|

市场调查报告书

商品编码

1936487

人工智慧在汽车网路安全领域的市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)AI in Automotive Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

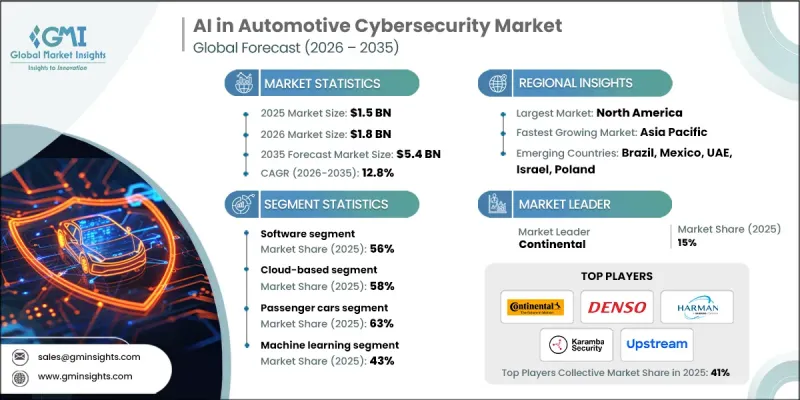

全球汽车网路安全人工智慧市场预计到 2025 年将达到 15 亿美元,到 2035 年将达到 54 亿美元,年复合成长率为 12.8%。

联网汽车、自动驾驶技术和以软体为中心的汽车平臺的快速普及正在推动市场成长。现代汽车高度依赖复杂的软体架构,其电控系统包含超过1亿行程式码,显着增加了系统面临的网路风险。随着车辆数位化程度的提高,网路安全已成为设计和营运的关键优先事项。人工智慧正被越来越多地应用于即时监控、分析和回应网路威胁,从而实现主动防御机製而非被动防御。向软体定义车辆的转型代表着汽车设计的根本性变革,因为软体控制着核心功能、远端特性管理和持续性能改进。传统手动软体更新带来的成本负担估计每年高达4.5亿至5亿美元,这加速了原始设备製造商(OEM)采用人工智慧驱动的网路安全平台,以支援远端更新、威胁缓解和系统完整性,从而在日益互联的汽车生态系统中发挥作用。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 15亿美元 |

| 预测金额 | 54亿美元 |

| 复合年增长率 | 12.8% |

软体领域的主导地位反映了整个产业向代码驱动型车辆架构的转变,在这种架构中,关键功能由数位平台而非机械部件控制。基于软体的网路安全解决方案旨在保护嵌入式韧体、防御车载应用程序,并创建可信任执行环境以检验授权程式码的行为。这些解决方案还管理加密通讯协定和身份验证流程,以确保安全的资料交换和更新交付。人工智慧透过持续分析车载网路的行为并识别异常和潜在入侵来增强这些平台。车辆软体内容的快速成长(跨多个系统的程式码量超过1亿行)持续推动着对能够随着系统复杂性的增加而扩展的先进、以软体为中心的网路安全解决方案的需求。

到2025年,基于硬体的解决方案将占据27%的市场份额,巩固其作为车辆安全基础层的地位。这些解决方案将实体安全机制直接整合到车辆电子设备中,保护关键系统免受篡改和未授权存取。硬体元件旨在安全地储存加密凭证、执行加密过程,并建立可信任的启动环境,从而防止执行被篡改的软体。其他硬体安全元件支援独特的设备身份验证,并分担复杂的加密处理,从而维持车辆的整体性能。这些技术共同构成了一个安全的物理基础,与人工智慧驱动的软体防御相辅相成。

预计到2025年,随着汽车网路安全战略越来越依赖集中式平台来管理庞大的车队,基于云端的部署方案将占据显着份额。云端解决方案可提供即时威胁情报、系统级分析,并可在分散式车辆网路中快速部署安全性更新。这种方法透过实现集中式通讯管理和可扩展的数据处理,支援联网汽车服务和远端软体交付。聚合来自数百万辆汽车的网路安全数据,可实现先进的机器学习分析,从而识别新兴威胁并协调快速反应措施,而无需人工干预。

