|

市场调查报告书

商品编码

1892850

汽车物流市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Automotive Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

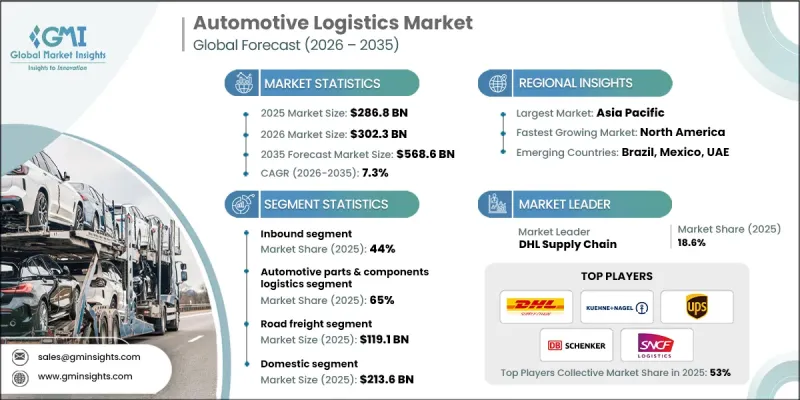

2025年全球汽车物流市场价值为2,868亿美元,预计到2035年将以7.3%的复合年增长率成长至5,686亿美元。

汽车产业的蓬勃发展,使得高效物流解决方案的需求日益增长,以满足供应链中车辆、零件的运输需求。企业逐渐意识到,能够优化运输路线、管理库存并提供即时货物追踪的软体至关重要。然而,许多汽车製造商仍然依赖过时的软体和传统系统进行物流管理,这使得现代解决方案的整合面临挑战,需要进行大量的资料迁移和客製化。此外,供应链端到端即时可见性有限、运输网路复杂以及合作伙伴之间资料透明度参差不齐,都构成了额外的障碍。为了应对这些挑战,软体供应商正在引入人工智慧和机器学习技术,以改善路线规划、自动化重复性任务并增强决策能力。预测分析和需求预测功能使企业能够预测未来需求、优化库存并更有效地分配资源,从而主动应对供应链中断。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 2868亿美元 |

| 预测值 | 5686亿美元 |

| 复合年增长率 | 7.3% |

预计到2025年,入库物流市场占有率将达到44%,并预计在2026年至2035年间以8%的复合年增长率成长。入库物流在汽车物流市场中扮演着至关重要的角色,它有效率地将原材料、零件和子组件从供应商运送到OEM组装厂。其高频次、大批量的营运确保了生产流程的顺畅,同时支援准时制(JIT)和准时排序(JIS)生产,从而降低库存持有成本。采用包括公路、铁路、航空和海运多模式方式,进一步提升了入库供应链的速度、可靠性和成本效益。

2025年,汽车零件物流领域占据了65%的市场份额,预计2026年至2035年将以7.6%的复合年增长率成长。该领域占据主导地位的原因在于,零件在整车製造商(OEM)以及一级和二级供应商网路中的流动具有复杂性、数量庞大且频率高。它确保零件能够安全、及时、经济高效地送达组装厂、区域配送中心和售后服务网络,从而维持生产的顺利进行和运作。

中国汽车物流市场占39%的市场份额,预计2025年市场规模将达432亿美元。中国市场的领先地位主要得益于汽车产量的快速成长、乘用车和商用车的强劲需求以及对先进物流技术的大规模投资。该地区拥有完善的交通网络、广泛的仓储和配送基础设施,并且数位化供应链解决方案、基于物联网的追踪系统和自动化物料搬运系统等技术的应用日益普及,这些都为其市场发展提供了有利条件。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 全球汽车产量成长及售后市场扩张

