|

市场调查报告书

商品编码

1892843

精品盐市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Gourmet Salts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

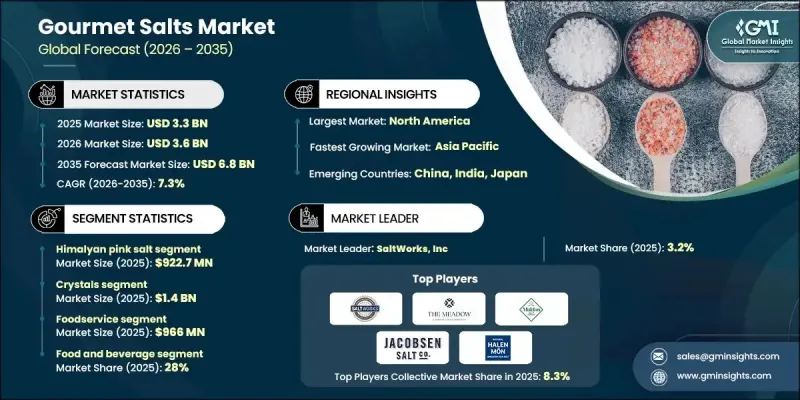

2025 年全球高级盐市场价值为 33 亿美元,预计到 2035 年将以 7.3% 的复合年增长率增长至 68 亿美元。

精品盐以其独特的矿物成分、色泽、质地和风味而着称,与普通食盐截然不同。这些盐通常含有天然微量矿物质或特定的结晶模式,从而提升口感和外观。许多精品盐产自特定的海洋环境、古老盐床或火山地区,赋予其独特的风土,如同特色食品或优质葡萄酒一般。采收、脱水和结晶製程的进步使生产商能够精确控制这些盐的颗粒大小、质地和品质。更先进的矿物分析技术和电子商务平台扩大了全球市场的覆盖范围,而从粗粒到细粒的不同质地也满足了各种烹饪需求。例如,片状盐能带来细腻的酥脆口感,因此在烹饪中常被用作点缀盐。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 33亿美元 |

| 预测值 | 68亿美元 |

| 复合年增长率 | 7.3% |

预计到2025年,喜马拉雅粉红盐市场规模将达到9.227亿美元。该市场涵盖多种盐类,包括海盐、片状盐和其他特色品种,这主要得益于消费者对天然、加工最少、富含矿物质的食材日益增长的需求。这些盐不仅因其口感和外观而备受青睐,更因其能够提升专业厨房和家庭厨房的整体烹饪体验而备受推崇。

预计到2025年,餐饮服务业市场规模将达9.66亿美元。餐厅和餐饮服务业的需求成长主要得益于厨师们对高品质食材的重视,他们致力于提升用餐体验。家庭消费者越来越多地使用高檔食盐进行烹饪和餐桌摆设,而化妆品和个人护理行业则将富含矿物质的食盐应用于沐浴和护肤产品中。广泛的应用领域支撑着市场的稳定成长和创新,而不断变化的消费者偏好和健康趋势也为其註入了动力。

预计到2025年,美国高檔食盐市场规模将达到10.7亿美元。北美消费者越来越青睐食盐,不仅因为其风味和美观,更因为其功能性益处。烟熏盐和风味盐因其能为日常菜餚增添层次感而广受欢迎,而富含矿物质的食盐则被广泛应用于健康产品中。专业零售商和线上商城的普及使得优质食盐触手可及,从而促进了市场成长并提升了市场知名度。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 消费者对天然产品的偏好日益增长

- 来自高端餐饮领域的需求

- 电子商务和零售通路的扩张

- 产业陷阱与挑战

- 品质和真实性问题

- 储存和保存期限问题

- 市场机会

- 产品创新和风味盐

- 永续环保的做法

- 拓展新兴市场

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2022-2035年

- 海盐

- 海盐之花

- 凯尔特灰盐(Sel Gris)

- 喜马拉雅粉红盐

- 片状盐

- 夏威夷盐(红/黑)

- 烟熏盐

- 黑盐(Kala Namak)

- 风味盐和浸泡盐

第六章:市场估算与预测:依产品形式划分,2022-2035年

- 晶体

- 薄片

- 粉末

第七章:市场估算与预测:依应用领域划分,2022-2035年

- 麵包糕点店

- 肉类和家禽产品

- 海鲜产品

- 酱汁和咸味小吃

- 食品加工

- 餐饮服务

- 家庭/零售

- 化妆品和个人护理

第八章:市场估算与预测:依最终用途产业划分,2022-2035年

- 食品饮料业

- 专业烹饪和高级餐饮

- 特种食品製造

- 饭店业

- 零售消费者

- 健康与保健

第九章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Alaska Pure Sea Salt Company

- Amagansett Sea Salt Co.

- Bitterman Salt Co.

- Brittany Sea Salt

- Celtic Sea Salt

- Cargill Inc. / Morton Salt

- Cheetham Salt Limited

- Gilles Hervy

- Halen Mon

- Infosa

- Jacobsen Salt Co.

- Le Guerandais

- Louis Sel

- Maldon Crystal Salt Company Ltd.

- Murray River Salt (Sun Salt Pty Ltd)

- Pyramid Salt (Sun Salt / Pyramid Hill)

- Redmond Real Salt (Redmond Life)

- SaltWorks, Inc.

- San Francisco Salt Company

- Sassi Salts

- The Meadow

- The Salt Table

The Global Gourmet Salts Market was valued at USD 3.3 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 6.8 billion by 2035.

