|

市场调查报告书

商品编码

1892730

电动汽车电池健康监测市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)EV Battery Health Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

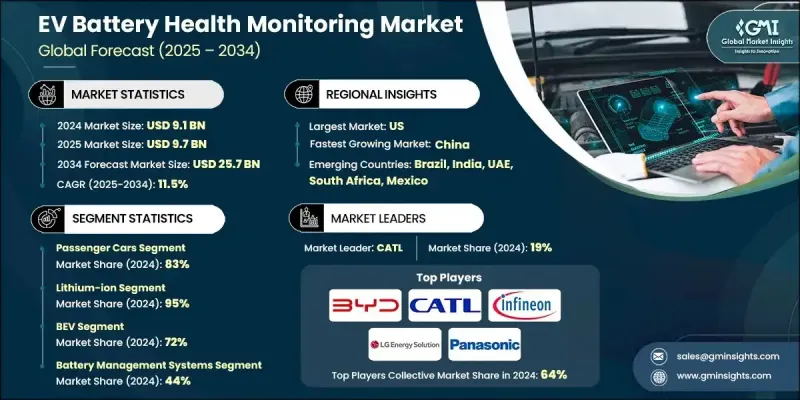

2024 年全球电动车电池健康监测市场价值为 91 亿美元,预计到 2034 年将以 11.5% 的复合年增长率成长至 257 亿美元。

电动车的快速普及催生了对精准、即时电池健康资料的迫切需求。电池成本几乎占电动车总成本的一半,因此,原始设备製造商 (OEM) 和车队营运商密切监控电池的荷电状态 (SOC) 和健康状态 (SOH),以减少保固索赔、提升运行安全性并增强消费者信心。先进的电池监控系统正日益融合预测性维护、人工智慧和机器学习技术,以预测故障、优化充电模式并预防热问题。这些创新技术能够最大限度地减少停机时间、延长电池寿命并提高车队可靠性。随着软体定义电池平台的兴起,预测分析和数位孪生技术正成为高效电池管理的关键要素。政府法规以及对电池安全和回收利用的生命週期透明度要求,进一步推动了全球范围内先进诊断和监控解决方案的部署,从而支撑了预测期内市场的强劲增长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 91亿美元 |

| 预测值 | 257亿美元 |

| 复合年增长率 | 11.5% |

2024年乘用车市占率达83%,预计2025年至2034年将以11%的复合年增长率成长。电动车在乘用车领域的普及推动了对精准即时电池资料的需求。更长的保固期、更高的安全性和可预测的性能促使製造商整合先进的SOH(电池健康状态)和SOC(电池荷电状态)演算法,从而增强消费者信任并实现车型差异化。

锂离子电池在2024年占据了95%的市场份额,预计2025年至2034年将以11.5%的复合年增长率成长。其在电动车中的广泛应用凸显了监测关键性能指标的必要性。高能量密度、对温度波动的敏感度、电压不平衡以及频繁的充放电循环,都要求精密的诊断技术,以在各种驾驶条件下保持性能稳定、确保安全并延长电池寿命。

美国电动车电池健康监测市场占 86% 的市场份额,预计到 2024 年将创造 31 亿美元的收入。政府激励措施、税收优惠和清洁旅行计画的大力支持,推动了电动车的普及,促使汽车製造商和车队营运商寻求先进的电池健康管理系统,以确保安全、优化保修,并在各种条件下实现可靠的长期运作。