- 采用数位化和智慧物流技术

- 电动车製造和电池物流的成长

- 全球化供应链与跨境贸易的扩张

- 产业陷阱与挑战

- 供应链中断与产能瓶颈

- 电动车零件运作成本高且处理复杂

- 市场机会

- 对永续和绿色物流的需求日益增长

- 售后市场电子商务分销的快速成长

- 先进技术的融合

- 新兴市场的扩张

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 美国联邦汽车运输安全管理局 (FMCSA)、美国国家公路交通安全管理局 (NHTSA)、美国环保署 (EPA) 排放标准

- 加拿大运输部安全法规

- 欧洲

- 德国欧盟车辆安全法规,TUV认证

- 法国国家科学研究中心排放与安全标准

- 英国车辆安全与合规部门

- 义大利交通部车辆法规

- 亚太地区

- 中国交通部交通安全法规、新能源汽车政策

- 日本JAMA车辆安全法规、排放标准

- 韩国产业通商资源部安全与环境合规

- 印度汽车产业标准 (AIS)

- 拉丁美洲

- CONTRAN车辆安全与排放规则

- NOM汽车安全标准

- 中东和非洲

- 阿联酋标准化与计量局车辆法规

- SASO车辆安全与环境标准

- 北美洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 使用案例场景

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依服务类型划分,2022-2035年

- 入境物流

- 出站

- 反向

- 售后市场

第六章:市场估算与预测:依产品划分,2022-2035年

- 成品车

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型

- 中型

- 重负

- 搭乘用车

- 汽车零件

- 车轮和轮胎

- 电气和电子

- 车身和底盘

- 悬吊和转向系统

- 煞车系统

- 引擎和动力系统

第七章:市场估计与预测:依运输方式划分,2022-2035年

- 公路货运

- 海运

- 空运

- 铁路货运

第八章:市场估算与预测:依通路划分,2022-2035年

- 国内的

- 国际的

第九章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Global Player

- CH Robinson Worldwide

- CEVA Logistics

- DHL Supply Chain & Global Forwarding

- DSV-Schenker

- Expeditors International of Washington

- GEODIS (SNCF)

- Hellmann Worldwide Logistics

- Kuehne+Nagel International

- Penske Logistics

- XPO Logistics

- Regional Player

- BLG Logistics

- Hyundai Glovis

- Kintetsu World Express

- Mosolf

- Nippon Express

- Schnellecke Logistics

- Toll

- Yusen Logistics

- 新兴参与者

- Flexport

- FourKites

- Hodlmayr International

- project44

- Uber Freight

The Global Automotive Logistics Market was valued at USD 286.8 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 568.6 billion by 2035.

The expanding automotive industry has increased the need for efficient logistics solutions to transport vehicles, parts, and components across the supply chain. Companies are recognizing the importance of software that can optimize transportation routes, manage inventory, and provide real-time shipment tracking. Many automakers still rely on outdated software and legacy systems for logistics management, which makes integration of modern solutions challenging, requiring extensive data migration and customization. Limited real-time visibility into the end-to-end supply chain, complex transportation networks, and varying data transparency among partners pose additional hurdles. To address these challenges, software providers are incorporating AI and machine learning to improve route planning, automate repetitive tasks, and enhance decision-making. Predictive analytics and demand forecasting capabilities allow companies to anticipate future demand, optimize inventory, and allocate resources more efficiently, enabling proactive solutions to supply chain disruptions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $286.8 Billion |

| Forecast Value | $568.6 Billion |

| CAGR | 7.3% |

The inbound logistics segment held a 44% share in 2025 and is projected to grow at a CAGR of 8% between 2026 and 2035. Inbound logistics plays a critical role in the automotive logistics market by efficiently transporting raw materials, components, and subassemblies from suppliers to OEM assembly plants. Its high-frequency, high-volume operations ensure smooth production flows while supporting just-in-time (JIT) and just-in-sequence (JIS) manufacturing, reducing inventory carrying costs. The use of multimodal transportation, including road, rail, air, and sea, further enhances the speed, reliability, and cost-efficiency of inbound supply chains.