预计到2025年,美国汽车网路安全市场将占据显着份额,这主要得益于配备先进数位化功能的高价值车辆推动了单车网路安全投资的成长。完善的交通基础设施为先进的车辆互联提供了支持,而成熟的网路安全生态系统则促进了专用车辆保护解决方案的开发。对互联出行基础设施投资的不断增长,也推动了对强大网路安全框架的需求,以保护车辆通讯、数位道路系统和智慧交通管理平台。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 联网汽车、电动车和自动驾驶汽车日益普及

- 必须遵守联合国法规 R155/R156 和 ISO/SAE 21434

- 针对汽车的网路攻击正变得越来越复杂。

- 软体定义汽车和空中升级的成长

- V2X 和车载数位服务的扩展

- 产业潜在风险与挑战

- 高昂的实施和整合成本

- 基于人工智慧的网路安全系统的复杂性

- 汽车网路安全领域熟练人才短缺

- 传统汽车平臺相容性挑战

- 市场机会

- 基于人工智慧的预测性威胁侦测解决方案

- 边缘人工智慧实现即时、低延迟安全

- 用于车辆访问和支付的生物识别

- 安全即服务订阅模式

- 传统车辆的售后网路安全

- 成长潜力分析

- 监管环境

- 北美洲

- 美国联邦机动车辆安全标准/国家公路交通安全管理局指南

- 加拿大 - 机动车辆安全法规 (MVSR)

- 欧洲

- 德国/欧盟通用安全法规(GSR)

- 英国- 道路车辆(许可)条例

- 法国-欧盟自动驾驶汽车(AV)和道路安全框架

- 义大利 - 国家道路安全计画 (PNSS)

- 亚太地区

- 中国-GB/T标准/GB标准

- 印度-机动车辆(修正)法案与AIS标准

- 日本-道路交通法及国土交通省自动驾驶指南

- 澳洲 - 澳洲外观设计规则 (ADR)

- LATAM

- 墨西哥-NOM汽车安全标准

- 阿根廷 - 交通法第 24.449 号

- 中东和非洲

- 南非共和国 - 国家道路交通法(1996 年)

- 沙乌地阿拉伯—交通法与2030愿景交通倡议

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 人工智慧和机器学习在汽车安全领域的演进

- 用于威胁侦测的深度学习演算法

- 自然语言处理在安全情报的应用

- 新兴技术

- 电脑视觉在安全监控上的应用

- 情境感知计算与自动回应

- 量子抗性密码技术的发展

- 当前技术趋势

- 专利分析

- 人工智慧安全专利的发展趋势

- 主要专利拥有者人和技术领导者

- 新兴智慧财产权趋势与申请模式

- 专利授权与合作模式

- 定价分析

- 解决方案定价模式(订阅、永久授权、收费车辆计费)

- 硬体成本趋势

- 服务定价趋势

- 总拥有成本分析

- 用例和成功案例

- 车队管理安全用例

- 自动驾驶车辆保护场景

- 车载支付和商业安全

- OTA 更新安全实施

- V2X 通讯保护用例

- 互联资讯娱乐系统的安全应用

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 投资与资金筹措分析

- 创投创业投资

- 併购活动与市场整合

- 策略联盟与合作

- 政府资助和津贴

- 未来前景与机会

- 监管演变及其影响

- 战略机会

- 未来威胁情势

- 投资机会

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 按组件分類的市场估算与预测,2022-2035年

- 硬体

- AI加速处理器

- 硬体安全模组(HSM)

- 安全网关及网路设备

- 储存和记忆体组件

- 软体

- 人工智慧驱动的安全平台

- 独立安全应用程式

- 整合软体解决方案

- 服务

- 专业服务

- 咨询和顾问服务

- 实施和整合服务

- 支援和维护服务

- 资安管理服务

- 威胁监控与侦测

- 事件回应服务

- 安全营运中心 (SOC) 服务

- 专业服务

第六章 依车辆类型分類的市场估计与预测,2022-2035年

- 搭乘用车

- 掀背车

- SUV

- 轿车

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

- 电动车(EV)

第七章 按技术分類的市场估计与预测,2022-2035年

- 机器学习

- 自然语言处理(NLP)

- 电脑视觉

- 情境感知计算

- 其他的

第八章 依部署方式分類的市场估算与预测,2022-2035年

- 本地部署

- 云

第九章 证券市场估计与预测(2022-2035年)

