|

市场调查报告书

商品编码

1892918

汽车感测器市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Automotive Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

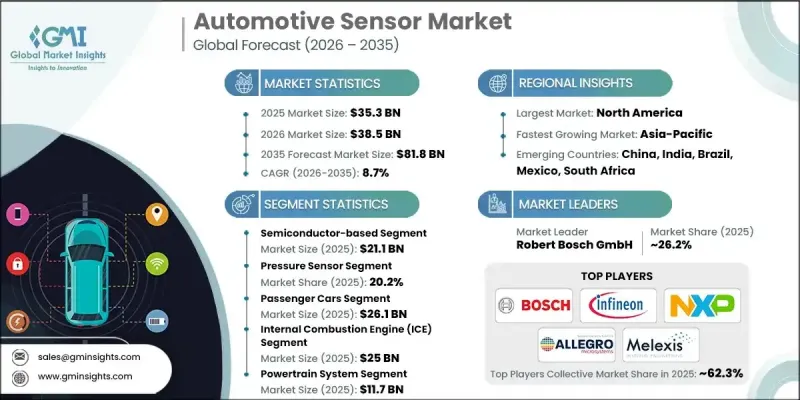

2025年全球汽车感测器市场价值为353亿美元,预计到2035年将以8.7%的复合年增长率成长至818亿美元。

市场成长的驱动力来自先进驾驶辅助系统(ADAS) 的日益普及、互联自动驾驶汽车的日益流行,以及能够提升安全性、效率和整体车辆性能的智慧感测器的部署。自适应巡航控制、车道偏离预警、自动煞车和盲点监测等功能推动了雷达、光达、摄影机和超音波感测器的集成,从而实现即时态势感知。此外,向电动车的转型也带动了对用于管理电池性能、热调节、马达控制和能源效率的感测器的需求。政府为促进安全、减少排放和提高燃油效率而製定的强制性规定,进一步加速了各细分市场感测器的应用。电动车产量的成长和清洁交通诱因也促进了全球市场的成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 353亿美元 |

| 预测值 | 818亿美元 |

| 复合年增长率 | 8.7% |

预计到2024年,半导体感测器市场规模将达211亿美元。这些感测器精度高、可靠性强,并且能够在单一晶片上整合多种功能。它们结构紧凑、功耗低、成本效益高,并且与先进的汽车电子设备相容,使其成为电动车、自动驾驶汽车和智慧网联汽车不可或缺的组件。这些感测器广泛应用于高阶驾驶辅助系统(ADAS)、动力系统、电池管理、资讯娱乐系统和安全系统等领域,在全球市场保持强劲的需求。

预计到2025年,压力感测器市场规模将达到71亿美元。其广泛应用源自于引擎管理、变速箱系统、轮胎压力监测、煞车系统和电动车电池管理等领域。对车辆安全、法规遵循、排放控制和燃油效率的日益重视,持续推动全球乘用车和商用车对这类感测器的需求。

预计到2025年,北美汽车感测器市场份额将达到37.1%。该地区的领先地位归功于其强大的汽车製造业基础、对先进汽车技术的早期应用以及对安全性、燃油效率和排放合规车辆日益增长的需求。对电气化、连网汽车和自动驾驶解决方案的日益重视推动了高级驾驶辅助系统(ADAS)和动力总成系统中感测器的部署。此外,严格的政府法规和消费者对创新汽车技术的偏好也巩固了北美在全球市场的领先地位。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 电动车和自动驾驶汽车的普及

- 严格的安全和排放法规

- 消费者对提升车内体验的需求

- 技术进步和成本降低

- 高级驾驶辅助系统(ADAS)的需求不断增长

- 产业陷阱与挑战

- 高昂的开发和生产成本

- 整合和相容性问题的复杂性

- 市场机会

- 电动车(EV)的扩张

- 高级驾驶辅助系统(ADAS)和自动驾驶汽车

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴商业模式

- 合规要求

- 永续性措施

- 消费者情绪分析

- 专利和智慧财产权分析

- 地缘政治与贸易动态

第四章:竞争格局

- 公司市占率分析简介

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 市场集中度分析

- 主要参与者的竞争基准化分析

- 财务绩效比较

- 收入

- 利润率

- 研发

- 产品组合比较

- 产品范围广度

- 科技

- 创新

- 地理分布比较

- 全球足迹分析

- 服务网路覆盖范围

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导人

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2022-2025 年主要发展动态

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/新创企业竞争对手格局

第五章:市场估算与预测:依感测器类型划分,2022-2035年

- 压力感测器

- 燃油轨道压力感知器

- 歧管绝对压力(MAP)感知器

- 差压感知器(GPF/DPF)