The automotive parts and components logistics segment accounted for a 65% share in 2025 and is expected to grow at a CAGR of 7.6% from 2026 to 2035. This segment dominates due to the complexity, volume, and frequency of part movements across OEMs and Tier-1 and Tier-2 supplier networks. It ensures that parts are delivered securely, on time, and cost-effectively to assembly plants, regional distribution centers, and aftermarket service networks, maintaining seamless production and operations.

China Automotive Logistics Market held a 39% share, generating USD 43.2 billion in 2025. China's dominance is driven by rapid growth in vehicle production, strong demand for passenger and commercial vehicles, and large-scale investments in advanced logistics technologies. The region benefits from well-developed transportation networks, extensive warehousing and distribution infrastructure, and rising adoption of digital supply chain solutions, IoT-based tracking, and automated material handling systems.

Key players in the Global Automotive Logistics Market include Bosch Service Solutions GmbH, Basware Oy, Blue Yonder, SAP SE, Kinaxis, Inc., Infor Corporation, Oracle Corporation, Ceres Technology Inc., and Manhattan Associates, Inc. Companies in the Global Automotive Logistics Market are strengthening their position by investing in AI and ML integration to enhance predictive capabilities and operational efficiency. They are prioritizing cloud-based platforms to offer scalable and flexible solutions that meet evolving customer demands. Strategic partnerships with technology providers and industry stakeholders help expand market reach and ensure seamless software integration. Firms are also focusing on continuous R&D to innovate features such as real-time tracking, advanced analytics, and automated workflow management, creating a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Product

- 2.2.4 Mode of Transportation

- 2.2.5 Distribution

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production & aftermarket expansion

- 3.2.1.2 Adoption of digital & intelligent logistics technologies

- 3.2.1.3 Growth of EV manufacturing & battery logistics

- 3.2.1.4 Expansion of globalized supply chains & cross-border trade

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions & capacity bottlenecks

- 3.2.2.2 High operational costs & complexity of handling EV components

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for sustainable & green logistics

- 3.2.3.2 Rapid growth in aftermarket e-commerce distribution

- 3.2.3.3 Integration of advanced technologies

- 3.2.3.4 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 FMCSA, NHTSA, EPA Emissions Standards

- 3.4.1.2 Transport Canada Safety Regulations

- 3.4.2 Europe

- 3.4.2.1 Germany EU Vehicle Safety Regulations, TUV Certification

- 3.4.2.2 France CNRS Emissions & Safety Standards

- 3.4.2.3 United Kingdom DVSA Vehicle Safety & Compliance

- 3.4.2.4 Italy Ministry of Transport Vehicle Regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China Ministry of Transport Safety Rules, NEV Policies

- 3.4.3.2 Japan JAMA Vehicle Safety Regulations, Emission Standards

- 3.4.3.3 South Korea MOTIE Safety & Environmental Compliance

- 3.4.3.4 India AIS (Automotive Industry Standards)

- 3.4.4 Latin America

- 3.4.4.1 CONTRAN Vehicle Safety & Emission Rules

- 3.4.4.2 NOM Automotive Safety Standards

- 3.4.5 Middle East and Africa

- 3.4.5.1 Emirates Authority for Standardization & Metrology Vehicle Regulations

- 3.4.5.2 SASO Vehicle Safety & Environmental Standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($ Bn, TEU)

- 5.1 Key trends

- 5.2 Inbound Logistics

- 5.3 Outbound

- 5.4 Reverse

- 5.5 Aftermarket

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($ Bn, TEU)

