|

市场调查报告书

商品编码

1936527

机器人即服务 (RaaS) 市场机会、成长要素、产业趋势分析及预测(2026-2035 年)Robotics as a Service (RaaS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

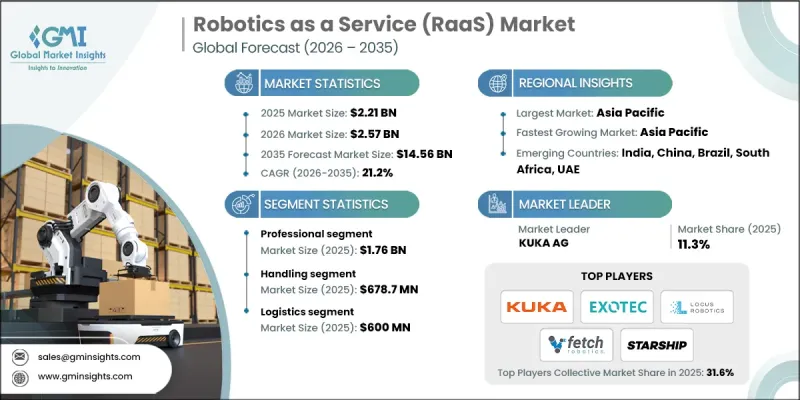

全球机器人即服务市场预计到 2025 年将达到 22.1 亿美元,到 2035 年将达到 145.6 亿美元,年复合成长率为 21.2%。

推动这一扩张的因素有很多,包括物流、製造和医疗保健行业严重的劳动力短缺,以及企业日益增长的从资本密集型投资模式转向营运支出模式的需求。人工智慧、云端机器人和自主导航技术的快速发展为远端操控机器人集群奠定了实际的基础,而远端操控机器人集群正是机器人即服务 (RaaS) 模式的基石。即时效能追踪、集中式软体更新和自适应学习使服务供应商能够有效管理分散式机器人,从而减少停机时间和维护成本,同时提高可靠性。基于订阅、以结果为导向的方法为企业提供扩充性、柔软性且随选的自动化解决方案,使其具有商业性吸引力。企业越来越依赖 RaaS 来维持营运连续性、优化生产力,并在无需漫长招募週期的情况下执行重复性或高离职率的任务。人工智慧、互联互通和智慧软体整合的融合进一步强化了对自动化的关注,使 RaaS 成为现代工业效率的关键驱动力。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 22.1亿美元 |

| 预测金额 | 145.6亿美元 |

| 复合年增长率 | 21.2% |

预计2025年,专业机器人市场规模将达到17.6亿美元。面对技术纯熟劳工短缺和提高生产力的压力,企业正在积极采用专业机器人。物流、医疗保健和製造业等行业尤其增加对机器人系统的投资,以维持业务连续性、提高效率并减少对专业人才的依赖。订阅式机器人服务正成为管理劳力密集流程、确保稳定生产且不影响效能的实用解决方案。

预计到2025年,搬运设备市场规模将达到6.787亿美元。物流自动化是推动这项需求的主要因素,仓库和配销中心越来越多地采用订阅式机器人服务来运输货物、减少错误、提高吞吐量,并缓解高峰期的人员短缺问题。先进的感测器和软体使自主移动机器人能够安全且有效率地搬运更重的货物,从而以较低的总成本为企业提供可靠的解决方案。

预计到2025年,北美将占据机器人即服务(RaaS)市场36.8%的份额,成为RaaS领域竞争最激烈的地区。美国和加拿大已建立起完善的技术生态系统,促进了自主移动机器人的快速普及,从而降低劳动成本并提高营运效率。该地区拥有广泛的数位基础设施和创新网络,为服务导向的机器人技术提供支持,并可在物流、医疗保健和智慧工厂等商业应用中实现可扩展的订阅式解决方案。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 物流、製造业和医疗领域劳动力短缺问题日益严重

