|

市场调查报告书

商品编码

1936478

汽车人工智慧模拟与合成资料生成市场机会、成长要素、产业趋势分析及2026年至2035年预测Automotive AI Simulation and Synthetic Data Generation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

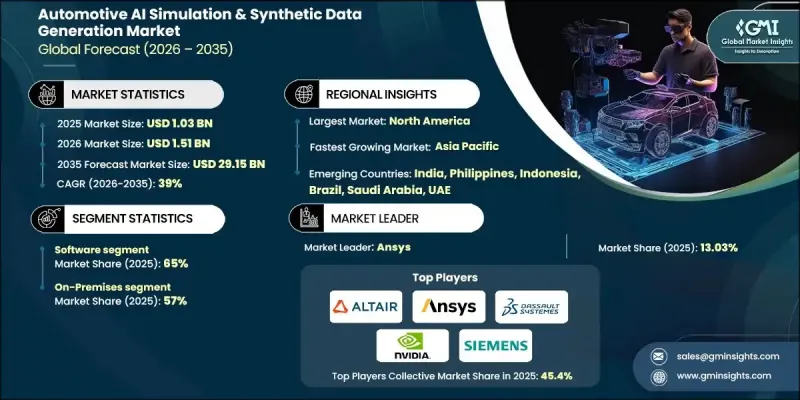

全球汽车人工智慧模拟和合成数据生成市场预计到 2025 年将达到 10.3 亿美元,到 2035 年将达到 291.5 亿美元,年复合成长率为 39%。

随着进阶驾驶辅助系统 (ADAS) 和自动驾驶技术全面进入量产阶段,车辆设计和检验方式正在发生根本性转变,而人工智慧驱动的模拟和合成资料工具正成为日益复杂的汽车软体虚拟开发、大规模人工智慧训练和安全检验的核心基础技术。这些平台使製造商和供应商能够在受控环境中数位化地模拟大量的驾驶场景、感测器互动和环境变量,从而显着减少对成本高且耗时的物理测试的依赖。市场也受惠于整个生态系统内日益密切的合作,汽车製造商、一级供应商、云端基础设施供应商和模拟软体供应商携手合作,简化开发流程。以模拟为先的开发模式现已广泛应用于自动驾驶和 ADAS 专案中,整合解决方案有助于降低工程复杂性、提高模型精度并降低整车开发成本。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 10.3亿美元 |

| 预测金额 | 291.5亿美元 |

| 复合年增长率 | 39% |

预计到2025年,软体领域将占据65%的市场份额,并在2035年之前以38.5%的复合年增长率成长。这一主导地位反映了产业加速向软体定义车辆转型的趋势,在这种模式下,核心驾驶智慧的建构、测试和改进不再依赖实体原型,而是透过数位环境进行。模拟软体能够对车辆行为、感测器性能和交通动态进行广泛的虚拟测试,从而可以高效且反覆地评估数百万种应用场景。

预计到2025年,本地部署方案将占据57%的市场份额,并在2026年至2035年间以37.9%的复合年增长率成长。这一趋势的驱动力源于对资料隐私、智慧财产权保护以及汽车安全和网路安全框架合规性的严格要求。汽车製造商和一级供应商管理着高度敏感的车辆系统、感知逻辑和专有资料集,这些通常受到外部环境的限制。本地部署基础设施能够提供对资料、模拟资产和人工智慧工作流程的完全所有权和管治,同时符合内部安全和监管标准。

预计到2025年,北美汽车人工智慧模拟和合成数据生成市场将占据85%的市场份额,市场规模达3.283亿美元。该地区的成长主要得益于对自动驾驶和高级驾驶辅助系统(ADAS)技术的大力投资,以及对安全检验和法规遵循日益增长的期望。随着企业寻求在确保系统效能高度可靠的同时,尽可能减少实体测试,基于场景的模拟和虚拟测试的应用正在加速发展。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 对高级驾驶辅助系统(ADAS)和自动驾驶汽车开发的需求不断增长

- 车辆软体系统日益复杂

- 对虚拟检验和基于场景的测试的需求激增

- 人工智慧/机器学习在感测器融合和感知系统中的应用日益广泛

- 产业潜在风险与挑战

- 高昂的初始投资成本

- 模拟工具复杂度

- 市场机会

- 基于云端的仿真即服务模式的成长

- 对经认证的虚拟检验框架的需求日益增长

- 车辆开发中数位双胞胎的应用日益广泛

- 将模拟应用扩展到乘用车以外领域

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国:NHTSA自动驾驶系统引导与自动驾驶车辆测试倡议

- 欧洲

- 欧盟:联合国欧洲经济委员会第R157号条例(ALKS)

