|

市场调查报告书

商品编码

1913391

输送机系统市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035 年)Conveyor System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

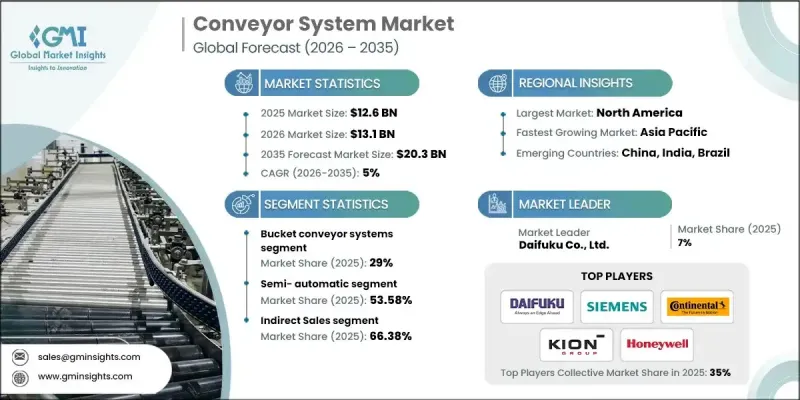

全球输送机系统市场预计到 2025 年将达到 126 亿美元,到 2035 年将达到 203 亿美元,年复合成长率为 5%。

市场成长得益于工业供应链各环节对营运效率、成本优化和长期永续性重视。透过併购实现的产业整合正在加速技术进步并增强竞争优势,从而促进系统的广泛应用。随着企业从劳力密集物料搬运转向自动化、节能的解决方案,输送机系统正日益受到青睐。现代系统设计优先考虑降低电力消耗量和减少营运排放,这与全球永续性目标一致。对环保製造和物流实践的日益关注持续影响投资决策。工业营运中对稳定吞吐量、可靠性和扩充性的需求不断增长,进一步推动了市场需求。随着企业对其设施进行现代化改造以满足不断变化的配送和履约需求,输送机系统正成为高效物料流策略的核心要素。预计这些趋势将在预测期内推动市场稳步扩张。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 126亿美元 |

| 市场规模预测 | 203亿美元 |

| 复合年增长率 | 5% |

北美地区对先进仓储物流基础设施的需求持续成长。同时,欧洲和亚太地区对工业和数位商务设施的投资不断增加,推动了相关技术在商业领域的广泛应用。企业越来越倾向于采用自动化、高效的系统来满足其吞吐量需求,并逐步抛弃速度较慢、劳力密集的流程。

2025年,斗式输送机系统市占率占比达29%。该细分市场持续保持强劲成长势头,这得益于其在有限的空间布局内高效输送大批量物料的能力。稳定的运作性能和物料处理能力也使其在散装物料应用中广泛应用。

预计到2025年,间接销售通路将占市场份额的66.38%,并在2035年之前保持强劲成长。系统整合商和专业经销商透过提供客製化安装、技术专长和持续的服务支援发挥关键作用。买家越来越依赖这些管道,以获得快速的维护回应和在地化的支援。

受自动化设施持续投资和分销网络不断扩张的推动,美国输送机系统市场预计到2034年将维持5.4%的复合年增长率。对职场安全、营运一致性和效率提升的高度重视也持续支撑着全国范围内的需求。

目录

第一章:分析方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 电子商务和履约的快速成长

- 工业4.0和智慧製造

- 永续性和能源效率

- 产业潜在风险与挑战

- 初始投资额高,投资回收期长

- 对遗留网站维修的复杂性

- 市场机会

- 物联网与预测性维护的集成

- 模组化和灵活的输送机设计

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要企业的竞争分析

- 竞争定位矩阵

- 主要趋势

- 企业合併(M&A)

- 商业伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依产品类型分類的市场估算与预测(2022-2035 年)

- 斗式输送机系统

- 皮带输送机系统

- 重力式滚筒输送机

- 输送机

- 炼式输送机

- 其他类型(天花板类型、地板类型、托盘类型等)

6. 按营运类型分類的市场估算与预测(2022-2035 年)

- 半自动

- 全自动

7. 依最终用途领域分類的市场估计与预测(2022-2035 年)

- 飞机场

- 零售

- 车

- 食品/饮料

- 其他的

第八章 按分销管道分類的市场估算和预测(2022-2035 年)

- 直接地

- 间接

第九章 各地区市场估算与预测(2022-2035 年)

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Beumer Group

- Continental AG

- Daifuku Co., Ltd.

- FlexLink AB(Coesia Group)

- Fives Group

- KION Group

- Honeywell Intelligrated

- Interroll Holding AG

- Hytrol Conveyor Company, Inc.

- Siemens Logistics

- Intralox, LLC(part of Laitram, LLC)

- Rexnord Corporation

- Shuttleworth, LLC(ProMach)

- Viastore Systems GmbH

- Swisslog Holding AG(KUKA AG)

- WAMGROUP SpA

The Global Conveyor System Market was valued at USD 12.6 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 20.3 billion by 2035.

Market growth is supported by increasing focus on operational productivity, cost optimization, and long-term sustainability across industrial supply chains. Industry consolidation through mergers and acquisitions is accelerating technological advancement and strengthening competitive positioning, which is contributing to broader system adoption. Conveyor systems are increasingly preferred as organizations transition away from labor-intensive material movement toward automated and energy-conscious solutions. Modern system designs prioritize reduced power consumption and lower operational emissions, aligning with global sustainability objectives. Growing commitment to environmentally responsible manufacturing and logistics practices continues to influence investment decisions. The rising need for consistent throughput, reliability, and scalability across industrial operations further supports demand. As companies modernize facilities to meet evolving distribution and fulfillment requirements, conveyor systems are becoming a core component of efficient material flow strategies. These trends collectively position the market for steady expansion over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.6 Billion |

| Forecast Value | $20.3 Billion |

| CAGR | 5% |

Demand for advanced warehousing and logistics infrastructure is increasing steadily across North America. At the same time, rising investment in industrial and digital commerce facilities across Europe and the Asia-Pacific region is supporting strong commercial adoption. Businesses are increasingly favoring automated, high-efficiency systems to meet throughput requirements, moving away from slower and labor-dependent processes.