- 轮胎压力监测感知器

- 煞车压力感知器

- 其他的

- 气体感测器

- 颗粒物(PM)感测器

- 氮氧化物(NOx)感测器

- 氧气(λ)感测器

- 二氧化碳感测器

- 碳氢化合物(HC)感测器

- 其他的

- 温度感测器

- 排气温度(EGT)感知器

- 引擎冷却液温度感知器

- 电池温度感测器(电动车)

- 环境温度感测器

- 油温感知器

- 其他的

- 电流和电压感测器

- 电池电流感测器(电动车)

- 电池电压感测器(电动车)

- 高压联锁迴路(HVIL)感测器

- 充电电流感测器

- 其他的

- 位置和速度感测器

- 凸轮轴位置感知器

- 曲轴位置感知器

- 车轮速度感测器

- 转向角传感器

- 节气门位置感知器

- 其他的

- 光学感测器

- 相机/影像感光元件

- 光达感测器

- 红外线感测器

- 雨量/光线感应器

- 其他的

- 雷达感测器

- 24 GHz 雷达感测器

- 77 GHz 雷达感测器

- 79 GHz 雷达感测器

- 其他的

- 超音波感测器

- 停车辅助感应器

- 人体感应感应器

- 其他的

- 惯性感测器

- 加速度计

- 陀螺仪

- 惯性测量单元(IMU)

- 其他的

- 其他的

第六章:市场估算与预测:依技术划分,2022-2035年

- 基于半导体的感测器

- 硅基感测器

- 陶瓷基感测器

- 微机电系统(MEMS)

- 磁性感应器

- 霍尔效应感测器

- 磁阻感测器

- 光学感测器

- 电化学感测器

第七章:市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 小型车

- 中型轿车

- 豪华轿车

- SUV

- 轻型商用车

- 重型商用车辆

- 中型卡车

- 重型卡车

- 公车

第八章:市场估算与预测:依推进类型划分,2022-2035年

- 内燃机(ICE)

- 汽油

- 柴油引擎

- 替代燃料(压缩天然气、液化石油气)

- 电动车

- 混合动力电动车(HEV)

- 插电式混合动力电动车(PHEV)

- 电池电动车(BEV)

- 燃料电池电动车(FCEV)

第九章:市场估算与预测:依应用领域划分,2022-2035年

- 动力总成系统

- 引擎管理系统

- 变速箱控制系统

- 燃油输送系统

- 废气后处理系统

- 电气化系统

- 电池管理系统

- 马达控制系统

- 充电系统

- 热管理系统(电动车)

- 高压安全系统

- 安全与ADAS系统

- 防碰撞系统

- 车道维持辅助系统

- 自适应巡航控制系统

- 停车辅助系统

- 盲点侦测系统

- 车身及底盘系统

- 转向系统

- 悬吊系统

- 煞车系统

- 气候控制系统

- 照明系统

- 舒适便利系统

- 资讯娱乐系统

- 座椅控制系统

- 门禁系统

- 其他的

第十章:市场估价与预测:依销售管道划分,2022-2035年

- 原始设备製造商(OEM)

- 售后市场

第十一章:市场估计与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十二章:公司简介

- Allegro MicroSystems LLC

- Analog Devices Inc.

- Aptiv PLC

- BorgWarner Inc.

- Continental AG

- Denso Corporation

- First Sensor AG

- Hitachi Astemo Americas Inc.

- Honeywell International Inc.

- Infineon Technologies AG

- Melexis NV

- Microchip Technology Inc.

- NXP Semiconductors

- OMNIVISION Technologies Inc.

- ON Semiconductor

- Panasonic Corporation

- Renesas Electronics Corporation

- Robert Bosch GmbH

- Sensata Technologies Inc.

- STMicroelectronics NV

- TE Connectivity Ltd.

- Valeo SA

The Global Automotive Sensor Market was valued at USD 35.3 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 81.8 billion by 2035.

