|

市场调查报告书

商品编码

1906159

欧洲汽车物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

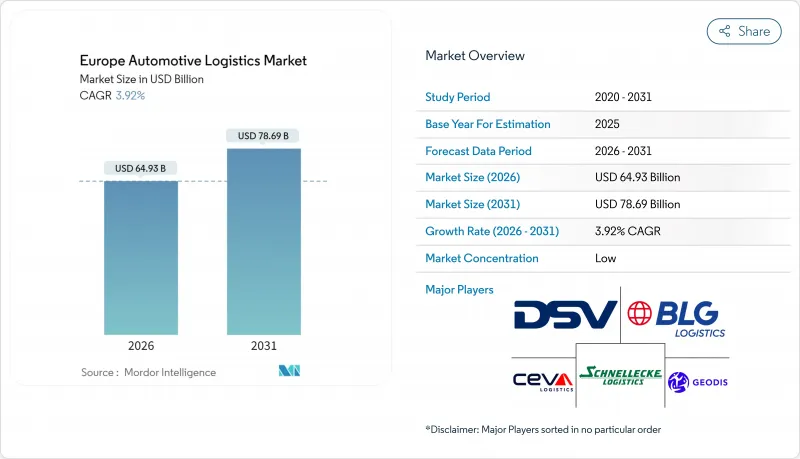

欧洲汽车物流市场预计到 2026 年将达到 649.3 亿美元,高于 2025 年的 624.8 亿美元。

预计到 2031 年将达到 786.9 亿美元,2026 年至 2031 年的复合年增长率为 3.92%。

随着原始设备製造商 (OEM)、第三方物流 (3PL) 营运商和技术专家围绕电气化、数位化协作和严格的脱碳要求重组其网络,这一前景逐渐显现。儘管运输服务仍然重要,但对温控电池物流和高频电商组件供应的快速需求正促使投资转向增值能力。整合的 3PL/4PL伙伴关係、多模态优化和自动化应用正在提高营运韧性,而公路和铁路运力限制则继续限制利润率的提升。德国是区域收入的基础,而波兰仓储业的蓬勃发展凸显了一种地域格局的重新平衡,这种平衡有利于拥有泛欧业务的灵活供应商。

欧洲汽车物流市场趋势与洞察

OEM製造商越来越多地将业务外包给整合的3PL/4PL专业公司

欧洲汽车製造商正越来越多地将端到端物流外包给兼具实体和数位化能力的策略合作伙伴。大众汽车和宝马汽车正在深化与供应商签订的多年期合同,这些供应商能够协调零件入库管理、工厂准时交付以及整车跨境运输。德迅集团和DHL供应链正在积极回应,扩展其“汽车解决方案中心”,整合运输规划、控制塔分析和永续发展报告。 ISO 14001和IATF 16949认证提高了行业标准,促使企业更加关注那些拥有品质和环境资质的供应商。欧洲汽车物流市场正受惠于汽车製造商将资金从资产所有权转向电气化研发,从而将物流创新交给专业公司。外包还能透过变动成本合约和灵活调整规模以应对需求高峰和低谷来缓衝生产波动。

由于电动车产量快速成长,对温控电池物流的需求日益增长。

匈牙利、德国和波兰的超级工厂集群正在加速对温度控制在摄氏15至25度之间的温控供应链的需求,以保护锂离子电池的完整性。 DHL在义大利和英国的电动车专业中心提供配备灭火系统、符合ADR标准的包装和即时温度监控系统的专用仓储设施。物流业者正在投资隔热交换车厢、电动穿梭车和冗余电源,以确保跨境运输过程中的温度稳定性。这导致欧洲汽车物流市场资本投资激增,包括专用车辆资产和仓库维修,这些投资价格不菲。宁德时代等电池製造商正在利用区域服务中心扩大对入库和出库流程的直接控制,以缩短运输时间并维持保固标准。

欧洲公路和铁路货运面临司机短缺和运力不足的问题

在德国,超过8万名专业驾驶员的缺口正对汽车物流的即时交付模式带来巨大压力,并推高薪资成本。年轻人对长途驾驶工作的低迷加剧了离职率,而基础设施建设和以乘客为先的政策也给铁路货运能力带来了压力。物流公司正透过发放留任奖金、实施弹性工作制和引入自动驾驶场内牵引车来维持服务水准。运力波动导致欧洲汽车物流市场出现溢价和现货运费波动。汽车製造商正努力透过增加安全库存缓衝和在工厂附近实施越库作业转运来降低交货风险。

