|

市场调查报告书

商品编码

1936594

主动式及智慧包装市场机会、成长要素、产业趋势分析及预测(2026-2035年)Active and Intelligent Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球主动式智慧包装市场预计到 2025 年将达到 149 亿美元,到 2035 年将达到 414 亿美元,年复合成长率为 11%。

该市场的成长主要受消费者对保存食品需求不断增长以及食品安全和品质意识日益增强的推动。尖端材料和感测器技术的创新使得包装技术能够与产品进行主动交互,从而即时提供产品新鲜度、劣化和环境状况等资讯。全球加工食品和包装食品消费量的成长正在推动对能够确保产品品质、防止污染并提供透明度的包装的需求,并加速其普及应用。製造商和零售商也正在采用主动式和智慧包装技术,以减少废弃物、遵守监管要求并提高供应链效率。消费者偏好、监管压力和技术进步的融合,为未来十年市场的持续成长奠定了基础。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 149亿美元 |

| 预测金额 | 414亿美元 |

| 复合年增长率 | 11% |

预计到2025年,活性包装市场规模将达到90亿美元。活性包装广泛应用于延长产品保质期、维持产品品质以及防止污染,其原理包括使用氧气吸收剂、水分吸收剂和抗菌剂等。活性包装能够直接与包装产品相互作用,这使其在食品、饮料和製药等行业中具有关键优势。企业正日益整合这些技术,以确保产品完整性、减少变质并符合严格的安全标准,进一步推动全球对活性包装解决方案的需求。

预计到2025年,食品饮料产业市场规模将达到59亿美元。该产业率先采用主动式和智慧包装解决方案,运用保鲜指示器、氧气吸收剂、水分吸收剂和抗菌薄膜等技术,以维持产品品质、延长保质期并符合食品安全法规。该行业的企业正在加速采用这些解决方案,以最大限度地减少废弃物、改善库存管理、优化供应链效率,并满足消费者对安全新鲜产品日益增长的期望。领先的食品饮料製造商持续投资于包装创新和自动化,进一步巩固了该行业的领先地位。

预计到2025年,北美的主动式智慧包装市占率将达到31.7%。该地区受惠于良好的营商环境、食品饮料产业的强劲投资、先进的物流基础设施以及强大的研发生态系统。美国市场由强大的包装技术公司、研究机构和创新中心网路支撑,这些公司和中心专注于主动式包装、智慧标籤和感测器整合。这些因素使企业能够快速推出新型包装解决方案,从而提高产品安全性、可追溯性和消费者参与度,使北美成为该行业的全球领导者。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 对食品安全和品质的需求日益增长

- 电子商务和低温运输物流的成长

- 智慧感测器和射频识别技术的进步

- 监管重点在于减少食物废弃物和提高食物可追溯性

- 使用永续和可生物降解的包装

- 产业潜在风险与挑战

- 先进封装的高成本和复杂性

- 回收和监管合规方面的挑战

- 市场机会

- 整合数位技术和物联网包装

- 拓展包装在製药和医疗领域的应用

- 司机

- 成长潜力分析

- 监管环境

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 永续性措施

- 全球消费者态度分析

- 专利分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线丰富

- 科技

- 创新

- 按地区分類的企业发展比较

- 全球足迹分析

- 服务网路覆盖范围

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 新兴企业

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年主要发展动态

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张与投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞赛的趋势

第五章 依技术类型分類的市场估算与预测,2022-2035年

- 活性包装

- 氧气吸收剂

- 吸湿剂

- 乙烯吸收剂

- 抗菌剂

- 温控包装

- 味道和气味吸收剂

- 智慧包装

- 时间温度指示器 (TTIS)

- RFID标籤和QR码

- 新鲜度指标

- 气体感测器

- 智慧标籤

- 互动包装

第六章 依功能分類的市场估计与预测,2022-2035年

- 延长储存期

- 水分管理

- 氧气控制

- 乙烯控制

- 抗菌保护

- 品质保证

- 新鲜度指标

- 时间温度指示器

- 可追溯性和安全性

- RFID标籤

- QR码

- 防篡改包装

- 消费者互动

- 互动包装

- 智慧标籤

第七章 包装材料市场估价与预测(2022-2035年)

