|

市场调查报告书

商品编码

1885859

医疗设备维护市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Medical Equipment Maintenance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

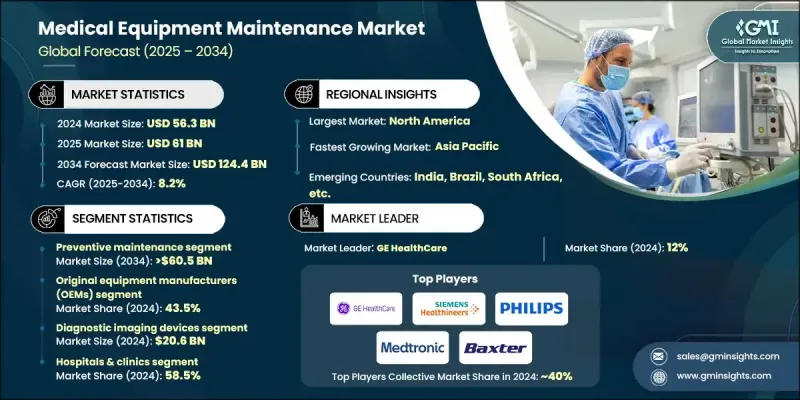

2024 年全球医疗设备维护市场价值为 563 亿美元,预计到 2034 年将以 8.2% 的复合年增长率增长至 1244 亿美元。

市场成长的驱动因素包括:对病人安全的日益重视、翻新和先进医疗设备的普及、慢性病盛行率的上升以及医疗设备维护方面日益严格的监管要求。医院和诊所致力于最大限度地降低设备故障的风险,因为设备故障会危及患者的护理和安全。预防性维护计画正被广泛采用,以确保设备在安全参数范围内运作、减少错误并符合相关法规。对可靠性、运作效率和监管的需求促使医疗机构选择计划性维护策略,从而推动市场扩张。该领域的维护包括对医疗设备进行定期检查、保养、维修和校准,以确保医疗机构设备的最佳性能、安全性和更长的使用寿命。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 563亿美元 |

| 预测值 | 1244亿美元 |

| 复合年增长率 | 8.2% |

2024年,预防性维护业务市占率达47.2%。该业务的成长得益于专为小型医疗机构设计的经济高效的维护解决方案。预防性维护包括例行检查、校准和保养,旨在减少设备意外故障并保持最佳效能。透过及早发现并解决潜在问题,预防性维护可以最大限度地减少停机时间,延长设备使用寿命,并提高病患安全。越来越多的医院采用这些方案,以符合相关法规并降低紧急维修成本。

到2024年,原始设备製造商(OEM)市占率将达到43.5%。 OEM透过提供客製化服务、基于规格的零件和专业技术来维持市场主导地位。他们的策略包括长期服务协议、预测性维护和远端监控,这些通常由数位化平台提供支援。 OEMOEM能够确保符合法规要求并提供高品质的服务,因此成为关键和高价值医疗设备的首选供应商。

2024年,北美医疗设备维护市场占40.7%的份额。该地区先进的医疗保健体系、对新型医疗技术的广泛应用以及严格的监管标准,推动了对预防性和预测性维护的需求。该地区的主要原始设备製造商(OEM)提供整合服务合约和数位化解决方案,而独立服务机构(ISO)也越来越多地提供经济高效的外包维护方案。

全球医疗设备维护市场的主要参与者包括富士胶片、Alliance Medical CORPORATION、Drive DeVilbiss HEALTHCARE、百特、日立高新技术、ALTHEA、STERIS HEALTHCARE、飞利浦、Aramark、美敦力、GE医疗、Probo MEDICAL、瑞思迈、GETINGE和西门子医疗。各公司正透过投资先进的数位化维护平台、预测性维护技术和远端监控解决方案来巩固其市场地位。策略合作、併购有助于企业拓展至新的地区和医疗保健领域。提供客製化的服务合同,包括预防性和紧急维护方案,有助于提升客户忠诚度。各公司注重合规性、认证和培训项目,以建立信誉和信任。此外,透过独立销售机构(ISO)提供的外包解决方案为医院提供了更具成本效益的替代方案,而维护解决方案的创新则确保了停机时间的减少、效率的提高和患者安全性的提升,从而巩固了企业的长期市场地位。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 先进医疗器材的日益普及

