|

市场调查报告书

商品编码

1936490

精密农业无人机市场机会、成长要素、产业趋势分析及预测(2026-2035年)Precision Agriculture Drone Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

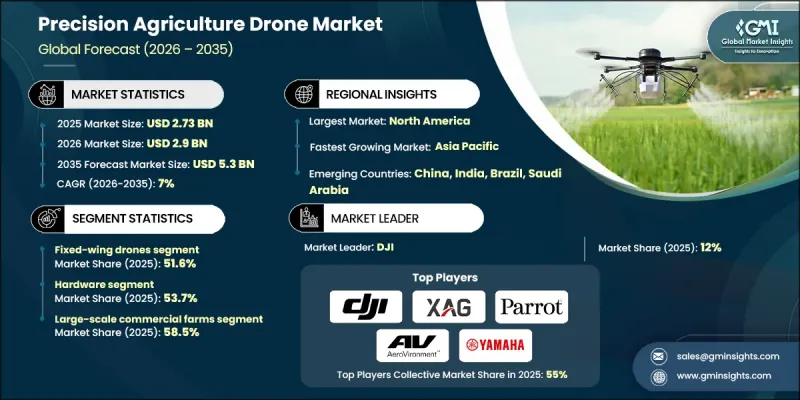

全球精密农业无人机市场预计到 2025 年将达到 27.3 亿美元,到 2035 年将达到 53 亿美元,年复合成长率为 7%。

市场成长的驱动力在于人们对作物生命週期管理和产量优化的日益关注,以及现代农场对提高营运效率的需求。随着种植者寻求即时洞察和精准的田间评估,对先进的空中监测和喷洒解决方案的需求不断增长。领先製造商之间的策略联盟和日益增强的整合活动进一步推动了产业发展,加速了创新并扩大了解决方案的范围。成熟的无人机开发商和农业智慧供应商之间加强合作,正在提升整个产业的技术能力并丰富产品系列。传统的作物巡查方法在大规模农业生产中效率低下,这促使人们转向基于无人机的自动化系统。连接性、人工智慧 (AI) 驱动的分析和云端数据处理技术的进步,在提高决策准确性的同时,也帮助农民减少投入浪费并提高整体生产力。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 27.3亿美元 |

| 预测金额 | 53亿美元 |

| 复合年增长率 | 7% |

到2025年,硬体部分将占据53.7%的市场份额,创造15亿美元的收入。先进感测器、长寿命电源系统和轻量化结构设计等核心硬体组件,为精密农业作业提供了所需的基本性能和有效载荷能力。增强的定位技术提高了导航精度和运行可靠性。硬体部分的领先地位反映了该行业对强大的实体基础设施的依赖,以支援符合数据驱动型农业实践的自动化测绘、监测和应用活动。

预计到2025年,大型商业农场将占58.5%的市场。该领域采用无人机技术的主要驱动力在于高效管理大片农地并最大限度地减少劳动力投入。这些企业优先考虑能够快速进行田间评估、自动数据采集以及在全部区域实现一致喷洒作业的无人机解决方案,从而支撑了对高性能精密农业无人机系统的强劲需求。

预计到2025年,美国精密农业无人机市占率将达到75.6% 。主导地位得益于早期技术应用、有利的法规环境以及大型农业企业广泛使用无人机监测。随着农民寻求提高效率、控製成本并提高大面积的生产力,对自动化农场管理和数据驱动的投入优化的关注持续推动着市场需求。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 从人类工作物调查过渡到自动化作物调查

- 人工智慧和边缘运算的兴起

- 政府补贴和“无人机力量”

- 产业潜在风险与挑战

- 先进有效载荷需要较高的初始资本支出(CAPEX)。

- 持证无人机飞行员短缺

- 机会

- 人工智慧驱动的预测分析

- 基于订阅的“资料即服务”

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 2022-2035年按产品分類的市场估算与预测

- 固定翼无人机

- 旋翼无人机

- 油电混合无人机

第六章 按组件分類的市场估算与预测,2022-2035年

- 硬体

- 软体

- 服务

7. 按农场规模分類的市场估计与预测,2022-2035 年

- 大型商业农场

- 中小农场

第八章 2022-2035年各系统市场估算与预测

- 嵌入式

- 振动分析仪

- 振动计

第九章 按应用领域分類的市场估算与预测,2022-2035年

- 田间测绘

- 变数施肥

- 作物巡查

- 其他的

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 3D Robotics

- AeroVironment, Inc.

- AGCO Corporation

- AgEagle Aerial Systems

- Agribotix

- Delair

- DJI

- DroneDeploy

- Parrot

- PrecisionHawk

- Quantum Systems

- senseFly

- Sentera

- Skeycatch

- Yamaha Motor Co., Ltd.

The Global Precision Agriculture Drone Market was valued at USD 2.73 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 5.3 billion by 2035.

Market growth is driven by increasing awareness around crop lifecycle management, yield optimization, and the need for higher operational efficiency across modern farms. Demand for advanced aerial monitoring and spraying solutions is rising as growers seek real-time insights and accurate field assessments. Industry momentum is further supported by an increase in strategic collaborations and consolidation activities among leading manufacturers, which has accelerated innovation and broadened solution offerings. The strengthening market presence of established drone developers, combined with agricultural intelligence providers, has enhanced technological capabilities and expanded product portfolios across the sector. Traditional crop inspection methods are increasingly viewed as inefficient for large-scale farming operations, prompting a shift toward automated drone-based systems. Advances in connectivity, artificial intelligence-driven analytics, and cloud-enabled data processing are improving decision-making accuracy while helping farmers reduce input waste and improve overall productivity.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.73 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 7% |

In 2025, the hardware segment accounted for 53.7% share, generating USD 1.5 billion. Core hardware components, including advanced sensors, extended-life power systems, and lightweight structural designs, provide the essential performance and payload capacity required for precision farming tasks. Enhanced positioning technologies are improving navigation accuracy and operational reliability. The dominance of the hardware segment reflects the industry's dependence on robust physical infrastructure to support automated mapping, monitoring, and application activities aligned with data-driven agricultural practices.

