|

市场调查报告书

商品编码

1892852

资料中心伺服器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Data Center Server Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

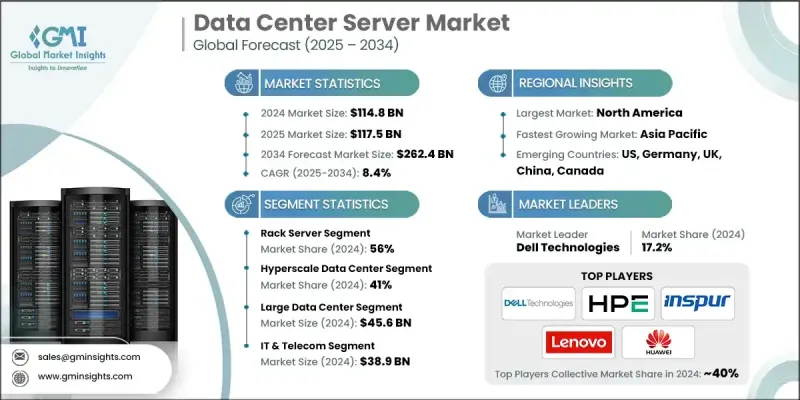

2024 年全球资料中心伺服器市场价值为 1,148 亿美元,预计到 2034 年将以 8.4% 的复合年增长率成长至 2,624 亿美元。

随着人工智慧工作负载的不断扩展,运算需求也在改变。大型语言模型训练、推理操作和加速分析越来越依赖高效能GPU和专用伺服器架构。市场对能够支援这些密集型任务的先进系统的需求正在迅速增长,这促使资料中心采用GPU密集型配置,而这些配置的冷却和电力需求远高于传统部署。同时,互联设备、企业平台、工业自动化系统和行动应用产生的资料规模日益庞大,也促使企业升级并扩展其运算基础设施。电信、银行、金融服务和保险(BFSI)、零售和医疗保健等行业需要处理海量信息,而这些信息需要能够支援即时分析的快速、可靠的伺服器。随着企业对过时的IT环境进行现代化改造,并持续向混合云和多云模式转型,可扩展的伺服器系统对于维持业务营运中的数位转型、自动化和资料密集型应用至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1148亿美元 |

| 预测值 | 2624亿美元 |

| 复合年增长率 | 8.4% |

2024年,机架式伺服器市占率达到56%,预计到2034年将以8.8%的复合年增长率成长。机架式系统使营运商能够在标准化机架内高效扩展容量,同时保持高运算密度和运维灵活性。其模组化设计与目前的云端部署相契合,使其成为企业和超大规模资料中心的首选基础架构。

超大规模资料中心在2024年占据了41%的市场份额,预计在2025年至2034年间将以9.1%的复合年增长率成长。超大规模营运商部署大型GPU丛集来支援包括推荐引擎、LLM训练和视觉模型在内的高阶工作负载。这些环境需要高密度的机架式运算资源,并配备先进的网路和散热管理系统,因此机架式伺服器成为支撑超大规模成长的主要架构。

2024年,美国资料中心伺服器市场规模达499亿美元。美国拥有全球最密集的超大规模资料中心,这得益于主要云端服务供应商及其不断扩展的AI驱动型运算丛集。这些大规模部署每年消耗大量的机架式伺服器,巩固了美国在该地区的领先地位。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 半导体及元件供应商