- 塑胶

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚对苯二甲酸乙二醇酯(PET)

- 纸和纸板

- 纸板

- 纸盒

- 玻璃

- 瓶子

- 瓶子

- 金属

- 能

- 挫败

- 可生物降解材料

- 淀粉基材料

- 聚乳酸(PLA)

第八章 依最终用途产业分類的市场估算与预测,2022-2035年

- 食品/饮料

- 生鲜食品

- 加工食品

- 饮料

- 麵包糖果甜点

- 製药和医疗保健

- 製药

- 医疗设备

- 营养补充品

- 个人护理及化妆品

- 护肤品

- 护髮产品

- 化妆品

- 消费性电子产品

- 行动电话

- 穿戴式装置

- 配件

- 物流和供应链

- 仓储

- 运输

- 零售

- 其他的

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 3M Company

- Amcor Ltd.

- Avery Dennison Corporation

- CCL Industries Inc.

- Coveris Holdings SA

- Constantia Flexibles Group GmbH

- Dai Nippon Printing Co., Ltd.

- DuPont de Nemours, Inc.

- Huhtamaki Oyj

- Mondi plc

- Multisorb Technologies, Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Stora Enso Oyj

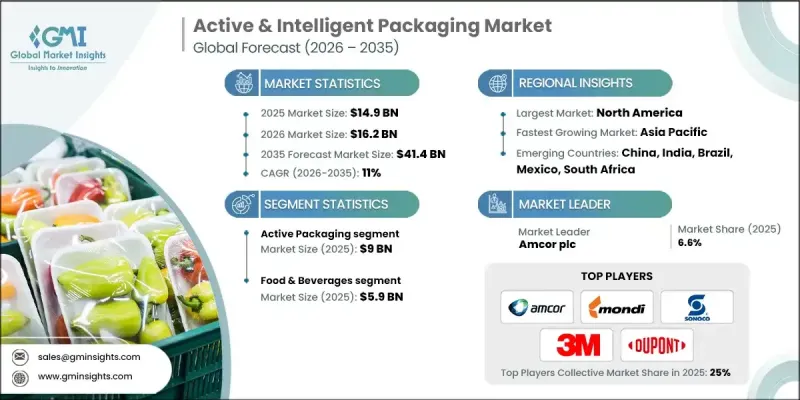

The Global Active & Intelligent Packaging Market was valued at USD 14.9 billion in 2025 and is estimated to grow at a CAGR of 11% to reach USD 41.4 billion by 2035.

The market is driven by rising consumer demand for longer shelf-life food products and increasing awareness about food safety and quality. Advanced materials and innovations in sensor technologies are enabling packaging that actively interacts with products while providing real-time information about freshness, spoilage, or environmental conditions. The growing consumption of packaged and processed foods worldwide is accelerating adoption, as consumers increasingly seek packaging that ensures product quality, prevents contamination, and offers transparency. Manufacturers and retailers are also embracing active and intelligent packaging to reduce waste, meet regulatory requirements, and enhance supply chain efficiency. This convergence of consumer preference, regulatory pressure, and technological advancement is positioning the market for sustained growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.9 Billion |

| Forecast Value | $41.4 Billion |

| CAGR | 11% |

The active packaging segment generated USD 9 billion in 2025. Active packaging is widely utilized for shelf-life extension, maintaining product quality, and preventing contamination through solutions such as oxygen scavengers, moisture absorbers, and antimicrobial agents. Its ability to directly interact with the packaged product provides a critical advantage across sectors like food, beverages, and pharmaceuticals. Companies are increasingly integrating these technologies to ensure product integrity, reduce spoilage, and comply with stringent safety standards, further fueling demand for active packaging solutions globally.

