|

市场调查报告书

商品编码

1928986

卡车编队行驶市场成长机会、成长要素、产业趋势分析及2026年至2035年预测Truck Platooning Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

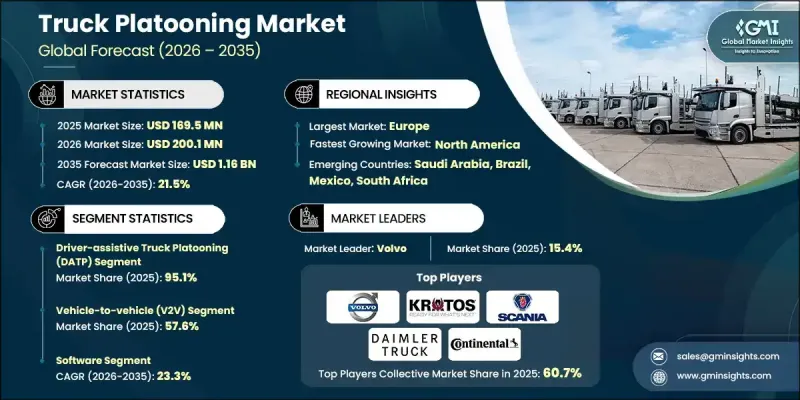

全球卡车编队行驶市场预计到 2025 年将达到 1.695 亿美元,到 2035 年将达到 11.6 亿美元,年复合成长率为 21.5%。

物流和运输公司对提高效率、节约燃油和提升繁忙路段安全性的需求日益增长,推动了市场成长。世界各国政府都在积极支持试验计画和道路试验,同时认真评估道路基础设施、实施成本、安全性和风险管理等因素。随着卡车编队行驶技术的成熟和商业性化,预计大型物流和电商公司将成为早期采用者,在其车队中部署编队行驶技术以提高营运效率。监管支持力度更大、交通网络更发达、货运量更高的地区可能会更快采用这项技术。此外,联网汽车技术的日益普及、货运运营数位化的提高以及物流行业持续推进的永续性倡议,也都在促进市场成长。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 起始值 | 1.695亿美元 |

| 预测金额 | 11.6亿美元 |

| 复合年增长率 | 21.5% |

到2025年,驾驶辅助卡车编队行驶(DATP)市占率将达到95.1%。 DATP系统至少需要一名驾驶员领头,而后方卡车则保持半自动驾驶状态。由于道路基础设施限制、交通密度和监管限制等因素,全自动驾驶编队行驶面临许多挑战,预计这种主导地位在可预见的未来仍将持续。依赖人工操作既能确保安全,又能让物流业者享受到降低油耗和提高编队行驶效率带来的益处。随着技术和监管法规结构日趋成熟,最终实现全自动驾驶解决方案,DATP也为车队提供了一个切实可行的过渡方案。

预计2026年至2035年间,车联网(V2X)技术领域将以23.1%的复合年增长率成长。 V2X技术能够实现车辆、基础设施和驾驶辅助系统之间的无缝连接,从而实现车队内部的即时协调。该技术的应用提高了车队行驶的效率、安全性和准确性,使加速、煞车和路线管理更加平稳。随着V2X技术的日益成熟,其与数位双胞胎模拟和自动驾驶车辆控制等先进技术的整合有望进一步提升卡车车队行驶系统的性能和扩充性。

预计到2025年,美国卡车编队行驶市场规模将达5,300万美元。政府政策以及联邦和州政府机构之间的合作正在推动这项技术从封闭测试场地向公共公路上的实际货运运营过渡。美国运输部已将卡车编队行驶确定为自动驾驶车辆在货运领域的早期应用之一,并正在推动各州之间的合作,以协调安全法规、发展基础设施并制定营运策略。推动市场成长的因素包括驾驶辅助系统的普及、相关立法的支持以及提高长途运输网路效率和降低成本的需求。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 由于燃油成本上涨,需要削减开支