目录

第一章:方法论

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 互联电动车平台的日益普及

- 向人工智慧驱动的电池诊断转型

- 电池安全法规和透明度要求

- 电动商用车队的成长

- 产业陷阱与挑战

- 先进监控硬体成本高昂

- 电池化学成分和设计的多样性

- 热安全问题

- 资料安全和隐私问题

- 市场机会

- 二次利用和回收市场的扩张

- 亚太地区电动汽车製造业务成长

- 充电基础设施集成

- 车队预测性维修服务

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 目前技术

- 先进的电池管理系统

- 车载电池诊断与嵌入式感测

- 云端电池分析平台

- 车辆远程资讯处理和基于 CAN 的资料集成

- 新兴技术

- 基于人工智慧的电池健康预测和剩余使用寿命建模

- 数位孪生电池建模

- 基于区块链的电池可追溯性和生命週期完整性

- 支援 5G 的低延迟电池遥测和 V2X 集成

- 目前技术

- 专利分析

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 价格趋势

- 按地区

- 透过电池

- 定价分析与成本结构

- BMS硬体成本明细

- 软体授权和订阅模式

- 车队营运商的总拥有成本

- 价格侵蚀趋势与商品化风险

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 电池化学多样性及监测复杂性

- 锂离子化学变异体

- 固态电池监控挑战

- 热管理和热失控预防架构

- 热失控机制及检测阶段

- 多点温度感测策略

- 热传播监测与预警系统

- 主动式与被动式热管理集成

- V2G 整合与电池损耗统计

- ISO 15118-20 双向功率传输协议

- V2G运作中的电池衰减机制

- V2 G 特定 SOH 追踪和报告

- 网格服务最佳化演算法

- 二次电池评估及循环经济可行性

- 首次生命终结标准与健康阈值

- 二次利用适用性分析

- 第二生命认证的健康监测

- 车队远端资讯处理整合及整体拥有成本优化

- 车队管理平台架构

- 电池健康监测辅助车队降低总拥有成本

- 多车电池健康基准测试

- 车队电气化投资报酬率建模

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估价与预测:依电池类型划分,2021-2034年

- 锂离子

- 铅酸

- 镍氢

- 其他的

第六章:市场估算与预测:以推进方式划分,2021-2034年

- 纯电动车

- 插电式混合动力汽车

- 戊型肝炎病毒

第七章:市场估价与预测:依车辆类型划分,2021-2034年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型

- 中型

- 重负

第八章:市场估算与预测:依技术划分,2021-2034年

- 电池管理系统

- 监测与诊断

- 人工智慧/机器学习和云端分析

- 车队远端资讯处理和远端监控

- 售后诊断解决方案

- 其他的

第九章:市场估计与预测:依应用领域划分,2021-2034年

- 首次车辆营运

- 车队管理

- 充电基础设施集成

- 车网互动服务

- 其他的

第十章:市场估计与预测:依最终用途划分,2021-2034年

- 汽车原厂设备製造商

- 车队营运商

- 电池製造商和供应商

- 充电基础设施供应商

- 售后服务提供者

- 其他的

第十一章:市场估计与预测:按地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- 全球参与者

- Continental

- LG Energy Solution

- Panasonic

- CATL

- BYD

- Analog Devices

- Samsung SDI

- Texas Instruments

- Infineon

- LEM International

- 区域玩家

- Samsara

- Geotab

- NXP Semiconductors

- Denso

- Valeo

- Renesas Electronics

- STMicroelectronics

- 新兴参与者:

- Qnovo

- Teltonika

- Twaice Technologies

- Breathe Battery Technologies

- Voltaiq

- Brill Power

The Global EV Battery Health Monitoring Market was valued at USD 9.1 billion in 2024 and is estimated to grow at a CAGR of 11.5% to reach USD 25.7 billion by 2034.

The accelerating adoption of electric vehicles has created a critical demand for accurate, real-time battery health data. Batteries account for nearly half of an EV's total cost, prompting OEMs and fleet operators to closely monitor state-of-charge (SOC) and state-of-health (SOH) to reduce warranty claims, enhance operational safety, and strengthen consumer confidence. Advanced battery monitoring systems are increasingly incorporating predictive maintenance, artificial intelligence, and machine learning to anticipate failures, optimize charging patterns, and prevent thermal issues. These innovations minimize downtime, extend battery longevity, and improve fleet reliability. With the rise of software-defined battery platforms, predictive analytics, and digital twins are becoming essential for efficient battery management. Government regulations and lifecycle transparency requirements for battery safety and recycling further drive the deployment of sophisticated diagnostic and monitoring solutions worldwide, supporting robust market growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.1 Billion |

| Forecast Value | $25.7 Billion |

| CAGR | 11.5% |

The passenger car segment held an 83% share in 2024 and is expected to grow at a CAGR of 11% from 2025 to 2034. Increasing EV adoption in passenger vehicles is fueling the demand for precise, real-time battery data. Longer warranty terms, improved safety, and predictable performance compel manufacturers to integrate advanced SOH and SOC algorithms, enhancing consumer trust and differentiating models.