- 端点安全

- 应用程式安全

- 无线网路安全

- 云端安全

- 其他的

第十章 依应用领域分類的市场估计与预测,2022-2035年

- ADAS(进阶驾驶辅助系统)与安全系统

- 资讯娱乐系统

- 车载资讯系统

- 动力传动系统系统

- 车身控制与舒适系统

- 其他的

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 瑞典

- 丹麦

- 波兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 以色列

第十二章:公司简介

- 世界玩家

- Aptiv

- BlackBerry

- Continental

- Denso

- Harman International Industries

- Karamba Security

- NVIDIA

- Robert Bosch

- Siemens

- Upstream Security

- 区域玩家

- Cybellum Technologies

- ESCRYPT

- GuardKnox Cyber Technologies

- Infineon Technologies

- Intertrust Technologies

- NCC

- NXP Semiconductors

- Renesas Electronics

- STMicroelectronics

- Trillium Security

- Vector Informatik

- 新兴科技创新者

- Aurora Labs

- C2A Security

- Cymotive Technologies

- VicOneg bmhjb

The Global AI in Automotive Cybersecurity Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 12.8% to reach USD 5.4 billion by 2035.

The rapid proliferation of connected vehicles, autonomous driving technologies, and software-centric vehicle platforms drives market growth. Modern vehicles now rely heavily on complex software architectures, with electronic control units containing more than 100 million lines of code, significantly increasing system exposure to cyber risks. As vehicles become more digitally integrated, cybersecurity has evolved into a critical design and operational priority. Artificial intelligence is increasingly deployed to monitor, analyze, and respond to cyber threats in real time, enabling proactive defense mechanisms rather than reactive protection. The transition toward software-defined vehicles represents a fundamental transformation of automotive design, where software governs core functionality, remote feature management, and continuous performance enhancement. The rising cost burden associated with traditional manual software updates, estimated at USD 450 million to USD 500 million annually for original equipment manufacturers, is accelerating the adoption of AI-enabled cybersecurity platforms that support remote updates, threat mitigation, and system integrity in an increasingly connected automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 12.8% |

The dominance of the software segment reflects the industry-wide movement toward code-driven vehicle architectures where digital platforms control critical functions rather than mechanical components. Software-based cybersecurity solutions are designed to secure embedded firmware, protect in-vehicle applications, and establish trusted execution environments that verify authorized code operation. These solutions also manage encryption protocols and authentication processes that ensure secure data exchange and update delivery. Artificial intelligence enhances these platforms by continuously analyzing in-vehicle network behavior to identify anomalies and potential intrusions. The rapid expansion of software content within vehicles, now exceeding 100 million lines of code across multiple systems, continues to drive demand for advanced software-focused cybersecurity solutions that can scale with increasing system complexity.

The hardware-based solutions segment held 27% share in 2025, reinforcing its role as a foundational layer of vehicle security. These solutions integrate physical security mechanisms directly into vehicle electronics to protect critical systems from tampering and unauthorized access. Hardware components are engineered to securely store cryptographic credentials, execute encryption processes, and establish trusted boot environments that prevent compromised software from running. Additional hardware security elements support unique device authentication and offload complex cryptographic operations to preserve overall vehicle performance. Together, these technologies form a secure physical backbone that complements AI-driven software defenses.

The cloud-based deployment segment reached a significant share in 2025 as automotive cybersecurity strategies increasingly rely on centralized platforms to manage large-scale vehicle fleets. Cloud-enabled solutions provide real-time threat intelligence, system-wide analytics, and rapid deployment of security updates across distributed vehicle networks. This approach supports connected vehicle services and remote software delivery by enabling centralized communication management and scalable data processing. Aggregating cybersecurity data from millions of vehicles allows for advanced machine learning analysis that identifies emerging threats and coordinates rapid response actions without requiring physical intervention.

United States AI in Automotive Cybersecurity Market held a notable share in 2025, driven by high-value vehicles equipped with advanced digital features, contributing to elevated per-unit cybersecurity investment. Extensive transportation infrastructure supports advanced vehicle connectivity, while a well-established cybersecurity ecosystem enables the development of specialized automotive protection solutions. Investments in connected mobility infrastructure are increasing the need for robust cybersecurity frameworks to safeguard vehicle communications, digital road systems, and intelligent traffic management platforms.