- 伺服器OEM厂商

- 冷却、机架基础设施和电源供应商

- 资料中心营运商

- 云端平台和服务供应商

- 最终用途

- 成本结构

- 利润率

- 每个阶段的价值增加

- 影响供应链的因素

- 颠覆者

- 供应商格局

- 对力的影响

- 成长驱动因素

- 云端运算和超大规模扩展的快速成长

- 人工智慧、机器学习和高效能运算(HPC)的爆炸性成长

- 各行业资料产生量不断增加

- 边缘运算在低延迟应用中的成长

- 产业陷阱与挑战

- 电力和散热方面的限制制约了高密度伺服器部署。

- 能源成本上涨对总体拥有成本和伺服器更新决策带来压力。

- 供应链波动和半导体短缺导致伺服器出货延迟。

- 市场机会

- 加速采用人工智慧最佳化和GPU加速伺服器

- 边缘运算的成长开启了新的伺服器部署空间

- 过渡到液冷散热会带来硬体升级週期。

- ARM架构伺服器及其他架构的兴起

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术趋势与创新生态系统

- 目前技术

- 基于 x86 的伺服器架构

- 用于人工智慧/高效能运算的GPU加速运算系统

- 传统风冷结合先进的气流管理

- 虚拟化与虚拟机器管理程式平台

- 新兴技术

- 基于 CXL 的解耦式可组合基础设施

- 用于人工智慧集群的硅光子学和光互连

- 可持续且节能的伺服器设计

- AI驱动的自主资料中心营运与优化

- 目前技术

- 专利分析

- 价格趋势分析

- 按地区

- 副产品

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 成本細項分析

- 风险分析与管理

- 营运风险评估

- 财务风险评估

- 技术与网路安全风险

- 风险缓解策略

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 用例

- 最佳情况

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依伺服器划分,2021-2034年

- 架子

- 塔

- 刀刃

- 微

- GPU加速

第六章:市场估算与预测:依资料中心划分,2021-2034年

- 企业

- 託管

- 超大规模

- 边缘

第七章:市场估算与预测:依资料中心规模划分,2021-2034年

- 小型资料中心

- 中型资料中心

- 大型资料中心

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 资讯科技与电信

- 金融服务业

- 政府与国防

- 卫生保健

- 零售与电子商务

- 製造业

- 其他的

第九章:市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 泰国

- 印尼

- 新加坡

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Global Leaders

- Cisco Systems

- Dell Technologies

- Fujitsu

- Hewlett Packard Enterprise (HPE)

- Huawei

- IBM

- Inspur Power Systems

- Lenovo

- Oracle

- Sugon

- Supermicro

- Wiwynn

- 区域冠军

- Atos

- Canovate Elektronik

- NEC

- OVHcloud

- Penguin Computing

- Quanta Cloud Technology

- Tyan Computer

- ZT Systems

- 新兴参与者

- Broadberry Data Systems

- Jabil

- Oxide Computer Company

The Global Data Center Server Market was valued at USD 114.8 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 262.4 billion by 2034.

Expanding AI workloads are reshaping compute requirements, as large language model training, inference operations, and accelerated analytics increasingly rely on high-performance GPU and specialized server architectures. Demand is rising rapidly for advanced systems built to support these intensive tasks, pushing data centers to adopt GPU-rich configurations with far higher cooling and power needs than traditional deployments. At the same time, the growing scale of data generated by connected devices, enterprise platforms, industrial automation systems, and mobile applications is prompting organizations to upgrade and expand their compute infrastructure. Industries such as telecom, BFSI, retail, and healthcare process enormous volumes of information that require fast, reliable servers capable of supporting real-time analytics. As companies modernize outdated IT environments and continue shifting toward hybrid and multi-cloud models, scalable server systems become essential to sustaining digital transformation, automation, and data-heavy applications across business operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $114.8 Billion |

| Forecast Value | $262.4 Billion |

| CAGR | 8.4% |

The rack server segment held a 56% share in 2024 and is expected to grow at an 8.8% CAGR through 2034. Rack-mounted systems allow operators to scale capacity efficiently within standardized racks while maintaining high compute density and operational flexibility. Their modularity aligns with current cloud deployments, making them the preferred infrastructure choice across enterprises and hyperscale facilities.

The hyperscale data center category held a 41% share in 2024 and is projected to grow at a CAGR of 9.1% between 2025 and 2034. Hyperscale operators deploy large GPU clusters to power advanced workloads, including recommendation engines, LLM training, and vision models. These environments require dense rack-based computes with advanced networking and thermal management, positioning rack servers as the primary architecture supporting hyperscale growth.

U.S. Data Center Server Market generated USD 49.9 billion in 2024. The country hosts the most extensive concentration of hyperscale facilities worldwide, supported by major cloud providers and their continuous expansion of AI-driven compute clusters. These large deployments consume vast numbers of rack servers each year, strengthening the country's leadership in the region.

Leading companies in the Global Data Center Server Market include Dell Technologies, HPE, Inspur Power Systems, Lenovo, Huawei, Supermicro, Cisco Systems, Fujitsu, IBM, and Sugon. To strengthen their presence in the Data Center Server Market, companies are prioritizing several key strategies. Many are expanding their portfolios with GPU-dense and AI-optimized server platforms designed to support high-performance computing and accelerated workloads. Partnerships with cloud providers, semiconductor manufacturers, and hyperscale operators help streamline integration of next-generation processors, networking, and cooling technologies. Firms are also investing heavily in energy-efficient architecture, liquid cooling, and modular designs that address rising power density challenges. Global manufacturing expansion and supply chain diversification ensure consistent delivery at hyperscale volumes. Additionally, companies are enhancing software-defined capabilities, automation tools, and infrastructure management platforms to deliver full-stack solutions that support modern cloud and hybrid environments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Server

- 2.2.3 Data Center

- 2.2.4 Data Center Size

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Semiconductor & component suppliers

- 3.1.1.2 Server OEMs

- 3.1.1.3 Cooling, rack infrastructure & power delivery vendors

- 3.1.1.4 Data center operators

- 3.1.1.5 Cloud platforms & service providers

- 3.1.1.6 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid growth of cloud computing & hyperscale expansion

- 3.2.1.2 Explosion of AI, machine learning & high-performance computing (HPC)

