|

市场调查报告书

商品编码

1928999

活动物流市场机会、成长要素、产业趋势分析及预测(2026-2035年)Event Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

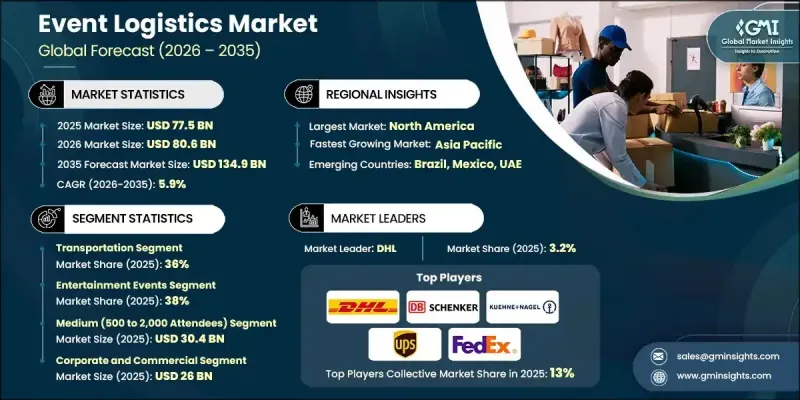

全球活动物流市场预计到 2025 年将达到 775 亿美元,到 2035 年将达到 1,349 亿美元,年复合成长率为 5.9%。

全球大型活动日益频繁,以及对高度协调、时效性强的物流服务需求不断增长,推动了市场扩张。活动组织者越来越重视复杂供应链的精准性、可靠性和成本控制,以确保营运顺畅,并为与会者带来正面的体验。随着活动日益复杂化和地理分散,对能够实现严格日程管理、最大限度降低营运风险并确保从策划到后续营运无缝协调的物流解决方案的需求也日益增长。此外,数位转型的广泛应用也推动了市场发展,物流供应商采用先进技术,提高了透明度、准确性和应对力速度。即时可见性和数据驱动的决策对于满足不断变化的客户期望至关重要。向整合式端到端物流模式的转变,提高了资源利用率、扩充性和跨多个活动场地的一致性。这些发展趋势正在强化专业活动物流供应商作为策略伙伴而非仅仅是供应商的角色。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 775亿美元 |

| 预测金额 | 1349亿美元 |

| 复合年增长率 | 5.9% |

2025年,运输环节占比达36%,预计2026年至2035年将以4.6%的复合年增长率成长。此环节占据核心地位,因为它负责确保活动相关资产的及时运输。数位追踪、连网监控系统和智慧路线规划平台的日益普及,正在提升交付的准确性和准时性。

预计到 2025 年,娱乐活动领域将占 38% 的市场份额,从 2026 年到 2035 年,年复合成长率将达到 7.1%。高营运强度和复杂的协调要求推动了该领域对技术赋能型物流解决方案的强烈依赖,从而巩固了其主导地位。

预计到 2025 年,美国活动物流市场规模将达到 230 亿美元,占全球市场份额的 83%。该地区的主导地位得益于先进的基础设施和对数位化物流平台的早期采用,这些平台提高了效率、监控和协调能力。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 全球事件数量不断增加

- 对准时可靠交货的需求

- 采用数位化和智慧物流技术

- 企业品牌和体验式行销的成长

- 产业潜在风险与挑战

- 操作复杂度高且风险大

- 利润空间有限,成本敏感度高。

- 市场机会

- 拓展混合式、虚拟式和全球性活动

- 永续且环保的活动物流解决方案

- 扩展基于云端的整合平台

- 推出利用人工智慧和机器学习的物流解决方案

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国:OSHA 和联邦活动安全指南

- 加拿大:运输部和职业安全与健康指南

- 欧洲

- 德国:BMVI 和 DGUV 法规

- 法国:DGME 和 CNES 指南

- 英国:海事和海洋事务部 (MCA) 和健康与安全执行局 (HSE) 的相关规定

- 义大利:ENAC 和 INAIL 指南

- 亚太地区

- 中国:运输部和活动安全法规

- 日本:JCAB 和国土交通省指南

- 韩国:国土交通旅游部安全指南

- 印度:航运部和码头安全规则

- 拉丁美洲

- 巴西:ANTAQ 和基础设施部指南

- 墨西哥:SEMAR 和 DGPM 法规

- 中东和非洲

- 阿联酋:能源和基础设施部法规

- 沙乌地阿拉伯:沙乌地阿拉伯港务局指南

- 北美洲

- 波特分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 使用案例场景

- 定价、商业和收入模式分析

- 需求面购买行为与决策框架

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 按服务分類的市场估算与预测,2022-2035年

- 运输

- 仓储服务

- 库存管理

- 现场安装和拆卸

- 物流规划与协调

- 其他的

第六章 依活动规模分類的市场估计与预测,2022-2035年

- 小规模(最多500人)

