|

市场调查报告书

商品编码

1906052

北美输送机市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)North America Conveyors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

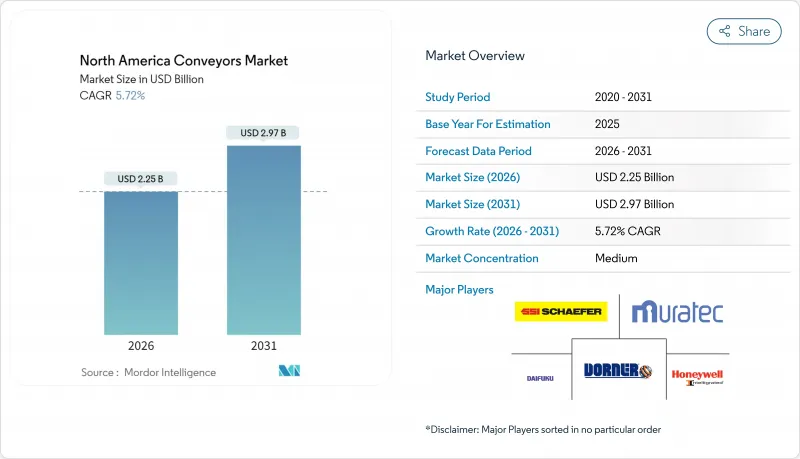

预计到 2026 年,北美输送机市场规模将达到 22.5 亿美元,高于 2025 年的 21.3 亿美元。

预计到 2031 年将达到 29.7 亿美元,2026 年至 2031 年的复合年增长率为 5.72%。

对自动化物料输送技术的投资不断增加、电子商务小包裹递送业务的持续增长以及旨在振兴国内製造业的联邦税收优惠政策,持续推动着新设备安装和维修的资金流入。日益严重的劳动力短缺(工厂空缺超过60万个,仓库人员离职率超过49%)进一步凸显了输送机的优势,因为输送机可以最大限度地减少人工操作环节。製造商青睐输送机的另一个原因是,它们能够轻鬆整合机器人和仓库管理软体,在不增加人员配置的情况下提高吞吐量。同时,终端用户也意识到,即使原物料价格波动,节能驱动装置和预测性维护分析也能降低全生命週期营运成本。这些因素共同支撑着稳定的设备更换需求,并为适应都市区有限空间的创新垂直和模组化布局创造了空间。

北美输送机市场趋势与洞察

电子商务与履约中心快速成长

如今,履约中心正在部署每小时可处理超过 10,000 个小包裹的传送带,并可在批量处理和单一拣选工作流程之间无缝切换。模组化、高吞吐量的分类机非常适合夹层和多层建筑。此类空间的年租金通常从每平方英尺 15 美元起。电脑视觉扫描器和人工智慧感测器可根据包裹大小动态调整传送带速度和分支角度,从而降低分类错误率和操作员的工作量。零售商在拓展线上订购线下取货和门市配送服务时,需要能够快速重新分配库存的弹性系统,以确保能够兑现当日送达的承诺。製药公司和汽车供应商也在效仿这些高速设计,以在不扩大面积的情况下应对 SKU 数量的激增。英特罗公司最近推出的紧凑型交叉传送带分类机顺应了小型化和更节能驱动装置的趋势,在提高小包裹吞吐量的同时降低了电力消耗。

自动化和工业4.0的普及推动了智慧输送机的发展

配备边缘感测器的连网输送机持续撷取振动、温度和电流消耗等数据,并将其传输至云端分析系统,提前10天预测故障,并将计画外停机时间减少30%。无线通讯协定使相邻区域能够自动调整速度,避免堵塞,并保持整个生产线的均匀流量。数位双胞胎模拟检验了建议的布局变更,缩短了试运行时间,并在硬体到货前识别并解决瓶颈问题。语音人机介面缩短了生产线主管的调整週期,他们可以监控多个工作区域并免提发出指令。将输送机与自主移动机器人 (AMR) 结合的设施能够即时调整拣选路径和转运点,这表明输送机和 AMR 作为互补资产而非替代品才能发挥最佳作用。