细分市场分析

到2025年,货运将占欧洲汽车物流市场61.35%的份额,这主要得益于道路运输的柔软性,能够满足严格的准时制生产週期。同时,随着碳定价推动运输方式的重新平衡,铁路和短程海运在长途运输的重要性日益凸显。附加价值服务虽然规模较小,但在2026年至2031年间,其复合年增长率将达到3.52%,这主要得益于交货前检验、电动车电池维护和控制塔协调等服务的成长。供应商正透过机器人驱动的越库作业数位双胞胎来优化服务组合,从而提高车辆停留时间和堆场容量。到2031年,在公路货运价格持续承压的情况下,附加价值服务将有助于稳定利润率,并巩固供应商作为欧洲汽车物流市场整合合作伙伴的地位。

仓储业正经历同步成长,自动化提高了多品种零件库存的吞吐量。 ISO 9001 和 IATF 16949 认证正成为供应商选择的标准,确保了收货、生产线定序和售后补货的可追溯性。智慧货架、AGV 车队和 RFID 扫描等技术的运用缩短了週期时间,进一步推动了欧洲汽车物流市场在核心运输之外的服务层面的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- OEM製造商越来越多地将业务外包给整合的3PL/4PL专业公司

- 随着电动车产量激增,对温控电池物流的需求日益增长。

- 售后服务电子商务推动了小批量、高频率的物流发展。

- 欧盟绿色交易奖励促进多式联运和二氧化碳减排

- 半导体和软体定义汽车组件创造了新的高附加价值流程

- 区域电池回收走廊的出现(从原始设备製造商到超级工厂的反向循环)

- 市场限制

- 欧洲公路和铁路货运面临司机和运力短缺问题

- 燃料和人事费用上涨给利润率带来压力。

- 滚装船短缺导致成品车港口拥挤

- 互联物流平台中的网路安全漏洞

- 价值/供应链分析

- 监管环境(政府法规和政策)

- 技术展望(自动化、物联网、人工智慧、区块链)

- 专题报导-电子商务对汽车物流的影响

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治事件的影响

第五章 市场规模与成长预测

- 透过服务

- 运输

- 路

- 铁路

- 航空

- 海上/滚装/近岸

- 仓储、配送和库存管理

- 附加价值服务

- 运输

- 按类型

- OEM

- 售后市场

- 按货物类型

- 已完成的汽车

- 汽车零件

- 电动汽车电池和电力电子

- 其他货物

- 按国家/地区

- 德国

- 西班牙

- 法国

- 义大利

- 波兰

- 英国

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- BLG Logistics

- CEVA Logistics AG

- DSV

- Schnellecke Logistics

- GEODIS

- Nippon Express Co., Ltd

- XPO Logistics, Inc.

- DHL Supply Chain

- Kuehne+Nagel

- Hellmann Worldwide Logistics

- Wallenius Wilhelmsen Logistics

- Yusen Logistics

- CAT Group

- FIEGE Automotive

- Ryder System, Inc.

- Rohlig Logistics

- Rhenus Logistics

- Scan Global Logistics

- LOGISTEED Europe BV

- TOP AUTO Logistik GmbH

第七章 市场机会与未来展望

Europe Automotive Logistics Market size in 2026 is estimated at USD 64.93 billion, growing from 2025 value of USD 62.48 billion with 2031 projections showing USD 78.69 billion, growing at 3.92% CAGR over 2026-2031.

The outlook emerges as OEMs, 3PLs, and technology specialists reshape networks around electrification, digital orchestration, and rigorous decarbonization mandates. Transportation services remain pivotal, yet rapid demand for temperature-controlled battery flows and high-frequency e-commerce parts fulfillment is refocusing investment toward value-added capabilities. Integrated 3PL/4PL partnerships, multimodal optimization, and automation adoption drive operational resilience while capacity constraints in road and rail continue to temper margin expansion. Germany anchors regional revenue, but Poland's warehouse boom underscores a geographic rebalancing that rewards agile providers with pan-European reach.

