|

市场调查报告书

商品编码

1936555

印刷基板市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Printed Circuit Board (PCB) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

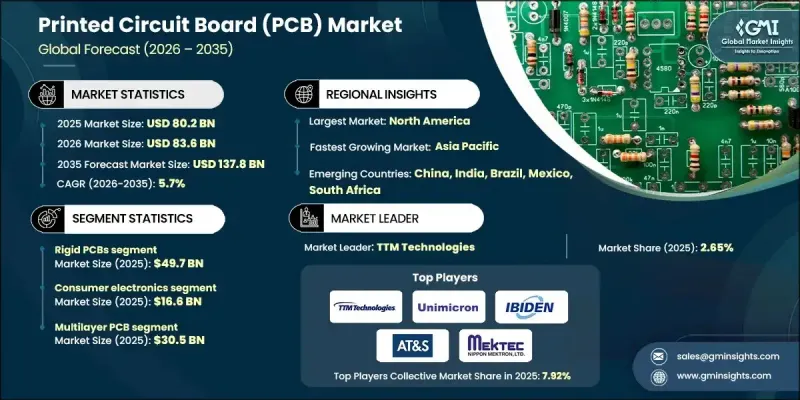

全球印刷电路基板(PCB) 市场预计到 2025 年将达到 802 亿美元,到 2035 年将达到 1,378 亿美元,年复合成长率为 5.5%。

这一成长主要源自于现代电子设备日益复杂的特性,推动了PCB设计朝更大、更先进的方向发展。业界需要高效率的组装设备,能够处理多层、高密度基板,同时保持热稳定性和讯号完整性。 5G网路、人工智慧运算和高速资料中心的普及,推动了对尖端材料和超低损耗PCB的需求。为了确保包括家用电子电器、工业机械、通讯和穿戴式技术在内的所有领域的品质、可靠性和扩充性,业界正越来越多地采用自动化组装、精密焊接和检测工具。对小型化、弹性化和多方向元件日益增长的需求,进一步推动了全球先进PCBA解决方案的普及。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 802亿美元 |

| 预测金额 | 1378亿美元 |

| 复合年增长率 | 5.5% |

预计2025年,柔性PCB市场规模将达到440亿美元。柔性组件因其轻巧紧凑的设计、多向连接性以及易于整合到可穿戴设备、医疗设备、物联网和汽车系统中等优势而备受青睐。成熟的製造工艺和扩充性使其成为大规模生产的理想选择。

预计到2025年,波峰焊接市场规模将达到5,28亿美元,并且仍然是大批量PCB组装的首选方法。其均匀的焊料涂覆、可靠性以及对通孔元件的适应性,使其成为製造复杂基板的关键技术。生产线自动化程度的不断提高,持续推动波峰焊接技术在各工业领域的应用。

预计到2025年,北美印刷电路基板(PCB)市占率将达到75.9%。来自航太、国防、医疗电子和汽车产业的强劲需求,以及製造业回流计画和政府支援措施(例如美国《晶片製造和整合计画法案》),正在增强美国国内的PCB组装能力。 5G的部署和在电动车中的整合正在推动高密度基板(HDI)和软式电路板的应用,而永续性倡议则加速了无铅和环保材料的使用。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 家用电器和物联网设备的需求增加

- 汽车电子产品和电动车(EV)的扩张

- 扩大5G基础设施和通讯领域的应用

- 在工业自动化和智慧製造领域不断扩大应用

- 高密度基板(HDI)和柔性PCB的进展

- 产业潜在风险与挑战

- 供应链中断与原物料价格波动

- 生产製造流程复杂度高,成本压力大

- 市场机会

- 与电动车 (EV) 和先进汽车电子产品的集成

- 拓展至5G基础设施及通讯领域

- 司机

- 成长潜力分析

- 监管环境

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 永续性措施

- 消费者心理分析

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线丰富

- 科技

- 创新

- 按地区分類的企业发展比较

- 全球扩张分析

- 服务网路覆盖范围

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年主要发展动态

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张与投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞赛的趋势

第五章 依基板结构分類的市场估算与预测,2022-2035年

- 刚性PCB

- 软式电路板(FPC)

- 软硬复合基板

第六章 按类型分類的市场估算与预测,2022-2035年

- 单面印刷基板

- 双面印刷基板

- 多层印刷电路基板

- 高层数印刷基板

第七章 依基板的市场估算与预测,2022-2035年

- FR-4(玻璃环氧树脂)