The food & beverages segment reached USD 5.9 billion in 2025. This sector is the primary adopter of active and intelligent packaging solutions, employing technologies like freshness indicators, oxygen scavengers, moisture absorbers, and antimicrobial films to maintain quality, extend shelf life, and ensure compliance with food safety regulations. Companies in this segment are increasingly deploying these solutions to minimize waste, improve inventory management, optimize supply chain efficiency, and meet rising consumer expectations for safe and fresh products. The segment's dominance is reinforced by ongoing investments in packaging innovation and automation by leading food and beverage manufacturers.

North America Active & Intelligent Packaging Market held a 31.7% share in 2025. The region benefits from a favorable business environment, strong investments in the food and beverage sector, advanced logistics infrastructure, and a robust research and development ecosystem. The U.S. market is supported by a strong network of packaging technology firms, research institutions, and innovation hubs that focus on active packaging, intelligent labeling, and sensor integration. These factors enable companies to rapidly deploy new packaging solutions, ensuring product safety, traceability, and enhanced consumer engagement, positioning North America as a global leader in this industry.

Key players in the Global Active & Intelligent Packaging Market include 3M Company, Mondi plc, Huhtamaki Oyj, CCL Industries Inc., Amcor plc, Multisorb Technologies, Inc., Sealed Air Corporation, Stora Enso Oyj, Dai Nippon Printing Co., Ltd., Avery Dennison Corporation, DuPont de Nemours, Inc., Coveris Holdings S.A., Sonoco Products Company, and Constantia Flexibles Group GmbH. Companies in the active and intelligent packaging market are adopting strategies to strengthen their position by investing heavily in research and development for next-generation packaging materials, sensors, and smart labeling technologies. Firms are forming strategic partnerships with food and beverage manufacturers, pharmaceutical companies, and retailers to integrate customized solutions into their supply chains. Expanding production facilities, acquiring innovative startups, and collaborating with technology providers are also key strategies to enhance product offerings.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Technology type trends

- 2.2.3 Functionality trends

- 2.2.4 Packaging material trends

- 2.2.5 End use industry trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Executive decision points

- 2.3.2 Critical Success Factors

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Food Safety and Quality

- 3.2.1.2 Growth of E-Commerce and Cold Chain Logistics

- 3.2.1.3 Advancements in Smart Sensors and RFID Technologies

- 3.2.1.4 Regulatory Focus on Food Waste Reduction and Traceability

- 3.2.1.5 Adoption of Sustainable and Biodegradable Packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Cost and Complexity of Advanced Packaging Technologies

- 3.2.2.2 Recycling and Regulatory Compliance Challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of Digital Technologies and IoT-Enabled Packaging

- 3.2.3.2 Expansion in Pharmaceutical and Healthcare Packaging Applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Measures

- 3.11 Global Consumer Sentiment Analysis

- 3.12 Patent Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit Margin

- 4.3.1.3 R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1 Product Range Breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global Footprint Analysis

- 4.3.3.2 Service Network Coverage

- 4.3.3.3 Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 1.1.1 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Active packaging

- 5.2.1 Oxygen scavengers

- 5.2.2 Moisture absorbers

- 5.2.3 Ethylene absorbers

- 5.2.4 Antimicrobial agents

- 5.2.5 Temperature control packaging

- 5.2.6 Flavor/odor absorbers

- 5.3 Intelligent packaging

- 5.3.1 Time-temperature indicators (TTIS)

- 5.3.2 RFID tags and QR codes

- 5.3.3 Freshness indicators

- 5.3.4 Gas sensors

- 5.3.5 Smart labels

- 5.3.6 Interactive packaging

Chapter 6 Market Estimates and Forecast, By Functionality, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Shelf-life extension

- 6.2.1 Moisture control

- 6.2.2 Oxygen control

- 6.2.3 Ethylene control

- 6.2.4 Antimicrobial protection

- 6.3 Quality assurance

- 6.3.1 Freshness indicators

- 6.3.2 Time-temperature indicators

- 6.4 Traceability & safety

- 6.4.1 RFID tags

- 6.4.2 QR codes

- 6.4.3 Tamper evident packaging

- 6.5 Consumer engagement

- 6.5.1 Interactive packaging

- 6.5.2 Smart labels

Chapter 7 Market Estimates and Forecast, By Packaging Material, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Plastics

