|

市场调查报告书

商品编码

1913429

高压加工设备市场机会、成长要素、产业趋势分析及预测(2026年至2035年)High-Pressure Processing (HPP) Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

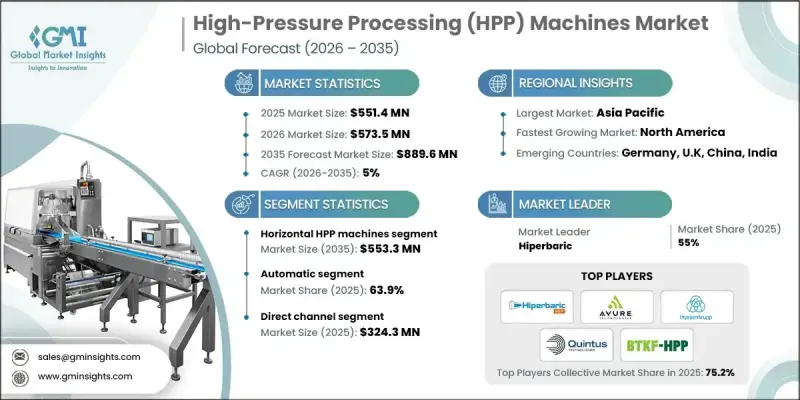

全球压力处理设备市场预计到 2025 年将达到 5.514 亿美元,到 2035 年将达到 8.896 亿美元,年复合成长率为 5%。

市场成长势头源于消费者偏好的转变,他们更倾向于选择天然成分和加工过程最少的健康食品。製造商正越来越多地采用高压加工技术,该技术无需依赖合成添加剂即可保存食品,同时保持其原始的感官和营养特性。这种非热加工方法符合消费者对洁净标示产品和长期保质期的不断增长的需求,且不会影响产品品质。该技术在有效降低微生物风险、同时保持产品完整性方面也发挥关键作用,有助于解决全球食品安全问题。围绕食品安全标准的监管压力持续推动加工企业采用相关设备。随着生产商专注于差异化和合规性,高压加工系统正成为现代食品生产营运中不可或缺的资产。设备效率、扩充性和自动化程度的提升持续惠及市场,使加工商能够在满足全球市场竞争和监管要求的同时,有效管理食品安全、延长保质期并保持产品一致性。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 5.514亿美元 |

| 预测金额 | 8.896亿美元 |

| 复合年增长率 | 5% |

预计2025年,水平高压加工(HPP)设备市场规模将达3.397亿美元,2035年将达5.533亿美元。水平高压加工(HPP)设备凭藉其高效的运作和多功能性,持续引领市场。根据美国农业部(USDA)报告显示,HPP技术的应用正以每年超过15%的速度成长。 HPP技术已成为商业性食品加工的首选解决方案,因为它能够在维持产品品质、质地和营养价值的同时,提高食品安全性并延长保质期。

预计到2025年,自动化高压加工(HPP)设备将占据63.9%的市场。自动化HPP系统对于大规模食品饮料生产商至关重要,因为它们能够提供精准稳定的性能,从而确保高生产率。这些设备能够简化製作流程、减少停机时间并保持运作可靠性,这对果汁、肉品和已调理食品生产商至关重要。自动化HPP解决方案能够帮助企业在满足大量生产需求的同时,保障产品的安全性和品质。

预计到2025年,美国高压加工设备市占率将达到73.7%。美国食品药物管理局(FDA)和美国农业部(USDA)对食品安全法规的严格执行,使美国成为全球安全食品保藏技术的领导者。严格的政府标准正促使食品加工商采用高压加工(HPP)等非热加工解决方案,这些方案能够在维持产品品质的同时,减少病原体,延长保质期,并消除对化学防腐剂的需求。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 消费者对洁净标示和无防腐剂食品的需求日益增长

- 严格的食品安全法规

- 冷压产品扩张

- 产业潜在风险与挑战

- 高初始资本投入

- 新兴市场认知度与接受度较低

- 机会

- 引入提高精度和能源效率的新技术

- 整合物联网和预测性维护解决方案

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 透过装置

- 按地区

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计(HS编码8419.89)

- 主要进口国

- 主要出口国

- 差距分析

- 风险评估与缓解

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依设备类型分類的市场估算与预测,2022-2035年

- 卧式高压加工机

- 立式高功率压力机(HPP)