Key companies operating in the AI in Automotive Cybersecurity Market include NVIDIA, Robert Bosch, Continental, BlackBerry, Harman International, Denso, Upstream Security, Trillium Secure, Karamba Security, and GuardKnox Cyber Technologies. Companies in the AI in Automotive Cybersecurity Market are strengthening their competitive position through continuous innovation, strategic collaborations, and platform expansion. Leading players are investing in AI-driven threat detection, behavioral analytics, and automated response systems to stay ahead of evolving cyber risks. Many firms are forming partnerships with automakers, software vendors, and cloud service providers to integrate security solutions directly into vehicle architectures. Portfolio diversification across software, hardware, and cloud-based offerings is enabling vendors to address varied customer requirements. In parallel, companies are expanding global delivery capabilities and emphasizing regulatory compliance to support international deployments.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicles

- 2.2.4 Technology

- 2.2.5 Deployment Mode

- 2.2.6 Security

- 2.2.7 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising connected, electric, and autonomous vehicle adoption

- 3.2.1.3 Mandatory compliance with UN R155/R156 and ISO/SAE 21434

- 3.2.1.4 Increasing cyberattack complexity targeting vehicles

- 3.2.1.5 Growth of software-defined vehicles and OTA updates

- 3.2.1.6 Expansion of V2X and in-vehicle digital services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Complexity of AI-based cybersecurity systems

- 3.2.2.3 Shortage of skilled automotive cybersecurity talent

- 3.2.2.4 Legacy vehicle platform compatibility issues

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven predictive threat detection solutions

- 3.2.3.2 Edge AI for real-time, low-latency security

- 3.2.3.3 Biometric authentication for vehicle access and payments

- 3.2.3.4 Security-as-a-service and subscription-based models

- 3.2.3.5 Aftermarket cybersecurity for legacy vehicles

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- FMVSS and NHTSA guidelines

- 3.4.1.2 Canada - Motor vehicle safety regulations (MVSR)

- 3.4.2 Europe

- 3.4.2.1 Germany- EU General Safety Regulation (GSR)

- 3.4.2.2 UK- Road Vehicles (Approval) Regulations

- 3.4.2.3 France- EU AV and road safety frameworks

- 3.4.2.4 Italy- National Road Safety Plan (PNSS)

- 3.4.3 Asia Pacific

- 3.4.3.1 China- GB/T and GB standards

- 3.4.3.2 India- Motor Vehicles (Amendment) Act and AIS standards

- 3.4.3.3 Japan- Road Traffic Act and MLIT autonomous driving guidelines

- 3.4.3.4 Australia- Australian Design Rules (ADR)

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 AI & machine learning evolution in automotive security

- 3.7.1.2 Deep learning algorithms for threat detection

- 3.7.1.3 Natural language processing for security intelligence

- 3.7.2 Emerging technologies

- 3.7.2.1 Computer vision applications in security surveillance

- 3.7.2.2 Context-aware computing & automated response

- 3.7.2.3 Quantum-resilient encryption development

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.8.1 AI-powered security patent landscape

- 3.8.2 Key patent holders & technology leaders

- 3.8.3 Emerging IP trends & filing patterns

- 3.8.4 Patent licensing & collaboration models

- 3.9 Pricing analysis

- 3.9.1 Solution pricing models (subscription, perpetual license, per-vehicle)

- 3.9.2 Hardware cost trends

- 3.9.3 Service pricing dynamics

- 3.9.4 Total cost of ownership analysis

- 3.10 Use cases & success stories

- 3.10.1 Fleet management security use cases

- 3.10.2 Autonomous vehicle protection scenarios

- 3.10.3 In-vehicle payment & commerce security

- 3.10.4 OTA update security implementation

- 3.10.5 V2X communication protection use cases

- 3.10.6 Connected infotainment security applications

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Investment & funding analysis

- 3.12.1 Venture capital investment trends

- 3.12.2 M&A activity & market consolidation

- 3.12.3 Strategic partnerships & collaborations

- 3.12.4 Government funding & grants

- 3.13 Future outlook and opportunities

- 3.13.1 Regulatory evolution & impact

- 3.13.2 Strategic opportunities

- 3.13.3 Future threat landscape

- 3.13.4 Investment opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 AI accelerators & processors