- 中等规模(500至2000人)

- 大型(2000 至 10000 人)

- 超大规模(超过10,000人)

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 企业活动

- 体育赛事

- 娱乐活动

- 公共活动

- 私人活动

第八章 依最终用途分類的市场估算与预测,2022-2035年

- 公司及商业

- 娱乐与媒体

- 运动的

- 政府/公共部门

- 教育机构

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Global Player

- CH Robinson

- CEVA Logistics

- DB Schenker

- DHL

- DSV Panalpina

- FedEx

- Kuehne+Nagel

- Nippon Express

- UPS

- XPO Logistics

- Regional Player

- Agility Logistics

- Bollore Logistics

- DB Cargo Logistics

- GEFCO

- Geodis

- Hellmann Worldwide Logistics

- Kerry Logistics

- Mainfreight

- Rhenus Logistics

- TVS Supply Chain Solutions

- 新兴企业

- Flexport

- Locus Logistics

- OnTime Logistics

- Senpex

- ShipMonk

The Global Event Logistics Market was valued at USD 77.5 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 134.9 billion by 2035.

Market expansion is supported by the rising frequency of large-scale events worldwide and the growing need for highly coordinated, time-sensitive logistics services. Event organizers are increasingly prioritizing precision, reliability, and cost control across complex supply chains to ensure smooth execution and positive participant experiences. As events become more sophisticated and geographically dispersed, demand is increasing for logistics solutions that can manage tight schedules, minimize operational risks, and deliver seamless coordination from planning through post-event operations. The market is also benefiting from widespread digital transformation, as logistics providers adopt advanced technologies to enhance transparency, accuracy, and responsiveness. Real-time visibility and data-driven decision-making are becoming essential to meet evolving client expectations. The shift toward integrated, end-to-end logistics models is enabling better resource utilization, scalability, and consistency across multiple event locations. These developments are reinforcing the role of specialized event logistics providers as strategic partners rather than basic service vendors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $77.5 Billion |

| Forecast Value | $134.9 Billion |

| CAGR | 5.9% |

The transportation segment held 36% share in 2025 and is expected to grow at a CAGR of 4.6% from 2026 to 2035. This segment holds a central position due to its responsibility for ensuring the timely movement of event-related assets. Increased use of digital tracking, connected monitoring systems, and intelligent routing platforms is improving delivery accuracy and schedule adherence.

The entertainment events segment accounted for 38% share in 2025 and is projected to grow at a CAGR of 7.1% from 2026 to 2035. High operational intensity and complex coordination requirements are driving strong reliance on technology-enabled logistics solutions within this segment, supporting its leading position.

United States Event Logistics Market held 83% share and generated USD 23 billion in 2025. Regional leadership is supported by advanced infrastructure and early adoption of digital logistics platforms that enhance efficiency, monitoring, and coordination.

Key companies operating in the Global Event Logistics Market include DHL, UPS, FedEx, Kuehne + Nagel, DB Schenker, C.H. Robinson, XPO Logistics, CEVA Logistics, Nippon Express, and DSV Panalpina. Companies in the Global Event Logistics Market are strengthening their competitive position through technology integration, service diversification, and global network expansion. Many providers are investing in digital platforms that enable real-time visibility, predictive planning, and centralized coordination across event supply chains. Expanding end-to-end service offerings allows companies to manage transportation, storage, on-site handling, and reverse logistics more efficiently. Strategic partnerships with event organizers and venue operators help secure long-term contracts. Firms are also enhancing sustainability initiatives by optimizing routes and reducing emissions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Event Size

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Number of Global Events

- 3.2.1.2 Need for Time-Critical & Reliable Delivery

- 3.2.1.3 Adoption of Digital & Smart Logistics Technologies

- 3.2.1.4 Growth of Corporate Branding & Experiential Marketing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Operational Complexity & Risk

- 3.2.2.2 Limited Margins & High-Cost Sensitivity

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of hybrid, virtual & global events

- 3.2.3.2 Sustainable & green event logistics solutions

- 3.2.3.3 Expansion of cloud-based and integrated platforms

- 3.2.3.4 Adoption of AI- and ML-driven logistics solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: OSHA & Federal Event Safety Guidelines

