|

市场调查报告书

商品编码

1642011

云端微服务:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Cloud Microservices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

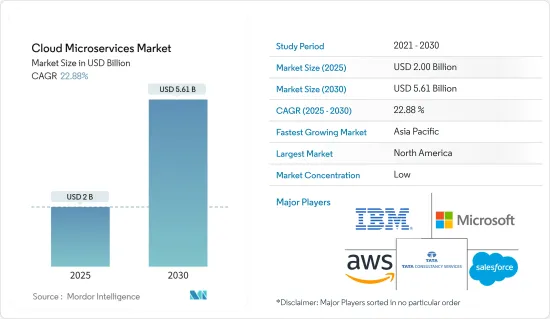

预计 2025 年云端微服务市场规模为 20 亿美元,到 2030 年预计将达到 56.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 22.88%。

随着 Kubernetes 的采用率不断增长,企业将开始意识到仅仅采用 Kubernetes 是不够的。您也可能改变流程、工具和架构的各个方面。 Kubernetes 很可能成为整个公司变革的主要推动力。 Kubernetes 提供了一种更好的方式来管理容器,使得微服务架构在企业规模上可行。

主要亮点

- 新冠疫情的爆发增加了全球对云端运算的需求。这使得云端微服务一直受到明显的影响,直到去年年底。由于劳动力短缺和远端监控需求,对云端服务的需求正在增加。

- 微服务架构的流行正在推动市场的发展,因为它鼓励将应用程式分解为更小的元件。它使得应用更改变得更容易。引入这样的元件不会影响大部分程式码库。这种架构风格对于使用轻量级容器配置的云端原生应用程式来说是典型的。原因在于大量的服务、分散式持续交付和 DevOps。

- 各个终端用户产业对混合云的采用正在推动市场发展,许多企业目前处于云端采用的不同阶段。混合云为探索新产品和经营模式提供了最大的灵活性。随着IT部门角色的扩大,资料中心的负担也随之增加。投资运算和储存升级成本高昂,但混合云端应用程式具有成本效益,并且在市场上越来越受欢迎。

- BFSI、IT、零售和其他各行业越来越多地采用云端技术,推动了云端微服务市场的成长。云端微服务是整体云端管理策略的重要组成部分,让 IT 管理员能够了解其云端基础的资源的运作情况。例如,总部位于阿拉伯联合大公国的马什雷克银行采用了领先的数位营运模式,利用微服务架构,并使用即时资料进行分析。

- 安全和合规问题正在抑制市场成长。虽然容器可以提供更灵活的软体开发环境,但它们也引入了影响合规性的新安全风险。网路攻击者可以利用云端架构的权限设定中的漏洞来存取敏感资讯服务。

云端微服务市场趋势

製造业可望大幅成长

- 智慧技术的进步正在瓦解传统的自动化金字塔,增加了製造业对微服务云的需求。此外,製造业IT正在朝向服务和应用导向发展。

- 亚马逊网路服务 (AWS)计量收费的微服务和无伺服器运算模式以最少的前期投资和几乎无限的按需容量降低了运行互联製造工厂和智慧产品程式的成本。

- 「云端网路製造」提供了新的经营方式,因为製造公司意识到,如果没有资讯科技(IT)支援和电脑辅助功能,他们可能无法在竞争激烈的市场中生存。微软是製造业强大的核心技术供应商,为製造商提供支援 OPC(开放平台通讯)UA 的机器的数位双胞胎,显着增强了安全性和身份验证管理。在这里,客户可以使用在 Azure 上执行的微服务直接从云端控制和管理他们的 OPC 孪生。

- 德国跨国企业集团蒂森克虏伯利用物联网技术将电梯连接到微服务云。从电梯感测器收集的资料可让演算法处理资讯并预测电梯在发生故障之前何时需要维护。扩增实境进一步增强了这种预测性维护,使电梯技术人员可以使用 Microsoft HoloLens 在现场接收来自专家的免持远端指令。

北美占有最大市场占有率

- 由于先进技术的不断采用,该地区正在占据较高的市场占有率。此外,金融、电子商务、旅游服务等领域对微服务架构的采用正在推动北美公司的需求。微服务架构有助于经济高效地储存资讯和资料,并使其更加灵活、高效和扩充性。

- 据国际电信联盟称,加拿大在数位转型技术和服务方面的支出将包括对认知/人工智慧 (AI) 系统、物联网、下一代安全以及扩增实境实境和虚拟实境、3D 列印和机器人等新兴技术的投资。

- 沃尔玛加拿大将其软体架构重构为微服务。儘管无法处理每分钟 600 万次的页面浏览量,该公司还是看到了即时的效果,因为他们的转换率在一夜之间大幅提升。停机时间也被最小化,并且公司透过用较便宜的虚拟x86 伺服器替换昂贵的商品硬件,实现了 20-50% 的总体成本节省。这显示了该行业对云端微服务的需求。

- 在美国,由 IBM Cloud Functions 和 Cloud Foundry 支援的微服务为商店购物应用程式提供支援。它展示了古董计算设备的目录,客户可以购买并添加评论,从而促进市场成长。

