|

市场调查报告书

商品编码

1913353

铅酸蓄电池回收市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Lead Acid Battery Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球铅酸电池回收市场预计到 2025 年将达到 132 亿美元,到 2035 年将达到 313 亿美元,年复合成长率为 9.1%。

加速推进电气化以及铅酸电池在交通运输、储能和工业系统中日益广泛的应用,正在推动这一成长。铅酸电池回收是指系统性地收集和处理废弃电池,以回收铅、塑胶零件和电解等可再利用材料的过程。这种做法有助于提高资源利用效率,降低环境风险,并符合全球永续性目标。回收过程在减少污染、确保安全处置废弃物以及满足不断变化的合规要求方面发挥关键作用。电池消费量的成长以及日益严格的环境监管,正在加速全球回收工作的发展。各国政府和监管机构正在加强系统化的电池废弃物管理,建立支持市场长期成长的框架,并促进多个终端用户产业采用循环经济模式。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 132亿美元 |

| 预测金额 | 313亿美元 |

| 复合年增长率 | 9.1% |

铅酸电池在车辆、备用电源系统和工业基础设施的应用日益广泛,导致其回收量显着增长。随着储能需求的不断扩大,回收已成为材料供应链的关键环节,有助于减少对原生资源的依赖。以环境保护和材料回收为重点的法规结构持续鼓励製造商和回收商推广负责任的电池报废管理实践。

预计到2025年,湿式冶金回收将占据59.4%的市场份额,并在2035年之前以9.2%的复合年增长率成长。与其他回收製程相比,此方法排放更低、废弃物产生量更少、能耗更低,因此正日益受到青睐。它能够在实现高纯度金属回收的同时,帮助企业满足环境法规的要求,使其成为注重永续营运的回收企业的重要技术选择。

预计到2025年,SLI细分市场将占据71.8%的市场份额,并在2026年至2035年间以9%的复合年增长率成长。汽车产业的持续需求和稳定的换代週期支撑着稳定的回收量。日益严格的电池处置环境法规进一步推动了该应用领域负责任的回收方法和材料再利用。

北美铅酸电池回收市场占全球市场的 92.3%,预计到 2035 年将成长至 43 亿美元。更严格的环境法规、不断增长的储能需求以及对降低铅暴露相关健康风险的日益重视,都推动了先进回收方法的发展和运营效率的提高。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系统

- 原物料供应及采购分析

- 製造能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 成本结构分析

- 波特五力分析

- PESTEL 分析

- 新的机会与趋势

- 数位化和物联网集成

- 拓展新兴市场

- 投资分析及未来展望

第四章 竞争情势

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

- 战略仪錶板

- 策略倡议

- 企业标竿管理

- 创新与科技趋势

第五章 依製程分類的市场规模及预测(2022-2035年)

- 火法冶金

- 湿式冶金

- 物理/机械

第六章 依应用领域分類的市场规模及预测(2022-2035年)

- SLI

- 固定式

- 其他的

第七章 2022-2035年各地区市场规模及预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 西班牙

- 德国

- 法国

- 亚太地区

- 中国

- 韩国

- 日本

- 印度

- 世界其他地区

第八章 公司简介

- Amara Raja

- Aqua Metals

- Battery Recyclers of America

- BPL Nigeria Limited

- Cirba Solutions

- Clarios

- Doe Run Company

- East Penn Manufacturing Company

- Ecobat

- EnerSys

- Engitec Technologies

- Exide Technologies

- Glencore

- GME Recycling

- Gopher Resource LLC

- Gravita India

- Interstate Batteries

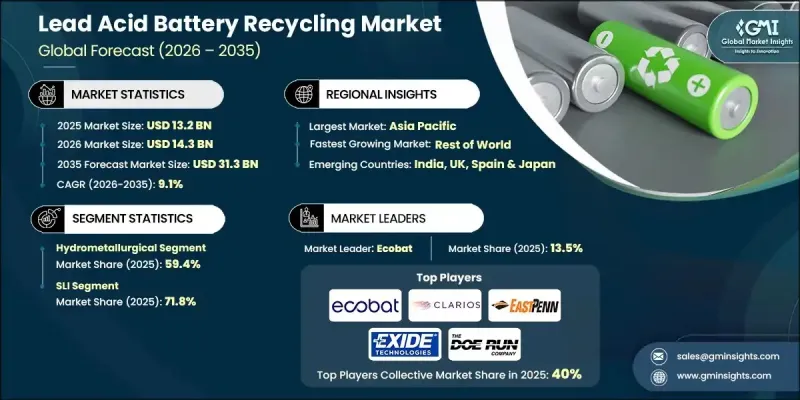

The Global Lead Acid Battery Recycling Market was valued at USD 13.2 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 31.3 billion by 2035.