- 从资本支出模式转向营运支出模式

- 人工智慧、云端机器人和自主导航技术的快速发展

- 对扩充性、柔软性的自动化解决方案的需求

- 基于绩效和订阅的经营模式正日益普及

- 陷阱与挑战

- 复杂用例的初始服务价格较高

- 资料安全、保障和合规性问题

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 永续发展倡议

- 供应链韧性

- 地缘政治分析

- 数位转型

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 按地区分類的企业发展比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年主要发展动态

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张与投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞赛的趋势

第五章 按类型分類的市场估算与预测,2022-2035年

- 面向专业人士

- 对于个人

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 处理

- 组装

- 自动贩卖机

- 加工

- 焊接和焊焊

- 其他的

7. 2022-2035年按最终用途产业分類的市场估算与预测

- 製造业

- 车

- 食品/饮料

- 后勤

- 卫生保健

- 零售

- 其他的

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- 主要企业

- Locus Robotics

- Fetch Robotics

- Sarcos Robotics

- 6 River Systems

- Exotec

- 按地区分類的主要企业

- 北美洲

- Aethon

- Savioke

- Cobalt Robotics

- Knightscope

- 欧洲

- Starship Technologies

- Sofigate

- Marble

- 亚太地区

- Liquid Robotics

- inVia Robotics

- 北美洲

- 小众/颠覆性公司

- Bossa Nova Robotics

- PrecisionHawk

- RedZone Robotics

- Hirebotics

- Fellow Robots

- Glomatriz

The Global Robotics as a Service Market was valued at USD 2.21 billion in 2025 and is estimated to grow at a CAGR of 21.2% to reach USD 14.56 billion by 2035.

The expansion is driven by multiple factors, including acute labor shortages across logistics, manufacturing, and healthcare sectors, and the increasing preference for shifting from capital-intensive investments to operating expenditure models. Rapid advancements in artificial intelligence, cloud robotics, and autonomous navigation technologies have created viable frameworks for remotely controlled robot fleets, which form the foundation of the RaaS model. Real-time performance tracking, centralized software updates, and adaptive learning not only reduce downtime and service costs but also improve reliability, enabling service providers to manage distributed robots efficiently. The subscription-based, outcome-oriented approach has become commercially attractive, offering businesses scalable, flexible, and on-demand automation solutions. Organizations increasingly rely on RaaS to maintain operational continuity, optimize productivity, and tackle repetitive or high-turnover tasks without the burden of long recruitment cycles. This growing emphasis on automation is reinforced by the convergence of AI, connectivity, and smart software integration, making RaaS a key driver of efficiency in modern industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.21 Billion |

| Forecast Value | $14.56 Billion |

| CAGR | 21.2% |

The professional segment was valued at USD 1.76 billion in 2025. Companies facing skilled labor shortages and productivity pressures are driving the adoption of professional robotics. Industries such as logistics, healthcare, and manufacturing are particularly invested in robotic systems to maintain operational continuity, improve efficiency, and reduce reliance on specialized personnel. Subscription-based robotic services are becoming a practical solution for managing labor-intensive processes and ensuring consistent output without compromising on performance.

The handling segment generated USD 678.7 million in 2025. Logistics automation is a significant driver of this demand, as warehouses and distribution centers increasingly deploy robots on a subscription basis to transport goods, minimize errors, increase throughput, and fill staffing gaps during peak periods. Advanced sensors and software enable autonomous mobile robots to move heavier loads safely and efficiently, offering businesses dependable solutions at a lower total cost.

North America Robotics as a Service Market held a 36.8% share in 2025, making it the most competitive region for RaaS. The U.S. and Canada have established technology ecosystems that facilitate the rapid adoption of autonomous mobile robots to reduce labor costs and enhance operational efficiency. The region benefits from extensive digital infrastructure and innovation networks that support service-oriented robotics and enable scalable subscription-based solutions in commercial applications across logistics, healthcare, and smart factories.

