|

市场调查报告书

商品编码

1929002

碱性电池市场机会、成长要素、产业趋势分析及2026年至2035年预测Alkaline Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

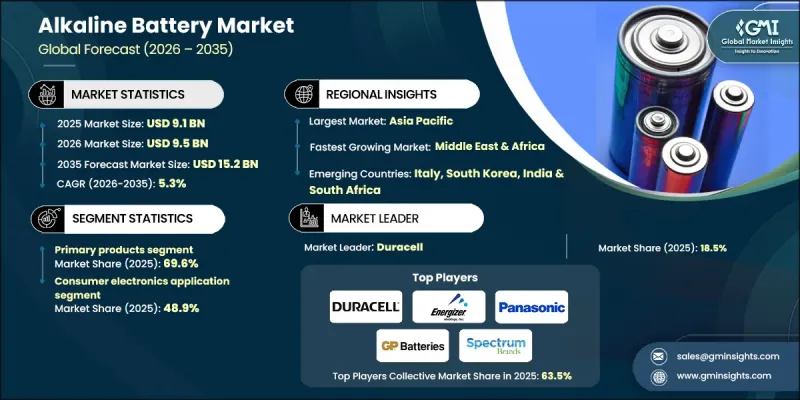

全球碱性电池市场预计到 2025 年将达到 91 亿美元,到 2035 年将达到 152 亿美元,年复合成长率为 5.3%。

市场扩张的驱动力在于消费者对无需特殊处理、充电基础设施或定期维护的低成本电池日益增长的需求。碱性电池因其可靠性、能源效率和低洩漏风险,被广泛认可为主要电源,其采用碱性电解液系统,可提供稳定的电化学性能和较长的保质期。碱性电池的可靠性、能源效率和低洩漏风险使其在住宅和商业环境中广泛应用。人们对携带式、高耗能电子设备的依赖性日益增强,推动了对能够在长时间使用循环中提供稳定电力的电池的需求。随着日常生活数位化,消费者越来越重视电池的耐用性、易用性和可靠性。不断增强的环保意识也在影响产品开发,製造商正投资研发无汞碱性电池,以满足永续性预期和监管标准。旨在提高能量密度和安全性的持续技术创新正在增强长期需求,并支撑市场稳步成长。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 91亿美元 |

| 预测金额 | 152亿美元 |

| 复合年增长率 | 5.3% |

预计到2025年,一次碱性电池市占率将达到69.6%,并在2035年之前以5.1%的复合年增长率成长。一次性电池无需额外设备即可立即使用,因其便利性和可靠性,市场需求不断增长。终端用户在需要快速更换和不间断运行的应用场景中,尤其是在家庭和职场环境中,更倾向于选择此类产品。

预计到2025年,家用电子电器应用领域将占据48.9%的市场份额,并在2026年至2035年间以4.8%的复合年增长率成长。该领域的成长主要得益于现代电子产品对高能量密度、小巧便携电源的需求。由于碱性电池具有稳定的功率输出和可靠的使用寿命,製造商和消费者仍然青睐此类电池。

预计到2025年,美国碱性电池市占率将达到95.9%,到2035年将成长至32亿美元。消费者对价格实惠且可靠的电源解决方案的强劲需求持续推动着碱性电池在美国的普及。较长的保质期和稳定的性能也使其在美国不断增长的电子产品市场中得以继续使用。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系统

- 原物料供应及采购分析

- 製造能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 成本结构分析

- 波特分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

- 新的机会与趋势

- 数位化和物联网集成

- 拓展新兴市场

- 投资分析及未来展望

第四章 竞争情势

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 战略仪錶板

- 策略倡议

- 企业标竿管理

- 创新与科技趋势

第五章 2022-2035年依产品分類的市场规模及预测

- 基本的

- 次要

第六章 依应用领域分類的市场规模及预测(2022-2035年)

- 家用电子电器

- 玩具

- 其他的

第七章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 亚太地区

- 中国

- 澳洲

- 印度

- 日本

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第八章 公司简介

- Camelion Batterien

- Duracell

- Energizer Holding

- FDK Corporation

- Geti.eu

- GPB International Limited

- ISKRA

- Kodak

- Maxell Holdings

- Nanfu

- Panasonic Corporation

- Sanyo

- Sony

- Spectrum Brands Holdings

- Tenergy

- Toshiba International

- Urban Electric Power

- VARTA Consumer Batteries

- Voniko Batteries

- Zhejiang Mustang Battery

The Global Alkaline Battery Market was valued at USD 9.1 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 15.2 billion by 2035.