The large-scale commercial farms segment held 58.5% share in 2025. Adoption within this segment is driven by the need to manage extensive farmland efficiently while minimizing labor requirements. These operations prioritize drone solutions for rapid field assessment, automated data collection, and consistent application processes across large and continuous agricultural areas, reinforcing strong demand for high-performance precision drone systems.

United States Precision Agriculture Drone Market held 75.6% share in 2025. Market leadership is supported by early technology adoption, a favorable regulatory environment, and widespread utilization of drone-based monitoring across large farming enterprises. Emphasis on automated farm management and data-driven input optimization continues to drive demand as agricultural operators seek to improve efficiency, control costs, and enhance productivity across extensive crop areas.

Key companies operating in the Global Precision Agriculture Drone Market include DJI, PrecisionHawk, Parrot, AeroVironment, Inc., AGCO Corporation, AgEagle Aerial Systems, DroneDeploy, Yamaha Motor Co., Ltd., senseFly, Sentera, Quantum Systems, Delair, 3D Robotics, Agribotix, and Skeycatch. Companies in the precision agriculture drone market are reinforcing their competitive position through technology innovation, strategic partnerships, and targeted acquisitions. Leading players are investing in research and development to enhance flight endurance, data accuracy, and analytics capabilities. Many are expanding integrated software and hardware ecosystems to deliver end-to-end farming solutions. Firms are also focusing on geographic expansion and collaborations with agritech providers to strengthen distribution networks. Customization of drone platforms for specific crop types and farming scales, along with improved after-sales support and training services, is helping companies build long-term customer relationships and secure sustained market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Monitoring Process

- 2.2.4 Application

- 2.2.5 System

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift from manual to automated crop scouting

- 3.2.1.2 Proliferation of AI & Edge Computing

- 3.2.1.3 Government Subsidies & "Drone Shakti"

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial CAPEX for advanced payloads

- 3.2.2.2 Shortage of certified drone pilots

- 3.2.3 Opportunities

- 3.2.3.1 AI-Powered prescriptive analytics

- 3.2.3.2 Subscription-based "Data-as-a-Service"

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Fixed-wing Drones

- 5.3 Rotary-wing Drones

- 5.4 Hybrid Drones

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By Farm Size, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Large-scale Commercial Farms

- 7.3 Small and Medium Farms

Chapter 8 Market Estimates and Forecast, By System, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Embedded

- 8.3 Vibration Analyzers

- 8.4 Vibration Meter

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Field mapping

- 9.3 Variable rate application

- 9.4 Crop Scouting

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3D Robotics

- 11.2 AeroVironment, Inc.

- 11.3 AGCO Corporation

- 11.4 AgEagle Aerial Systems

- 11.5 Agribotix

- 11.6 Delair

- 11.7 DJI

- 11.8 DroneDeploy

- 11.9 Parrot

- 11.10 PrecisionHawk

- 11.11 Quantum Systems

- 11.12 senseFly

- 11.13 Sentera

- 11.14 Skeycatch

- 11.15 Yamaha Motor Co., Ltd.

2026年全球农业无人机市场报告

2026年全球农业无人机市场报告 无人机喷洒器市场:按平台、推进方式、技术、应用和最终用户分類的全球市场预测 – 2026-2032 年农业无人机市场:按组件、无人机类型、技术、农场类型、负载容量、应用和销售管道,全球预测,2026-2032年农业无人机市场:按类型、组件、无人机等级、应用和最终用户划分,全球预测,2026-2032年农业无人机市场:按类型、有效载荷能力、应用和最终用户划分,全球预测,2026-2032年

无人机喷洒器市场:按平台、推进方式、技术、应用和最终用户分類的全球市场预测 – 2026-2032 年农业无人机市场:按组件、无人机类型、技术、农场类型、负载容量、应用和销售管道,全球预测,2026-2032年农业无人机市场:按类型、组件、无人机等级、应用和最终用户划分,全球预测,2026-2032年农业无人机市场:按类型、有效载荷能力、应用和最终用户划分,全球预测,2026-2032年 全球农业无人机市场规模、份额、趋势和成长分析报告(2026-2034年)

全球农业无人机市场规模、份额、趋势和成长分析报告(2026-2034年) 农业无人机市场-全球产业规模、份额、趋势、机会及预测(按类型、组件、应用、地区和竞争格局划分),2021-2031年无人机资料管理软体市场:按部署类型、公司规模、解决方案类型和最终用户产业划分,全球预测(2026-2032年)

农业无人机市场-全球产业规模、份额、趋势、机会及预测(按类型、组件、应用、地区和竞争格局划分),2021-2031年无人机资料管理软体市场:按部署类型、公司规模、解决方案类型和最终用户产业划分,全球预测(2026-2032年) 农业无人机市场规模、份额和趋势分析报告:按类型、组件、农业环境、应用、地区和细分市场预测(2026-2033 年)

农业无人机市场规模、份额和趋势分析报告:按类型、组件、农业环境、应用、地区和细分市场预测(2026-2033 年) 尿素需求、产能、产量、价格分布、产业展望(截至2034年)

尿素需求、产能、产量、价格分布、产业展望(截至2034年)