Key players in the Global Robotics as a Service Market include Fetch Robotics, Locus Robotics, Starship Technologies, 6 River Systems, Sarcos Robotics, Glomatriz, Savioke, Bossa Nova Robotics, Liquid Robotics, inVia Robotics, PrecisionHawk, Fellow Robots, Cobalt Robotics, Knightscope, RedZone Robotics, Marble, Hirebotics, Exotec, Sofigate, and Aethon. Companies in the Global Robotics as a Service (RaaS) Market strengthen their presence by focusing on advanced technology integration, service scalability, and strategic partnerships. Providers invest heavily in AI-driven navigation, cloud connectivity, and remote fleet management software to enhance robot efficiency and reduce downtime. They expand their footprint by collaborating with logistics, manufacturing, and healthcare operators to tailor solutions for industry-specific needs. Subscription-based pricing models, flexible deployment options, and outcome-oriented offerings attract cost-conscious clients.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Application trends

- 2.2.3 End-use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising labor shortages across logistics, manufacturing, and healthcare

- 3.2.1.2 Shift from capital expenditure to operating expenditure models

- 3.2.1.3 Rapid advancements in AI, cloud robotics, and autonomous navigation

- 3.2.1.4 Demand for scalable and flexible automation solutions

- 3.2.1.5 Growing adoption of outcome-based and subscription business models

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High initial service pricing for complex use cases

- 3.2.2.2 Data security, safety, and regulatory compliance concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Professional

- 5.3 Personal

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Handling

- 6.3 Assembling

- 6.4 Dispensing

- 6.5 Processing

- 6.6 Welding & Soldering

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Manufacturing

- 7.3 Automotive

- 7.4 Food & beverage

- 7.5 Logistics

- 7.6 Healthcare

- 7.7 Retail

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Locus Robotics

- 9.1.2 Fetch Robotics

- 9.1.3 Sarcos Robotics

- 9.1.4 6 River Systems

- 9.1.5 Exotec

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Aethon

- 9.2.1.2 Savioke

- 9.2.1.3 Cobalt Robotics

- 9.2.1.4 Knightscope

- 9.2.2 Europe

- 9.2.2.1 Starship Technologies

- 9.2.2.2 Sofigate

- 9.2.2.3 Marble

- 9.2.3 Asia Pacific

- 9.2.3.1 Liquid Robotics

- 9.2.3.2 inVia Robotics

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Bossa Nova Robotics

- 9.3.2 PrecisionHawk

- 9.3.3 RedZone Robotics

- 9.3.4 Hirebotics

- 9.3.5 Fellow Robots

- 9.3.6 Glomatriz

2026年全球机器人即服务(RaaS)市场报告

2026年全球机器人即服务(RaaS)市场报告 亚太地区机器人即服务 (RaaS) 市场按应用程式、最终用户、类型和国家划分 - 分析与预测 (2025-2035)

亚太地区机器人即服务 (RaaS) 市场按应用程式、最终用户、类型和国家划分 - 分析与预测 (2025-2035) 欧洲机器人即服务 (RaaS) 市场按应用程式、最终用户、类型和国家/地区划分 - 分析和预测 (2025-2035)

欧洲机器人即服务 (RaaS) 市场按应用程式、最终用户、类型和国家/地区划分 - 分析和预测 (2025-2035) 全球机器人即服务 (RaaS) 市场:按应用、最终用户、产品和国家分類的分析和预测 (2025-2035)

全球机器人即服务 (RaaS) 市场:按应用、最终用户、产品和国家分類的分析和预测 (2025-2035) 全球机器人即服务市场

全球机器人即服务市场 按类型、最终用途行业和地区分類的机器人即服务 (RaaS) 市场

按类型、最终用途行业和地区分類的机器人即服务 (RaaS) 市场 机器人即服务(RAAS) 的全球市场 2024-2028

机器人即服务(RAAS) 的全球市场 2024-2028 Raas(机器人即服务)市场:依类型、最终用户、地区划分 - 到 2030 年的全球预测

Raas(机器人即服务)市场:依类型、最终用户、地区划分 - 到 2030 年的全球预测