第六章 依产能分類的市场估计与预测,2022-2035年

- 少于100公升

- 100升至300公升

- 超过300公升

7. 按营运类型分類的市场估算与预测,2022-2035 年

- 自动的

- 半自动

第八章 依压力范围分類的市场估计与预测,2022-2035年

- 高达 400 兆帕

- 400-600 MPa

- 600兆帕或以上

第九章 依技术分類的市场估计与预测,2022-2035年

- 冷等静压(CIP)

- 热等静压(HIP)

第十章 依应用领域分類的市场估计与预测,2022-2035年

- 水果和蔬菜

- 肉类和鱼贝类

- 乳製品

- 饮料

- 其他(包装调味料、谷物等)

第十一章 依最终用途分類的市场估计与预测,2022-2035年

- 中小企业

- 大公司

第十二章 按分销管道分類的市场估算与预测,2022-2035年

- 直销

- 间接销售

第十三章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十四章:公司简介

- Avure Technologies

- Bao Tou Kefa High Pressure Technology

- Engineered Pressure Systems International-EPSI

- Hiperbaric

- Kobe Steel

- Multivac Sepp Haggenmuller

- Next HPP

- Quintus Technologies

- Stansted Fluid Power

- Thyssenkrupp-Uhde HPT

- Hydrolock-Steribar HPP

- HTSM HPP

- Idus HPP Systems

- Resato International

- Shandong Pengneng Machinery Technology

The Global High-Pressure Processing Machines Market was valued at USD 551.4 million in 2025 and is estimated to grow at a CAGR of 5% to reach USD 889.6 million by 2035.

Market momentum is supported by shifting consumer preferences toward healthier food options that emphasize natural composition and minimal processing. Manufacturers are increasingly adopting high-pressure processing technology as it allows food preservation without relying on synthetic additives while maintaining original sensory and nutritional characteristics. This non-thermal approach aligns with evolving expectations for clean-label products and longer shelf stability without compromising quality. The technology also plays a critical role in addressing global food safety concerns by effectively reducing microbial risks while preserving product integrity. Regulatory pressure surrounding food safety standards continues to accelerate equipment adoption across processing facilities. As producers focus on differentiation and compliance, high-pressure processing systems are becoming essential assets for modern food manufacturing operations. The market continues to benefit from advancements in equipment efficiency, scalability, and automation, enabling processors to manage safety, shelf life, and product consistency while responding to competitive and regulatory demands across international markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $551.4 Million |

| Forecast Value | $889.6 Million |

| CAGR | 5% |

The horizontal HPP machines segment generated USD 339.7 million in 2025 and is projected to reach USD 553.3 million by 2035. Horizontal high-pressure processing (HPP) machines continue to lead the market due to their operational efficiency and versatility. Adoption of HPP technology has been growing at a rate of over 15% annually, according to reports from the U.S. Department of Agriculture (USDA). HPP technology enhances food safety and extends shelf life while preserving the quality, texture, and nutritional integrity of products, making it a preferred solution for commercial food processing.

The automatic HPP machines segment held 63.9% share in 2025. Automatic HPP systems are critical for large-scale food and beverage manufacturers because they deliver precise, consistent performance that ensures high productivity. These machines streamline processing, reduce downtime, and maintain operational reliability, which is essential for producers handling juices, meats, and ready-to-eat meals. Automated HPP solutions allow companies to meet high-volume production demands while ensuring product safety and quality remain uncompromised.

U.S. High-Pressure Processing Machines Market held 73.7% share in 2025. Strong enforcement of food safety regulations by the FDA and USDA positions the country as a global leader in safe food preservation technologies. Strict government standards encourage food processors to adopt non-thermal processing solutions like HPP, which reduce pathogens, extend shelf life, and eliminate the need for chemical preservatives while maintaining product quality.

Key companies active in the Global High-Pressure Processing (HPP) Machines Market include Hiperbaric S.A., Quintus Technologies AB, Avure Technologies (JBT Corporation), Universal Pure, LLC, Multivac Sepp Haggenmuller SE & Co. KG, American Pasteurization Company (APC), Kobe Steel Ltd., Thyssenkrupp AG, Next HPP, Nordic High-Pressure Processing (NHPP), Bao Tou KeFa High Pressure Technology Co., Ltd., Stansted Fluid Power Ltd, Engineered Pressure Systems International (EPSI), Pulsemaster, and HPP Italia S.r.l. Companies operating in the Global High-Pressure Processing (HPP) Machines Market are strengthening their market position through continuous investment in technology innovation and system efficiency. Manufacturers are focusing on developing scalable equipment that supports higher throughput and flexible production requirements. Strategic partnerships with food processors and contract service providers are helping expand market reach and adoption. Firms are also emphasizing automation, digital monitoring, and energy optimization to improve operational reliability and reduce costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment Type

