|

市场调查报告书

商品编码

1936528

二环戊二烯市场成长机会、成长要素、产业趋势分析及2026年至2035年预测Dicyclopentadiene (DCPD) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

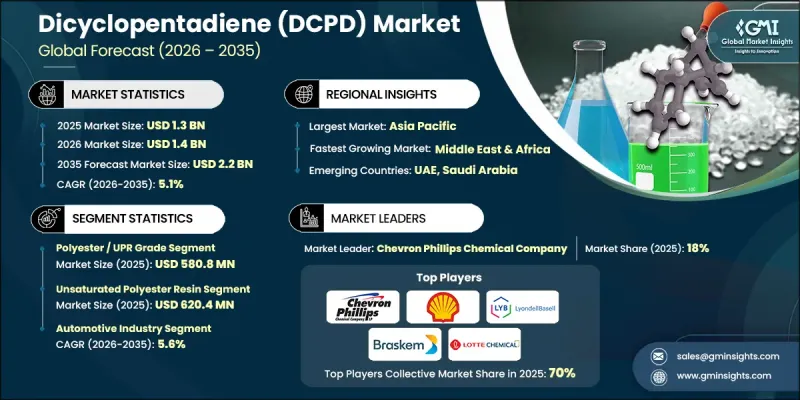

全球二环戊二烯市场预计到 2025 年将达到 13 亿美元,到 2035 年将达到 22 亿美元,年复合成长率为 5.1%。

随着医药包装产业的日益复杂化,对高性能包装解决方案的需求不断增长,而DCPD衍生的烃类树脂和黏合剂在这些解决方案的配方中发挥关键作用。虽然医药包装本身并不会直接消耗大量的DCPD,但其应用范围的扩大正在推动防护和防篡改系统中先进树脂和黏合剂中间体的应用,以满足严格的安全标准和合规要求。这进一步巩固了DCPD在化学和特殊材料领域的广泛价值链。另一个关键驱动因素是汽车产业转型为轻量化、高性能的材料。不饱和聚酯和聚DCPD复合材料越来越多地应用于车身面板、保险桿和结构件中,以满足燃油效率和排放气体目标。这些复合材料具有高强度重量比,使其在交通运输领域极具吸引力;此外,DCPD还能改善树脂系统的机械和热性能,从而推动其在汽车和航太领域的应用。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 13亿美元 |

| 预测金额 | 22亿美元 |

| 复合年增长率 | 5.1% |

到2025年,聚酯/UPR等级产品市场规模将达到5.808亿美元,这主要得益于其在建筑、汽车、船舶和基础设施等行业的不饱和聚酯树脂中的广泛应用。此外,其在玻璃纤维增强塑胶、模塑复合复合材料和耐腐蚀材料等领域也备受青睐,在这些领域,成本与性能之间的平衡至关重要。

2025 年,不饱和聚酯树脂 (UPR) 市值为 6.204 亿美元。基于 DCPD 的 UPR 在建筑、汽车、船舶和基础设施领域至关重要,因为它们为面板、管道、玻璃纤维增强部件和结构材料提供机械强度、耐腐蚀性、成本效益和可加工性。

预计到2025年,北美二环戊二烯市场将占全球市场份额的21%,其中美国将占据主导地位。这主要得益于美国高度发展的石化基础设施以及汽车、建筑和先进材料产业的强劲需求。轻型车辆、基础设施维修和耐腐蚀应用领域对DCPD基树脂和聚DCPD复合复合材料的需求不断增长,推动了市场成长。墨西哥湾沿岸地区石化工厂扩建的持续投资以及高性能聚合物和复合材料的日益普及,正在增强该地区的供应安全。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 汽车和航太领域对轻质复合材料的需求不断增长

- 风力发电的扩张推动了对多晶硅直流背压片电阻器(Poly-DCPD RIM)的需求。

- 药品包装需求不断成长

- 产业潜在风险与挑战

- 原料供应的不确定性

- 资本密集型生产基础设施

- 市场机会

- 自修復聚合物在风力发电的应用

- 3D列印与积层製造

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 各等级市场估算与预测,2022-2035年

- 超高纯度

- 高纯度

- 聚酯/UPR级

- 烃类树脂级

- 粗製DCPD

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 不饱和聚酯树脂

- 烃类树脂

- EPDM弹性体

- 环烯烃共聚物(COC)和聚合物(COP)

- 聚合物DCPD

- 其他的

7. 2022-2035年按最终用途产业分類的市场估算与预测

- 汽车产业

- 航运业

- 建设业

- 包装产业

- 航太与国防

- 其他的

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- Chevron Phillips Chemical Company

- Shell Chemicals

- Braskem

- LyondellBasell Industries

- LOTTE Chemical

- NOVA Chemicals Corporation

- Zeon Corporation

- Formosa Chemicals &Fibre Corporation

- Core Molding Technologies

- Mitsui Chemicals

- Eastman Chemical Company

- LG Chem

The Global Dicyclopentadiene Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 2.2 billion by 2035.