自动化系统需要较高的初始资本投入

承包自动化输送线的价格从 5 万美元到 50 万美元不等,不包括电气升级和地面加固。年度维护合约费用可能占到购买价格的 10% 到 15%,这使得利润率低的公司难以计算投资回报率。许多中小型製造商采用模组化方案,先购买基本传送带段,再添加分类模组,这可能会导致布局上的妥协。设备租赁和美国小型企业管理局 (SBA) 担保的融资可以缓解现金流压力,但仍会占用业主原本用于核心生产设备的信贷额度。儘管存在这些障碍,但人事费用的节省和品质的提升所带来的综合效益通常可以使其投资回收期缩短至三年以内,而稳定的利率也使得资金筹措谈判更加容易。

细分市场分析

预计到2024年,都市区房地产成本将达到每平方英尺15美元,这将推动人们对架空输送机的兴趣,预计到2031年,该品类将以7.06%的复合年增长率增长。由于皮带输送机在组装、仓库和包装线上具有广泛的兼容性,到2025年,皮带输送机仍将占据主导地位,占北美输送机市场份额的44.15%。滚筒式输送机对于输送每英尺超过1000磅的重物至关重要,这在汽车冲压加工中很常见。托盘系统适用于标准化单元搬运,而链条、螺旋和气动系统等专用系统则适用于需要冲洗和防爆功能的食品和製药环境。轻质合金轨道和低摩擦驱动装置可实现架空环形输送,从而释放宝贵的占地面积。整合式升降装置无需升降机或AGV即可在不同楼层之间移动料箱,从而缩短拣选路径长度并减少运输时间。凭藉封闭式链条回位装置和自动润滑站等增强的安全功能,架空式布局符合严格的 OSHA 指南,并减少了因人工维护而导致的停机时间。

这项创新的核心在于磁浮轨道,它几乎完全消除了机械磨损。试验应用主要集中在电子组装区域,这些区域对100级洁净室标准有严格的粒状物限制。虽然商业应用目前仍比较有限,但供应商预测,随着未来十年产量的扩大,成本曲线将会下降,并有可能在敏感区域取代炼式架空输送系统。

到2025年,单元式物料搬运系统将占据北美输送机市场59.20%的份额。这一主导地位主要得益于电子商务和药品包装领域对单一商品的快速输送。随着该地区製造业从低附加价值产品转向多品种、小批量生产,单元式物料搬运正以6.18%的复合年增长率增长,超过了散装搬运。视觉引导分流器能够即时读取条码,并将纸箱以亚毫米级的精度引导至相应的溜槽,这对于电子产品和汽车零件行业至关重要。儘管散装物料搬运系统在西部各州的矿区仍能以每小时1000吨的速度输送矿石和谷物,但资本预算优先考虑能够适应不断增长的库存单位(SKU)数量的灵活单元式生产线,并评估无需重大维修的设计方案。模组化单元透过快速连接轴连接,可以在季节性高峰期的週末进行快速重新配置。与WMS平台整合可实现即时库存可见性和自动补货,从而减少占用在安全库存中的营运资金。高密度堆迭区可缓衝下游堆垛机,防止因贴标和包装延迟而导致生产线停工。

先进的演算法会追踪产品在每个区域的停留时间,如果停留时间超过设定值,则会自动降低上游传送带的速度。这样可以均衡物料流动,无需人工干预。这种即时调节能够保护易碎食品包装的完整性,并最大限度地减少返工。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务和全通路履约中心的快速成长

- 对加工更大批量货物的需求不断增长,以及生产率的提高。

- 自动化和工业4.0的普及推动了智慧输送机的发展

- 食品饮料加工业的扩张对卫生输送解决方案提出了更高的要求。

- 《美国工业法案》中的税收优惠政策刺激了传送带投资。

- 劳动力短缺和日益严格的职业安全与健康管理局 (OSHA) 处罚推动了零压力和人体工学设计的发展。

- 市场限制

- 自动化系统的高初始资本支出

- 原物料价格波动推高了总拥有成本。

- 由于现有设施空间限制,传送带布局受到限制

- 微型仓配中心即插即用型自主移动机器人(AMR)的应用趋势

- 产业价值链分析

- 宏观经济因素的影响

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

第五章 市场规模与成长预测

- 依产品类型

- 腰带

- 滚筒

- 调色盘

- 开卖

- 其他特殊输送机

- 输送机分类

- 单元搬运运输送机

- 散装搬运机

- 透过驱动机构

- 交流马达驱动型

- 直流马达驱动型

- 液压驱动

- 气动

- 按最终用户行业划分

- 飞机场

- 零售与电子商务履约

- 车

- 一般製造业

- 食品/饮料

- 製药

- 采矿和采石

- 其他终端用户产业

- 按国家/地区

- 美国

- 加拿大

- 墨西哥

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Daifuku Co., Ltd.