The market's growth is fueled by the rising adoption of advanced driver assistance systems (ADAS), the increasing popularity of connected and autonomous vehicles, and the deployment of smart sensors that enhance safety, efficiency, and overall vehicle performance. Features such as adaptive cruise control, lane departure warning, automatic braking, and blind-spot monitoring are driving the integration of radar, lidar, camera, and ultrasonic sensors, enabling real-time situational awareness. Additionally, the transition to electric vehicles is supporting demand for sensors that manage battery performance, thermal regulation, motor control, and energy efficiency. Government mandates promoting safety, emission reduction, and fuel efficiency further accelerate sensor adoption across all vehicle segments. Rising production of EVs and incentives for cleaner transportation are also contributing to market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $35.3 Billion |

| Forecast Value | $81.8 Billion |

| CAGR | 8.7% |

The semiconductor-based sensors segment reached USD 21.1 billion in 2024. These sensors are highly accurate, reliable, and capable of integrating multiple functions on a single chip. Their compact design, low power requirements, cost-effectiveness, and compatibility with advanced automotive electronics make them indispensable in electric, autonomous, and connected vehicles. They are widely utilized across ADAS, powertrain, battery management, infotainment, and safety systems, sustaining strong demand across global markets.

The pressure sensor segment was valued at USD 7.1 billion in 2025. Their widespread adoption stems from applications in engine management, transmission systems, tire pressure monitoring, braking systems, and electric vehicle battery management. Rising emphasis on vehicle safety, regulatory compliance, emission control, and fuel efficiency continues to drive demand for these sensors across passenger and commercial vehicles worldwide.

North America Automotive Sensor Market held a 37.1% share in 2025. The region's dominance is attributed to its strong automotive manufacturing base, early adoption of advanced vehicle technologies, and increasing demand for safety, fuel efficiency, and emission-compliant vehicles. Growing focus on electrification, connected vehicles, and autonomous driving solutions has driven sensor deployment in ADAS and powertrain systems. Additionally, stringent government regulations and consumer preference for innovative automotive technologies support North America's leadership in the global market.

Key players operating in Global Automotive Sensor Market include Infineon Technologies AG, Denso Corporation, Panasonic Corporation, Melexis NV, Analog Devices Inc., Microchip Technology Inc., TE Connectivity Ltd., NXP Semiconductors, Honeywell International Inc., Allegro MicroSystems LLC, Renesas Electronics Corporation, Robert Bosch GmbH, BorgWarner Inc., ON Semiconductor, Aptiv PLC, Hitachi Astemo Americas Inc., Continental AG, Sensata Technologies Inc., First Sensor AG, Valeo SA, STMicroelectronics NV, and OMNIVISION Technologies Inc. Companies in the Global Automotive Sensor Market are employing diverse strategies to strengthen their presence and expand their market foothold. They are investing heavily in research and development to deliver innovative, high-precision sensors for ADAS, autonomous, and electric vehicles. Strategic partnerships, mergers, and acquisitions are being pursued to expand technological capabilities, geographic reach, and production capacity. Firms are also focusing on product differentiation through miniaturization, multi-function integration, and energy-efficient designs. Additionally, companies are enhancing customer support, providing software-enabled solutions, and targeting emerging markets to capture growth opportunities, strengthen distribution networks, and maintain a competitive edge in the rapidly evolving automotive sensor landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Sensor type trends

- 2.2.3 Technology type trends

- 2.2.4 Vehicle type trends

- 2.2.5 Propulsion type trends

- 2.2.6 Application trends

- 2.2.7 Sales channel trends

- 2.2.8 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO Perspectives: Strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical Success Factors

- 2.7 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Proliferation of electric and autonomous vehicles

- 3.2.1.2 Stringent safety and emission regulations

- 3.2.1.3 Consumer demand for enhanced in-vehicle experience

- 3.2.1.4 Technological advancements and cost reduction

- 3.2.1.5 Increasing Demand for Advanced Driver Assistance Systems (ADAS)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and production costs

- 3.2.2.2 Complexity of integration and compatibility issues

- 3.2.3 Market Opportunities

- 3.2.3.1 Expansion of Electric Vehicles (EVs)

- 3.2.3.2 Advanced Driver Assistance Systems (ADAS) and Autonomous Vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technological and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price Trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.13 Consumer sentiment analysis

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction Company market share analysis

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1. North America

- 4.2.2. Europe

- 4.2.3. Asia Pacific

- 4.2.2 Market concentration analysis

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1. Revenue

- 4.3.1.2. Profit Margin

- 4.3.1.3. R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1. Product Range Breadth

- 4.3.2.2. Technology

- 4.3.2.3. Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1. Global Footprint Analysis

- 4.3.3.2. Service Network Coverage

- 4.3.3.3. Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1. Leaders

- 4.3.4.2. Challengers

- 4.3.4.3. Followers

- 4.3.4.4. Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Sensor Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Pressure Sensors

