|

市场调查报告书

商品编码

1928887

杏仁配料市场机会、成长要素、产业趋势分析及2026年至2035年预测Almond Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

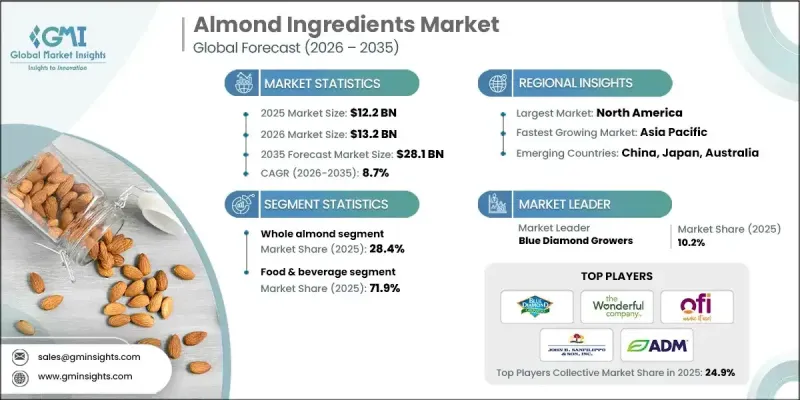

全球杏仁配料市场预计到 2025 年将达到 122 亿美元,到 2035 年将达到 281 亿美元,年复合成长率为 8.7%。

杏仁製品包括杏仁粉、杏仁酱、杏仁油、杏仁奶和杏仁膏等加工产品,广泛应用于烘焙、糖果甜点、饮料和乳製品替代品领域。消费者健康意识的增强和营养知识的提高推动了市场成长。杏仁富含蛋白质、膳食纤维和健康脂肪,是健康饮食的理想选择。研究表明,杏仁是植物性蛋白质和维生素E的丰富来源,有助于心臟健康和免疫功能。植物性饮食的日益普及,以及政府饮食指南的发布,推动了对无乳製品和无乳糖产品的需求。消费者越来越重视「洁净标示」和有机产品,促使生产商在有机杏仁产品领域不断创新。美国农业部(USDA)和欧盟委员会等监管机构制定的标准,进一步提升了该行业的透明度和品质。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 122亿美元 |

| 预测金额 | 281亿美元 |

| 复合年增长率 | 8.7% |

截至2025年,整颗杏仁的市占率达到28.4%,预计到2035年将以8.6%的复合年增长率成长。杏仁用途广泛且加工工序少,深受注重健康、追求天然零食的消费者的青睐。整颗杏仁正日益被定位为一种优质营养的食材,从而推动了全球需求。

预计到2025年,食品饮料产业将占市场份额的71.9%。杏仁原料广泛应用于烘焙产品、糖果甜点、零食和乳製品替代品。植物来源、无麸质和纯素产品的日益普及推动了饮料、蛋白棒和甜点领域的创新,巩固了该行业的主导地位。

预计2026年至2035年,北美杏仁原料市场将以8.7%的复合年增长率成长。消费者对植物来源、无过敏原和洁净标示产品的偏好正在推动食品、饮料和膳食补充剂行业的需求。日益增强的健康意识促使企业加大研发投入,以提高杏仁原料的永续性、功能性和质量,从而满足不断变化的消费者期望。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 人们的健康意识和对营养的兴趣日益增强

- 植物性食品的兴起与乳製品替代品的需求

- 偏好洁净标示和有机产品

- 产业潜在风险与挑战

- 杏仁价格波动和供应不确定性

- 来自其他植物性成分的竞争

- 市场机会

- 扩大有机杏仁市场

- 植物来源肉和植物乳製品中的杏仁蛋白

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 杏仁(整颗)

- 杏仁片

- 杏仁粉

- 杏仁酱

- 杏仁奶

- 杏仁油

- 其他的

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 饮食

- 烘焙产品

- 糖果甜点

- 乳製品替代品

- 冷冻甜点

- 即食谷物(RTE)

- 小吃

- 坚果和种子酱

- 饮料

- 食用油/烹饪用途

- 其他的

- 化妆品和个人护理

- 护肤品

- 护髮产品

- 按摩和芳香疗法

- 肥皂和洗涤剂

- 化妆品配方

- 其他的

- 药品和营养补充剂

- 动物饲料

- 牲畜饲料

- 家禽饲料

- 宠物食品

- 其他的

- 其他的

7. 2022-2035年按分销管道分類的市场估算与预测

- 大卖场/超级市场

- 便利商店

- 线上零售

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- ADM

- Blue Diamond Growers

- Olam Food International

- John B. Sanfilippo &Son, Inc

- Kanegrade

- Borges Agricultural &Industrial Nuts

- Treehouse California Almonds

- Harris Woolf Almonds

- The Wonderful Company

- Royal Nut Company

- Barry Callebaut Group

The Global Almond Ingredients Market was valued at USD 12.2 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 28.1 billion by 2035.