- 2.2.3 Capacity

- 2.2.4 Mode of Operation

- 2.2.5 Pressure Range

- 2.2.6 Technology

- 2.2.7 Application

- 2.2.8 End Use

- 2.2.9 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for clean-label and preservative-free foods

- 3.2.1.2 Stringent food safety regulations

- 3.2.1.3 Expansion of the cold-pressed products

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Limited awareness and adoption in emerging markets

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of new technology for precision & energy efficiency

- 3.2.3.2 Integration of IoT & predictive maintenance solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By equipment type

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code 8419.89)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2022-2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Horizontal HPP Machines

- 5.3 Vertical HPP Machines

Chapter 6 Market Estimates & Forecast, By Capacity, 2022-2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Below 100 Liters

- 6.3 100 Liters - 300 Liters

- 6.4 Above 300 Liters

Chapter 7 Market Estimates & Forecast, By Mode of Operation, 2022-2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Automatic

- 7.3 Semi-automatic

Chapter 8 Market Estimates & Forecast, By Pressure Range, 2022-2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Up to 400 MPa

- 8.3 400-600 MPa

- 8.4 Above 600 MPa

Chapter 9 Market Estimates & Forecast, By Technology, 2022-2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Cold Isostatic Pressing (CIP)

- 9.3 Hot Isostatic Pressing (HIP)

Chapter 10 Market Estimates & Forecast, By Application, 2022-2035 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Fruits & Vegetables

- 10.3 Meat & Seafood

- 10.4 Dairy Products

- 10.5 Beverages

- 10.6 Others (Packaged Condiments, Grains, etc.)

Chapter 11 Market Estimates & Forecast, By End Use, 2022-2035 (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 Small & Medium Enterprises (SMEs)

- 11.3 Large Enterprises

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Million) (Thousand Units)

- 12.1 Key trends

- 12.2 Direct sales

- 12.3 Indirect sales

Chapter 13 Market Estimates & Forecast, By Region, 2022-2035 (USD Million) (Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 France

- 13.3.3 UK

- 13.3.4 Italy

- 13.3.5 Spain

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 Australia

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Avure Technologies

- 14.2 Bao Tou Kefa High Pressure Technology

- 14.3 Engineered Pressure Systems International - EPSI

- 14.4 Hiperbaric

- 14.5 Kobe Steel

- 14.6 Multivac Sepp Haggenmuller

- 14.7 Next HPP

- 14.8 Quintus Technologies

- 14.9 Stansted Fluid Power

- 14.10 Thyssenkrupp - Uhde HPT

- 14.11 Hydrolock - Steribar HPP

- 14.12 HTSM HPP

- 14.13 Idus HPP Systems

- 14.14 Resato International

- 14.15 Shandong Pengneng Machinery Technology

高压加工解决方案市场:按设备、操作模式、包装、产能、应用和最终用户划分-全球预测,2026-2032年

高压加工解决方案市场:按设备、操作模式、包装、产能、应用和最终用户划分-全球预测,2026-2032年 2026年全球高压加工设备市场报告HPP技术市场按产品、运作模式、封装类型、应用和最终用户划分,全球预测(2026-2032)

2026年全球高压加工设备市场报告HPP技术市场按产品、运作模式、封装类型、应用和最终用户划分,全球预测(2026-2032) 高压加工设备市场规模、份额及成长分析(按安装方式、容器容量、设备类型、应用及地区划分)-产业预测(2026-2033年)高压加工设备市场(按应用产业、设备类型、压力范围、最终用户和销售管道)——2025-2032 年全球预测

高压加工设备市场规模、份额及成长分析(按安装方式、容器容量、设备类型、应用及地区划分)-产业预测(2026-2033年)高压加工设备市场(按应用产业、设备类型、压力范围、最终用户和销售管道)——2025-2032 年全球预测 高压加工设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

高压加工设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 亚太地区压力加工设备市场:按应用、产品和国家分类的分析和预测(2023-2033)

亚太地区压力加工设备市场:按应用、产品和国家分类的分析和预测(2023-2033) 欧洲高压加工设备市场:按应用、按产品、按国家 - 分析和预测(2023-2033)

欧洲高压加工设备市场:按应用、按产品、按国家 - 分析和预测(2023-2033) 高压加工市场分析:到 2030 年的趋势、预测与竞争分析

高压加工市场分析:到 2030 年的趋势、预测与竞争分析 高压加工 (HPP) 设备的全球市场 2024-2028

高压加工 (HPP) 设备的全球市场 2024-2028