|

市场调查报告书

商品编码

1929005

汽车轮胎电子零售市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)Automotive Tires E-Retailing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

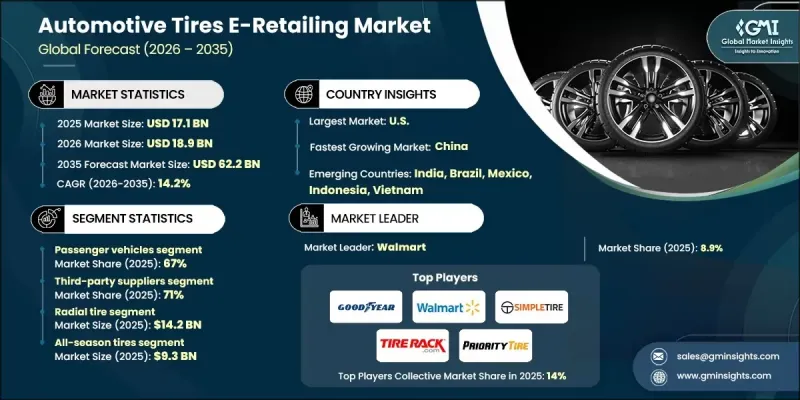

全球汽车轮胎电子零售市场预计到 2025 年将达到 171 亿美元,到 2035 年将达到 622 亿美元,年复合成长率为 14.2%。

市场成长正受到视觉和互动式数位商务工具在线上轮胎零售平台快速整合的影响。数位零售体验日趋沉浸式,使客户能够在购买前更好地评估产品,并做出更自信、更明智的决策。这种转变正在提升客户参与,降低产品退货率,并提高线上经销商的转换率。先进的数位展示室和配置工具的日益普及,使轮胎经销商能够在竞争激烈的市场环境中脱颖而出,同时提升整体客户满意度。专注于轮胎轮换週期、维护计划和季节性使用模式的订阅服务也在改变消费者的购买行为。这些模式使客户能够摆脱一次性购买,选择灵活且经济实惠的服务计划。这种模式正受到追求便利性和可预测支出的用户的青睐。预测分析技术透过基于使用数据实现最佳更换提案,进一步推动了这一发展,从而有助于提升客户终身价值。人工智慧驱动的建议引擎持续影响购买决策,并正在重新定义消费者在线上购买轮胎的方式。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 171亿美元 |

| 预测金额 | 622亿美元 |

| 复合年增长率 | 14.2% |

预计到2025年,乘用车市场将占据67%的市场份额,并在2026年至2035年间以14%的复合年增长率成长。不断增长的车辆保有量和更长的车辆使用週期支撑了市场需求,并持续推动轮胎更换需求。由于便于价格比较、获取用户回馈以及简化购买流程,线上平台越来越受到消费者的青睐。随着越来越多的车辆运作时间延长,透过数位化管道购买替换轮胎的需求持续成长。消费者优先考虑便利性和速度,电商平台正透过简化的流程和高效率的购买方式来满足这些期望。

预计到2025年,第三方供应商将占据71%的市场份额,并在2026年至2035年间以13.5%的复合年增长率成长。主导地位得益于涵盖多个品牌、规格和价格范围的丰富产品线。强大的采购网路和基于批量筹资策略使其能够在保持性能和安全标准的同时,提供具有竞争力的价格。这种以价值为导向的提案符合线上购物者的期望,并持续巩固其市场地位。

预计到2025年,美国汽车轮胎电商市场将占据82%的市场份额,销售额将达到40亿美元。美国较高的汽车保有量和稳定的轮胎更换需求支撑着该国的线上轮胎销售。消费者越来越倾向选择产品种类丰富、价格优惠且提供宅配服务的线上管道。零售商则透过会员奖励和灵活的数位支付解决方案进一步推动销售成长,提升了产品的可负担性和便利性。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 扩大线上轮胎市场

- 消费者越来越倾向于直接面向消费者的销售方式

- 汽车零售业数位化兴起

- 消费者对便利性的偏好日益增强

- 产业潜在风险与挑战

- 由于尺寸选择错误导致退货率高

- 购买前检查实物的能力有限

- 对最后一公里物流和安装人员的依赖

- 在线经销商之间的价格竞争

- 市场机会

- 基于人工智慧的轮胎推荐引擎

- 订阅模式和轮胎即服务模式

- 电动车轮胎需求不断成长

- 新兴市场的扩张

- 与安装商和服务网络建立合作关係

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- FMVSS - 联邦机动车辆安全标准(轮胎)