- 慢性病盛行率激增

- 越来越重视病人安全和设备正常运作时间

- 医疗器械维护的监管合规要求

- 翻新医疗器材的高采用率

- 产业陷阱与挑战

- 维护服务和合约成本高昂

- 复杂设备熟练技术人员短缺

- 机会

- 利用人工智慧和物联网进行预测性维护

- 远端监控解决方案,提高成本效益

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 服务合约模式展望

- 永续发展和绿色维护倡议

- 波特的分析

- PESTEL 分析

- 差距分析

- 远端监控与远端维护的集成

- 未来市场趋势

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新服务上线

- 扩张计划

第五章:市场估算与预测:依服务类型划分,2021-2034年

- 主要趋势

- 预防性维护

- 修正性维护

- 运作维护

第六章:市场估算与预测:依服务提供者划分,2021-2034年

- 主要趋势

- 原始设备製造商(OEM)

- 内部维护

- 独立服务机构(ISO)

第七章:市场估算与预测:依设备类型划分,2021-2034年

- 主要趋势

- 诊断影像设备

- 电疗设备

- 手术器械

- 病人监护和维生设备

- 牙科设备

- 内视镜设备

- 实验室设备

- 其他设备

第八章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 医院和诊所

- 诊断影像中心

- 门诊手术中心(ASC)

- 牙医诊所

- 透析中心

- 其他最终用途

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Alliance Medical CORPORATION

- ALTHEA

- Aramark

- Baxter

- Drive DeVilbiss HEALTHCARE

- FUJIFILM

- GE HealthCare

- GETINGE

- Hitachi High-Tech

- Medtronic

- PHILIPS

- Probo MEDICAL

- Resmed

- SIEMENS Healthineers

- STERIS HEALTHCARE

The Global Medical Equipment Maintenance Market was valued at USD 56.3 billion in 2024 and is estimated to grow at a CAGR of 8.2 % to reach USD 124.4 billion by 2034.

Market growth is driven by increasing emphasis on patient safety, rising adoption of refurbished and advanced medical devices, growing prevalence of chronic diseases, and stringent regulatory requirements for medical device upkeep. Hospitals and clinics are focusing on minimizing the risks posed by equipment failure, which can compromise patient care and safety. Preventive maintenance programs are being widely adopted to ensure devices operate within safe parameters, reduce errors, and maintain compliance with regulations. The need for reliability, operational efficiency, and oversight is pushing healthcare providers to opt for planned maintenance strategies, thereby fueling market expansion. Maintenance in this sector includes regular inspection, servicing, repair, and calibration of medical devices, ensuring optimal performance, safety, and longer equipment lifespan across healthcare facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $56.3 Billion |

| Forecast Value | $124.4 Billion |

| CAGR | 8.2% |

The preventive maintenance segment held a 47.2% share in 2024. Growth in this segment is supported by cost-effective maintenance solutions designed for smaller healthcare facilities. Preventive maintenance involves routine inspections, calibration, and servicing to reduce unplanned device failures and maintain peak performance. By identifying and resolving potential issues early, it minimizes downtime, extends equipment life, and enhances patient safety. Hospitals increasingly adopt these programs to comply with regulations and reduce the costs associated with emergency repairs.

The original equipment manufacturers (OEMs) segment held a 43.5% share in 2024. OEMs maintain control by offering tailored service, specification-based parts, and technical expertise. Their strategies include long-term service agreements, predictive maintenance, and remote monitoring, often supported by digital platforms. OEM maintenance guarantees compliance with regulations and high-quality service, making them preferred providers for critical and high-value medical equipment.

North America Medical Equipment Maintenance Market captured 40.7% share in 2024. The region's advanced healthcare systems, high adoption of new medical technologies, and stringent regulatory standards drive demand for preventive and predictive maintenance. Major OEMs in the region provide integrated service contracts and digital solutions, while independent service organizations (ISOs) are increasingly offering cost-effective outsourced maintenance options.

Key players in the Global Medical Equipment Maintenance Market include FUJIFILM, Alliance Medical CORPORATION, Drive DeVilbiss HEALTHCARE, Baxter, Hitachi High-Tech, ALTHEA, STERIS HEALTHCARE, Philips, Aramark, Medtronic, GE Healthcare, Probo MEDICAL, ResMed, and GETINGE, SIEMENS Healthineers. Companies are strengthening their presence by investing in advanced digital maintenance platforms, predictive maintenance technologies, and remote monitoring solutions. Strategic partnerships, mergers, and acquisitions allow expansion into new regions and healthcare segments. Offering customized service contracts, including preventive and emergency maintenance packages, enhances customer loyalty. Firms focus on regulatory compliance, certifications, and training programs to build credibility and trust. Additionally, outsourcing solutions via ISOs provides cost-effective alternatives to hospitals, while innovation in maintenance solutions ensures reduced downtime, improved efficiency, and higher patient safety, reinforcing long-term market positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Service type trends

- 2.2.3 Service provider trends

- 2.2.4 Equipment trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of advanced medical devices