- Schaefer Systems International, Inc.

- Murata Machinery USA, Inc.

- Honeywell Intelligrated Inc.

- Dorner Manufacturing Corporation

- BEUMER Corporation

- Bastian Solutions, LLC

- Interlake Mecalux, Inc.

- KNAPP Inc.

- Swisslog Logistics, Inc.

- Kardex Remstar, LLC

- Viastore Systems Inc.

- Hytrol Conveyor Company, Inc.

- Material Handling Systems, Inc.

- Precision, Inc.

- Interroll Holding AG

- FlexLink AB

- Fives Intralogistics Corp.

- Siemens Logistics LLC

- TGW Systems Inc.

- Dematic Corp.

第七章 市场机会与未来展望

The North America conveyors market size in 2026 is estimated at USD 2.25 billion, growing from 2025 value of USD 2.13 billion with 2031 projections showing USD 2.97 billion, growing at 5.72% CAGR over 2026-2031.

Rising investment in automated material-handling technology, continuous growth in e-commerce parcel shipments, and federal tax incentives aimed at revitalizing domestic manufacturing continue to drive capital toward new installations and retrofits. Persistent labor shortages, leaving more than 600,000 factory positions vacant and warehouse turnover rates above 49%, reinforce the business case for conveyors that minimize manual touchpoints. Manufacturers also favor conveyors because they integrate easily with robotics and warehouse management software, improving throughput without requiring an increase in headcount. Meanwhile, end users see energy-efficient drives and predictive maintenance analytics lowering lifetime operating costs, even when raw material prices fluctuate. Together, these factors anchor steady replacement demand and create headroom for innovative vertical and modular layouts that fit tight urban footprints.

North America Conveyors Market Trends and Insights

Rapid Growth of E-commerce and Omnichannel Fulfillment Hubs

Fulfillment centers now feature conveyors capable of moving more than 10,000 parcels per hour, switching seamlessly between bulk and individual-pick workflows. Modular, high-throughput sorters are ideal for mezzanine and multi-level buildings, where rented space typically commands USD 15+ per square foot annually. Computer-vision scanners and AI-enabled sensors dynamically adjust belt speed and diverter angles based on package size, reducing mis-sort rates and operator touches. Retailers extending click-and-collect and ship-from-store programs require flexible systems that can redirect inventory within seconds, ensuring they keep same-day delivery promises. Pharmaceutical and automotive suppliers mimic these high-velocity designs to manage SKU proliferation without enlarging footprints. Recent compact cross-belt sorters launched by Interroll underscore the trend toward narrower frames and energy-efficient drives that reduce power consumption while increasing parcel throughput.

Automation and Industry 4.0 Adoption Driving Smart Conveyors

Networked conveyors equipped with edge sensors collect continuous data on vibration, temperature, and current draw, which is then fed into cloud analytics that predict failures up to 10 days in advance, resulting in a 30% reduction in unplanned stops. Wireless protocols enable adjacent zones to auto-throttle their speed to avoid jams, maintaining a balanced flow across the entire line. Digital-twin simulations model proposed layout changes, reducing commissioning time and ensuring bottlenecks are identified and resolved before hardware arrives. Voice-enabled human-machine interfaces shorten adjustment cycles for line leaders who can issue hands-free commands while monitoring multiple work areas. Facilities that pair conveyors with autonomous mobile robots (AMRs) orchestrate pick paths and transfer points in real-time, demonstrating that conveyors and AMRs operate best as complementary assets rather than substitutes.

High Initial Capital Expenditure for Automated Systems

A turnkey automated conveyor line ranges from USD 50,000 to USD 500,000, excluding electrical upgrades or floor reinforcements. Annual service contracts can equal 10-15% of purchase cost, complicating ROI models for firms with thin margins. Many small manufacturers adopt a modular approach, buying basic belt sections first and adding sort modules later, though that can create layout compromises. Equipment leasing and SBA-backed loans ease cash-flow strain yet still tie up credit lines that owners prefer to earmark for core production machinery. Despite these hurdles, payback periods often fall below three years once labor savings and quality gains are tallied, making financing conversations easier when interest rates stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Labor Shortages and Rising OSHA Penalties Boosting Ergonomic Designs