- 加拿大车辆安全标准(CVSS)

- 欧洲

- UNECE R117/E 标誌认证

- EUDR-欧盟森林砍伐法规

- 轮胎标记法规(欧盟 2020/740)

- 亚太地区

- 轮胎中国强制产品认证(CCC)

- 生产者延伸责任制(EPR)

- 日本轮胎工业标准(JIS)

- 拉丁美洲

- INMETRO轮胎认证和标记系统

- IRAM/区域轮胎标准

- 车辆和轮胎符合欧洲标准

- 中东和非洲

- 具备RFID功能的轮胎识别标籤

- SASO轮胎性能和耐热标准

- EPR轮胎回收/废弃物管理标准

- 北美洲

- 波特分析

- PESTEL 分析

- 专利分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 生产统计

- 生产基地

- 进出口

- 主要进口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 消费者购买过程与决策因素

- 关键线上决策参数(价格、评价、适用性工具)

- 人工智慧轮胎推荐引擎的作用

- 比较工具、使用者评论和评分的影响

- 付款方式偏好

- 未来市场展望与结构性变化

- 向全通路轮胎零售的转型

- 订阅轮胎服务的成长

- 加快製造商直接向消费者销售的速度

- 电子零售平台整合展望

第四章 竞争情势

- 介绍

- 公司市占率分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 依轮胎类型分類的市场估计与预测,2022-2035年

- 全天候轮胎

- 夏季轮胎

- 冬季轮胎

- 其他的

6. 按产品类型分類的市场估算与预测,2022-2035年

- 子午线轮胎

- 斜交轮胎

第七章 依车辆类型分類的市场估计与预测,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第八章 按分销管道分類的市场估算与预测,2022-2035年

- OEM

- 第三方供应商

第九章 依销售模型分類的市场估计与预测,2022-2035年

- 直接面向消费者(D2C)

- 线上到线下 (O2O)

- 提供安装服务的市场

第十章 2022-2034年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 丹麦

- 芬兰

- 挪威

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章 公司简介

- 世界公司

- Amazon Tires

- Costco Tires

- Discount Tire Direct

- Goodyear

- Pep Boys

- 山姆会员店轮胎

- SimpleTire

- Tire Rack

- TireBuyer

- Walmart Tires

- 该地区顶尖公司

- 4 Wheel Parts

- BJ轮胎中心

- BJ's Wholesale Club 轮胎

- Discounted Wheel Warehouse

- Fountain Tire

- Les Schwab Tires

- NTB(National Tire &Battery)

- Priority Tire

- Tire Kingdom

- Tires-easy.com

- 新兴企业

- 123 Tire

- AlloTire

- BestOne Tire &Auto

- Blackcircles

- CarParts.com Tires

- Falken Tires Online

- Just Tires

- Oponeo

- Tyremarket

- WheelMax

The Global Automotive Tires E-Retailing Market was valued at USD 17.1 billion in 2025 and is estimated to grow at a CAGR of 14.2% to reach USD 62.2 billion by 2035.

Market growth is shaped by the rapid integration of visual and interactive digital commerce tools across online tire retail platforms. Digital retail experiences are becoming more immersive, allowing customers to better evaluate products before purchase and make informed decisions with higher confidence. This shift is improving engagement levels, lowering product return rates, and strengthening conversion performance for online sellers. The growing use of advanced digital showrooms and configuration tools is enabling tire sellers to differentiate themselves while improving overall customer satisfaction in a competitive landscape. Subscription-based offerings focused on tire replacement cycles, maintenance scheduling, and seasonal usage patterns are also reshaping purchasing behavior. These models allow customers to move away from one-time purchases in favor of flexible, cost-efficient service plans. The model is gaining traction among users seeking convenience and predictable expenses. Predictive analytics are further supporting this evolution by enabling retailers to recommend timely replacements based on usage data, supporting higher lifetime customer value. Artificial intelligence-driven recommendation engines continue to influence purchasing decisions and redefine how consumers approach online tire buying.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.1 Billion |

| Forecast Value | $62.2 Billion |

| CAGR | 14.2% |

The passenger vehicle segment held 67% share in 2025 and is forecast to grow at a CAGR of 14% from 2026 to 2035. Market demand is supported by rising vehicle ownership and longer vehicle usage cycles, which are driving consistent replacement needs. Online platforms are increasingly preferred due to ease of price comparison, access to user feedback, and simplified purchasing workflows. As more vehicles remain in operation for extended periods, demand for replacement tires through digital channels continues to rise. Consumers are prioritizing convenience and speed, and e-retailing platforms are meeting these expectations through streamlined access and purchasing efficiency.