- 5.2.1 Fuel Rail Pressure Sensors

- 5.2.2 Manifold Absolute Pressure (MAP) Sensors

- 5.2.3 Differential Pressure Sensors (GPF/DPF)

- 5.2.4 Tire Pressure Monitoring Sensors

- 5.2.5 Brake Pressure Sensors

- 5.2.6 Others

- 5.3 Gas Sensors

- 5.3.1 Particulate Matter (PM) Sensors

- 5.3.2 NOx (Nitrogen Oxide) Sensors

- 5.3.3 Oxygen (Lambda) Sensors

- 5.3.4 CO2 Sensors

- 5.3.5 Hydrocarbon (HC) Sensors

- 5.3.6 Others

- 5.4 Temperature Sensors

- 5.4.1 Exhaust Gas Temperature (EGT) Sensors

- 5.4.2 Engine Coolant Temperature Sensors

- 5.4.3 Battery Temperature Sensors (EV)

- 5.4.4 Ambient Temperature Sensors

- 5.4.5 Oil Temperature Sensors

- 5.4.6 Others

- 5.5 Current & Voltage Sensors

- 5.5.1 Battery Current Sensors (EV)

- 5.5.2 Battery Voltage Sensors (EV)

- 5.5.3 High Voltage Interlock Loop (HVIL) Sensors

- 5.5.4 Charging Current Sensors

- 5.5.5 Others

- 5.6 Position & Speed Sensors

- 5.6.1 Camshaft Position Sensors

- 5.6.2 Crankshaft Position Sensors

- 5.6.3 Wheel Speed Sensors

- 5.6.4 Steering Angle Sensors

- 5.6.5 Throttle Position Sensors

- 5.6.6 Others

- 5.7 Optical Sensors

- 5.7.1 Camera/Image Sensors

- 5.7.2 LiDAR Sensors

- 5.7.3 Infrared Sensors

- 5.7.4 Rain/Light Sensors

- 5.7.5 Others

- 5.8 Radar Sensors

- 5.8.1 24 GHz Radar Sensors

- 5.8.2 77 GHz Radar Sensors

- 5.8.3 79 GHz Radar Sensors

- 5.8.4 Others

- 5.9 Ultrasonic Sensors

- 5.9.1 Parking Assistance Sensors

- 5.9.2 Occupancy Detection Sensors

- 5.9.3 Others

- 5.10 Inertial Sensors

- 5.10.1 Accelerometers

- 5.10.2 Gyroscopes

- 5.10.3 Inertial Measurement Units (IMU)

- 5.10.4 Others

- 5.11 Others

Chapter 6 Market estimates & forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Semiconductor-based Sensors

- 6.2.1 Silicon-based Sensors

- 6.2.2 Ceramic-based Sensors

- 6.3 MEMS (Micro-Electro-Mechanical Systems)

- 6.4 Magnetic Sensors

- 6.4.1 Hall-Effect Sensors

- 6.4.2 Magneto-Resistive Sensors

- 6.5 Optical Sensors

- 6.6 Electrochemical Sensors

Chapter 7 Market estimates & forecast, By Vehicle Type, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Compact Cars

- 7.2.2 Mid-size Cars

- 7.2.3 Luxury Cars

- 7.2.4 SUVs

- 7.3 Light Commercial Vehicles

- 7.4 Heavy Commercial Vehicles

- 7.4.1 Medium-duty Trucks

- 7.4.2 Heavy-duty Trucks

- 7.4.3 Buses

Chapter 8 Market estimates & forecast, By Propulsion Type, 2022-2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Internal Combustion Engine (ICE)

- 8.1.1 Gasoline

- 8.1.2 Diesel

- 8.3 Alternative Fuels (CNG, LPG)

- 8.1.3 Electrified Vehicles

- 8.1.4 Hybrid Electric Vehicle (HEV)

- 8.1.5 Plug-in Hybrid Electric Vehicle (PHEV)

- 8.1.6 Battery Electric Vehicle (BEV)

- 8.1.7 Fuel Cell Electric Vehicle (FCEV)

Chapter 9 Market estimates & forecast, By Application, 2022-2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Powertrain Systems

- 9.2.1 Engine Management Systems

- 9.2.2 Transmission Control Systems

- 9.2.3 Fuel Delivery Systems

- 9.2.4 Emissions After-treatment Systems

- 9.3 Electrification Systems

- 9.3.1 Battery Management Systems

- 9.3.2 Electric Motor Control Systems

- 9.3.3 Charging Systems

- 9.3.4 Thermal Management Systems (EV)