- 车对车(V2V)技术的进步

- 扩大ADAS(进阶驾驶辅助系统)的应用

- 政府对互联和自动驾驶交通的支持

- 产业潜在风险与挑战

- 网路安全和资料隐私问题

- 新兴经济体基础建设发展落后

- 市场机会

- 与 L2-L4 级自动驾驶卡车解决方案集成

- 在专用货运走廊引入

- 汽车製造商、车队营运商和技术提供者之间的伙伴关係

- 大型物流和电子商务车队的采用情况

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国联邦自动驾驶汽车政策指南(NHTSA 指南)

- 联邦自动驾驶汽车法案

- 加拿大运输部指南

- 各州自动驾驶汽车法律

- 欧洲

- 联合国第157号条例-自动车道维持系统(ALKS)

- 欧盟法规(EU)

- 自动驾驶法案

- 亚太地区

- 中国的自动驾驶道路测试法规

- 日本道路交通法与汽车运输业务法

- 东协自动驾驶汽车现状

- 拉丁美洲

- 巴西自动驾驶汽车测试指南

- 智利批准自动驾驶汽车飞行员

- RCEP区域技术合作框架

- 中东和非洲

- 阿联酋/杜拜自动驾驶运输战略和卡车框架

- 南非自动驾驶/联网汽车政策草案

- 北美洲

- 波特分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 成本細項分析

- 永续性和环境影响

- 环境影响评估

- 社会影响力和社区服务

- 公司管治与企业社会责任

- 永续金融与投资趋势

- 案例研究

- 车队经济性、投资收益报酬率 (ROI) 和投资回收期分析

- 商业化准备与应用成熟度评估

- 优先考虑有前景的走廊和用例

- 硬体架构和初始投资分析

- 软体和业务收益货币化模式

- 编队软体堆迭

- 供应商使用的定价模式

- 订阅和定期收费结构

- 营运服务成本

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 市场估价与预测:编队行驶,2022-2035年

- 驾驶员辅助卡车编队行驶(DATP)

- 自动驾驶卡车编队行驶

第六章 按组件分類的市场估算与预测,2022-2035年

- 硬体

- 雷达

- LiDAR

- 相机

- 其他硬体

- 软体

- 服务

7. 通讯技术市场估算与预测,2022-2035年

- 车对车(V2V)通信

- 车路通讯(V2I)

- Vehicle-to-Everything(V2X)

第八章 按车辆类型分類的市场估算与预测,2022-2035年

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 新加坡

- 马来西亚

- 印尼

- 越南

- 泰国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 世界公司

- Daimler Truck

- Volvo

- Scania

- Continental

- IVECO

- MAN Truck &Bus

- DAF Trucks

- ZF Friedrichshafen

- Robert Bosch

- Knorr-Bremse

- Plus(PlusAI)

- 当地公司

- Kratos Defense &Security Solutions

- Waabi

- Gatik

- Bendix Commercial Vehicle Systems

- Denso

- Hyundai Motor

- 新兴企业

- UD Trucks

- Hino Motors

- Cohda Wireless

The Global Truck Platooning Market was valued at USD 169.5 million in 2025 and is estimated to grow at a CAGR of 21.5% to reach USD 1.16 billion by 2035.

The market growth is driven by increasing interest from logistics and transportation companies seeking efficiency, fuel savings, and safety improvements along frequently used routes. Governments worldwide are actively supporting pilot programs and on-road trials, carefully evaluating factors such as road infrastructure, deployment costs, safety, and risk management. As truck platooning technology matures and becomes commercially viable, major logistics and e-commerce players are expected to be early adopters, deploying platooning in their fleets to improve operational efficiency. Regions with strong regulatory support, robust transportation networks, and higher freight volumes are poised to experience faster adoption. The market is also benefiting from the rise of connected vehicle technologies, increasing digitalization in freight operations, and the ongoing push toward sustainability in the logistics industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $169.5 Million |

| Forecast Value | $1.16 Billion |

| CAGR | 21.5% |

The driver-assistive truck platooning (DATP) segment held a 95.1% share in 2025. DATP systems require at least one driver to lead the convoy, while following trucks remain semi-automated. This dominance is expected to continue in the near term as fully autonomous platooning faces challenges due to road infrastructure limitations, traffic density, and regulatory constraints. The reliance on a human operator ensures safety while allowing logistics operators to benefit from reduced fuel consumption and improved convoy efficiency. DATP also provides a practical transition stage for fleets as technology and regulatory frameworks mature toward fully autonomous solutions.