- Tax Incentives Under U.S. Industrial Bills Accelerating Conveyor Investments

- Volatility in Raw Material Prices Inflating Total Cost of Ownership

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Overhead conveyors garnered faster interest as tight urban real estate costs reached USD 15 per sq ft in 2024, catalyzing a 7.06% CAGR through 2031 for this category. Belt units still dominated the North America conveyor market, with a 44.15% share in 2025, due to their broad compatibility across assembly, warehousing, and packaging lines. Roller models remain indispensable for handling heavy loads exceeding 1,000 lb per linear foot, which is common in automotive stamping. Pallet systems serve standardized unit loads, while niche variants, such as chain, screw, or pneumatic systems, address food or pharma environments that require wash-down or explosion-proof features. Lightweight alloy tracks and low-friction drives enable ceiling-mounted loops, freeing valuable floor area. Integrated lift sections now transfer totes between tiers without the need for lifts or AGVs, thereby compressing pick-path length and reducing travel time. Safety upgrades, including enclosed chain returns and auto-lube stations, help overhead layouts meet strict OSHA guidelines, reducing downtime for manual maintenance.

Innovation centers on magnetic-levitation tracks that virtually eliminate mechanical wear; pilot deployments focus on electronics assembly, where class-100 clean-room standards prohibit particulates. While commercial rollout remains limited, suppliers expect cost curves to fall as volume scales over the decade, potentially displacing chain-based overhead designs in sensitive sectors.

Unit handling systems held a 59.20% share of the North America conveyor market in 2025, a lead driven by discrete-item flows in e-commerce and pharma packaging. Growth at 6.18% CAGR outpaces bulk handling as the region's manufacturing pivots from low-value commodities toward high-mix, low-volume goods. Vision-guided diverters read barcodes on the fly, steering cartons into the correct chutes with sub-millimeter accuracy, which is crucial for electronics and auto parts. While bulk systems still move ore and grain at 1,000 t/h in the mining belts of the western provinces, capital budgeting increasingly rewards flexible unit lines that allow SKU proliferation without requiring overhauls. Modular sections lock together via quick-connect shafts, allowing for weekend reconfiguration during seasonal peaks. Integration with WMS platforms provides real-time inventory snapshots and triggers automated replenishment, trimming working capital tied up in safety stock. High-density accumulation zones buffer downstream palletizers, preventing line starve-outs when labeling or wrapping slows.

Advanced algorithms track dwell time per zone; if product backups exceed parameters, upstream belts automatically decelerate, smoothing the flow and eliminating the need for manual intervention. This real-time tuning ensures that fragile food packages remain intact and minimizes rework.

The North America Conveyors Market Report is Segmented by Product Type (Belt, Roller, Pallet, and More), Conveyor Class (Unit Handling Conveyors and Bulk Handling Conveyors), Drive Mechanism (AC Electric Motor Driven, DC Electric Motor Driven, and More), End-User Industry (Airport, Retail and E-Commerce Fulfillment, Automotive, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Daifuku Co., Ltd.

- Schaefer Systems International, Inc.

- Murata Machinery USA, Inc.

- Honeywell Intelligrated Inc.

- Dorner Manufacturing Corporation

- BEUMER Corporation

- Bastian Solutions, LLC

- Interlake Mecalux, Inc.

- KNAPP Inc.

- Swisslog Logistics, Inc.

- Kardex Remstar, LLC

- Viastore Systems Inc.

- Hytrol Conveyor Company, Inc.

- Material Handling Systems, Inc.

- Precision, Inc.

- Interroll Holding AG

- FlexLink AB

- Fives Intralogistics Corp.

- Siemens Logistics LLC

- TGW Systems Inc.

- Dematic Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of e-commerce and omnichannel fulfillment hubs

- 4.2.2 Increasing demand for handling larger volumes of goods and improving productivity

- 4.2.3 Automation and Industry 4.0 adoption driving smart conveyors

- 4.2.4 Expansion of food and beverage processing requiring hygienic conveyor solutions

- 4.2.5 Tax incentives under U.S. industrial bills accelerating conveyor investments

- 4.2.6 Labor shortages and rising OSHA penalties boosting zero-pressure and ergonomic designs