The rising sophistication of the pharmaceutical packaging industry is creating demand for high-performance packaging solutions, where DCPD-derived hydrocarbon resins and adhesives play a critical role in formulations. Although pharmaceutical packaging does not directly consume large volumes of DCPD, its expansion drives the adoption of advanced resin and adhesive intermediates in protective and tamper-evident systems to meet strict safety and compliance requirements. This, in turn, strengthens the broader DCPD value chain across chemicals and specialty materials. Another significant driver is the automotive sector's shift toward lightweight, high-performance materials, with unsaturated polyester and poly-DCPD composites increasingly utilized in body panels, bumpers, and structural components to meet fuel efficiency and emission reduction targets. These composites provide high strength-to-weight ratios, making them attractive for transportation applications, while DCPD enhances the mechanical and thermal performance of resin systems, boosting adoption in automotive and aerospace segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.1% |

The polyester/UPR grade segment accounted for USD 580.8 million in 2025, driven by its extensive use in unsaturated polyester resins across construction, automotive, marine, and infrastructure applications. Its popularity is linked to fiberglass-reinforced plastics, molded composites, and corrosion-resistant materials, where the balance of cost and performance is essential.

The unsaturated polyester resin (UPR) segment generated USD 620.4 million in 2025, as DCPD-based UPRs offer mechanical strength, corrosion resistance, cost efficiency, and processability for panels, pipes, fiberglass-reinforced components, and structural materials, making them indispensable in construction, automotive, marine, and infrastructure sectors.

North America Dicyclopentadiene Market accounted for 21% share in 2025, with the United States leading the region due to its well-developed petrochemical infrastructure and strong demand from automotive, construction, and advanced materials industries. Growth is fueled using DCPD-based resins and poly-DCPD composites in lightweight vehicles, infrastructure repair, and corrosion-resistant applications. Ongoing investments in petrochemical capacity along the Gulf Coast and increased deployment of high-performance polymers and composites are strengthening supply security in the region.

Key players operating in the Global Dicyclopentadiene Market include NOVA Chemicals Corporation, Zeon Corporation, Chevron Phillips Chemical Company, Shell Chemicals, Braskem, LOTTE Chemical, Formosa Chemicals & Fibre Corporation, Core Molding Technologies, Mitsui Chemicals, LyondellBasell Industries, Eastman Chemical Company, and LG Chem. Companies in the Dicyclopentadiene (DCPD) Market are enhancing their foothold by investing heavily in R&D to develop high-performance resin and composite solutions tailored to end-use industries such as automotive, aerospace, and construction. Strategic collaborations with OEMs and specialty chemical manufacturers ensure early integration of DCPD-based composites and adhesives into new product lines. Firms are expanding production capacities, improving supply chain efficiency, and enhancing regional distribution networks to meet rising global demand. Product innovation, cost optimization, and development of multifunctional resin systems are being leveraged to differentiate offerings, while compliance with international standards strengthens credibility. Additionally, companies focus on sustainability, lightweighting solutions, and technical support services to drive adoption and maintain a competitive edge across key applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Grade

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for lightweight composites in automotive & aerospace

- 3.2.1.2 Wind energy expansion driving Poly-DCPD RIM demand

- 3.2.1.3 Rising pharmaceutical packaging demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material supply uncertainty

- 3.2.2.2 Capital-intensive production infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Self-healing polymer applications in wind energy

- 3.2.3.2 3D printing & additive manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022 - 2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Ultra-high purity grade

- 5.3 High purity grade

- 5.4 Polyester / UPR Grade

- 5.5 Hydrocarbon resin grade

- 5.6 Crude DCPD

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Unsaturated Polyester Resin

- 6.3 Hydrocarbon Resins

- 6.4 EPDM Elastomers

- 6.5 Cyclic Olefin Copolymer (COC) & Polymer (COP)

- 6.6 Poly-DCPD

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive industry

- 7.3 Marine industry

- 7.4 Construction

- 7.5 Packaging industry

- 7.6 Aerospace & defense

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Chevron Phillips Chemical Company

- 9.2 Shell Chemicals

- 9.3 Braskem

- 9.4 LyondellBasell Industries

- 9.5 LOTTE Chemical

- 9.6 NOVA Chemicals Corporation

- 9.7 Zeon Corporation

- 9.8 Formosa Chemicals & Fibre Corporation

- 9.9 Core Molding Technologies

- 9.10 Mitsui Chemicals

- 9.11 Eastman Chemical Company

- 9.12 LG Chem

全球二环戊二烯(DCPD)市场规模、份额、趋势和成长分析报告(2026-2034年)

全球二环戊二烯(DCPD)市场规模、份额、趋势和成长分析报告(2026-2034年) 二环戊二烯市场规模、份额及成长分析(按类型、最终用户、应用和地区划分)-2026-2033年产业预测

二环戊二烯市场规模、份额及成长分析(按类型、最终用户、应用和地区划分)-2026-2033年产业预测 全球环戊二烯(CPD)和双环戊二烯(DCPD)市场需求及预测分析(2018-2034)

全球环戊二烯(CPD)和双环戊二烯(DCPD)市场需求及预测分析(2018-2034) 2025-2033年双环戊二烯市场类型、应用、最终用户和地区报告双环戊二烯市场,规模,占有率,趋势,产业分析报告:各用途,各等级,各地区 - 市场预测,2025年~2034年

2025-2033年双环戊二烯市场类型、应用、最终用户和地区报告双环戊二烯市场,规模,占有率,趋势,产业分析报告:各用途,各等级,各地区 - 市场预测,2025年~2034年 全球双环戊二烯(DCPD)市场2024-2028

全球双环戊二烯(DCPD)市场2024-2028 双环戊二烯 (DCPD) 市场:全球规模、份额、趋势分析、机会、预测,2019-2030 年双环戊二烯市场 - 2024 年至 2029 年预测

双环戊二烯 (DCPD) 市场:全球规模、份额、趋势分析、机会、预测,2019-2030 年双环戊二烯市场 - 2024 年至 2029 年预测