- 5.2.2 Hardware security modules (HSM)

- 5.2.3 Secure gateways & network devices

- 5.2.4 Storage & memory components

- 5.3 Software

- 5.3.1 AI-powered security platforms

- 5.3.2 Standalone security applications

- 5.3.3 Integrated software solutions

- 5.4 Services

- 5.4.1 Professional services

- 5.4.1.1 Consulting & advisory services

- 5.4.1.2 Deployment & integration services

- 5.4.1.3 Support & maintenance Services

- 5.4.2 Managed security services

- 5.4.2.1 Threat monitoring & detection

- 5.4.2.2 Incident response services

- 5.4.2.3 Security operations center (SOC) services

- 5.4.1 Professional services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 SUV

- 6.2.3 Sedan

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

- 6.4 Electric vehicles (EVs)

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Machine learning

- 7.3 Natural language processing (NLP)

- 7.4 Computer vision

- 7.5 Context-aware computing

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 On premises

- 8.3 Cloud

Chapter 9 Market Estimates & Forecast, By Security, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Endpoint security

- 9.3 Application security

- 9.4 Wireless network security

- 9.5 Cloud security

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Advanced driver assistance system (ADAS) & safety systems

- 10.3 Infotainment system

- 10.4 Telematics system

- 10.5 Powertrain system

- 10.6 Body control & comfort system

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.3.9 Denmark

- 11.3.10 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Israel

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Aptiv

- 12.1.2 BlackBerry

- 12.1.3 Continental

- 12.1.4 Denso

- 12.1.5 Harman International Industries

- 12.1.6 Karamba Security

- 12.1.7 NVIDIA

- 12.1.8 Robert Bosch

- 12.1.9 Siemens

- 12.1.10 Upstream Security

- 12.2 Regional Players

- 12.2.1 Cybellum Technologies

- 12.2.2 ESCRYPT

- 12.2.3 GuardKnox Cyber Technologies

- 12.2.4 Infineon Technologies

- 12.2.5 Intertrust Technologies

- 12.2.6 NCC

- 12.2.7 NXP Semiconductors

- 12.2.8 Renesas Electronics

- 12.2.9 STMicroelectronics

- 12.2.10 Trillium Security

- 12.2.11 Vector Informatik

- 12.3 Emerging Technology Innovators

- 12.3.1 Aurora Labs

- 12.3.2 C2A Security

- 12.3.3 Cymotive Technologies

- 12.3.4 VicOneg bmhjb

汽车网路安全市场:按车辆类型、安全类型、部署模式、组件类型和最终用户划分-2026-2032年全球市场预测

汽车网路安全市场:按车辆类型、安全类型、部署模式、组件类型和最终用户划分-2026-2032年全球市场预测 2026年全球汽车网路安全市场报告

2026年全球汽车网路安全市场报告 互联行动安全解决方案市场预测至2034年:按产品类型、连接类型、技术、应用、最终用户和地区分類的全球分析2026年全球外部云端汽车保全服务市场报告

互联行动安全解决方案市场预测至2034年:按产品类型、连接类型、技术、应用、最终用户和地区分類的全球分析2026年全球外部云端汽车保全服务市场报告 汽车网路安全市场规模、份额、成长率和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

汽车网路安全市场规模、份额、成长率和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 汽车软体开发与安全解决方案

汽车软体开发与安全解决方案 汽车网路安全市场(至 2040 年):依组件、形式、安全类型、车辆类型、应用、地区和主要参与者划分的行业趋势和全球预测

汽车网路安全市场(至 2040 年):依组件、形式、安全类型、车辆类型、应用、地区和主要参与者划分的行业趋势和全球预测 联网汽车安全市场机会、成长要素、产业趋势分析及2026年至2035年预测

联网汽车安全市场机会、成长要素、产业趋势分析及2026年至2035年预测 汽车网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分2026-2034年全球汽车网路安全市场规模、份额、趋势和成长分析报告

汽车网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分2026-2034年全球汽车网路安全市场规模、份额、趋势和成长分析报告