- 4.3 Market Restraints

- 4.3.1 High initial capital expenditure for automated systems

- 4.3.2 Volatility in raw material prices inflating total cost of ownership

- 4.3.3 Space constraints in legacy facilities limiting conveyor layouts

- 4.3.4 Preference for plug-and-play AMRs in micro-fulfillment sites

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Belt

- 5.1.2 Roller

- 5.1.3 Pallet

- 5.1.4 Overhead

- 5.1.5 Other Specialized Conveyors

- 5.2 By Conveyor Class

- 5.2.1 Unit Handling Conveyors

- 5.2.2 Bulk Handling Conveyors

- 5.3 By Drive Mechanism

- 5.3.1 AC Electric Motor Driven

- 5.3.2 DC Electric Motor Driven

- 5.3.3 Hydraulic Driven

- 5.3.4 Pneumatic Driven

- 5.4 By End-User Industry

- 5.4.1 Airport

- 5.4.2 Retail and E-commerce Fulfillment

- 5.4.3 Automotive

- 5.4.4 General Manufacturing

- 5.4.5 Food and Beverage

- 5.4.6 Pharmaceuticals

- 5.4.7 Mining and Quarrying

- 5.4.8 Other End-User Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Daifuku Co., Ltd.

- 6.4.2 Schaefer Systems International, Inc.

- 6.4.3 Murata Machinery USA, Inc.

- 6.4.4 Honeywell Intelligrated Inc.

- 6.4.5 Dorner Manufacturing Corporation

- 6.4.6 BEUMER Corporation

- 6.4.7 Bastian Solutions, LLC

- 6.4.8 Interlake Mecalux, Inc.

- 6.4.9 KNAPP Inc.

- 6.4.10 Swisslog Logistics, Inc.

- 6.4.11 Kardex Remstar, LLC

- 6.4.12 Viastore Systems Inc.

- 6.4.13 Hytrol Conveyor Company, Inc.

- 6.4.14 Material Handling Systems, Inc.

- 6.4.15 Precision, Inc.

- 6.4.16 Interroll Holding AG

- 6.4.17 FlexLink AB

- 6.4.18 Fives Intralogistics Corp.

- 6.4.19 Siemens Logistics LLC

- 6.4.20 TGW Systems Inc.

- 6.4.21 Dematic Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

振动输送机市场:依输送机类型、驱动系统、处理能力范围及最终用途产业划分-2026-2032年全球市场预测输送机系统市场:2026-2032年全球市场预测(依产品类型、自动化类型、驱动系统、负载能力、输送方向、皮带材料、输送方式、组件、终端用户产业及销售管道)输送秤市场:2026-2032年全球市场预测(以秤类型、技术、容量、精准度等级、销售管道和最终用户划分)分类输送机市场:按分类机类型、设备、驱动类型、皮带材质和终端用户产业划分,全球预测,2026-2032年输送机自动化系统市场:按类型、运作模式、组件、应用和最终用户产业划分,全球预测,2026-2032年

振动输送机市场:依输送机类型、驱动系统、处理能力范围及最终用途产业划分-2026-2032年全球市场预测输送机系统市场:2026-2032年全球市场预测(依产品类型、自动化类型、驱动系统、负载能力、输送方向、皮带材料、输送方式、组件、终端用户产业及销售管道)输送秤市场:2026-2032年全球市场预测(以秤类型、技术、容量、精准度等级、销售管道和最终用户划分)分类输送机市场:按分类机类型、设备、驱动类型、皮带材质和终端用户产业划分,全球预测,2026-2032年输送机自动化系统市场:按类型、运作模式、组件、应用和最终用户产业划分,全球预测,2026-2032年 全球输送系统市场规模、份额、趋势和成长分析报告(2026-2034)高速输送机市场按类型、自动化程度、运作模式、驱动系统、负载能力和最终用户产业划分,全球预测,2026-2032年全球振动给料输送机市场规模、份额、趋势及成长分析报告(2026-2034)全球振动输送机市场规模、份额、趋势和成长分析报告(2026-2034)

全球输送系统市场规模、份额、趋势和成长分析报告(2026-2034)高速输送机市场按类型、自动化程度、运作模式、驱动系统、负载能力和最终用户产业划分,全球预测,2026-2032年全球振动给料输送机市场规模、份额、趋势及成长分析报告(2026-2034)全球振动输送机市场规模、份额、趋势和成长分析报告(2026-2034) 日本工业输送系统市场规模、份额、趋势及预测(按类型、承载能力、运作类型、最终用途产业及地区划分),2026-2034年

日本工业输送系统市场规模、份额、趋势及预测(按类型、承载能力、运作类型、最终用途产业及地区划分),2026-2034年