The third-party suppliers segment held a 71% share in 2025 and is expected to grow at a CAGR of 13.5% from 2026 to 2035. Their leadership position is supported by broad product assortments covering multiple brands, specifications, and pricing tiers. These suppliers can offer competitive pricing while maintaining performance and safety standards due to strong procurement networks and volume-based sourcing strategies. This value-driven proposition aligns well with online buyer expectations and continues to reinforce their market presence.

United States Automotive Tires E-Retailing Market held 82% share in 2025, generating USD 4 billion. Strong vehicle ownership levels and consistent replacement demand are sustaining online tire sales across the country. Consumers are increasingly turning to digital channels that offer wide product availability, competitive pricing, and home delivery services. Retailers are further supporting sales momentum through loyalty incentives and flexible digital payment solutions that enhance affordability and convenience.

Key companies operating in the Global Automotive Tires E-Retailing Market include Tire Rack, Amazon, Walmart Tires, Discount Tire Direct, Goodyear, SimpleTire, Priority Tire, Pep Boys, Tires-easy, and NTB. These companies are actively shaping the competitive environment through platform innovation and service expansion. Companies in the automotive tires e-retailing market are reinforcing their competitive position through digital optimization, customer-centric services, and supply chain efficiency. Many players are investing in advanced data analytics to personalize recommendations and improve demand forecasting. Expanding private-label offerings and exclusive partnerships is helping improve margins and brand loyalty. Retailers are also enhancing fulfillment capabilities through faster delivery options and expanded installation networks. Subscription services and flexible payment plans are being used to encourage repeat purchases and long-term engagement.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Tire

- 2.2.3 Manufacturing

- 2.2.4 Vehicle

- 2.2.5 Distribution channel

- 2.2.6 Sales model

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of online tire marketplaces

- 3.2.1.2 Rising preference for direct-to-consumer sales

- 3.2.1.3 Growing digitalization in automotive retail

- 3.2.1.4 Increased consumer preference for convenience

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High return rates due to incorrect size selection

- 3.2.2.2 Limited physical inspection before purchase

- 3.2.2.3 Dependence on last-mile logistics & installers

- 3.2.2.4 Price competition among online sellers

- 3.2.3 Market opportunities

- 3.2.3.1 AI-based tire recommendation engines

- 3.2.3.2 Subscription & tire-as-a-service models

- 3.2.3.3 Growth of EV-specific tire demand

- 3.2.3.4 Expansion in emerging markets

- 3.2.3.5 Partnerships with installers & service networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 FMVSS - Federal Motor Vehicle Safety Standards (Tires)

- 3.4.1.2 Canada Vehicle Safety Standards (CVSS)

- 3.4.2 Europe

- 3.4.2.1 UNECE R117 / E-Mark Certification

- 3.4.2.2 EUDR - EU Deforestation Regulation

- 3.4.2.3 Tyre Labelling Regulation (EU 2020/740)

- 3.4.3 Asia Pacific

- 3.4.3.1 China Compulsory Certification (CCC) for Tires

- 3.4.3.2 Extended Producer Responsibility (EPR)

- 3.4.3.3 Japan Industrial Standards (JIS) for Tires

- 3.4.4 Latin America

- 3.4.4.1 INMETRO Tire Certification & Labeling

- 3.4.4.2 IRAM / Local Tire Standards

- 3.4.4.3 Vehicle & Tire Relevance to Euro Standards

- 3.4.5 MEA

- 3.4.5.1 Tire Identification Labels with RFID

- 3.4.5.2 SASO Tire Performance & Heat Resistance Standards

- 3.4.5.3 EPR Tire Recycling / Waste Management Standards

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Patent analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Cost breakdown analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Import and export

- 3.11.3 Major import countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Consumer buying journey & decision factors

- 3.13.1 Key online decision parameters (price, reviews, fitment tools)

- 3.13.2 Role of AI-based tire recommendation engines

- 3.13.3 Comparison tools, user reviews, and ratings impact

- 3.13.4 Payment preferences

- 3.14 Future market outlook & structural shifts

- 3.14.1 Shift toward omnichannel tire retailing

- 3.14.2 Growth of subscription-based tire services

- 3.14.3 Direct OEM-to-consumer acceleration

- 3.14.4 Consolidation outlook among e-retail platforms

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Tire, 2022 - 2035 ($Mn & Units)