Gourmet salts are distinguished by their unique mineral compositions, colors, textures, and flavors, setting them apart from standard table salt. These salts often contain natural trace minerals or specific crystallization patterns that enhance both taste and presentation. Many are sourced from specific marine environments, ancient salt beds, or volcanic regions, giving them a distinctive terroir, like specialty foods or fine wines. Technological advancements in harvesting, dehydration, and crystal formation have allowed producers to control the size, texture, and quality of these salts with precision. Enhanced mineral analysis and e-commerce platforms have expanded global access, while different textures from coarse to fine serve various culinary purposes. Flaky salts, for instance, provide a delicate crunch, making them highly sought after as finishing salts in culinary applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.3 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 7.3% |

The Himalayan pink salt segment generated USD 922.7 million in 2025. The market encompasses a wide range of salts, including sea salts, flake salts, and other specialty varieties, driven by rising consumer preference for natural, minimally processed, and mineral-rich ingredients. These salts are valued not only for their taste and visual appeal but also for enhancing the overall culinary experience in both professional and home kitchens.

The foodservice segment reached USD 966 million in 2025. Restaurants and catering services drive demand as chefs prioritize high-quality ingredients to elevate dining experiences. Household consumers are increasingly using gourmet salts for cooking and tabletop purposes, while the cosmetics and personal care industry leverages mineral-rich salts in bath and skincare products. The broad range of applications supports steady growth and innovation, fueled by changing consumer preferences and wellness trends.

U.S. Gourmet Salts Market garnered USD 1.07 billion in 2025. North American consumers are increasingly drawn to salts for their flavor, aesthetic appeal, and functional benefits. Smoked and flavored varieties are popular for adding complexity to everyday dishes, while mineral-enriched salts are incorporated into wellness products. Specialty retailers and online marketplaces make premium salts widely accessible, supporting market growth and visibility.

Key players in the Global Gourmet Salts Market include Redmond Real Salt (Redmond Life), SaltWorks, Inc., Murray River Salt (Sun Salt Pty Ltd), The Meadow, Alaska Pure Sea Salt Company, San Francisco Salt Company, Brittany Sea Salt, Sassi Salts, Le Guerandais, Halen Mon, Jacobsen Salt Co., Cargill Inc. / Morton Salt, Cheetham Salt Limited, The Salt Table, Louis Sel, Maldon Crystal Salt Company Ltd., Gilles Hervy, Amagansett Sea Salt Co., Celtic Sea Salt, and B Medical Systems. Market leaders focus on strategies such as expanding product lines with unique textures, flavors, and mineral compositions to meet diverse culinary and personal care demands. Companies invest in technological innovations in harvesting, drying, and crystallization to ensure consistent quality and enhance the sensory experience of their salts. Branding and storytelling around terroir, purity, and artisanal methods help differentiate offerings. Firms also leverage e-commerce platforms, social media campaigns, and partnerships with specialty retailers and restaurants to broaden reach and accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Physical form

- 2.2.3 Application

- 2.2.4 End Use industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer preference for natural products

- 3.2.1.2 Demand from premium culinary segments

- 3.2.1.3 Expansion of e-commerce and retail channels

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Quality and authenticity concerns

- 3.2.2.2 Storage and shelf-life issues

- 3.2.3 Market opportunities

- 3.2.3.1 Product innovation and flavored salts

- 3.2.3.2 Sustainable and eco-friendly practices

- 3.2.3.3 Expansion into emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Sea Salt

- 5.3 Fleur de Sel

- 5.4 Sel Gris (Celtic Grey Salt)

- 5.5 Himalayan Pink Salt

- 5.6 Flake Salt

- 5.7 Hawaiian Salt (Red/Black)

- 5.8 Smoked Salt

- 5.9 Black Salt (Kala Namak)

- 5.10 Flavored & Infused Salts

Chapter 6 Market Estimates and Forecast, By Product Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Crystals

- 6.3 Flakes

- 6.4 Powder

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery and confectionery

- 7.3 Meat and Poultry Products

- 7.4 Seafood products

- 7.5 Sauces and savories

- 7.6 Food processing

- 7.7 Foodservice

- 7.8 Household / retail

- 7.9 Cosmetics and personal care

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food and beverage industry

- 8.3 Professional culinary and fine dining

- 8.4 Specialty food manufacturing

- 8.5 Hospitality sector

- 8.6 Retail consumers

- 8.7 Health and wellness

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Alaska Pure Sea Salt Company

- 10.2 Amagansett Sea Salt Co.

- 10.3 Bitterman Salt Co.

- 10.4 Brittany Sea Salt

- 10.5 Celtic Sea Salt

- 10.6 Cargill Inc. / Morton Salt

- 10.7 Cheetham Salt Limited

- 10.8 Gilles Hervy

- 10.9 Halen Mon

- 10.10 Infosa

- 10.11 Jacobsen Salt Co.

- 10.12 Le Guerandais

- 10.13 Louis Sel

- 10.14 Maldon Crystal Salt Company Ltd.

- 10.15 Murray River Salt (Sun Salt Pty Ltd)

- 10.16 Pyramid Salt (Sun Salt / Pyramid Hill)

- 10.17 Redmond Real Salt (Redmond Life)

- 10.18 SaltWorks, Inc.

- 10.19 San Francisco Salt Company

- 10.20 Sassi Salts

- 10.21 The Meadow

- 10.22 The Salt Table