Almond ingredients encompass processed products such as almond flour, butter, oil, milk, and paste, widely used in bakery, confectionery, beverages, and dairy alternatives. Market growth is driven by rising health consciousness and increasing nutritional awareness among consumers. Almonds are recognized for their high protein, fiber, and healthy fat content, making them a preferred choice for nutrient-dense diets. Research indicates that almonds are a rich source of plant-based protein and vitamin E, supporting heart health and immunity. Rising adoption of plant-based diets, coupled with government dietary recommendations, is driving demand for dairy-free and lactose-free products. Consumers are also prioritizing clean-label and organic options, prompting manufacturers to innovate in organic almond products. Regulatory standards by agencies such as the USDA and European Commission are further encouraging transparency and quality in this sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.2 Billion |

| Forecast Value | $28.1 Billion |

| CAGR | 8.7% |

The whole almonds segment accounted for 28.4% share in 2025 and is expected to grow at a CAGR of 8.6% through 2035. Their versatility and minimal processing appeal to health-conscious consumers seeking natural snack options. Whole almonds are increasingly marketed as premium, nutrient-rich ingredients, boosting global demand.

The food & beverage sector held a 71.9% share in 2025. Almond ingredients are widely used in bakery, confectionery, snacks, and dairy alternatives. The rise of plant-based, gluten-free, and vegan formulations has driven innovation in beverages, protein bars, and desserts, solidifying the sector's leading position.

North America Almond Ingredients Market is forecast to grow at a CAGR of 8.7% between 2026 and 2035. Consumer preference for plant-based, allergen-free, and clean-label products has fueled demand across food, beverage, and nutraceutical applications. Growing health and wellness awareness encourages companies to invest in research and development to enhance the sustainability, functionality, and quality of almond ingredients, aligning with evolving consumer expectations.

Key companies operating in the Global Almond Ingredients Market include Blue Diamond Growers, ADM, Olam Food International, The Wonderful Company, Barry Callebaut Group, Kanegrade, Borges Agricultural & Industrial Nuts, John B. Sanfilippo & Son, Inc., Treehouse California Almonds, Royal Nut Company, and Harris Woolf Almonds. To strengthen their position, companies in the Almond Ingredients Market are focusing on product innovation and diversification, developing value-added almond products such as fortified flours, protein-enriched butters, and functional beverages. Many firms are expanding their direct-to-consumer channels and e-commerce capabilities to reach wider audiences. Sustainability initiatives, including eco-friendly sourcing, organic certifications, and traceability programs, enhance brand credibility. Partnerships with food and beverage manufacturers support the co-development of new formulations. Strategic geographic expansion targets emerging markets with growing plant-based product demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health consciousness & nutritional awareness

- 3.2.1.2 Plant-based diet adoption & dairy alternative demand

- 3.2.1.3 Clean-label & organic product preference

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Almond price volatility & supply uncertainty

- 3.2.2.2 Competition from alternative plant-based ingredients

- 3.2.3 Market opportunities

- 3.2.3.1 Organic almond market expansion

- 3.2.3.2 Almond protein in plant-based meat & dairy

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Whole almond

- 5.3 Almond pieces

- 5.4 Almond flour

- 5.5 Almond paste

- 5.6 Almond milk

- 5.7 Almond oil

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.2.1 Bakery products

- 6.2.2 Confectionery

- 6.2.3 Dairy alternatives

- 6.2.4 Frozen desserts

- 6.2.5 Ready-to-eat (RTE) cereals

- 6.2.6 Snacks

- 6.2.7 Nut & seed butters

- 6.2.8 Beverages

- 6.2.9 Cooking oils & culinary applications

- 6.2.10 Others

- 6.3 Cosmetics & personal care

- 6.3.1 Skin care products

- 6.3.2 Hair care products

- 6.3.3 Massage & aromatherapy

- 6.3.4 Soaps & cleansers

- 6.3.5 Cosmetic formulations

- 6.3.6 Others

- 6.4 Pharmaceutical & nutraceutical

- 6.4.1 Animal feed

- 6.4.2 Livestock feed

- 6.4.3 Poultry feed

- 6.4.4 Pet food

- 6.4.5 Others

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Hypermarkets/supermarkets

- 7.3 Convenience stores

- 7.4 Online retail

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ADM

- 9.2 Blue Diamond Growers

- 9.3 Olam Food International

- 9.4 John B. Sanfilippo & Son, Inc

- 9.5 Kanegrade

- 9.6 Borges Agricultural & Industrial Nuts

- 9.7 Treehouse California Almonds

- 9.8 Harris Woolf Almonds

- 9.9 The Wonderful Company

- 9.10 Royal Nut Company

- 9.11 Barry Callebaut Group

全球杏仁原料市场

全球杏仁原料市场 杏仁原料市场分析及预测(至2034年):类型、产品、应用、配方、技术、最终用户、成分、製程、原料类型

杏仁原料市场分析及预测(至2034年):类型、产品、应用、配方、技术、最终用户、成分、製程、原料类型 杏仁原料市场:2025-2030 年预测

杏仁原料市场:2025-2030 年预测 2030 年杏仁原料市场预测:按产品类型、格式、分销管道、应用和地区进行的全球分析

2030 年杏仁原料市场预测:按产品类型、格式、分销管道、应用和地区进行的全球分析