云端微服务产业概览

云端微服务市场是分散的。主要企业正在采用各种策略,包括新产品发布、伙伴关係和收购,涉及多种部署模式——公共云端、私有云端和混合云端。透过扩大我们在这个市场的影响力,这有助于我们实现长期永续发展。主要参与者包括亚马逊网路服务公司、微软公司和 IBM 公司。目前市场的发展包括:

- 2022 年 1 月 - 领先的 EHS 软体和内容提供者 Red-on-line 收购 EHS 平台解决方案领导者 Gutwinski Management GmbH。此次收购创造了一个深度互补的客户组合,使产品和服务能够惠及全球更多客户。

- 分析自动化公司 Alteryx, Inc. 收购了提供云端优先功能的 Trifacta。透过此次收购,Alteryx 可以向大型企业提供云端整合的、端到端的、低程式码/无程式码分析自动化平台。它还使您能够满足整个企业的需求,包括资料分析团队、IT/资料工程团队和业务用户。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素与限制因素简介

- 市场驱动因素

- 微服务架构的兴起

- 各种最终用户产业采用混合云端

- 市场限制

- 安全性与合规性

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第 5 章。

第六章 市场细分

- 依部署方式

- 平台

- 按服务

- 按公司规模

- 中小企业

- 大型企业

- 按最终用户产业

- BFSI

- 零售

- 电子商务

- 製造业

- 通讯业

- IT 和 IT 公司

- 卫生保健

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Amazon Web Services Inc.

- Microsoft Corporation

- IBM Corporation

- Salesforce.com Inc.

- Tata Consultancy Services Limited

- Broadcom Inc.(CA Technologies)

- VMware Inc.(Pivotal Software Inc.)

- Infosys Ltd

- Oracle Corporation

- NGINX Inc.

- Syntel Inc.

- Idexcel Inc.

- RapidValue IT Services Private Limited

第八章投资分析

第九章 市场机会与未来趋势

The Cloud Microservices Market size is estimated at USD 2.00 billion in 2025, and is expected to reach USD 5.61 billion by 2030, at a CAGR of 22.88% during the forecast period (2025-2030).

As Kubernetes' adoption grows, companies are expected to start realizing that it is not enough to adopt it. They will also likely change all aspects of their processes, tools, and architecture. Kubernetes is likely to be a big push for profound company-wide changes. It provides an excellent way to manage containers and makes microservices architectures practical at an enterprise scale.

Key Highlights

- Owing to the COVID-19 outbreak, the global demand for the cloud increased. Due to this, the cloud microservices were severely influenced until last year's end. The need for cloud services is growing due to a lack of workforce and remote monitoring requirements.

- The microservices architecture proliferation is driving the market, as it encourages breaking the application into smaller components. It becomes easy to apply changes. Deploying such components does not end up impacting a large part of the codebase. It is standard for such an architectural style to be adopted for cloud-native applications using lightweight container deployment. It is because of the large number of services, decentralized continuous delivery, and DevOps.

- Hybrid cloud adoption across various end-user industries is driving the market, as many enterprises are currently in different stages of cloud adoption. The hybrid cloud gives them maximum flexibility to explore new products and business models. As IT's role grew, the load on the data center was evolving. Investing money in upgrading computing or storage is costly, but hybrid cloud applications are cost-effective and drive the market.

- The growing cloud technology adoption across industries such as BFSI, IT, retail, and various others is augmenting the cloud microservices market growth. It is a significant part of an overall cloud management strategy, enabling IT administrators to review the cloud-based resources' operational status. For instance, United Arab Emirates-based Mashreq Bank adopted an advanced digital operating model, utilized microservices architecture, and leveraged real-time data for analytics.

- Security and compliance issues are restraining the market from witnessing growth. The container can create more software development environments, but it leads to new security risks that affect compliance. Cyber attackers can benefit from vulnerabilities inside the permission settings of cloud architecture to reach sensitive data services.

Cloud Microservices Market Trends

Manufacturing Sector Expected to Register a Significant Growth

- Due to intelligent technology advancement, the microservice cloud demand is increasing in the manufacturing sector as the traditional automation pyramid dissolves. Moreover, manufacturing IT is moving toward service orientation and app orientation.

- AWS (Amazon Web Services) pay-as-you-go microservices and serverless computing models reduce the cost of running the connected manufacturing plant or smart product programs with minimum upfront investment and nearly unlimited on-demand capacity.

- "Cloud network manufacturing" provides a new way for business, as manufacturing companies discovered they may not survive in the competitive market without Information Technology (IT) support and computer-aided capabilities. Microsoft is the dominant core technology supplier to the manufacturing industry, which provides manufacturers a digital twin of their OPC (Open platform communication) UA-enabled machines and significantly enhances security and certification management. Here, customers can control and manage their OPC twins directly from the cloud using microservices running on Azure.