The lithium-ion batteries segment held a 95% share in 2024, expected to grow at a CAGR of 11.5% from 2025 to 2034. Their widespread use in EVs underscores the necessity of monitoring key performance metrics. High energy density, sensitivity to temperature fluctuations, voltage imbalance, and frequent charge cycles require sophisticated diagnostics to maintain uniform performance, ensure safety, and extend battery life under diverse driving conditions.

US EV Battery Health Monitoring Market held an 86% share, generating USD 3.1 billion in 2024. Strong EV adoption supported by government incentives, tax benefits, and clean mobility initiatives has driven OEMs and fleet operators to seek advanced battery health management systems for safety, warranty optimization, and reliable long-term operation across varying conditions.

Major players in the EV Battery Health Monitoring Market include LG Energy Solution, Analog Devices, BYD, CATL, Continental, Infineon, LEM International, Panasonic, Samsung SDI, and Texas Instruments. Market leaders in EV battery health monitoring are focusing on developing advanced chipsets and sensor solutions to enhance real-time monitoring capabilities. Companies are investing heavily in AI-driven predictive maintenance platforms and machine learning algorithms to anticipate failures, optimize charging cycles, and improve safety. Strategic partnerships with EV manufacturers and fleet operators ensure widespread integration of monitoring systems. Firms are also expanding their global distribution networks and local service capabilities to support diverse regional requirements. Continuous research and development efforts are driving innovation in software-defined battery management and digital twin technologies. Regulatory compliance, product customization, and technology differentiation remain central to maintaining competitive advantage and securing long-term market presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery

- 2.2.3 Technology

- 2.2.4 Propulsion

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.2.7 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of connected EV platforms

- 3.2.1.2 Shift toward AI-driven battery diagnostics

- 3.2.1.3 Battery safety regulations and transparency mandates

- 3.2.1.4 Growth of electrified commercial fleets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced monitoring hardware

- 3.2.2.2 Variability in battery chemistries and designs

- 3.2.2.3 Thermal safety concerns

- 3.2.2.4 Data security and privacy issues

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of second-life and recycling markets

- 3.2.3.2 Growth in APAC EV manufacturing

- 3.2.3.3 Charging infrastructure integration

- 3.2.3.4 Predictive maintenance services for fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current Technologies

- 3.7.1.1 Advanced battery management systems

- 3.7.1.2 On-board battery diagnostics & embedded sensing

- 3.7.1.3 Cloud-connected battery analytics platforms

- 3.7.1.4 Vehicle telematics & can-based data integration

- 3.7.2 Emerging Technologies

- 3.7.2.1 AI-powered predictive battery health & RUL modeling

- 3.7.2.2 Digital twin battery modeling

- 3.7.2.3 Blockchain-Enabled Battery Traceability & Lifecycle Integrity

- 3.7.2.4 5G-enabled low-latency battery telemetry & V2X integration

- 3.7.1 Current Technologies

- 3.8 Patent analysis

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By battery

- 3.11 Pricing analysis & cost structure

- 3.11.1 BMS hardware cost breakdown

- 3.11.2 Software licensing & subscription models

- 3.11.3 Total cost of ownership for fleet operators

- 3.11.4 Price erosion trends & commoditization risk

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Battery chemistry diversity & monitoring complexity