- 5.1 Key trends

- 5.2 All-season tires

- 5.3 Summer tires

- 5.4 Winter tires

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Manufacturing, 2022 - 2035 ($Mn & Units)

- 6.1 Key trends

- 6.2 Radial tire

- 6.3 Bias tire

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn & Units)

- 7.1 Key trends

- 7.2 Passenger car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 Light commercial vehicle (LCV)

- 7.3.2 Medium commercial vehicle (MCV)

- 7.3.3 Heavy commercial vehicle (HCV)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn & Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Third-party suppliers

Chapter 9 Market Estimates & Forecast, By Sales Model, 2022 - 2035 ($Mn & Units)

- 9.1 Key trends

- 9.2 Direct-to-Consumer (D2C)

- 9.3 Online-to-Offline (O2O)

- 9.4 Marketplace with Installed Services

Chapter 10 Market Estimates & Forecast, By Region, 2022-2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Denmark

- 10.3.8 Finland

- 10.3.9 Norway

- 10.3.10 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Amazon Tires

- 11.1.2 Costco Tires

- 11.1.3 Discount Tire Direct

- 11.1.4 Goodyear

- 11.1.5 Pep Boys

- 11.1.6 Sam’s Club Tires

- 11.1.7 SimpleTire

- 11.1.8 Tire Rack

- 11.1.9 TireBuyer

- 11.1.10 Walmart Tires

- 11.2 Regional Champions

- 11.2.1. 4 Wheel Parts

- 11.2.2 BJ’s Tire Center

- 11.2.3 BJ’s Wholesale Club Tires

- 11.2.4 Discounted Wheel Warehouse

- 11.2.5 Fountain Tire

- 11.2.6 Les Schwab Tires

- 11.2.7 NTB (National Tire & Battery)

- 11.2.8 Priority Tire

- 11.2.9 Tire Kingdom

- 11.2.10 Tires-easy.com

- 11.3 Emerging Players

- 11.3.1. 123 Tire

- 11.3.2 AlloTire

- 11.3.3 BestOne Tire & Auto

- 11.3.4 Blackcircles

- 11.3.5 CarParts.com Tires

- 11.3.6 Falken Tires Online

- 11.3.7 Just Tires

- 11.3.8 Oponeo

- 11.3.9 Tyremarket

- 11.3.10 WheelMax

2026年全球汽车售后市场报告

2026年全球汽车售后市场报告 智慧经销商CRM市场预测至2034年:按类型、功能、应用和区域分類的全球分析

智慧经销商CRM市场预测至2034年:按类型、功能、应用和区域分類的全球分析 2026-2030年全球汽车售后市场电子商务零售市场

2026-2030年全球汽车售后市场电子商务零售市场 美国汽车经销商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

美国汽车经销商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年) 日本汽车零售市场规模、份额、趋势和预测:按类型、车型、销售管道和地区划分,2026-2034年

日本汽车零售市场规模、份额、趋势和预测:按类型、车型、销售管道和地区划分,2026-2034年 云端原生汽车销售平台市场(按组件、部署方式、最终用户和销售管道),全球预测(2026-2032)按部署模式、车辆类型、销售管道、动力系统、应用程式和最终用户分類的汽车数位化经销商整合平台市场,全球预测,2026-2032年汽车印刷基板连接器市场(按连接器类型、安装类型、引脚数、额定电流、材质和应用划分)—2026-2032年全球预测汽车基板对板连接器市场:2026-2032年全球预测(按连接器类型、额定电流、间距、引脚数、安装方式、绝缘材料、触点镀层和锁定机制划分)汽车级闆对板连接器市场(按外形规格、间距、引脚数、额定电流、应用和最终用户行业划分)—全球预测,2026-2032年

云端原生汽车销售平台市场(按组件、部署方式、最终用户和销售管道),全球预测(2026-2032)按部署模式、车辆类型、销售管道、动力系统、应用程式和最终用户分類的汽车数位化经销商整合平台市场,全球预测,2026-2032年汽车印刷基板连接器市场(按连接器类型、安装类型、引脚数、额定电流、材质和应用划分)—2026-2032年全球预测汽车基板对板连接器市场:2026-2032年全球预测(按连接器类型、额定电流、间距、引脚数、安装方式、绝缘材料、触点镀层和锁定机制划分)汽车级闆对板连接器市场(按外形规格、间距、引脚数、额定电流、应用和最终用户行业划分)—全球预测,2026-2032年