|

市场调查报告书

商品编码

1936624

氯硅烷市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Chlorosilane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

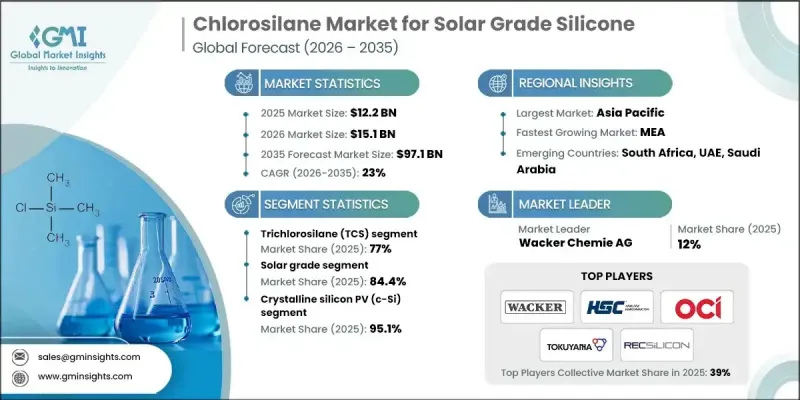

2025 年全球太阳能级硅酮用氯硅烷市场价值 122 亿美元,预计到 2035 年将达到 971 亿美元,年复合成长率为 23%。

氯硅烷作为生产超高纯度硅和用于光伏应用的硅酮的中间体发挥重要作用,这推动了市场成长。 2021年至2025年,硅酮的需求主要由本地供应满足,这得益于光伏製造能力的扩张和区域供应链一体化的增强。在此期间,光伏材料的化学成分基本上保持稳定,而技术优化提高了生产效率。多晶硅和光伏生产技术的进步带来了更严格的纯度要求,促使製造商对氯硅烷采用更严格的加工标准。这些改进带来了更高的材料一致性、更高的产量比率和更佳的电池效率。同时,能源安全问题和相关政策倡议正加速一体化光伏製造生态系统的发展。该地区正在加快氯硅烷、多晶硅、硅锭和组件生产的集中化,减少对跨境供应链的依赖,并提高长期供应安全。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 122亿美元 |

| 预测金额 | 971亿美元 |

| 复合年增长率 | 23% |

预计到2025年,太阳能级产品市占率将达到84.4%,2026年至2035年的复合年增长率将达到22.6%。高纯度太阳能级和电子级材料由于规格要求更为严格,价格也更高,而工业级材料的需求量依然庞大。太阳能和半导体技术的进步促使买家对杂质控制要求更加严格,从而导致长期供应协议和认证流程的加强,这有利于那些拥有良好业绩记录和可靠性的成熟製造商。

预计到2025年,晶体硅太阳能电池技术将占据95.1%的市场份额,并在2035年之前以22.8%的复合年增长率成长。由于单晶硅具有性能和成本优势,已成为主流,市场需求持续向单晶硅转移,这一转变推动了对高纯度氯硅烷原料的需求,并提高了对严格製程控制的要求。薄膜太阳能电池技术的需求仍微乎其微,氯硅烷的消耗与晶体硅产能的扩张和效率的提升密切相关。

预计到2025年,北美太阳能级硅酮用氯硅烷市场规模将达8.64亿美元。该地区的成长得益于先进的太阳能发电部署、持续的技术升级、强大的研发能力以及有利的政策环境。成熟的多晶硅一体化生产商群体持续确保氯硅烷需求的稳定,同时提升材料回收的经济效益与营运效率。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 太阳能发电能力快速成长

- 扩大脱碳和净零排放目标

- 高效率电池技术的进步

- 产业潜在风险与挑战

- 高资本和营运强度

- 严格的环境和安全法规

- 市场机会

- 扩大多晶硅回收利用及先进技术

- 在新兴市场建设国内太阳能製造

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 依产品类型分類的市场估算与预测,2022-2035年

- 三氯硅烷(TCS)