- 3.2.1.3 Increasing data generation across industries

- 3.2.1.4 Growth of edge computing for low-latency applications

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Power & cooling constraints limit high-density server deployments

- 3.2.2.2 Rising energy costs pressure TCO and server refresh decisions

- 3.2.2.3 Supply chain volatility and semiconductor shortages delay server shipments

- 3.2.3 Market opportunities

- 3.2.3.1 Accelerated adoption of AI-optimized and GPU-accelerated servers

- 3.2.3.2 Growth of edge computing opens new server deployment footprints

- 3.2.3.3 Transition to liquid cooling creates hardware upgrade cycles

- 3.2.3.4 Rise of ARM-based servers and alternative architectures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology trends & innovation ecosystem

- 3.7.1 Current technologies

- 3.7.1.1 x86-based server architectures

- 3.7.1.2 GPU-accelerated compute systems for AI/HPC

- 3.7.1.3 Traditional air-cooling with advanced airflow management

- 3.7.1.4 Virtualization & hypervisor platforms

- 3.7.2 Emerging technologies

- 3.7.2.1 CXL-based disaggregated & composable infrastructure

- 3.7.2.2 Silicon photonics & optical interconnects for AI clusters

- 3.7.2.3 Sustainable & energy-efficient server designs

- 3.7.2.4 AI-driven autonomous data center operations & optimization

- 3.7.1 Current technologies

- 3.8 Patent analysis

- 3.9 Price trend analysis

- 3.9.1 By region

- 3.9.2 By Products

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Risk analysis & management

- 3.12.1 Operational risk assessment

- 3.12.2 Financial risk evaluation

- 3.12.3 Technology & cybersecurity risks

- 3.12.4 Risk mitigation strategies

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Use cases

- 3.15 Best case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Server, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Rack

- 5.3 Tower

- 5.4 Blade

- 5.5 Micro

- 5.6 GPU/Accelerated

Chapter 6 Market Estimates & Forecast, By Data Center, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Enterprise

- 6.3 Colocation

- 6.4 Hyperscale

- 6.5 Edge

Chapter 7 Market Estimates & Forecast, By Data Center Size, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Small data centers

- 7.3 Medium data center

- 7.4 Large data center

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 IT & Telecom

- 8.3 BFSI

- 8.4 Government & Defense

- 8.5 Healthcare

- 8.6 Retail & E-commerce

- 8.7 Manufacturing

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Benelux

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Thailand

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Leaders

- 10.1.1 Cisco Systems

- 10.1.2 Dell Technologies

- 10.1.3 Fujitsu

- 10.1.4 Hewlett Packard Enterprise (HPE)

- 10.1.5 Huawei

- 10.1.6 IBM

- 10.1.7 Inspur Power Systems

- 10.1.8 Lenovo

- 10.1.9 Oracle

- 10.1.10 Sugon

- 10.1.11 Supermicro

- 10.1.12 Wiwynn

- 10.2 Regional Champions

- 10.2.1 Atos

- 10.2.2 Canovate Elektronik

- 10.2.3 NEC

- 10.2.4 OVHcloud

- 10.2.5 Penguin Computing

- 10.2.6 Quanta Cloud Technology

- 10.2.7 Tyan Computer

- 10.2.8 ZT Systems

- 10.3 Emerging Players

- 10.3.1 Broadberry Data Systems

- 10.3.2 Jabil

- 10.3.3 Oxide Computer Company

2026年全球资料中心伺服器市场报告

2026年全球资料中心伺服器市场报告 风冷伺服器市场:依伺服器类型、部署类型、冷却类型、最终用户和通路划分,全球预测,2026-2032年

风冷伺服器市场:依伺服器类型、部署类型、冷却类型、最终用户和通路划分,全球预测,2026-2032年 资料中心伺服器市场规模、份额和成长分析(按组件、类型、设计、公司规模、层级和地区划分)-2026-2033年产业预测

资料中心伺服器市场规模、份额和成长分析(按组件、类型、设计、公司规模、层级和地区划分)-2026-2033年产业预测 资料中心智慧推理伺服器:全球市场份额和排名、总收入和需求预测(2025-2031 年)

资料中心智慧推理伺服器:全球市场份额和排名、总收入和需求预测(2025-2031 年) CPX和Rubin的整合:全球伺服器的GDDR7

CPX和Rubin的整合:全球伺服器的GDDR7 2025-2029年全球资料中心与伺服器市场全球资料中心伺服器市场:2034 年的机会与策略

2025-2029年全球资料中心与伺服器市场全球资料中心伺服器市场:2034 年的机会与策略 日本资料中心伺服器市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

日本资料中心伺服器市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 全球资料中心伺服器市场、市场规模和占有率分析:依类型和应用分类 - 收入估算和需求预测(截至 2030 年)

全球资料中心伺服器市场、市场规模和占有率分析:依类型和应用分类 - 收入估算和需求预测(截至 2030 年)