- 3.2.1.2 Surging prevalence of chronic diseases

- 3.2.1.3 Growing focus on patient safety and equipment uptime

- 3.2.1.4 Regulatory compliance requirements for medical device maintenance

- 3.2.1.5 High adoption of refurbished medical equipment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of maintenance services and contracts

- 3.2.2.2 Shortage of skilled technicians for complex devices

- 3.2.3 Opportunities

- 3.2.3.1 Predictive maintenance using AI and IoT

- 3.2.3.2 Remote monitoring solutions for cost efficiency

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Service contract models outlook

- 3.7 Sustainability and green maintenance initiatives

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Gap analysis

- 3.11 Integration of remote monitoring and tele-maintenance

- 3.12 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Service Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Preventive maintenance

- 5.3 Corrective maintenance

- 5.4 Operational maintenance

Chapter 6 Market Estimates and Forecast, By Service Provider, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Original equipment manufacturers (OEMs)

- 6.3 In-house maintenance

- 6.4 Independent service organizations (ISOs)

Chapter 7 Market Estimates and Forecast, By Equipment, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Diagnostic imaging devices

- 7.3 Electromedical devices

- 7.4 Surgical instruments

- 7.5 Patient monitoring and life support devices

- 7.6 Dental equipment

- 7.7 Endoscopic devices

- 7.8 Laboratory equipment

- 7.9 Other equipment

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals & clinics

- 8.3 Diagnostic imaging centers

- 8.4 Ambulatory surgical centers (ASCs)

- 8.5 Dental clinics

- 8.6 Dialysis centers

- 8.7 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alliance Medical CORPORATION

- 10.2 ALTHEA

- 10.3 Aramark

- 10.4 Baxter

- 10.5 Drive DeVilbiss HEALTHCARE

- 10.6 FUJIFILM

- 10.7 GE HealthCare

- 10.8 GETINGE

- 10.9 Hitachi High-Tech

- 10.10 Medtronic

- 10.11 PHILIPS

- 10.12 Probo MEDICAL

- 10.13 Resmed

- 10.14 SIEMENS Healthineers

- 10.15 STERIS HEALTHCARE

医疗设备维修与维护市场:2026-2030年全球市场预测(依设备类型、服务类型、服务模式、最终用户、适应症和服务供应商划分)

医疗设备维修与维护市场:2026-2030年全球市场预测(依设备类型、服务类型、服务模式、最终用户、适应症和服务供应商划分) 2026年全球医疗设备维护市场报告

2026年全球医疗设备维护市场报告 全球医疗设备维护市场规模、份额、趋势和成长分析报告(2026-2034年)

全球医疗设备维护市场规模、份额、趋势和成长分析报告(2026-2034年) 医疗设备维修软体市场 - 全球产业规模、份额、趋势、机会、预测:按部署模式、最终用途、地区和竞争格局划分,2021-2031年医疗设备维护市场-全球产业规模、份额、趋势、机会、预测:按设备、服务、地区和竞争对手划分,2021-2031年医用修復敷料市场按产品类型、伤口类型、最终用户和分销管道划分 - 全球预测 2026-2032医疗影像诊断设备维护服务市场(按服务类型、设备类型、合约类型、服务提供者和最终用户划分)-2026-2032年全球预测医疗设备维修服务市场(按设备类型、服务模式、服务供应商、合约类型和最终用户划分)-2026-2032年全球预测

医疗设备维修软体市场 - 全球产业规模、份额、趋势、机会、预测:按部署模式、最终用途、地区和竞争格局划分,2021-2031年医疗设备维护市场-全球产业规模、份额、趋势、机会、预测:按设备、服务、地区和竞争对手划分,2021-2031年医用修復敷料市场按产品类型、伤口类型、最终用户和分销管道划分 - 全球预测 2026-2032医疗影像诊断设备维护服务市场(按服务类型、设备类型、合约类型、服务提供者和最终用户划分)-2026-2032年全球预测医疗设备维修服务市场(按设备类型、服务模式、服务供应商、合约类型和最终用户划分)-2026-2032年全球预测 医疗设备维护市场规模、份额和成长分析(按设备类型、服务类型、服务供应商、合约类型和地区划分)-2026-2033年产业预测

医疗设备维护市场规模、份额和成长分析(按设备类型、服务类型、服务供应商、合约类型和地区划分)-2026-2033年产业预测 全球医疗设备维护市场(至 2030 年)按设备(MRI、X 光、CT、超音波、病患监测、牙科设备)、提供者(OEM、ISO)、服务(预防、纠正)、合约服务(客製化、附加元件)和最终用户(医院、ASC)划分

全球医疗设备维护市场(至 2030 年)按设备(MRI、X 光、CT、超音波、病患监测、牙科设备)、提供者(OEM、ISO)、服务(预防、纠正)、合约服务(客製化、附加元件)和最终用户(医院、ASC)划分