|

市场调查报告书

商品编码

1936529

丙烯酸乳液市场机会、成长要素、产业趋势分析及2026年至2035年预测Acrylic Emulsion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

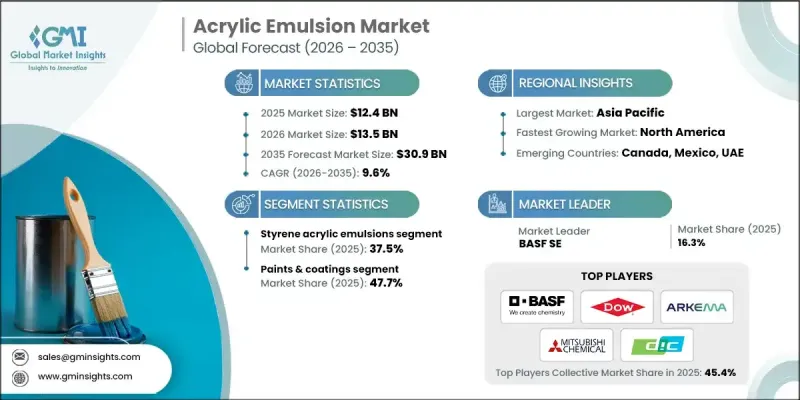

全球丙烯酸乳液市场预计到 2025 年将达到 124 亿美元,到 2035 年将达到 309 亿美元,年复合成长率为 9.6%。

丙烯酸乳液是一种合成弹性体,具有优异的耐热性、耐化学性和耐多种流体性能,使其成为需要高性能密封和涂层解决方案的行业不可或缺的材料。其主要应用领域包括汽车、航太、化工以及石油天然气产业。市场动态受原材料(包括丙烯酸单体和其他化学原料)的供应和价格的强烈影响,而这些原材料的价格会因地缘政治事件和自然灾害造成的供应中断而波动。成本的快速波动为製造商维持产品价格稳定带来了挑战,可能导致利润率下降并影响营运效率。永续性趋势正在重塑该行业,水性、低VOC丙烯酸乳液正日益受到青睐,以应对日益严格的环境法规和消费者对环保配方不断增长的需求。对更绿色、更安全解决方案的追求预计将塑造市场的长期成长轨迹。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 124亿美元 |

| 预测金额 | 309亿美元 |

| 复合年增长率 | 9.6% |

预计到2025年,苯乙烯丙烯酸乳液市占率将达到37.5%,并在2035年之前以9.4%的复合年增长率成长。这些乳液因其性能和成本效益的平衡而备受青睐,尤其是在装饰涂料、黏合剂和密封剂领域。它们具有防水、耐用和经济的涂层特性,使其适用于从消费品到快速都市化市场等广泛的应用领域。

到2025年,涂料领域将占据47.7%的市场。丙烯酸乳液广泛应用于建筑、室内、室外和工业涂料。特别是室内涂料,具有附着力强、耐久性好、VOC排放低等优点,使其适用于住宅和商业环境。对高品质涂料的稳定需求持续推动全球市场的扩张。

预计2026年至2035年,北美丙烯酸乳液市场将以9.4%的复合年增长率成长。这一成长主要得益于污水回收、废水处理以及符合循环经济原则的永续製造等产业的创新。此外,消费者在个人护理、清洁和医疗保健领域对环保产品的日益关注和偏好,也促使企业采用符合更严格生态学标准的丙烯酸乳液,从而进一步推动市场发展。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 对环保低VOC涂料的需求日益增长

- 建设产业的成长正在推动对丙烯酸乳胶漆的需求。

- 丙烯酸乳液在功能性整理的应用促进了纺织业的发展。

- 产业潜在风险与挑战

- 对环保低VOC涂料的需求日益增长

- 建设产业的成长正在推动对丙烯酸乳胶漆的需求。

- 市场机会

- 包装和标籤行业需求不断增长

- 拓展至创新环保配方

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

(註:贸易统计数据仅涵盖主要国家。)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 按类型分類的市场估算与预测,2022-2035年