The vehicle-to-everything (V2X) communication technology segment is projected to grow at a CAGR of 23.1% from 2026 to 2035. V2X enables seamless connectivity between vehicles, infrastructure, and driver assistance systems, allowing real-time coordination within platoons. Its adoption is driving efficiency, safety, and precision in convoy operations, enabling smoother acceleration, braking, and route management. As V2X matures, it is expected to integrate with advanced technologies such as digital twin simulations and autonomous vehicle controls, further enhancing the performance and scalability of truck platooning systems.

U.S. Truck Platooning Market reached USD 53 million in 2025. The market is transitioning from closed-track testing to actual freight operations on public highways, supported by government policies and collaborative efforts between federal and state agencies. The U.S. Department of Transportation has identified truck platooning as one of the earliest applications of automated vehicles in freight, encouraging partnerships between states to align safety regulations, develop infrastructure, and plan operational strategies. Growth is driven by the adoption of driver-assistive systems, supportive legislation, and the need for greater efficiency and cost savings in long-haul transportation networks.

Major players operating in the Global Truck Platooning Market include MAN Truck & Bus, Daimler Truck, Volvo, IVECO, Robert Bosch, Kratos, Scania, Knorr-Bremse, Continental, and DAF Trucks. These companies lead through technological innovation, strategic partnerships, and early involvement in pilot programs, ensuring strong positions in the emerging truck platooning market. They continue to invest in R&D, autonomous driving technologies, and connected vehicle systems to meet evolving market demands and regulatory requirements. Companies in the Global Truck Platooning Market are employing several strategies to strengthen their foothold. They focus on technological innovation, including the development of V2X-enabled systems, driver-assistive solutions, and autonomous-ready platooning platforms. Strategic partnerships with logistics operators, e-commerce companies, and government agencies accelerate testing, adoption, and infrastructure readiness. Mergers and acquisitions are used to consolidate expertise, expand geographic reach, and enhance product portfolios.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Platooning

- 2.2.3 Component

- 2.2.4 Communication Technology

- 2.2.5 Vehicle

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising fuel cost reduction imperative

- 3.2.1.2 Advancements in vehicle-to-vehicle (V2V) communication

- 3.2.1.3 Growing adoption of advanced driver assistance systems (ADAS)

- 3.2.1.4 Government support for connected and autonomous mobility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity and data privacy concerns

- 3.2.2.2 Limited infrastructure readiness in emerging economies

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with level 2-4 autonomous trucking solutions

- 3.2.3.2 Deployment in dedicated freight corridors

- 3.2.3.3 Partnerships between OEMs, fleet operators, and tech providers

- 3.2.3.4 Adoption by large logistics and e-commerce fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Federal AV Policy Guidance (NHTSA Guidelines)

- 3.4.1.2 Federal AV Legislation Bills

- 3.4.1.3 Transport Canada Guidelines

- 3.4.1.4 State Autonomous Vehicle Laws

- 3.4.2 Europe

- 3.4.2.1 UN Regulation No. 157 - Automated Lane Keeping Systems (ALKS)

- 3.4.2.2 EU Regulation (EU)

- 3.4.2.3 Automated Driving Act

- 3.4.3 Asia Pacific

- 3.4.3.1 China Autonomous Driving Road Test Regulations

- 3.4.3.2 Japan Road Traffic Act & Road Transport Vehicle Act

- 3.4.3.3 ASEAN Autonomous Vehicle Landscape

- 3.4.4 Latin America

- 3.4.4.1 Brazil Autonomous Vehicle Testing Guidelines

- 3.4.4.2 Chile Autonomous AV Pilot Approvals

- 3.4.4.3 RCEP Regional Tech Collaboration Framework

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE / Dubai Autonomous Transportation Strategy & Truck Framework