- 二氯硅烷(DCS)

- 四氯硅烷(STC)

- 一氯硅烷(MCS)

- 其他氯硅烷

第六章 依纯度等级分類的市场估算与预测,2022-2035年

- 太阳能级

- 电子级

- 工业级

7. 依最终用途分類的市场估计与预测,2022-2035 年

- 晶体硅太阳能电池(c-Si)

- 单晶硅

- 多晶硅

- 薄膜太阳能电池(与太阳能多晶硅製造製程的相关性有限)

- 硅基太阳能组件和系统周边设备

- 模组(层压、接线盒密封)

- 逆变器和电力电子装置(灌封、导热界面材料)

- 安装系统和追踪器(密封剂、涂层)

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- Wacker Chemie AG

- Hemlock Semiconductor(HSC)

- OCI Company Ltd.

- Tokuyama Corporation

- REC Silicon ASA

- Evonik Industries AG

- Dow

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- RoHM and Haas Electronic Materials(Dow)

- Mitsubishi Chemical Group

- Gelest, Inc.

The Global Chlorosilane Market for Solar Grade Silicone was valued at USD 12.2 billion in 2025 and is estimated to grow at a CAGR of 23% to reach USD 97.1 billion by 2035.

Market growth is driven by the critical role chlorosilanes play as intermediates in the production of ultra-high-purity silicon and silicone used in solar-grade applications. Between 2021 and 2025, demand for silicone was largely met through localized supply as photovoltaic manufacturing capacity expanded and supply chains became more regionally integrated. During this period, photovoltaic material chemistry remained largely stable, while manufacturing efficiency improved through technology optimization. Advancements in polysilicon and PV production have increased purity requirements, leading manufacturers to adopt tighter chlorosilane processing standards. These improvements have resulted in better material consistency, higher yields, and improved cell efficiency. At the same time, energy security concerns and policy initiatives are accelerating the development of integrated solar manufacturing ecosystems. Regions are increasingly co-locating chlorosilane, polysilicon, ingot, and module production to reduce reliance on cross-border supply chains and improve long-term supply stability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.2 Billion |

| Forecast Value | $97.1 Billion |

| CAGR | 23% |

The solar grade products segment accounted for 84.4% share in 2025 and is expected to grow at a CAGR of 22.6% from 2026 to 2035. Higher-purity solar and electronic grades command premium pricing due to stricter specifications, while industrial-grade materials remain driven by volume demand. As photovoltaic and semiconductor technologies advance, buyers are applying greater scrutiny to impurity control, reinforcing long-term supply agreements and qualification processes that favor established manufacturers with proven reliability.

The crystalline silicon photovoltaic technology segment held 95.1% share in 2025 and is projected to grow at a CAGR of 22.8% through 2035. Market demand continues to shift toward monocrystalline silicon, which has become the preferred standard due to performance and cost advantages. This transition is increasing the need for higher-purity chlorosilane inputs and stricter process control. Demand from thin-film photovoltaic technologies remains minimal, keeping chlorosilane consumption closely tied to crystalline silicon capacity expansion and efficiency improvements.

North America Chlorosilane Market for Solar Grade Silicone reached USD 864 million in 2025. Regional growth is supported by advanced photovoltaic deployments, ongoing technology upgrades, strong research capabilities, and supportive policy frameworks. A well-established base of integrated polysilicon producers continues to ensure stable chlorosilane demand while improving material recycling economics and operational efficiency.