- 纯丙烯酸乳液

- 苯乙烯丙烯酸乳液

- 乙烯基丙烯酸乳液

- 丙烯酸Silicone emulsion

- 其他的

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 油漆和涂料

- 建筑涂料

- 室内涂料

- 外墙涂料

- 工业涂料

- 汽车涂料

- 木器漆

- 金属漆

- 其他的

- 特种涂料

- 船舶涂料

- 保护漆

- 其他的

- 建筑涂料

- 黏合剂和密封剂

- 压敏黏着剂

- 建筑黏合剂

- 包装黏合剂

- 其他的

- 建筑材料

- 水泥改质剂

- 防水剂

- 水泥浆和砂浆

- 其他的

- 纤维和不织布

- 纺织加工剂

- 不织布黏合剂

- 其他的

- 纸张/包装

- 纸颜料

- 包装涂料

- 其他的

- 其他的

7. 2022-2035年按最终用途产业分類的市场估算与预测

- 建筑/施工

- 住宅

- 商业建筑

- 基础设施开发

- 汽车/运输设备

- 搭乘用车

- 商用车辆

- 其他的

- 工业的

- 金属加工

- 化学加工

- 其他的

- 消费品

- 家具

- 家用电器

- 其他的

- 包装

- 食品/饮料包装

- 消费品包装

- 工业包装

- 纺织品和皮革

- 其他的

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- BASF SE

- AkzoNobel NV

- Allnex

- Arkema SA

- Asian Paints

- Celanese Corporation

- DIC Corporation

- Dow Inc.

- Evonik Industries AG

- Lubrizol Corporation

- Mitsubishi Chemical Corporation

- Momentive Performance Materials Inc

- Sika AG

- Synthomer plc

- Wacker Chemie AG

The Global Acrylic Emulsion Market was valued at USD 12.4 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 30.9 billion by 2035.

Acrylic emulsions are synthetic elastomers known for their excellent resistance to heat, chemicals, and a variety of fluids, making them indispensable in industries that demand high-performance sealing and coating solutions. Key applications span automotive, aerospace, chemical processing, and oil and gas sectors. Market dynamics are strongly influenced by the availability and pricing of raw materials, including acrylic monomers and other chemical inputs, which can fluctuate due to geopolitical events or natural disruptions. Sudden cost volatility can challenge manufacturers in maintaining stable product pricing, potentially compressing profit margins and affecting operational efficiency. Sustainability trends are shaping the industry, with water-based, low-VOC acrylic emulsions gaining prominence in response to stricter environmental regulations and increasing consumer demand for eco-friendly formulations. The drive for greener, safer solutions is expected to shape the market's long-term growth trajectory.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $30.9 Billion |

| CAGR | 9.6% |

The styrene acrylic emulsions segment accounted for 37.5% share in 2025 and is anticipated to grow at a CAGR of 9.4% through 2035. These emulsions are highly valued for their combination of performance and cost efficiency, particularly in applications such as decorative coatings, adhesives, and sealants. They offer water-resistance, durability, and cost-effective coverage, which make them suitable for both consumer-grade products and rapidly urbanizing markets.

The paints & coatings segment held a 47.7% share in 2025. Acrylic emulsions are extensively used across architectural, interior, exterior, and industrial coatings. Interior coatings, in particular, benefit from strong adhesion, long-lasting durability, and low VOC emissions, making them suitable for residential and commercial environments. The consistent demand for high-quality paints and coatings continues to drive market expansion globally.

North America Acrylic Emulsion Market is projected to grow at a CAGR of 9.4% share from 2026 to 2035. Growth is fueled by industrial innovations in wastewater recycling, effluent treatment, and sustainable manufacturing aligned with circular economy principles. Additionally, increasing consumer awareness and preference for environmentally friendly products across personal care, cleaning, and healthcare sectors are encouraging companies to adopt acrylic emulsions that meet stricter ecological standards, further supporting market development.