- 3.4.1.2 Canada: Transport Canada & WorkSafe Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: BMVI & DGUV Regulations

- 3.4.2.2 France: DGME & CNES Guidelines

- 3.4.2.3 UK: MCA & HSE Regulations

- 3.4.2.4 Italy: ENAC & INAIL Guidelines

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Transport & Event Safety Regulations

- 3.4.3.2 Japan: JCAB & MLIT Guidelines

- 3.4.3.3 South Korea: MOLIT & Safety Guidelines

- 3.4.3.4 India: Ministry of Shipping & Dock Safety Rules

- 3.4.4 Latin America

- 3.4.4.1 Brazil: ANTAQ & Ministry of Infrastructure Guidelines

- 3.4.4.2 Mexico: SEMAR & DGPM Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Ministry of Energy & Infrastructure Regulations

- 3.4.5.2 Saudi Arabia: Saudi Ports Authority Guidelines

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 Pricing, Commercial & Revenue Model Analysis

- 3.14 Demand-Side Buying Behavior & Decision Framework

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Transportation

- 5.3 Warehousing and storage

- 5.4 Inventory management

- 5.5 On-site setup and dismantling

- 5.6 Logistics planning and Coordination

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Event Size, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Small (up to 500 attendees)

- 6.3 Medium (500 to 2,000 attendees)

- 6.4 Large (2,000 to 10,000 attendees)

- 6.5 Mega (over 10,000 attendees)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Corporate Events

- 7.3 Sports Events

- 7.4 Entertainment Events

- 7.5 Public Events

- 7.6 Private Events

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Corporate and commercial

- 8.3 Entertainment & media

- 8.4 Sports

- 8.5 Government & public sector

- 8.6 Educational institutions

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global Player

- 10.1.1 C.H. Robinson

- 10.1.2 CEVA Logistics

- 10.1.3 DB Schenker

- 10.1.4 DHL

- 10.1.5 DSV Panalpina

- 10.1.6 FedEx

- 10.1.7 Kuehne + Nagel

- 10.1.8 Nippon Express

- 10.1.9 UPS

- 10.1.10 XPO Logistics

- 10.2 Regional Player

- 10.2.1 Agility Logistics

- 10.2.2 Bollore Logistics

- 10.2.3 DB Cargo Logistics

- 10.2.4 GEFCO

- 10.2.5 Geodis

- 10.2.6 Hellmann Worldwide Logistics

- 10.2.7 Kerry Logistics

- 10.2.8 Mainfreight

- 10.2.9 Rhenus Logistics

- 10.2.10 TVS Supply Chain Solutions

- 10.3 Emerging Players

- 10.3.1 Flexport

- 10.3.2 Locus Logistics

- 10.3.3 OnTime Logistics

- 10.3.4 Senpex

- 10.3.5 ShipMonk

全球活动物流市场:市场规模、份额、趋势分析(按类型、应用和地区)、展望和预测(2025-2032 年)

全球活动物流市场:市场规模、份额、趋势分析(按类型、应用和地区)、展望和预测(2025-2032 年) 活动物流市场:全球2025-2029

活动物流市场:全球2025-2029 活动物流市场分析及预测至 2033 年:依类型、产品、服务、技术、组件、应用、流程、最终用户、解决方案、阶段

活动物流市场分析及预测至 2033 年:依类型、产品、服务、技术、组件、应用、流程、最终用户、解决方案、阶段 亚太活动物流:市场占有率分析、产业趋势与成长预测(2025-2030 年)

亚太活动物流:市场占有率分析、产业趋势与成长预测(2025-2030 年) 亚太地区活动物流市场预测至 2031 年 - 区域分析 - 按类型和最终用户

亚太地区活动物流市场预测至 2031 年 - 区域分析 - 按类型和最终用户 北美活动物流市场预测至 2031 年 - 区域分析 - 按类型和最终用户

北美活动物流市场预测至 2031 年 - 区域分析 - 按类型和最终用户 欧洲活动物流市场预测至 2031 年 - 区域分析 - 按类型和最终用户

欧洲活动物流市场预测至 2031 年 - 区域分析 - 按类型和最终用户 活动物流市场规模、份额、趋势分析报告:按类型、按应用、按地区、细分市场预测,2024-2030 年

活动物流市场规模、份额、趋势分析报告:按类型、按应用、按地区、细分市场预测,2024-2030 年 活动物流市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按类型、最终用户和地理位置

活动物流市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按类型、最终用户和地理位置