The bucket conveyor systems segment held 29% share in 2025. This segment continues to perform strongly due to its ability to transport high volumes efficiently within limited spatial layouts. Consistent operational performance and load-handling capability support continued adoption across bulk material applications.

The indirect sales segment held 66.38% share in 2025 and is expected to maintain strong growth through 2035. System integrators and specialized distributors play a key role by delivering customized installations, technical expertise, and ongoing service support. Buyers increasingly rely on these channels for maintenance responsiveness and localized assistance.

U.S. Conveyor System Market held a CAGR of 5.4% through 2034, driven by sustained investment in automated facilities and expanding distribution networks. Emphasis on workplace safety, operational consistency, and efficiency improvement continues to support demand nationwide.

Key companies active in the Global Conveyor System Market include Daifuku Co., Ltd., Interroll Holding AG, Honeywell Intelligrated, KION Group, Beumer Group, Swisslog Holding AG (KUKA AG), Hytrol Conveyor Company, Inc., Siemens Logistics, Continental AG, Intralox, L.L.C., Fives Group, Rexnord Corporation, Viastore Systems GmbH, FlexLink AB (Coesia Group), Shuttleworth, LLC, and WAMGROUP S.p.A. Companies operating in the Global Conveyor System Market are reinforcing their market position through product innovation, automation integration, and strategic expansion. Manufacturers are investing in modular and scalable system designs to meet diverse customer requirements. Partnerships with logistics providers and system integrators are helping expand market reach and improve solution customization. Firms are also enhancing digital capabilities, including smart monitoring and predictive maintenance features, to increase system reliability and lifecycle value.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Operation

- 2.2.4 End- Use Vertical

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid E-commerce & Fulfillment Growth

- 3.2.1.2 Industry 4.0 & Smart Manufacturing

- 3.2.1.3 Sustainability & Energy Efficiency

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial CAPEX & Long ROI

- 3.2.2.2 Complexity of Retrofitting Legacy Sites

- 3.2.3 Opportunities

- 3.2.3.1 IoT & Predictive Maintenance Integration

- 3.2.3.2 Modular & Flexible Conveyor Design

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Bucket Conveyor Systems

- 5.3 Belt Conveyor System

- 5.4 Gravity Roller Conveyor

- 5.5 Screw (Auger) Conveyors

- 5.6 Chain Conveyors

- 5.7 Others (Overhead, Floor, Pallet, etc)

Chapter 6 Market Estimates and Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Semi-automatic

- 6.3 Automatic

Chapter 7 Market Estimates and Forecast, By End Use Vertical, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Airport

- 7.3 Retail

- 7.4 Automotive

- 7.5 Food & Beverages

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Beumer Group

- 10.2 Continental AG

- 10.3 Daifuku Co., Ltd.

- 10.4 FlexLink AB (Coesia Group)

- 10.5 Fives Group

- 10.6 KION Group

- 10.7 Honeywell Intelligrated

- 10.8 Interroll Holding AG

- 10.9 Hytrol Conveyor Company, Inc.

- 10.10 Siemens Logistics

- 10.11 Intralox, L.L.C. (part of Laitram, L.L.C.)

- 10.12 Rexnord Corporation

- 10.13 Shuttleworth, LLC (ProMach)

- 10.14 Viastore Systems GmbH

- 10.15 Swisslog Holding AG (KUKA AG)

- 10.16 WAMGROUP S.p.A.

分类输送机市场:按分类机类型、设备、驱动类型、皮带材质和终端用户产业划分,全球预测,2026-2032年输送机自动化系统市场:按类型、运作模式、组件、应用和最终用户产业划分,全球预测,2026-2032年高速输送机市场按类型、自动化程度、运作模式、驱动系统、负载能力和最终用户产业划分,全球预测,2026-2032年

分类输送机市场:按分类机类型、设备、驱动类型、皮带材质和终端用户产业划分,全球预测,2026-2032年输送机自动化系统市场:按类型、运作模式、组件、应用和最终用户产业划分,全球预测,2026-2032年高速输送机市场按类型、自动化程度、运作模式、驱动系统、负载能力和最终用户产业划分,全球预测,2026-2032年 全球振动给料输送机市场规模、份额、趋势及成长分析报告(2026-2034)全球振动输送机市场规模、份额、趋势和成长分析报告(2026-2034)

全球振动给料输送机市场规模、份额、趋势及成长分析报告(2026-2034)全球振动输送机市场规模、份额、趋势和成长分析报告(2026-2034) 日本工业输送系统市场规模、份额、趋势及预测(按类型、承载能力、运作类型、最终用途产业及地区划分),2026-2034年日本智慧输送系统市场规模、份额、趋势及预测(按组件、产品类型、技术、自动化程度、产业领域及地区划分),2026-2034年

日本工业输送系统市场规模、份额、趋势及预测(按类型、承载能力、运作类型、最终用途产业及地区划分),2026-2034年日本智慧输送系统市场规模、份额、趋势及预测(按组件、产品类型、技术、自动化程度、产业领域及地区划分),2026-2034年 2026年全球包装输送机市场报告2026年全球输送机系统市场报告斗式提昇机市场 - 2026-2031年预测

2026年全球包装输送机市场报告2026年全球输送机系统市场报告斗式提昇机市场 - 2026-2031年预测