Market expansion is supported by rising demand for cost-efficient batteries that do not require special handling, charging infrastructure, or routine maintenance. Alkaline batteries are widely recognized as primary power sources that operate through an alkaline electrolyte system, enabling stable electrochemical performance and extended shelf life. Their reputation for reliability, energy efficiency, and reduced leakage risk continues to support adoption across residential and commercial environments. Growing reliance on portable and energy-intensive electronic equipment is increasing the need for batteries capable of delivering consistent output over longer usage cycles. Consumers increasingly prioritize durability, ease of use, and dependable performance as daily routines become more digitally oriented. Environmental awareness is also shaping product development, with manufacturers investing in mercury-free alkaline batteries to meet sustainability expectations and regulatory standards. Continuous innovation aimed at improving energy density and safety is reinforcing long-term demand and supporting steady market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.1 Billion |

| Forecast Value | $15.2 Billion |

| CAGR | 5.3% |

The primary alkaline batteries segment accounted for 69.6% share in 2025 and is projected to grow at a CAGR of 5.1% through 2035. Demand for single-use batteries that are immediately functional without additional equipment is increasing due to their simplicity and reliability. End users favor these products for applications where quick replacement and uninterrupted performance are essential, particularly in household and workplace settings.

The consumer electronics application segment held a 48.9% share in 2025 and is anticipated to grow at a CAGR of 4.8% from 2026 to 2035. Growth in this segment is driven by the need for compact power sources with high energy density that can support consistent operation of modern electronic products. Manufacturers and consumers alike continue to favor alkaline batteries for their stable output and dependable lifespan.

United States Alkaline Battery Market held 95.9% share in 2025 and is expected to generate USD 3.2 billion by 2035. Strong demand for affordable and reliable power solutions continues to drive adoption nationwide. Long storage life and consistent performance support ongoing use as the domestic electronics market continues to expand.

Prominent companies operating in the Global Alkaline Battery Market include Duracell, Panasonic Corporation, Energizer Holding, VARTA Consumer Batteries, Toshiba International, Nanfu, Maxell Holdings, Spectrum Brands Holdings, Sony, Camelion Batterien, Kodak, GPB International Limited, FDK Corporation, Tenergy, Zhejiang Mustang Battery, Geti.eu, ISKRA, Sanyo, Urban Electric Power, and Voniko Batteries. Companies in the Alkaline Battery Market are strengthening their market position through product innovation, sustainability initiatives, and global distribution expansion. Many manufacturers are investing in mercury-free and environmentally responsible designs to meet regulatory requirements and align with consumer expectations. Brand differentiation through improved energy efficiency and longer shelf life remains a key focus. Firms are also expanding manufacturing capacity and optimizing supply chains to ensure consistent product availability. Strategic partnerships with retailers and private-label offerings are helping increase market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.2 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Porter';s analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Primary

- 5.3 Secondary

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Toys

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Camelion Batterien

- 8.2 Duracell

- 8.3 Energizer Holding

- 8.4 FDK Corporation

- 8.5 Geti.eu

- 8.6 GPB International Limited

- 8.7 ISKRA

- 8.8 Kodak

- 8.9 Maxell Holdings

- 8.10 Nanfu

- 8.11 Panasonic Corporation

- 8.12 Sanyo

- 8.13 Sony

- 8.14 Spectrum Brands Holdings

- 8.15 Tenergy

- 8.16 Toshiba International

- 8.17 Urban Electric Power

- 8.18 VARTA Consumer Batteries

- 8.19 Voniko Batteries

- 8.20 Zhejiang Mustang Battery

全球碱性电池市场规模、份额、趋势和成长分析报告(2026-2034年)

全球碱性电池市场规模、份额、趋势和成长分析报告(2026-2034年) 锂碳氟化物纽扣电池市场(按电池尺寸、应用、最终用户和分销管道划分)—2026-2032年全球预测全球碱性电池市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

锂碳氟化物纽扣电池市场(按电池尺寸、应用、最终用户和分销管道划分)—2026-2032年全球预测全球碱性电池市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 碱性电池市场规模、份额和成长分析(按产品、规格、应用和地区划分):产业预测(2026-2033 年)碱性电池市场-2025年至2030年预测

碱性电池市场规模、份额和成长分析(按产品、规格、应用和地区划分):产业预测(2026-2033 年)碱性电池市场-2025年至2030年预测 碱性电池市场-全球产业规模、份额、趋势、机会和预测,按电池类型(一次碱性电池、二次碱性电池)、按规模、按最终用途行业、按地区和竞争情况细分,2020 年至 2030 年

碱性电池市场-全球产业规模、份额、趋势、机会和预测,按电池类型(一次碱性电池、二次碱性电池)、按规模、按最终用途行业、按地区和竞争情况细分,2020 年至 2030 年 碱性电池全球市场,2025-2029

碱性电池全球市场,2025-2029 一次性薄膜电池市场机会、成长动力、产业趋势分析及2025-2034年预测

一次性薄膜电池市场机会、成长动力、产业趋势分析及2025-2034年预测 碱性电池:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

碱性电池:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 2030 年碱性电池市场预测:按产品、电池尺寸、外形规格、容量、价格、分销管道、应用、最终用户和地区进行的全球分析

2030 年碱性电池市场预测:按产品、电池尺寸、外形规格、容量、价格、分销管道、应用、最终用户和地区进行的全球分析