Key participants operating in the Global Chlorosilane Market for Solar Grade Silicone include Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, Dow, Hemlock Semiconductor (HSC), Tokuyama Corporation, Momentive, OCI Company Ltd., REC Silicon ASA, Evonik Industries AG, Mitsubishi Chemical Group, Gelest, Inc., and Rohm and Haas Electronic Materials (Dow). Companies in the Chlorosilane Market for Solar Grade Silicone are strengthening their market position by investing in advanced purification technologies and tighter process control to meet rising purity requirements. Firms are expanding regional production capacity to support localized solar manufacturing ecosystems and reduce supply chain risks. Long-term supply agreements with photovoltaic and polysilicon manufacturers are being prioritized to secure stable demand. Players are also focusing on operational efficiency, recycling optimization, and yield improvement to enhance margins. Strategic collaborations with downstream partners, along with continuous R&D investment, are enabling manufacturers to align with evolving photovoltaic technologies while maintaining cost competitiveness and regulatory compliance across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Purity grade

- 2.2.4 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid solar PV capacity additions

- 3.2.1.2 Rising decarbonization and net-zero commitments

- 3.2.1.3 Advances in high-efficiency cell technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and operational intensity

- 3.2.2.2 Stringent environmental and safety regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of polysilicon recycling and upgrading

- 3.2.3.2 Emerging markets building domestic PV manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Trichlorosilane (TCS)

- 5.3 Dichlorosilane (DCS)

- 5.4 Tetrachlorosilane (STC)

- 5.5 Monochlorosilane (MCS)

- 5.6 Other chlorosilanes

Chapter 6 Market Estimates and Forecast, By Purity Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solar grade

- 6.3 Electronic grade

- 6.4 Industrial grade

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Crystalline silicon PV (c-Si)

- 7.2.1 Mono c-Si

- 7.2.2 Multi c-Si

- 7.3 Thin-film PV (limited relevance for solar-grade polysilicon chain)

- 7.4 Solar components and balance-of-system using silicones

- 7.4.1 Modules (lamination, junction box sealing)

- 7.4.2 Inverters and power electronics (potting, TIMs)

- 7.4.3 Mounting systems and trackers (sealants, coatings)

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Wacker Chemie AG

- 9.2 Hemlock Semiconductor (HSC)

- 9.3 OCI Company Ltd.

- 9.4 Tokuyama Corporation

- 9.5 REC Silicon ASA

- 9.6 Evonik Industries AG

- 9.7 Dow

- 9.8 Momentive

- 9.9 Shin-Etsu Chemical Co., Ltd.

- 9.10 RoHM and Haas Electronic Materials (Dow)

- 9.11 Mitsubishi Chemical Group

- 9.12 Gelest, Inc.

三氯硅烷全球市场规模、份额、趋势和成长分析报告(2026-2034)全球氯硅烷市场规模、份额、趋势和成长分析报告(2026-2034年)全球硅烷市场规模、份额、趋势和成长分析报告(2026-2034年)

三氯硅烷全球市场规模、份额、趋势和成长分析报告(2026-2034)全球氯硅烷市场规模、份额、趋势和成长分析报告(2026-2034年)全球硅烷市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球硅烷市场报告硅烷市场-2026-2031年预测

2026年全球硅烷市场报告硅烷市场-2026-2031年预测 三氯硅烷市场机会、成长要素、产业趋势分析及预测(2026年至2035年)

三氯硅烷市场机会、成长要素、产业趋势分析及预测(2026年至2035年) 电子级六氯二硅烷市场按产品类型、分销管道、应用和最终用途产业划分,全球预测(2026-2032年)电子级六甲基二硅氮烷市场:依纯度、形态、製造方法、应用及销售管道-2026-2032年全球预测电子级六甲基二硅氮烷(HMDS)市场按形态、纯度、晶圆尺寸、分销渠道和应用/最终用途划分-2026-2032年全球预测硅烷市场机会、成长要素、产业趋势分析及2026年至2035年预测

电子级六氯二硅烷市场按产品类型、分销管道、应用和最终用途产业划分,全球预测(2026-2032年)电子级六甲基二硅氮烷市场:依纯度、形态、製造方法、应用及销售管道-2026-2032年全球预测电子级六甲基二硅氮烷(HMDS)市场按形态、纯度、晶圆尺寸、分销渠道和应用/最终用途划分-2026-2032年全球预测硅烷市场机会、成长要素、产业趋势分析及2026年至2035年预测