- 9.3.5 High Voltage Safety Systems

- 9.4 Safety & ADAS Systems

- 9.4.1 Collision Avoidance Systems

- 9.4.2 Lane Keeping Assistance Systems

- 9.4.3 Adaptive Cruise Control Systems

- 9.4.4 Parking Assistance Systems

- 9.4.5 Blind Spot Detection Systems

- 9.5 Body & Chassis Systems

- 9.5.1 Steering Systems

- 9.5.2 Suspension Systems

- 9.5.3 Braking Systems

- 9.5.4 Climate Control Systems

- 9.5.5 Lighting Systems

- 9.6 Comfort & Convenience Systems

- 9.6.1 Infotainment Systems

- 9.6.2 Seat Control Systems

- 9.6.3 Access Control Systems

- 9.6.4 Others

Chapter 10 Market estimates & forecast, By Sales channel, 2022-2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 Original Equipment Manufacturer (OEM)

- 10.3 Aftermarket

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 U.K.

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East & Africa

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profile

- 12.1 Allegro MicroSystems LLC

- 12.2 Analog Devices Inc.

- 12.3 Aptiv PLC

- 12.4 BorgWarner Inc.

- 12.5 Continental AG

- 12.6 Denso Corporation

- 12.7 First Sensor AG

- 12.8 Hitachi Astemo Americas Inc.

- 12.9 Honeywell International Inc.

- 12.10 Infineon Technologies AG

- 12.11 Melexis NV

- 12.12 Microchip Technology Inc.

- 12.13 NXP Semiconductors

- 12.14 OMNIVISION Technologies Inc.

- 12.15 ON Semiconductor

- 12.16 Panasonic Corporation

- 12.17 Renesas Electronics Corporation

- 12.18 Robert Bosch GmbH

- 12.19 Sensata Technologies Inc.

- 12.20 STMicroelectronics NV

- 12.21 TE Connectivity Ltd.

- 12.22 Valeo SA

汽车光束感测器市场:按组件、感测器类型、技术、车辆类型、应用和销售管道划分-2026-2032年全球预测

汽车光束感测器市场:按组件、感测器类型、技术、车辆类型、应用和销售管道划分-2026-2032年全球预测 2026-2034年全球汽车感测器市场规模、份额、趋势和成长分析报告

2026-2034年全球汽车感测器市场规模、份额、趋势和成长分析报告 2026年全球汽车感测器市场报告数位汽车超音波感测器市场按安装类型、换能器类型、运作频率、车辆类型和应用划分-全球预测,2026-2032年汽车电流感测器:2026-2032年全球市场预测(按感测器类型、应用、车辆类型、技术和最终用户划分)

2026年全球汽车感测器市场报告数位汽车超音波感测器市场按安装类型、换能器类型、运作频率、车辆类型和应用划分-全球预测,2026-2032年汽车电流感测器:2026-2032年全球市场预测(按感测器类型、应用、车辆类型、技术和最终用户划分) 全球下一代自动驾驶安全系统市场:未来预测(至2032年)-按系统类型、车辆类型、最终用户和地区分類的分析

全球下一代自动驾驶安全系统市场:未来预测(至2032年)-按系统类型、车辆类型、最终用户和地区分類的分析 日本汽车感测器市场报告(按类型、车辆类型、应用、销售管道(原厂配套、售后市场)和地区划分,2026-2034年)

日本汽车感测器市场报告(按类型、车辆类型、应用、销售管道(原厂配套、售后市场)和地区划分,2026-2034年) 汽车主动安全感测器市场规模、份额和成长分析(按车辆类型、应用、感测器类型和地区划分)—2026-2033年产业预测

汽车主动安全感测器市场规模、份额和成长分析(按车辆类型、应用、感测器类型和地区划分)—2026-2033年产业预测 轮胎感测器市场规模、份额及成长分析(按产品类型、销售管道、车辆类型及地区划分)-2026-2033年产业预测

轮胎感测器市场规模、份额及成长分析(按产品类型、销售管道、车辆类型及地区划分)-2026-2033年产业预测 汽车惯性测量单元(IMU)市场规模、份额和成长分析(按技术、应用和地区划分)-2026-2033年产业预测

汽车惯性测量单元(IMU)市场规模、份额和成长分析(按技术、应用和地区划分)-2026-2033年产业预测