- 金属核

- 聚酰亚胺

- PTFE

- 陶瓷基板

- 其他的

8. 2022-2035年按最终用途产业分類的市场估算与预测

- 家用电子电器

- 车

- 电讯

- 工业电子

- 医疗设备

- 航太/国防

- 计算资料中心

- 其他的

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 全球公司:

- AT&S

- Ibiden

- Nippon Mektron

- Samsung Electro-Mechanics

- Tripod Technology

- TTM Technologies

- Unimicron

- 当地公司

- Allied Circuit(ACCL)

- Benchmark Electronics

- Compeq Manufacturing

- Daeduck Electronics

- Meiko Electronics

- Sanmina

- Schweizer Electronic

- 新兴企业

- Cirexx

- Epec

- Flex

- Jabil

- Sheldahl(Multek/Flex subsidiary)

The Global Printed Circuit Board (PCB) Market was valued at USD 80.2 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 137.8 billion by 2035.

The growth is driven by the increasing complexity of modern electronic devices and the shift toward larger and more sophisticated PCB designs. Industries are demanding highly efficient assembly machines capable of handling multi-layer, high-density boards while maintaining thermal stability and signal integrity. The proliferation of 5G networks, AI computing, and high-speed data centers has fueled the need for advanced materials and ultra-low-loss PCBs. The industry is embracing automated assembly, precision soldering, and inspection tools to ensure quality, reliability, and scalability across sectors, including consumer electronics, industrial machinery, telecommunications, and wearable technology. Rising demand for miniaturized, flexible, and multi-directional devices is further boosting the adoption of advanced PCBA solutions globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $80.2 billion |

| Forecast Value | $137.8 billion |

| CAGR | 5.5% |

The flexible PCB segment generated USD 44 billion in 2025. Flexible assemblies are highly sought for their lightweight, compact designs, multi-directional connectivity, and integration into wearables, medical devices, IoT, and automotive systems. Their established production processes and scalability make them ideal for high-volume manufacturing.

The wave soldering segment accounted for USD 52.8 billion in 2025 and remains a preferred method for high-volume PCB assembly. Its uniform solder application, reliability, and suitability for through-hole components make it critical for complex board manufacturing. Growing automation in production lines continues to drive wave soldering adoption across various industries.

North America Printed Circuit Board (PCB) Market held 75.9% share in 2025. Strong demand from aerospace, defense, medical electronics, and automotive sectors, combined with reshoring initiatives and government incentives such as the U.S. CHIPS Act, has strengthened domestic PCB assembly capabilities. Adoption of HDI and flexible assemblies is rising with 5G deployment and electric vehicle integration, while sustainability efforts are accelerating the use of lead-free and eco-friendly materials.

Key players in the Global Printed Circuit Board (PCB) Market include Alfa Electronics, ALLPCB.com, Altek Electronics, Inc., Benchmark Electronics, Inc., Bittele Electronics Inc., Clarydon Electronic Services Limited, Eurocircuits, Jayshree Instruments Pvt. Ltd, Miracle Electronics Devices Pvt Ltd, PCB Assembly Express, INC, PCB Power Market, PCB Unlimited, PCBGOGO, PCBWay, Podrain Electronics, RAYMING TECHNOLOGY, Seeed Technology Co., Ltd., Tempo, Vexos, Visual Communications Company, LLC, and WellPCB Technology Co., Ltd. Companies in the Printed Circuit Board (PCB) Market are employing several strategies to strengthen their market position. These include investing in R&D for high-density and flexible PCB assembly technologies, expanding production capacities to meet growing demand, and adopting automation to improve efficiency and reduce defects. Strategic partnerships, mergers, and acquisitions allow firms to broaden their client base and enter new geographic regions. Companies are also prioritizing sustainability by introducing lead-free and environmentally friendly manufacturing processes. Offering end-to-end solutions, including design, assembly, testing, and after-sales support, enhances customer loyalty and long-term retention, while digitalization and AI-enabled production lines improve quality control and operational agility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 PCB structure trends

- 2.2.3 Type trends

- 2.2.4 Substrate trends

- 2.2.5 End Use industry trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand from Consumer Electronics and IoT Devices

- 3.2.1.2 Expansion of Automotive Electronics and Electric Vehicles (EVs)