Europe Automotive Logistics Market Trends and Insights

OEMs' Rising Outsourcing to Integrated 3PL/4PL Specialists

European manufacturers increasingly channel end-to-end logistics to strategic partners that fuse physical and digital competencies. Volkswagen and BMW deepen multi-year agreements with providers capable of orchestrating inbound parts, just-in-sequence plant deliveries, and outbound finished-vehicle distribution across borders. Kuehne+Nagel and DHL Supply Chain answer by expanding Automotive Solution Centers that unify transport planning, control-tower analytics, and sustainability reporting. Certifications under ISO 14001 and IATF 16949 elevate selection thresholds, directing share toward providers with quality and environmental credentials. The Europe automotive logistics market benefits as OEM capital shifts from asset ownership to electrification R&D, leaving logistics innovation to specialized experts. Outsourcing also buffers production volatility by allowing variable-cost contracts that scale with demand peaks and troughs.

Surge in EV Production Requiring Temperature-Controlled Battery Logistics

Gigafactory clusters in Hungary, Germany, and Poland accelerate demand for 15-25 °C controlled supply chains that safeguard lithium-ion cell integrity. DHL's EV Centers of Excellence in Italy and the UK showcase purpose-built storage with fire-suppression systems, ADR-compliant packaging, and real-time thermal monitoring. Logistics providers invest in insulated swap bodies, electric shuttles, and redundant power backup to guarantee temperature stability during cross-border transits. The Europe automotive logistics market thus funnels capex into specialized fleet assets and warehouse retrofits that command premium pricing. Battery OEMs such as CATL extend direct control over inbound and reverse flows, leveraging in-region service hubs to curtail transit time and uphold warranty standards.

Driver & Capacity Shortages in European Road/Rail Freight

A deficit exceeding 80,000 professional drivers in Germany strains just-in-time automotive flows and inflates wage costs. Low appeal of long-haul careers among younger cohorts compounds attrition, while infrastructure works and passenger priority squeeze rail freight slots. Logistics firms adopt retention bonuses, flexible scheduling, and autonomous yard tractors to sustain service levels. The Europe automotive logistics market experiences spot-rate volatility as capacity swings trigger premium surcharges. OEMs respond by increasing safety-stock buffers and exploring cross-docking near plants to dampen schedule risk.

Other drivers and restraints analyzed in the detailed report include:

- After-Sales E-Commerce Boosting Small-Lot, High-Frequency Flows

- EU Green Deal Incentives for Multimodal Freight & CO2 Cuts

- Rising Fuel and Labor Costs Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for a 61.35% share of the Europe automotive logistics market in 2025, anchored by road haulage flexibility that meets stringent just-in-sequence production cadences. Rail and short-sea alternatives gain relevance on longer corridors as carbon pricing steers modal recalibration. Meanwhile, value-added services, though smaller, are expanding at a 3.52% CAGR (2026-2031), driven by pre-delivery inspection, EV battery conditioning, and control-tower orchestration. Providers elevate service mix through robotics-enabled cross-docks and digital twins that optimize dwell time and yard capacity. By 2031, value-added offerings will underpin margin resilience as commoditized line-haul rates remain under pressure, thereby entrenching integrated partners across the Europe automotive logistics market.

A parallel upswing is visible in warehousing, where automation increases throughput for multi-SKU part inventories. ISO 9001 and IATF 16949 certifications govern provider selection, ensuring traceability across inbound, line-side sequencing, and aftermarket replenishment. Smart racking, AGV fleets, and RFID scanning compress cycle times, reinforcing the Europe automotive logistics market size growth trajectory for service layers beyond core transport.

The Europe Automotive Logistics Market Report is Segmented by Service (Transportation, Warehousing, Distribution & Inventory Management, and Value-Added Services), Type (OEM and Aftermarket), Cargo Type (Finished Vehicles, Auto Components, EV Batteries & Power-Electronics, and Other Cargo), Country (Germany, Spain, France, Italy, United Kingdom, Poland, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- BLG Logistics

- CEVA Logistics AG

- DSV

- Schnellecke Logistics

- GEODIS

- Nippon Express Co., Ltd

- XPO Logistics, Inc.

- DHL Supply Chain

- Kuehne + Nagel

- Hellmann Worldwide Logistics

- Wallenius Wilhelmsen Logistics

- Yusen Logistics

- CAT Group

- FIEGE Automotive

- Ryder System, Inc.

- Rohlig Logistics

- Rhenus Logistics

- Scan Global Logistics

- LOGISTEED Europe B.V.

