust security model implementation

- 3.14.3 Observability & AIops platform integration

- 3.14.4 Gitops & infrastructure-as-code adoption

- 3.14.5 Sustainable computing & green technology

- 3.14.6 Quantum-safe cryptography & security preparation

- 3.15 Open source vs proprietary solution analysis

- 3.16 Data management & analytics platform evolution

- 3.17 Investment & funding landscape analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Platform/Solution

- 5.2.1 Container Orchestration Platforms

- 5.2.2 API Management Platforms

- 5.2.3 DevOps & CI/CD Integration Tools

- 5.2.4 Others

- 5.3 Services

- 5.3.1 Deployment & Integration Services

- 5.3.2 Consulting & Advisory Services

- 5.3.3 Maintenance & Support Services

- 5.3.4 Training & Certification Services

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Public cloud

- 6.3 Private cloud

- 6.4 Hybrid cloud

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Large Enterprises

- 7.3 Small & Medium Enterprises (SMEs)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 IT & Telecommunications / ITeS

- 8.3 Retail & e-Commerce

- 8.4 Healthcare

- 8.5 BFSI (Banking, Financial Services & Insurance)

- 8.6 Manufacturing

- 8.7 Media & Entertainment

- 8.8 Government & Public Sector

- 8.9 Transportation & Logistics

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 AWS (Amazon)

- 10.1.2 Microsoft

- 10.1.3 Google

- 10.1.4 IBM / Red Hat

- 10.1.5 VMware

- 10.1.6 Oracle

- 10.1.7 Alibaba

- 10.1.8 SAP

- 10.1.9 Salesforce

- 10.1.10 Dell Technologies

- 10.1.11 Hewlett Packard Enterprise (HPE)

- 10.1.12 Cisco Systems

- 10.1.13 Adobe

- 10.1.14 Intel

- 10.1.15 Tencent Cloud

- 10.2 Regional Players

- 10.2.1 Huawei Cloud

- 10.2.2 Baidu Cloud

- 10.2.3 NTT Communications

- 10.2.4 Fujitsu

- 10.2.5 T-Systems

- 10.2.6 Orange Business Services

- 10.2.7 Capgemini

- 10.2.8 Atos

- 10.2.9 Rackspace Technology

- 10.2.10 DigitalOcean

- 10.3 Emerging Players / Disruptors

- 10.3.1 Snowflake

- 10.3.2 Databricks

- 10.3.3 HashiCorp

- 10.3.4 Pulumi

- 10.3.5 Cloudify

2026年全球云端微服务市场报告

2026年全球云端微服务市场报告 全球云端微服务市场规模、份额、趋势和成长分析报告(2026-2034)全球云端微服务市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球云端微服务市场规模、份额、趋势和成长分析报告(2026-2034)全球云端微服务市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 云端微服务市场 - 全球产业规模、份额、趋势、机会和预测,按组件、部署模式、企业类型、最终用户、地区和竞争格局细分,2021-2031 年预测

云端微服务市场 - 全球产业规模、份额、趋势、机会和预测,按组件、部署模式、企业类型、最终用户、地区和竞争格局细分,2021-2031 年预测 云端微服务市场规模、份额和成长分析(按组件、组织规模、部署模式、垂直产业和地区划分)-2026-2033年产业预测

云端微服务市场规模、份额和成长分析(按组件、组织规模、部署模式、垂直产业和地区划分)-2026-2033年产业预测 云端微服务市场规模、份额和趋势分析(按组件、部署、企业规模、最终用途、地区和细分市场预测,2025 年至 2033 年)

云端微服务市场规模、份额和趋势分析(按组件、部署、企业规模、最终用途、地区和细分市场预测,2025 年至 2033 年) 云端微服务:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

云端微服务:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)