- ThyssenKrupp, a German multinational conglomerate, drew upon IoT technology to connect its elevators to the microservice cloud. The data collected from an elevator's sensors allows algorithms to process information and predict when maintenance is required before the elevator breaks down. This predictive maintenance is further enhanced by augmented reality, with elevator technicians utilizing Microsoft HoloLens to receive remote, hands-free instructions from experts while in the field.

North America to Account for Largest Market Share

- Due to the increasingly advanced technologies adoption, this region is gaining a high market share. Moreover, there is a growing demand from North American companies, as they have adopted microservices architecture in financial, e-commerce, and travel services. It helps store information and data cost-effectively and increases agility, efficiency, and scalability.

- As per ITU, digital Transformation technologies and services spent in Canada are set to exceed USD 16 billion sustained by the investment in emerging technologies, such as cognitive/artificial intelligence (AI) systems, IoT, next-generation security, augmented reality or virtual reality, 3D printing, and robotics, driving the cloud microservices.

- Walmart Canada refactored its software architecture to microservices. The company, which could not handle the 6 million page views per minute it was getting, realized instant results with a significant increase in its conversion rate overnight. The downtime was also minimized, and the company can replace expensive commodity hardware with cheaper virtual x86 servers, resulting in overall cost savings between 20 and 50 %. It gives demand for cloud microservice in this sector.

- In the United States, Microservices with IBM Cloud Functions and Cloud Foundry deploys a storefront shopping application. It displays an antique computing devices catalog where customers can make purchases and add review comments, increasing the market's growth.

Cloud Microservices Industry Overview

The cloud microservices market is fragmented. The major players have used various strategies, such as new product launches, partnerships, acquisitions, and others, across multiple deployment modes, like public, private, and hybrid cloud. It helps increase their footprints in this market to sustain the long run. Amazon Web Services Inc., Microsoft Corporation, IBM Corporation, etc., are the primary players. Current advancements in the market are:

- January 2022 - Red-on-line, a leading EHS software and content provider, acquired Gutwinski Management GmbH, a leading EHS platform solution. The acquisition will create a profoundly complementary client portfolio product and have an opportunity to make products and services available to even more customers worldwide.

- Alteryx, Inc., the Analytics Automation company, acquired Trifacta, which offers cloud-first capabilities to help enterprises drive their analytics transformation at scale. With this acquisition, Alteryx will be uniquely positioned to provide large enterprises with an integrated end-to-end, low-code/no-code analytics automation platform in the cloud. It will also serve the needs of the entire enterprise: data analytics teams, IT/data engineering teams, and business users.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Proliferation of the Microservices Architecture

- 4.3.2 Adoption of Hybrid Cloud Across Various End-user Industries

- 4.4 Market Restraints

- 4.4.1 Security and Compliance

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Analysis on the impact of COVID-19 on the Cloud Microservices Market

6 MARKET SEGMENTATION

- 6.1 By Deployment Mode

- 6.1.1 Platforms

- 6.1.2 Service

- 6.2 By Enterprise Size

- 6.2.1 Small and Medium Enterprises

- 6.2.2 Large Enterprises

- 6.3 By End-user Industry

- 6.3.1 BFSI

- 6.3.2 Retail

- 6.3.3 E-commerce

- 6.3.4 Manufacturing

- 6.3.5 Telecommunications

- 6.3.6 IT and ITes

- 6.3.7 Healthcare

- 6.3.8 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amazon Web Services Inc.

- 7.1.2 Microsoft Corporation

- 7.1.3 IBM Corporation

- 7.1.4 Salesforce.com Inc.

- 7.1.5 Tata Consultancy Services Limited

- 7.1.6 Broadcom Inc. (CA Technologies)

- 7.1.7 VMware Inc. (Pivotal Software Inc.)

- 7.1.8 Infosys Ltd

- 7.1.9 Oracle Corporation

- 7.1.10 NGINX Inc.

- 7.1.11 Syntel Inc.

- 7.1.12 Idexcel Inc.

- 7.1.13 RapidValue IT Services Private Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球云端微服务市场规模、份额、趋势和成长分析报告(2026-2034)全球云端微服务市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球云端微服务市场规模、份额、趋势和成长分析报告(2026-2034)全球云端微服务市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 云端微服务市场 - 全球产业规模、份额、趋势、机会和预测,按组件、部署模式、企业类型、最终用户、地区和竞争格局细分,2021-2031 年预测

云端微服务市场 - 全球产业规模、份额、趋势、机会和预测,按组件、部署模式、企业类型、最终用户、地区和竞争格局细分,2021-2031 年预测 云端微服务市场规模、份额和成长分析(按组件、组织规模、部署模式、垂直产业和地区划分)-2026-2033年产业预测

云端微服务市场规模、份额和成长分析(按组件、组织规模、部署模式、垂直产业和地区划分)-2026-2033年产业预测 云端微服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

云端微服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 云端微服务市场规模、份额和趋势分析(按组件、部署、企业规模、最终用途、地区和细分市场预测,2025 年至 2033 年)

云端微服务市场规模、份额和趋势分析(按组件、部署、企业规模、最终用途、地区和细分市场预测,2025 年至 2033 年)