- 3.13.1 Lithium-ion chemistry variants

- 3.13.2 Solid-state battery monitoring challenges

- 3.14 Thermal management & thermal runaway prevention architecture

- 3.14.1 Thermal runaway mechanism & detection stages

- 3.14.2 Multi-point temperature sensing strategies

- 3.14.3 Thermal propagation monitoring & early warning systems

- 3.14.4 Active vs. Passive thermal management integration

- 3.15 V2G integration & battery wear accounting

- 3.15.1 ISO 15118-20 bidirectional power transfer protocol

- 3.15.2. Battery degradation mechanisms in V2 G operation

- 3.15.3. V2 G-specific SOH tracking & reporting

- 3.15.4 Grid service optimization algorithms

- 3.16 Second-life battery assessment & circular economy viability

- 3.16.1 End-of-first-life criteria & health thresholds

- 3.16.2 Second-life application suitability analysis

- 3.16.3 Health monitoring for second-life certification

- 3.17 Fleet telematics integration & total cost of ownership optimization

- 3.17.1 Fleet management platform architecture

- 3.17.2 Battery health monitoring for fleet tco reduction

- 3.17.3 Multi-vehicle battery health benchmarking

- 3.17.4 Fleet electrification roi modeling

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Lithium-ion

- 5.3 Lead-acid

- 5.4 NiMH

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 Light duty

- 7.3.2 Medium duty

- 7.3.3 Heavy duty

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Battery management systems

- 8.3 Monitoring & diagnostic

- 8.4 AI/ML & cloud-based analytics

- 8.5 Fleet telematics & remote monitoring

- 8.6 Aftermarket diagnostic solutions

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 First-life vehicle operation

- 9.3 Fleet management

- 9.4 Charging infrastructure integration

- 9.5 Vehicle-to-grid services

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Automotive OEMs

- 10.3 Fleet operators

- 10.4 Battery manufacturers & suppliers

- 10.5 Charging infrastructure providers

- 10.6 Aftermarket service providers

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Continental

- 12.1.2 LG Energy Solution

- 12.1.3 Panasonic

- 12.1.4 CATL

- 12.1.5 BYD

- 12.1.6 Analog Devices

- 12.1.7 Samsung SDI

- 12.1.8 Texas Instruments

- 12.1.9 Infineon

- 12.1.10 LEM International

- 12.2 Regional players

- 12.2.1 Samsara

- 12.2.2 Geotab

- 12.2.3 NXP Semiconductors

- 12.2.4 Denso

- 12.2.5 Valeo

- 12.2.6 Renesas Electronics

- 12.2.7 STMicroelectronics

- 12.3 Emerging Players:

- 12.3.1 Qnovo

- 12.3.2 Teltonika

- 12.3.3 Twaice Technologies

- 12.3.4 Breathe Battery Technologies

- 12.3.5 Voltaiq

- 12.3.6 Brill Power

医用电池市场:按化学成分、可充电类型、形状、技术、应用和最终用户划分-2026年至2032年全球预测

医用电池市场:按化学成分、可充电类型、形状、技术、应用和最终用户划分-2026年至2032年全球预测 2026年全球医用电池市场报告

2026年全球医用电池市场报告 电动车电池健康分析市场预测至2034年:按组件、电池类型、应用、最终用户和地区分類的全球分析

电动车电池健康分析市场预测至2034年:按组件、电池类型、应用、最终用户和地区分類的全球分析 无电池植入市场按植入类型、供电技术、植入部位、最终用户、病患小组、通路和地区划分

无电池植入市场按植入类型、供电技术、植入部位、最终用户、病患小组、通路和地区划分 全球医用电池市场:按类型、电池类型、应用、最终用户和地区划分 - 市场规模、行业趋势、机会分析和预测(2025-2033 年)

全球医用电池市场:按类型、电池类型、应用、最终用户和地区划分 - 市场规模、行业趋势、机会分析和预测(2025-2033 年) 电动汽车电池健康诊断系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测医疗电池市场按应用程式、电池类型、最终用户和地区划分

电动汽车电池健康诊断系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测医疗电池市场按应用程式、电池类型、最终用户和地区划分 全球医用电池市场:按产品、容量、应用、最终用户、地区划分 - 预测至 2029 年

全球医用电池市场:按产品、容量、应用、最终用户、地区划分 - 预测至 2029 年