Rising electrification trends and the increasing use of lead acid batteries across transportation, energy storage, and industrial systems drive this growth. Lead acid battery recycling involves the systematic collection and processing of spent batteries to recover reusable materials such as lead, plastic components, and electrolyte solutions. This approach supports resource efficiency, reduces environmental risks, and aligns with global sustainability objectives. The recycling process plays a critical role in reducing pollution, ensuring safe waste handling, and meeting evolving compliance requirements. Growing battery consumption, combined with stronger environmental oversight, is accelerating recycling activity worldwide. Governments and regulatory bodies are reinforcing structured battery waste management practices, creating a supportive framework for long-term market growth and encouraging circular economy adoption across multiple end-use industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.2 Billion |

| Forecast Value | $31.3 Billion |

| CAGR | 9.1% |

Rising deployment of lead-acid batteries in vehicles, power backup systems, and industrial infrastructure is significantly increasing recycling volumes. As energy storage demand grows, recycling is becoming an essential component of material supply chains, helping reduce dependency on newly mined resources. Regulatory frameworks focused on environmental protection and material recovery continue to push manufacturers and recyclers toward responsible end-of-life battery management practices.

The hydrometallurgical recycling segment held 59.4% share in 2025 and is projected to grow at a CAGR of 9.2% through 2035. This method is gaining preference due to its lower emissions, reduced waste generation, and lower energy requirements when compared to alternative recycling processes. Its ability to deliver high-purity metal recovery while supporting environmental compliance has made it a key technology choice for recyclers focused on sustainable operations.

The SLI segment held a 71.8% share in 2025 and is expected to grow at a CAGR of 9% from 2026 to 2035. Continued demand from the automotive sector and steady replacement cycles are supporting consistent recycling volumes. Strengthening environmental rules surrounding battery disposal is further reinforcing responsible recovery practices and material reuse for this application segment.

North America Lead Acid Battery Recycling Market held 92.3% share and is projected to generate USD 4.3 billion by 2035. Strict environmental enforcement, rising energy storage needs, and increased focus on reducing health risks associated with lead exposure are supporting advanced recycling practices and operational efficiency.

Prominent companies active in the Global Lead Acid Battery Recycling Market include Ecobat, Exide Technologies, Glencore, EnerSys, Clarios, Aqua Metals, Gravita India, Gopher Resource LLC, Cirba Solutions, East Penn Manufacturing Company, Interstate Batteries, Engitec Technologies, Doe Run Company, Amara Raja, Battery Recyclers of America, GME Recycling, and BPL Nigeria Limited. These participants continue to shape market dynamics through capacity expansion, technology upgrades, and strategic partnerships. Companies in the Global Lead Acid Battery Recycling Market are strengthening their competitive position through investments in cleaner recycling technologies and process optimization. Many players are focusing on expanding recycling capacity to meet rising battery disposal volumes while improving recovery efficiency. Vertical integration across collection, processing, and material reuse is being adopted to secure supply chains and control costs. Firms are also prioritizing compliance-driven innovation to meet tightening environmental standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.2 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Process trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of World

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Process, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Pyrometallurgical

- 5.3 Hydrometallurgical

- 5.4 Physical/mechanical

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 SLI

- 6.3 Stationary

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Spain

- 7.3.3 Germany

- 7.3.4 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 South Korea

- 7.4.3 Japan

- 7.4.4 India

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 Amara Raja

- 8.2 Aqua Metals

- 8.3 Battery Recyclers of America

- 8.4 BPL Nigeria Limited

- 8.5 Cirba Solutions

- 8.6 Clarios

- 8.7 Doe Run Company

- 8.8 East Penn Manufacturing Company

- 8.9 Ecobat

- 8.10 EnerSys

- 8.11 Engitec Technologies

- 8.12 Exide Technologies

- 8.13 Glencore

- 8.14 GME Recycling

- 8.15 Gopher Resource LLC

- 8.16 Gravita India

- 8.17 Interstate Batteries

全球铅酸蓄电池回收市场:市场规模、市场占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球铅酸蓄电池回收市场:市场规模、市场占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 铅酸电池回收市场 2025-2029

铅酸电池回收市场 2025-2029 到 2030 年铅酸电池回收市场预测:按类型、来源、製程、成分和地区进行的全球分析

到 2030 年铅酸电池回收市场预测:按类型、来源、製程、成分和地区进行的全球分析