- 6.1 Key trends

- 6.2 Finished Vehicle

- 6.2.1 Passenger car

- 6.2.1.1 Hatchback

- 6.2.1.2 Sedan

- 6.2.1.3 SUV

- 6.2.2 Commercial vehicle

- 6.2.2.1 Light duty

- 6.2.2.2 Medium duty

- 6.2.2.3 Heavy duty

- 6.2.1 Passenger car

- 6.3 Automotive Parts & Components

- 6.3.1 Wheels and tires

- 6.3.2 Electrical and electronic

- 6.3.3 Body and chassis

- 6.3.4 Suspension and steering

- 6.3.5 Braking system

- 6.3.6 Engine and powertrain

Chapter 7 Market Estimates & Forecast, By Mode of Transportation, 2022 - 2035 ($ Bn, TEU)

- 7.1 Key trends

- 7.2 Road Freight

- 7.3 Sea Freight

- 7.4 Air Freight

- 7.5 Rail Freight

Chapter 8 Market Estimates & Forecast, By Distribution, 2022 - 2035 ($ Bn, TEU)

- 8.1 Key trends

- 8.2 Domestic

- 8.3 International

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, TEU)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global Player

- 10.1.1 C.H. Robinson Worldwide

- 10.1.2 CEVA Logistics

- 10.1.3 DHL Supply Chain & Global Forwarding

- 10.1.4 DSV-Schenker

- 10.1.5 Expeditors International of Washington

- 10.1.6 GEODIS (SNCF)

- 10.1.7 Hellmann Worldwide Logistics

- 10.1.8 Kuehne+Nagel International

- 10.1.9 Penske Logistics

- 10.1.10 XPO Logistics

- 10.2 Regional Player

- 10.2.1 BLG Logistics

- 10.2.2 Hyundai Glovis

- 10.2.3 Kintetsu World Express

- 10.2.4 Mosolf

- 10.2.5 Nippon Express

- 10.2.6 Schnellecke Logistics

- 10.2.7 Toll

- 10.2.8 Yusen Logistics

- 10.3 Emerging Players

- 10.3.1 Flexport

- 10.3.2 FourKites

- 10.3.3 Hodlmayr International

- 10.3.4 project44

- 10.3.5 Uber Freight

成品车物流市场:依运输方式、服务类型、所有权类型、设备类型及最终用户划分-2026-2032年全球市场预测汽车OEM厂内物流市场:依零件、服务模式、自动化程度、物流方式、汽车零件类型及最终用户划分-2026-2032年全球市场预测电动物流车辆马达市场(按马达类型、额定功率、车辆类型、应用和最终用户产业划分)-全球预测,2026-2032年

成品车物流市场:依运输方式、服务类型、所有权类型、设备类型及最终用户划分-2026-2032年全球市场预测汽车OEM厂内物流市场:依零件、服务模式、自动化程度、物流方式、汽车零件类型及最终用户划分-2026-2032年全球市场预测电动物流车辆马达市场(按马达类型、额定功率、车辆类型、应用和最终用户产业划分)-全球预测,2026-2032年 全球汽车物流市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车物流市场规模、份额、趋势和成长分析报告(2026-2034) 汽车物流市场规模、份额、趋势及预测(按类型、活动、运输方式、物流解决方案、分销和地区划分),2026-2034年

汽车物流市场规模、份额、趋势及预测(按类型、活动、运输方式、物流解决方案、分销和地区划分),2026-2034年 2026-2030年全球汽车OEM厂商厂内物流市场

2026-2030年全球汽车OEM厂商厂内物流市场 欧洲汽车物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲汽车物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 工厂内物流自动化:全球市场份额和排名、总收入和需求预测(2025-2031 年)按类型、操作类型、控制模式、容量、安装类型、应用、最终用途产业和分销管道分類的厂内升降机市场 - 2025-2030 年全球预测

工厂内物流自动化:全球市场份额和排名、总收入和需求预测(2025-2031 年)按类型、操作类型、控制模式、容量、安装类型、应用、最终用途产业和分销管道分類的厂内升降机市场 - 2025-2030 年全球预测 汽车物流市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、解决方案、模式

汽车物流市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、解决方案、模式