- 德国:自动驾驶法

- 英国:互联与自动驾驶(CAM)法规

- 法国:自动驾驶车辆实验框架

- 亚太地区

- 中国:智慧网连网汽车(ICV)模拟标准

- 日本:国土交通省自动驾驶安全指南

- 韩国:自动驾驶汽车法

- 新加坡:自动驾驶车辆安全评估框架

- 拉丁美洲

- 巴西:国家智慧交通与物联网策略

- 墨西哥:智慧运输和自动驾驶汽车试点法规

- 智利:智慧型运输系统(ITS)政策

- 中东和非洲

- 阿拉伯联合大公国:杜拜自动驾驶交通战略

- 沙乌地阿拉伯:2030愿景智慧运输框架

- 南非:绿色交通与自动驾驶政策

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利分析

- 永续性和环境影响分析

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 未来前景与机会

- OEM实施框架

- 评估与策略

- 基础设施建设

- 试验计画

- 整合与扩张

- 优化和改进

- 成功的关键要素

- 常见陷阱及解决方法

- 使用案例和应用场景

- 都市区自动驾驶模拟

- 高速公路自动驾驶和卡车编队行驶

- 用于安全测试的极端情况生成

- 用于训练感知模型的合成数据

- 驾驶员监控系统检验

- V2X通讯仿真

- 在寒冷地区和极端环境下进行测试

- 停车和低速行驶

第四章 竞争情势

- 介绍

- 公司市占率分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 依产品类型分類的市场估算与预测,2022-2035年

- 软体

- 服务

6. 按模拟类型分類的市场估算与预测,2022-2035 年

- 感测器仿真

- 场景生成

- 车辆动力学

- HIL/SIL 测试

7. 基于综合资料的市场估算与预测,2022-2035年

- 图片和影片

- 表格形式

- 时间序列

- 其他的

第八章 按应用领域分類的市场估算与预测,2022-2035年

- ADAS测试

- 自动驾驶汽车的研发

- 人工智慧/机器学习模型训练

- 安全与合规

- 设计检验

9. 依最终用途分類的市场估计与预测,2022-2035 年

- OEM

- 一级供应商

- 科技公司

- 研究所

第十章 依实施类型分類的市场估计与预测,2022-2035年

- 本地部署

- 基于云端的

- 杂交种

第十一章 依车辆类型分類的市场估价与预测,2022-2035年

- 搭乘用车

- 轿车

- 掀背车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- MCV

- 重型商用车(HCV)

第十二章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十三章:公司简介

- 世界公司

- Altair Engineering

- Ansys

- Autodesk

- Dassault Systemes

- IBM

- MSC Software(Hexagon)

- NVIDIA

- PTC

- Siemens

- Synopsys

- The MathWorks

- 当地公司

- AVL List

- AVSimulation

- dSPACE

- ESI Group(Keysight)

- IPG Automotive

- SIMUL8

- 新兴企业

- Anyverse

- Applied Intuition

- Cognata

- Foretellix

- Mechanical Simulation

- MOOG

- Parallel Domain

- SimScale

The Global Automotive AI Simulation & Synthetic Data Generation Market was valued at USD 1.03 billion in 2025 and is estimated to grow at a CAGR of 39% to reach USD 29.15 billion by 2035.

The rapid expansion reflects a fundamental transformation in how vehicles are designed and validated as advanced driver assistance systems and autonomous technologies move deeper into production. AI-driven simulation and synthetic data tools are becoming core enablers of virtual development, large-scale AI training, and safety validation for increasingly complex automotive software. These platforms allow manufacturers and suppliers to digitally replicate massive volumes of driving scenarios, sensor interactions, and environmental variables in controlled settings, significantly reducing dependence on costly and time-intensive real-world testing. The market is also benefiting from growing collaboration across the ecosystem, as vehicle manufacturers, Tier-1 suppliers, cloud and infrastructure providers, and simulation software vendors align to streamline development workflows. Sim-first development models are now widely embedded into autonomous and ADAS programs, while integrated solutions are helping reduce engineering complexity, improve model accuracy, and lower overall vehicle development costs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.03 Billion |

| Forecast Value | $29.15 Billion |

| CAGR | 39% |

The software segment accounted for 65% share in 2025 and is forecast to grow at a CAGR of 38.5% through 2035. This dominance reflects the industry's accelerated transition toward software-defined vehicles, where core driving intelligence is built, tested, and refined through digital environments rather than physical prototypes. Simulation software enables extensive virtual testing of vehicle behavior, sensor performance, and traffic dynamics, allowing millions of use cases to be evaluated efficiently and repeatedly.