Leading players in the Global Acrylic Emulsion Market include BASF SE, AkzoNobel N.V., Allnex, Arkema S.A., Asian Paints, Celanese Corporation, DIC Corporation, Dow Inc., Evonik Industries AG, Lubrizol Corporation, Mitsubishi Chemical Corporation, Momentive Performance Materials Inc., Sika AG, Synthomer plc, and Wacker Chemie AG. Companies in the acrylic emulsion industry are employing diverse strategies to strengthen their market position. They are investing heavily in research and development to create eco-friendly, low-VOC, and water-based formulations that comply with evolving environmental regulations. Strategic partnerships with regional distributors and suppliers help expand supply chains and reach new end-use markets. Continuous product innovation, branding initiatives, and marketing campaigns emphasize sustainability and performance benefits, while targeted pricing strategies and flexible production capacities ensure competitiveness across price-sensitive and premium markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for eco-friendly and low-VOC coatings

- 3.2.1.2 Growth in the construction industry, driving demand for acrylic emulsion-based paints

- 3.2.1.3 Growth in the textile industry, leveraging acrylic emulsions in functional finishes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Increasing demand for eco-friendly and low-VOC coatings

- 3.2.2.2 Growth in the construction industry, driving demand for acrylic emulsion-based paints

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in packaging and labeling industries

- 3.2.3.2 Expansion into innovative and eco-friendly formulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pure acrylic emulsions

- 5.3 Styrene acrylic emulsions

- 5.4 Vinyl acrylic emulsions

- 5.5 Acrylic silicone emulsions

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Paints & coatings

- 6.2.1 Architectural coatings

- 6.2.1.1 Interior coatings

- 6.2.1.2 Exterior coatings

- 6.2.1.3 Industrial coatings

- 6.2.2 Automotive coatings

- 6.2.2.1 Wood coatings

- 6.2.2.2 Metal coatings

- 6.2.2.3 Others

- 6.2.3 Special purpose coatings

- 6.2.3.1 Marine coatings

- 6.2.3.2 Protective coatings

- 6.2.3.3 Others

- 6.2.1 Architectural coatings

- 6.3 Adhesives & sealants

- 6.3.1 Pressure-sensitive adhesives

- 6.3.2 Construction adhesives

- 6.3.3 Packaging adhesives

- 6.3.4 Others

- 6.4 Construction materials

- 6.4.1 Cement modifiers

- 6.4.2 Waterproofing compounds

- 6.4.3 Grouts and mortars

- 6.4.4 Others

- 6.5 Textiles & nonwovens

- 6.5.1 Textile finishes

- 6.5.2 Nonwoven binders

- 6.5.3 Others

- 6.6 Paper & packaging

- 6.6.1 Paper coatings

- 6.6.2 Packaging coatings

- 6.6.3 Others

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Building & construction

- 7.2.1 Residential construction

- 7.2.2 Commercial construction

- 7.2.3 Infrastructure development

- 7.3 Automotive & transportation

- 7.3.1 Passenger vehicles

- 7.3.2 Commercial vehicles

- 7.3.3 Others

- 7.4 Industrial

- 7.4.1 Metal processing

- 7.4.2 Chemical processing

- 7.4.3 Others

- 7.5 Consumer goods

- 7.5.1 Furniture

- 7.5.2 Appliances

- 7.5.3 Others

- 7.6 Packaging

- 7.6.1 Food & beverage packaging

- 7.6.2 Consumer goods packaging

- 7.6.3 Industrial packaging

- 7.7 Textile & leather

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 AkzoNobel N.V

- 9.3 Allnex

- 9.4 Arkema S.A

- 9.5 Asian Paints

- 9.6 Celanese Corporation

- 9.7 DIC Corporation

- 9.8 Dow Inc.

- 9.9 Evonik Industries AG

- 9.10 Lubrizol Corporation

- 9.11 Mitsubishi Chemical Corporation

- 9.12 Momentive Performance Materials Inc

- 9.13 Sika AG

- 9.14 Synthomer plc

- 9.15 Wacker Chemie AG