- 3.2.1.3 Growing Adoption in 5G Infrastructure and Telecommunications

- 3.2.1.4 Increased Use in Industrial Automation and Smart Manufacturing

- 3.2.1.5 Advancements in High-Density Interconnect (HDI) and Flexible PCBs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply Chain Disruptions and Raw Material Volatility

- 3.2.2.2 High Manufacturing Complexity and Cost Pressures

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with Electric Vehicles (EVs) and Advanced Automotive Electronics

- 3.2.3.2 Expansion into 5G Infrastructure and Telecommunications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Sustainability Measures

- 3.13 Consumer Sentiment Analysis

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit Margin

- 4.3.1.3 R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1 Product Range Breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global Footprint Analysis

- 4.3.3.2 Service Network Coverage

- 4.3.3.3 Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates and Forecast, By PCB Structure, 2022 - 2035 ($ Bn & Units)

- 5.1 Key trends

- 5.2 Rigid PCB

- 5.3 Flexible PCB (FPC)

- 5.4 Rigid-flex PCB

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Bn & Units)

- 6.1 Key trends

- 6.2 Single-sided PCB

- 6.3 Double-sided PCB

- 6.4 Multilayer PCB

- 6.5 High-Layer-Count PCB

Chapter 7 Market Estimates and Forecast, By Substrate, 2022 - 2035 ($ Bn & Units)

- 7.1 Key trends

- 7.2 FR-4 (Glass Epoxy)

- 7.3 Metal-core

- 7.4 Polyimide

- 7.5 PTFE

- 7.6 Ceramic Substrate

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 ($ Bn & Units)

- 8.1 Key trends

- 8.2 Consumer Electronics

- 8.3 Automotive

- 8.4 Telecommunications

- 8.5 Industrial Electronics

- 8.6 Medical Devices

- 8.7 Aerospace & Defense

- 8.8 Computing & Data Centers

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Bn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players:

- 10.1.1 AT&S

- 10.1.2 Ibiden

- 10.1.3 Nippon Mektron

- 10.1.4 Samsung Electro-Mechanics

- 10.1.5 Tripod Technology

- 10.1.6 TTM Technologies

- 10.1.7 Unimicron

- 10.2 Regional Players

- 10.2.1 Allied Circuit (ACCL)

- 10.2.2 Benchmark Electronics

- 10.2.3 Compeq Manufacturing

- 10.2.4 Daeduck Electronics

- 10.2.5 Meiko Electronics

- 10.2.6 Sanmina

- 10.2.7 Schweizer Electronic

- 10.3 Emerging Players

- 10.3.1 Cirexx

- 10.3.2 Epec

- 10.3.3 Flex

- 10.3.4 Jabil

- 10.3.5 Sheldahl (Multek / Flex subsidiary)

印刷基板市场报告:按类型、基板、最终用途产业和地区划分(2026-2034 年)

印刷基板市场报告:按类型、基板、最终用途产业和地区划分(2026-2034 年) 印刷基板组装市场机会、成长要素、产业趋势分析及预测(2026年至2035年)

印刷基板组装市场机会、成长要素、产业趋势分析及预测(2026年至2035年) 2026年全球印刷基板市场报告2026年全球铜币印刷电路基板(PCB)市场报告

2026年全球印刷基板市场报告2026年全球铜币印刷电路基板(PCB)市场报告 PCB检测服务市场:按检测技术、产品类型、服务模式、应用和最终用户划分,全球预测(2026-2032年)电视PCB电路基板市场按类型、层数、基板、封装技术和应用划分-全球预测,2026-2032年

PCB检测服务市场:按检测技术、产品类型、服务模式、应用和最终用户划分,全球预测(2026-2032年)电视PCB电路基板市场按类型、层数、基板、封装技术和应用划分-全球预测,2026-2032年 欧洲印刷基板市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲印刷基板市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 高密度互连电子市场预测至2032年:按产品类型、材料、技术、最终用户和地区分類的全球分析

高密度互连电子市场预测至2032年:按产品类型、材料、技术、最终用户和地区分類的全球分析 印刷电路板市场:产业趋势及全球预测(至 2035 年)-依 PCB 类型、材料类型、应用和地区划分

印刷电路板市场:产业趋势及全球预测(至 2035 年)-依 PCB 类型、材料类型、应用和地区划分 高频高速基板:2025-2031年全球市占率及排名、总营收及需求预测

高频高速基板:2025-2031年全球市占率及排名、总营收及需求预测