- 7.2.1 Polyethylene (PE)

- 7.2.2 Polypropylene (PP)

- 7.2.3 Polyethylene Terephthalate (PET)

- 7.3 Paper & paperboard

- 7.3.1 Corrugated paperboard

- 7.3.2 Cartons

- 7.4 Glass

- 7.4.1 Bottles

- 7.4.2 Jars

- 7.5 Metals

- 7.5.1 Cans

- 7.5.2 Foils

- 7.6 Biodegradable materials

- 7.6.1 Starch-based materials

- 7.6.2 Polylactic acid (PLA)

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food & beverages

- 8.2.1 Perishable foods

- 8.2.2 Processed foods

- 8.2.3 Beverages

- 8.2.4 Bakery and confectionery

- 8.3 Pharmaceuticals & healthcare

- 8.3.1 Medicines

- 8.3.2 Medical devices

- 8.3.3 Nutraceuticals

- 8.4 Personal care & cosmetics

- 8.4.1 Skincare products

- 8.4.2 Haircare products

- 8.4.3 Cosmetics

- 8.5 Consumer electronics

- 8.5.1 Mobile phones

- 8.5.2 Wearable devices

- 8.5.3 Accessories

- 8.6 Logistics & supply chain

- 8.6.1 Warehousing

- 8.6.2 Transportation

- 8.6.3 Retail

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3M Company

- 10.2 Amcor Ltd.

- 10.3 Avery Dennison Corporation

- 10.4 CCL Industries Inc.

- 10.5 Coveris Holdings S.A.

- 10.6 Constantia Flexibles Group GmbH

- 10.7 Dai Nippon Printing Co., Ltd.

- 10.8 DuPont de Nemours, Inc.

- 10.9 Huhtamaki Oyj

- 10.10 Mondi plc

- 10.11 Multisorb Technologies, Inc.

- 10.12 Sealed Air Corporation

- 10.13 Sonoco Products Company

- 10.14 Stora Enso Oyj

主动式、智慧式和智慧包装市场:按材料、包装类型、最终用途产业和分销管道划分-2026-2032年全球市场预测主动式智慧包装市场:2026-2032年全球市场预测(按包装类型、材料、技术和应用划分)

主动式、智慧式和智慧包装市场:按材料、包装类型、最终用途产业和分销管道划分-2026-2032年全球市场预测主动式智慧包装市场:2026-2032年全球市场预测(按包装类型、材料、技术和应用划分) 智慧包装市场预测至2034年:按组件、包装类型、材料、功能、技术、最终用户和地区分類的全球分析

智慧包装市场预测至2034年:按组件、包装类型、材料、功能、技术、最终用户和地区分類的全球分析 主动式智慧包装市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034年预测

主动式智慧包装市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034年预测 2026年全球主动式智慧包装市场报告

2026年全球主动式智慧包装市场报告 主动式智慧包装市场规模、份额及成长分析(按类型、功能、技术、材料、等级、应用和地区划分)-2026-2033年产业预测

主动式智慧包装市场规模、份额及成长分析(按类型、功能、技术、材料、等级、应用和地区划分)-2026-2033年产业预测 主动式和智慧包装市场规模、份额和成长分析(按类型、技术、应用、通路和地区划分)—2026-2033年产业预测2032年主动与智慧包装市场预测:按材料、技术、应用和地区分類的全球分析主动、受控和智慧包装市场:2025-2030 年预测

主动式和智慧包装市场规模、份额和成长分析(按类型、技术、应用、通路和地区划分)—2026-2033年产业预测2032年主动与智慧包装市场预测:按材料、技术、应用和地区分類的全球分析主动、受控和智慧包装市场:2025-2030 年预测 主动和智慧包装:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

主动和智慧包装:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)