The on-premises segment held 57% share in 2025 and is expected to grow at a CAGR of 37.9% from 2026 to 2035. This preference is driven by strict requirements around data privacy, intellectual property protection, and compliance with automotive safety and cybersecurity frameworks. Automotive manufacturers and Tier-1 suppliers manage highly confidential vehicle systems, perception logic, and proprietary datasets that are often restricted from external environments. On-premises infrastructure provides full ownership and governance over data, simulation assets, and AI workflows while aligning with internal security and regulatory standards.

North America Automotive AI Simulation & Synthetic Data Generation Market held 85% share and generated USD 328.3 million in 2025. Growth in the country is being fueled by strong investment in autonomous and ADAS technologies, alongside rising expectations for safety validation and regulatory readiness. The adoption of scenario-based simulation and virtual testing is accelerating as organizations seek to limit physical testing while maintaining high confidence in system performance.

Key companies active in the Global Automotive AI Simulation & Synthetic Data Generation Market include NVIDIA, Siemens, Dassault Systemes, Ansys, The MathWorks, dSPACE, Altair Engineering, PTC, Autodesk, and ESI Group. Leading companies in the Automotive AI simulation and synthetic data generation market are strengthening their positions through platform integration, strategic partnerships, and continuous innovation. Many vendors are expanding end-to-end simulation ecosystems that combine scenario creation, sensor modeling, AI validation, and regression testing into unified offerings. Collaboration with OEMs and Tier-1 suppliers is being used to tailor solutions to real-world development needs and accelerate adoption.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Simulation type

- 2.2.4 Synthetic data type

- 2.2.5 Application

- 2.2.6 End use

- 2.2.7 Deployment mode

- 2.2.8 Vehicle

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for ADAS & autonomous vehicle development

- 3.2.1.2 Rising complexity of vehicle software systems

- 3.2.1.3 Surge in demand for virtual validation and scenario-based testing

- 3.2.1.4 Increase in AI/ML adoption for sensor fusion and perception systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Complexity of simulation tools

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in cloud-based simulation-as-a-service models

- 3.2.3.2 Increase in demand for certified virtual validation frameworks

- 3.2.3.3 Rise in digital twin adoption for vehicle development

- 3.2.3.4 Expansion of simulation use beyond passenger vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States: NHTSA ADS Guidance & AV TEST Initiative.

- 3.4.2 Europe

- 3.4.2.1 European Union: UNECE Regulation R157 (ALKS)

- 3.4.2.2 Germany: Autonomous Driving Act

- 3.4.2.3 United Kingdom: Connected and Automated Mobility (CAM) Regulations

- 3.4.2.4 France: Autonomous Vehicle Experimentation Framework

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Intelligent Connected Vehicle (ICV) Simulation Standards

- 3.4.3.2 Japan: MLIT Automated Driving Safety Guidelines

- 3.4.3.3 South Korea: Autonomous Vehicle Act

- 3.4.3.4 Singapore: Autonomous Vehicle Safety Assessment Framework

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Intelligent Mobility & IoT Strategy

- 3.4.4.2 Mexico: Smart Mobility & AV Pilot Regulations

- 3.4.4.3 Chile: Intelligent Transport Systems (ITS) Policy

- 3.4.5 MEA

- 3.4.5.1 United Arab Emirates: Dubai Autonomous Transport Strategy

- 3.4.5.2 Saudi Arabia: Vision 2030 Smart Mobility Framework

- 3.4.5.3 South Africa: Green Transport & Automated Mobility Policy

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental impact analysis

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Future outlook & opportunities

- 3.11 OEM implementation framework

- 3.11.1 Assessment & strategy

- 3.11.2 Infrastructure setup

- 3.11.3 Pilot program

- 3.11.4 Integration & scaling

- 3.11.5 Optimization & expansion

- 3.11.6 Critical success factors

- 3.11.7 Common pitfalls & mitigation

- 3.12 Use Cases & application scenarios

- 3.12.1 Urban autonomous driving simulation

- 3.12.2 Highway autopilot & truck platooning

- 3.12.3 Edge case generation for safety testing

- 3.12.4 Synthetic data for perception model training

- 3.12.5 Driver monitoring system validation

- 3.12.6. V2X communication simulation

- 3.12.7 Cold weather & extreme climate testing

- 3.12.8 Parking & low-speed maneuvering

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Simulation Type, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Sensor Simulation