- TOP AUTO Logistik GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OEMs' rising outsourcing to integrated 3PL/4PL specialists

- 4.2.2 Surge in EV production requiring temperature-controlled battery logistics

- 4.2.3 After-sales e-commerce boosting small-lot, high-frequency flows

- 4.2.4 EU Green Deal incentives for multimodal freight & CO2 cuts

- 4.2.5 Semiconductor & software-defined vehicle parts creating new high-value flows

- 4.2.6 Emergence of regional battery-recycling corridors (OEM-to-gigafactory reverse loops)

- 4.3 Market Restraints

- 4.3.1 Driver & capacity shortages in European road/rail freight

- 4.3.2 Rising fuel and labor costs squeezing margins

- 4.3.3 Ro-Ro vessel scarcity causing port congestion for finished vehicles

- 4.3.4 Cyber-security vulnerabilities in connected logistics platforms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (Government Regulations & Initiatives)

- 4.6 Technological Outlook (Automation, IoT, AI, Blockchain)

- 4.7 Spotlight - E-commerce Impact on Automotive Logistics

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Impact of Geo-Political Events

5 Market Size & Growth Forecasts

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea / Ro-Ro / Short-Sea

- 5.1.2 Warehousing, Distribution & Inventory Management

- 5.1.3 Value-added Services

- 5.1.1 Transportation

- 5.2 By Type

- 5.2.1 OEM

- 5.2.2 Aftermarket

- 5.3 By Cargo Type

- 5.3.1 Finished Vehicles

- 5.3.2 Auto Components

- 5.3.3 EV Batteries and Power-Electronics

- 5.3.4 Other Cargo

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 Spain

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Poland

- 5.4.6 United Kingdom

- 5.4.7 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.8 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 BLG Logistics

- 6.4.2 CEVA Logistics AG

- 6.4.3 DSV

- 6.4.4 Schnellecke Logistics

- 6.4.5 GEODIS

- 6.4.6 Nippon Express Co., Ltd

- 6.4.7 XPO Logistics, Inc.

- 6.4.8 DHL Supply Chain

- 6.4.9 Kuehne + Nagel

- 6.4.10 Hellmann Worldwide Logistics

- 6.4.11 Wallenius Wilhelmsen Logistics

- 6.4.12 Yusen Logistics

- 6.4.13 CAT Group

- 6.4.14 FIEGE Automotive

- 6.4.15 Ryder System, Inc.

- 6.4.16 Rohlig Logistics

- 6.4.17 Rhenus Logistics

- 6.4.18 Scan Global Logistics

- 6.4.19 LOGISTEED Europe B.V.

- 6.4.20 TOP AUTO Logistik GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

成品车物流市场:依运输方式、服务类型、所有权类型、设备类型及最终用户划分-2026-2032年全球市场预测汽车OEM厂内物流市场:依零件、服务模式、自动化程度、物流方式、汽车零件类型及最终用户划分-2026-2032年全球市场预测电动物流车辆马达市场(按马达类型、额定功率、车辆类型、应用和最终用户产业划分)-全球预测,2026-2032年

成品车物流市场:依运输方式、服务类型、所有权类型、设备类型及最终用户划分-2026-2032年全球市场预测汽车OEM厂内物流市场:依零件、服务模式、自动化程度、物流方式、汽车零件类型及最终用户划分-2026-2032年全球市场预测电动物流车辆马达市场(按马达类型、额定功率、车辆类型、应用和最终用户产业划分)-全球预测,2026-2032年 全球汽车物流市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车物流市场规模、份额、趋势和成长分析报告(2026-2034) 汽车物流市场规模、份额、趋势及预测(按类型、活动、运输方式、物流解决方案、分销和地区划分),2026-2034年

汽车物流市场规模、份额、趋势及预测(按类型、活动、运输方式、物流解决方案、分销和地区划分),2026-2034年 2026-2030年全球汽车OEM厂商厂内物流市场

2026-2030年全球汽车OEM厂商厂内物流市场 汽车物流市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

汽车物流市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 工厂内物流自动化:全球市场份额和排名、总收入和需求预测(2025-2031 年)按类型、操作类型、控制模式、容量、安装类型、应用、最终用途产业和分销管道分類的厂内升降机市场 - 2025-2030 年全球预测

工厂内物流自动化:全球市场份额和排名、总收入和需求预测(2025-2031 年)按类型、操作类型、控制模式、容量、安装类型、应用、最终用途产业和分销管道分類的厂内升降机市场 - 2025-2030 年全球预测 汽车物流市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、解决方案、模式

汽车物流市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、解决方案、模式