- 3.4.5.2 South Africa Automated/Connected Vehicle Policy Drafts

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Sustainability and environmental impact

- 3.9.1 Environmental impact assessment

- 3.9.2 Social impact & community benefits

- 3.9.3 Governance & corporate responsibility

- 3.9.4 Sustainable finance & investment trends

- 3.10 Case studies

- 3.11 Fleet economics, ROI & payback analysis

- 3.12 Commercial readiness & deployment maturity assessment

- 3.13 High-potential corridors & use-case prioritization

- 3.14 Hardware architecture & upfront investment analysis

- 3.15 Software & service monetization model

- 3.15.1 Platooning software stack

- 3.15.2 Pricing models used by vendors

- 3.15.3 Subscription & recurring fee structure

- 3.15.4 Operational service costs

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Platooning, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Driver-Assistive Truck Platooning (DATP)

- 5.3 Autonomous Truck Platooning

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Radar

- 6.2.2 Lidar

- 6.2.3 Camera

- 6.2.4 Other Hardware

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates & Forecast, By Communication Technology, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Vehicle-to-Vehicle (V2V)

- 7.3 Vehicle-to-Infrastructure (V2I)

- 7.4 Vehicle-to-Everything (V2X)

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Light Commercial Vehicle (LCV)

- 8.3 Medium Commercial Vehicle (MCV)

- 8.4 Heavy Commercial Vehicle (HCV)

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Benelux

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.4.10 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Daimler Truck

- 10.1.2 Volvo

- 10.1.3 Scania

- 10.1.4 Continental

- 10.1.5 IVECO

- 10.1.6 MAN Truck & Bus

- 10.1.7 DAF Trucks

- 10.1.8 ZF Friedrichshafen

- 10.1.9 Robert Bosch

- 10.1.10 Knorr-Bremse

- 10.1.11 Plus (PlusAI)

- 10.2 Regional companies

- 10.2.1 Kratos Defense & Security Solutions

- 10.2.2 Waabi

- 10.2.3 Gatik

- 10.2.4 Bendix Commercial Vehicle Systems

- 10.2.5 Denso

- 10.2.6 Hyundai Motor

- 10.3 Emerging companies

- 10.3.1 UD Trucks

- 10.3.2 Hino Motors

- 10.3.3 Cohda Wireless

2026年全球卡车排队市场报告2026年全球轨道自动跟车系统市场报告2026年全球汽车自动跟车系统市场报告

2026年全球卡车排队市场报告2026年全球轨道自动跟车系统市场报告2026年全球汽车自动跟车系统市场报告 2026-2034年全球汽车自动跟车系统市场规模、份额、趋势和成长分析报告全球卡车编队行驶市场规模、份额、趋势和成长分析报告(2026-2034)

2026-2034年全球汽车自动跟车系统市场规模、份额、趋势和成长分析报告全球卡车编队行驶市场规模、份额、趋势和成长分析报告(2026-2034) 卡车编队行驶市场 - 全球产业规模、份额、趋势、机会及预测(按技术类型、基础设施类型、自动化程度、地区和竞争格局划分,2021-2031年)

卡车编队行驶市场 - 全球产业规模、份额、趋势、机会及预测(按技术类型、基础设施类型、自动化程度、地区和竞争格局划分,2021-2031年) 自动车辆调度系统的全球市场

自动车辆调度系统的全球市场 卡车排队:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)全球卡车排队市场

卡车排队:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)全球卡车排队市场 至 2030 年卡车编队市场预测:按车辆类型、编队配置、自动化等级、通讯模型、技术、应用、最终用户和地区进行全球分析

至 2030 年卡车编队市场预测:按车辆类型、编队配置、自动化等级、通讯模型、技术、应用、最终用户和地区进行全球分析