- 6.3 Scenario Generation

- 6.4 Vehicle Dynamics

- 6.5 HIL/SIL Testing

Chapter 7 Market Estimates & Forecast, By Synthetic Data, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Image & Video

- 7.3 Tabular

- 7.4 Time-Series

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 ADAS Testing

- 8.3 Autonomous Vehicle Development

- 8.4 AI/ML Model Training

- 8.5 Safety & Compliance

- 8.6 Design Validation

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Tier 1 Suppliers

- 9.4 Technology Companies

- 9.5 Research Institutions

Chapter 10 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 On-Premises

- 10.3 Cloud-Based

- 10.4 Hybrid

Chapter 11 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 Passenger vehicle

- 11.2.1 Sedan

- 11.2.2 Hatchback

- 11.2.3 SUV

- 11.3 Commercial vehicle

- 11.3.1 LCV

- 11.3.2 MCV

- 11.3.3 HCV

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Belgium

- 12.3.8 Netherlands

- 12.3.9 Sweden

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Philippines

- 12.4.7 Indonesia

- 12.4.8 Singapore

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 Altair Engineering

- 13.1.2 Ansys

- 13.1.3 Autodesk

- 13.1.4 Dassault Systemes

- 13.1.5 IBM

- 13.1.6 MSC Software (Hexagon)

- 13.1.7 NVIDIA

- 13.1.8 PTC

- 13.1.9 Siemens

- 13.1.10 Synopsys

- 13.1.11 The MathWorks

- 13.2 Regional Players

- 13.2.1 AVL List

- 13.2.2 AVSimulation

- 13.2.3 dSPACE

- 13.2.4 ESI Group (Keysight)

- 13.2.5 IPG Automotive

- 13.2.6 SIMUL8

- 13.3 Emerging Players

- 13.3.1 Anyverse

- 13.3.2 Applied Intuition

- 13.3.3 Cognata

- 13.3.4 Foretellix

- 13.3.5 Mechanical Simulation

- 13.3.6 MOOG

- 13.3.7 Parallel Domain

- 13.3.8 SimScale

2026-2030年全球汽车技术市场

2026-2030年全球汽车技术市场 汽车人工智慧:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

汽车人工智慧:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2034年全球汽车人工智慧市场规模、份额、趋势和成长分析报告

2026-2034年全球汽车人工智慧市场规模、份额、趋势和成长分析报告 汽车人工智慧(AI)市场-全球产业规模、份额、趋势、机会及预测(按组件、技术、工艺、应用、车辆类型、需求类别、地区和竞争格局划分,2021-2031)车辆智慧系统市场-全球产业规模、份额、趋势、机会与预测:按道路场景理解、车辆类型、进阶驾驶辅助与监控、地区和竞争格局划分,2021-2031年

汽车人工智慧(AI)市场-全球产业规模、份额、趋势、机会及预测(按组件、技术、工艺、应用、车辆类型、需求类别、地区和竞争格局划分,2021-2031)车辆智慧系统市场-全球产业规模、份额、趋势、机会与预测:按道路场景理解、车辆类型、进阶驾驶辅助与监控、地区和竞争格局划分,2021-2031年 汽车语音AI助理市场规模、占有率及预测:依AI引擎(自然语言理解、自然语言处理)、语言支援、整合类型(原生、云端连接)及功能(导航、媒体、车辆控制)划分-全球预测至2036年

汽车语音AI助理市场规模、占有率及预测:依AI引擎(自然语言理解、自然语言处理)、语言支援、整合类型(原生、云端连接)及功能(导航、媒体、车辆控制)划分-全球预测至2036年 AIGC平台模型市场:2026-2032年全球预测(按模型类型、部署格式、应用和产业划分)

AIGC平台模型市场:2026-2032年全球预测(按模型类型、部署格式、应用和产业划分) 汽车AI盒子(2026)

汽车AI盒子(2026) 全球汽车自动化市场预测至2032年:按组件、车辆类型、自动化程度、应用、最终用户和地区划分

全球汽车自动化市场预测至2032年:按组件、车辆类型、自动化程度、应用、最终用户和地区划分 汽车人工智慧维修服务市场规模、份额和成长分析(按服务类型、技术、部署类型、车辆类型、最终用户和地区划分)—产业预测(2026-2033 年)

汽车人工智慧维修服务市场规模、份额和成长分析(按服务类型、技术、部署类型、车辆类型、最终用户和地区划分)—产业预测(2026-2033 年)